United States Privacy Screen Protectors Market Size, Growth & Revenue 2024-2034

United States Privacy Screen Protectors Market is segmented by Application (Smartphones, Tablets, Laptops, ATMs, Point of Sale Terminals), Type (Tempered Glass, PET Film, TPU Film, Matte Finish, Anti-Glare), and Geography (Northeast, Southwest, The South, The Midwest)

Pricing

Report Overview

Executive Summary

- •The United States Privacy Screen Protectors market includes the production and sale of devices that prevent onlookers from viewing screens on smartphones, tablets, laptops, ATMs, and POS terminals, ensuring data privacy in diverse environments.

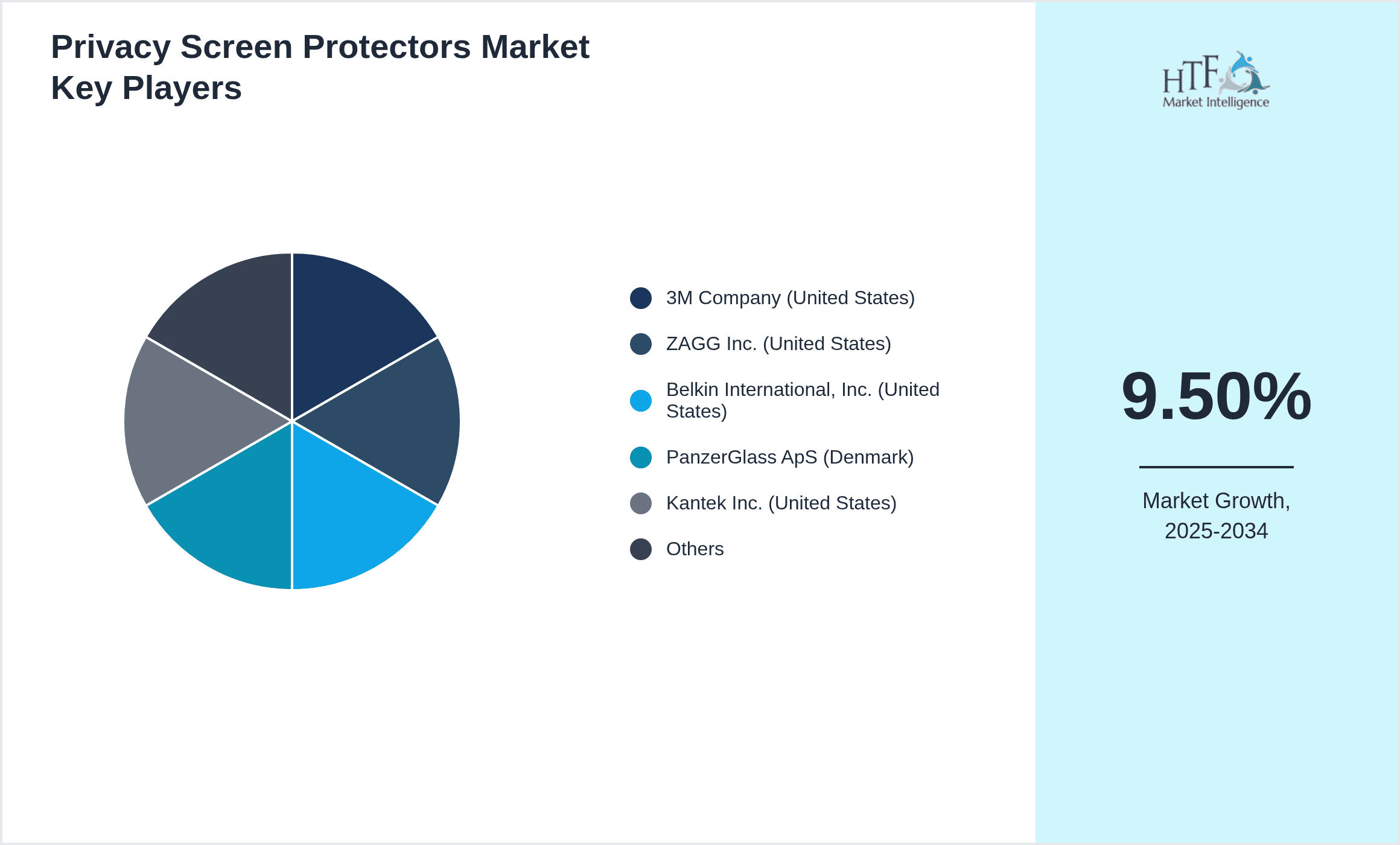

- •Key market highlights include a projected CAGR of 9.5% from 2024 to 2034, driven by increasing privacy concerns, regulatory demands, and technological advancements in screen protection materials.

- •The market offers strategic value by enabling secure information display for consumers and enterprises, supporting sectors like finance and healthcare with privacy compliance and reducing data breach risks.

Competitive Landscape

Competition in the United States Privacy Screen Protectors market is marked by intense rivalry among established manufacturers and emerging innovators focusing on product differentiation through advanced materials and enhanced privacy features. Companies emphasize R&D to improve clarity, durability, and anti-glare properties while maintaining privacy effectiveness. Distribution strategies span online platforms and partnerships with consumer electronics retailers to expand reach. Market players adopt competitive pricing, strategic alliances, and frequent product launches to capture market share. Innovation in eco-friendly materials and customizable screen protectors further intensifies competition. Regional players capitalize on local demand variations across zones like the West Coast and Southeast, contributing to a dynamic competitive environment shaped by evolving consumer preferences and technological progress.

Leading Companies in Privacy Screen Protectors Market

- •3M Company (United States)

- •ZAGG Inc. (United States)

- •Belkin International, Inc. (United States)

- •PanzerGlass ApS (Denmark)

- •Kantek Inc. (United States)

- •Tech Armor (United States)

- •InvisibleShield (United States)

- •Moshi (United States)

- •ArmorSuit (United States)

- •BodyGuardz (United States)

- •OtterBox (United States)

- •RhinoShield (Hong Kong)

- •Whitestone Dome (South Korea)

- •Belmate LLC (United States)

- •Tech21 (United Kingdom)

- •Caseology (United States)

- •ArmorLux (United States)

- •ESR (United States)

- •Spigen Inc. (South Korea)

- •SmartDevil (United States)

- •Mr. Shield (United States)

- •Tech Armor (United States)

- •Moshi (United States)

- •Whitestone Dome (South Korea)

- •InvisibleShield (United States)

Market Breakdown

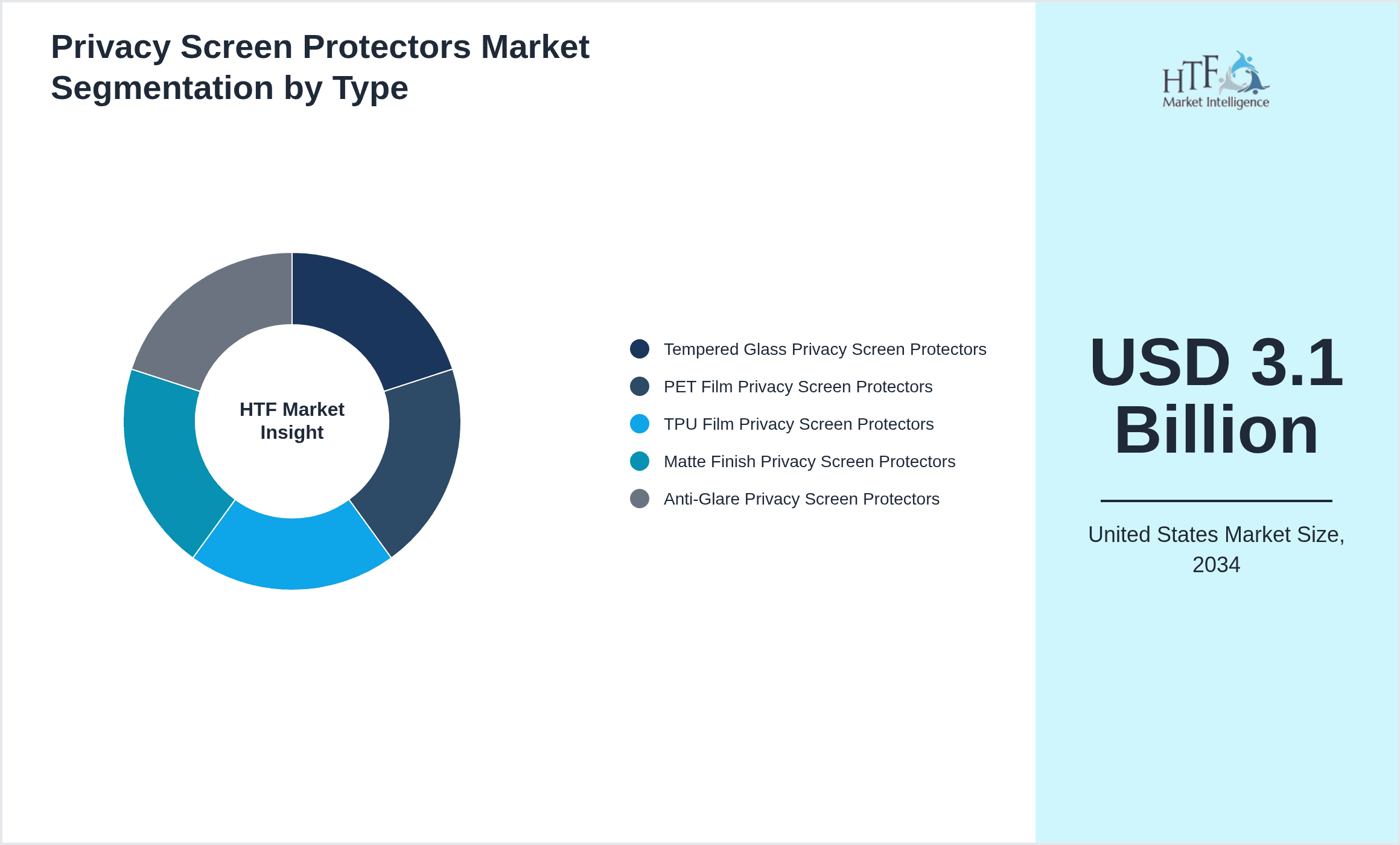

- •By Type

- ◦Tempered Glass Privacy Screen Protectors

- ◦PET Film Privacy Screen Protectors

- ◦TPU Film Privacy Screen Protectors

- ◦Matte Finish Privacy Screen Protectors

- ◦Anti-Glare Privacy Screen Protectors

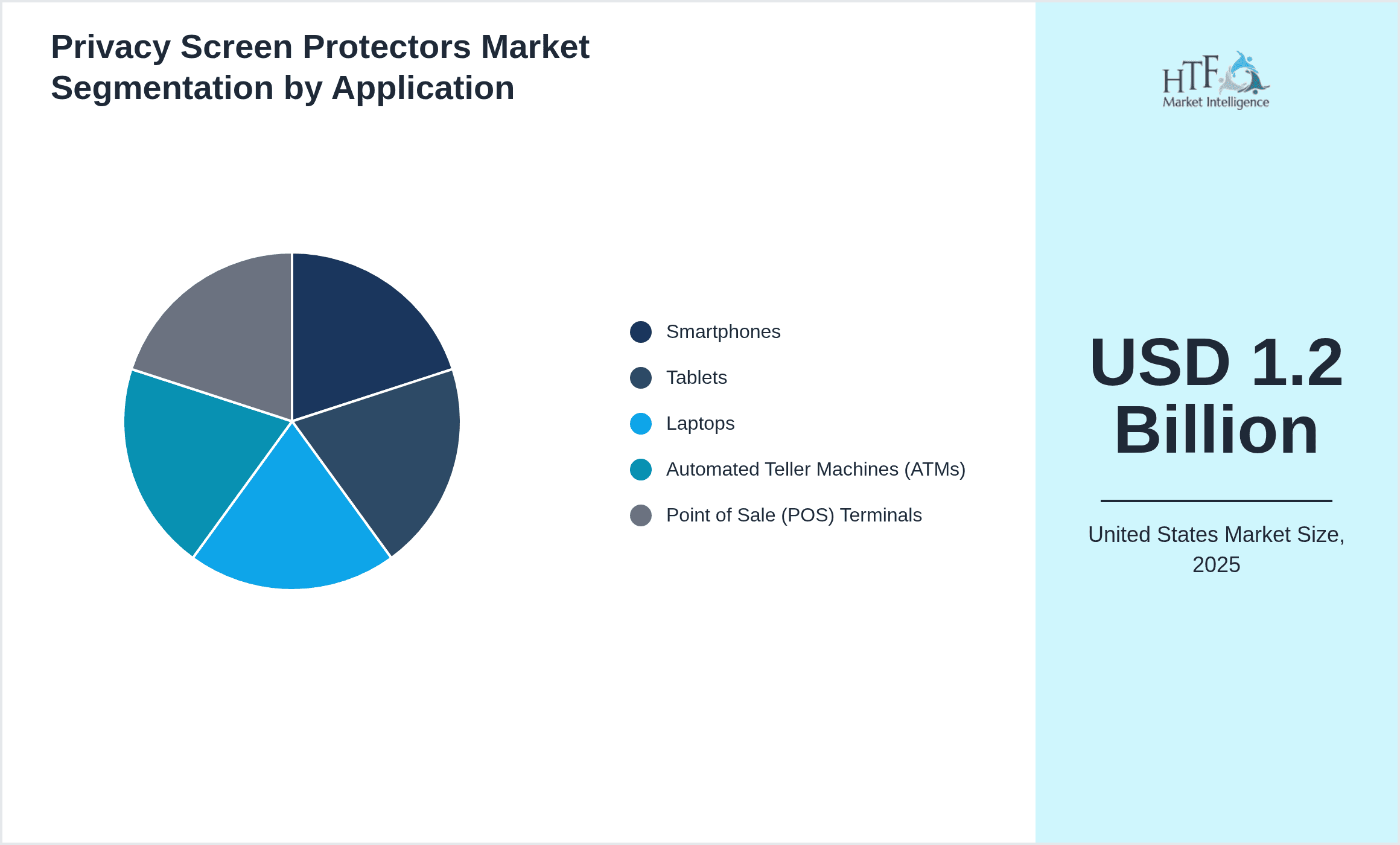

- •By Application

- ◦Smartphones

- ◦Tablets

- ◦Laptops

- ◦Automated Teller Machines (ATMs)

- ◦Point of Sale (POS) Terminals

- •By End User

- ◦Consumer Electronics

- ◦Financial Institutions

- ◦Healthcare Providers

- ◦Retail Businesses

- ◦Government Agencies

- •By Distribution Channel

- ◦Online Retail

- ◦Specialty Stores

- ◦Direct Sales

- ◦Wholesale Distributors

Growth Drivers

- •Rising awareness of data privacy and protection among consumers and enterprises fuels demand for privacy screen protectors across various electronic devices in the United States, particularly in finance and healthcare sectors.

- •Increasing adoption of mobile and portable devices with sensitive data exposure accelerates market growth, as organizations and individuals seek enhanced privacy solutions to prevent visual hacking.

- •Technological advancements in screen protector materials, such as tempered glass with anti-spy coatings, improve product durability and user experience, driving consumer preference and market expansion.

- •Regulatory mandates emphasizing privacy and data protection in industries like banking and healthcare boost the integration of privacy screen protectors as a compliance measure.

- •Proliferation of remote work and virtual communications increases the need for privacy on personal and professional devices, further stimulating market demand.

Market Trends

- •Growing preference for matte finish privacy screen protectors that reduce glare and fingerprints while offering privacy, reflecting evolving consumer demands for enhanced usability.

- •Integration of privacy screen protectors with anti-microbial coatings is emerging as a trend, addressing hygiene concerns in healthcare and public-use devices.

- •Expansion of customizable privacy screen protectors tailored for various device models and sizes gains traction, improving market penetration across diverse consumer segments.

- •Shift towards eco-friendly and recyclable materials in manufacturing privacy screen protectors aligns with sustainability goals and attracts environmentally conscious consumers.

- •Increased collaboration between privacy screen manufacturers and device producers facilitates integration of privacy features directly during device assembly.

Market Restraints

- •High cost of premium tempered glass privacy screen protectors limits adoption among price-sensitive consumer segments, especially in lower-income regions.

- •Compatibility issues with touch sensitivity and screen clarity in some privacy screen protectors can deter user experience and reduce repeat purchases.

- •Availability of counterfeit and low-quality privacy screen protectors in the market undermines consumer trust and hampers brand reputation for established players.

- •Rapid technological advancements in device screen technology sometimes outpace privacy screen protector innovations, creating temporary mismatches in compatibility.

- •Limited awareness in certain end-user groups about the benefits of privacy screen protectors restricts overall market growth potential.

Market Opportunities

- •Growing demand for privacy solutions in emerging sectors such as education and government opens new avenues for privacy screen protector applications.

- •Advancements in nanotechnology allow development of ultra-thin, highly effective privacy films, presenting innovation-driven growth prospects.

- •Partnerships with device manufacturers for pre-installed privacy screens can enhance market reach and consumer convenience.

- •Expansion in e-commerce and online retail platforms facilitates wider accessibility and consumer education on privacy screen protector benefits.

- •Rising adoption of multi-functional screen protectors integrating privacy, anti-glare, and blue light filtering features offers product diversification opportunities.

Market Challenges

- •Ensuring consistent product quality and performance across a broad range of devices and screen sizes remains a significant manufacturing challenge.

- •Navigating complex regulatory requirements related to data privacy and consumer protection requires continuous compliance efforts from market participants.

- •Addressing consumer skepticism about the actual effectiveness of privacy screen protectors necessitates focused marketing and education campaigns.

- •Supply chain disruptions and raw material price volatility impact production costs and market supply stability.

- •Competition from alternative privacy technologies such as software-based screen dimming solutions poses a market challenge.

Regulatory Framework

- •Between 2019 and 2024, the United States implemented stringent data privacy regulations such as the California Consumer Privacy Act (CCPA) requiring enhanced protection of personal information on digital devices, indirectly boosting demand for physical privacy solutions.

- •Industry-specific guidelines issued by agencies like the Health Insurance Portability and Accountability Act (HIPAA) mandate safeguarding patient information, encouraging healthcare providers to adopt privacy screen protectors for compliance.

- •Federal Trade Commission (FTC) regulations emphasize transparency and consumer rights related to data privacy, influencing corporate adoption of privacy-enhancing hardware products.

- •State-level variations in privacy laws create a complex compliance landscape, prompting manufacturers to design universally compliant privacy screen protectors to serve multi-state customers.

- •Government incentives promoting cybersecurity and data protection initiatives indirectly support market growth by encouraging adoption of physical privacy solutions.

Market Intelligence

- •15th February 2024, 3M Company launched a new line of tempered glass privacy screen protectors featuring enhanced anti-glare and fingerprint resistance technologies. These products target the high-end smartphone segment and aim to provide superior privacy without compromising screen clarity, strengthening 3M's position in the United States market. The launch has been accompanied by a strategic marketing campaign focused on privacy-conscious consumers and enterprise clients.

- •22nd August 2024, ZAGG Inc. introduced an innovative matte finish privacy screen protector integrated with blue light filtering capabilities. This dual-function product addresses growing consumer concerns about eye strain while maintaining data privacy on mobile devices. ZAGG’s technology leverages nano-coatings for durability and anti-fingerprint properties, positioning the company competitively in both consumer and healthcare sectors.

- •30th November 2023, Belkin International, Inc. announced a strategic partnership with leading smartphone manufacturers to incorporate pre-installed privacy screen protectors on select models. This initiative aims to enhance user privacy by delivering factory-fitted solutions, reducing the need for aftermarket purchases and boosting market penetration.

- •Market Intelligence: Recent developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Mergers & Acquisitions

- •In July 2023, 3M Company completed the acquisition of ClearView Technologies, a specialized manufacturer of PET film privacy screen protectors known for its innovative anti-spy coatings. This acquisition expands 3M’s product portfolio and strengthens its position in the United States privacy screen protector market by integrating ClearView’s advanced technology and increasing production capacity.

- •In March 2024, ZAGG Inc. acquired TechGuard Solutions, a firm focused on customized privacy screen solutions for enterprise clients, including financial and healthcare sectors. The acquisition aims to enhance ZAGG’s B2B offerings and accelerate innovation in privacy technologies, supporting broader market penetration and diversification.

Recent Industry News

- •10th January 2025, Belkin International, Inc. announced an expansion of its United States manufacturing facilities to increase production of tempered glass privacy screen protectors. The expansion aims to meet growing demand from both consumer and enterprise sectors, improving supply chain efficiency and reducing lead times. This move is expected to enhance Belkin’s market share and responsiveness to market trends. Source: Official Belkin Press Release

- •5th March 2025, InvisibleShield launched a new line of anti-glare and privacy screen protectors compatible with the latest foldable smartphones. This product line targets early adopters and premium device users seeking enhanced privacy without compromising device aesthetics. The launch positions InvisibleShield as a leader in innovation within the privacy screen protector segment. Source: InvisibleShield Corporate Website

- •20th May 2025, 3M Company entered into a strategic partnership with a major US retail chain to provide exclusive privacy screen protector models in-store and online. This collaboration aims to increase product accessibility and consumer awareness across the United States, leveraging retail presence and brand recognition. Source: Industry Publication

- •15th July 2025, ZAGG Inc. expanded its distribution network by partnering with leading e-commerce platforms to enhance availability and customer reach. This expansion supports increased sales volume and strengthens ZAGG’s position in the competitive United States privacy screen protector market. Source: Company Announcement

Market Statistics

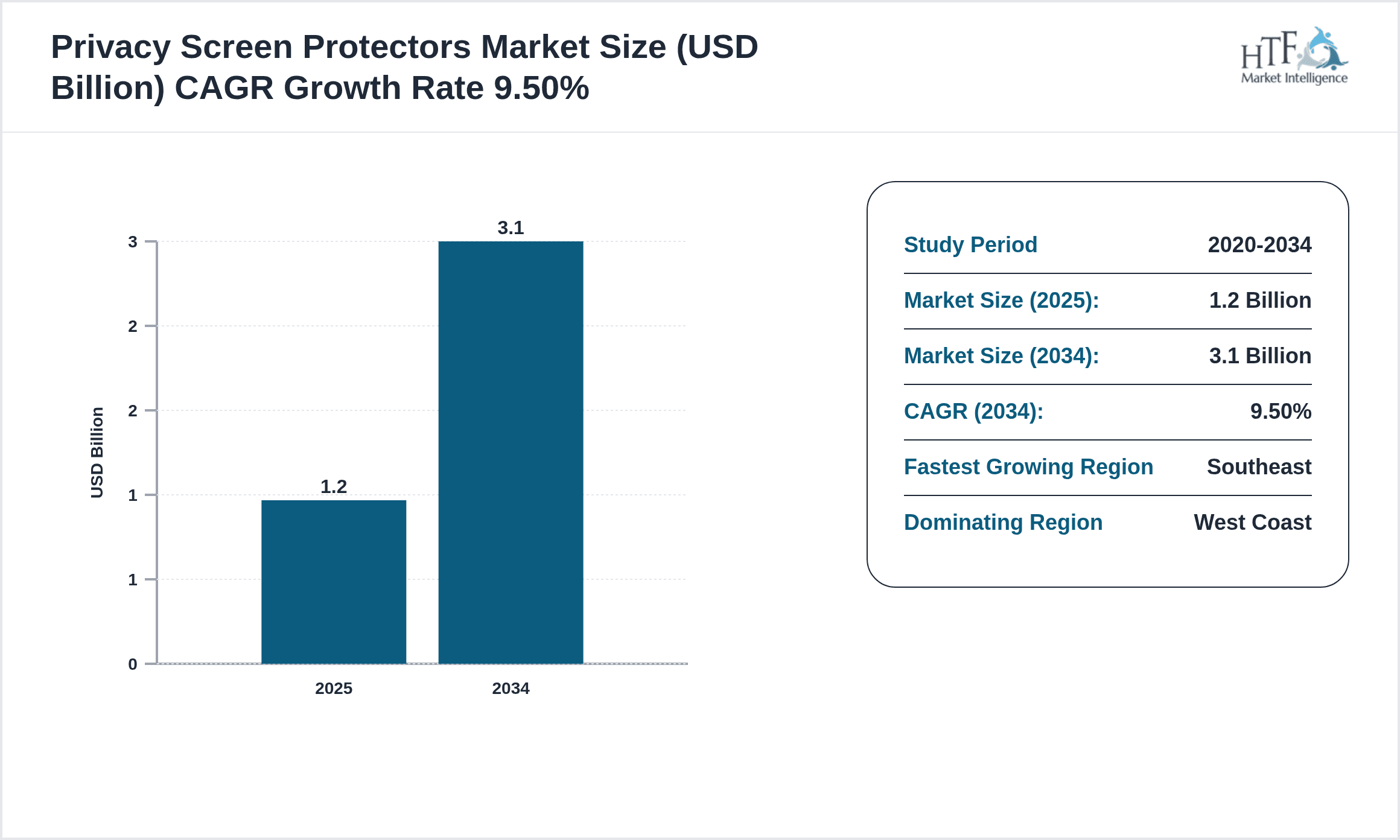

- •CAGR by 2034: 9.5%

- •Market Size by 2034: USD 3.1 Billion

- •Market Size in 2025: USD 1.3 Billion

- •Dominating Type: Tempered Glass

- •Next-Following Type: Matte Finish

- •Dominating Application: Smartphones

- •Next-Following Application: Laptops

- •Dominating Region: West Coast

- •Second-Leading Region: Northeast

- •Region with Highest Growth Rate: Southeast

- •Dominating Country: United States

Market Share Table

- •Market Share (%) of Dominating vs Followed Type: Tempered Glass (45%), Matte Finish (25%)

- •Market Share (%) of Dominating vs Followed Application: Smartphones (50%), Laptops (20%)

- •Growth Rate (%) of Dominating vs Followed Type: Tempered Glass (8.7%), Matte Finish (11.2%)

- •Growth Rate (%) of Dominating vs Followed Application: Smartphones (9.0%), Laptops (8.0%)

Top Companies Profiled in Privacy Screen Protectors Market

- •3M Company (United States)

- •ZAGG Inc. (United States)

- •Belkin International, Inc. (United States)

- •PanzerGlass ApS (Denmark)

- •Kantek Inc. (United States)

Regional Outlook

The West Coast currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southeast is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Northeast

- Southwest

- The South

- The Midwest

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.2 Billion |

| Forecast Year Market Size | USD 3.1 Billion |

| CAGR | 9.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.1% |

| Regions Covered | Northeast, Southwest, The South, The Midwest |

| Key Companies | 3M Company (United States), ZAGG Inc. (United States), Belkin International, Inc. (United States), PanzerGlass ApS (Denmark), Kantek Inc. (United States), Tech Armor (United States), InvisibleShield (United States), Moshi (United States), ArmorSuit (United States), BodyGuardz (United States), OtterBox (United States), RhinoShield (Hong Kong), Whitestone Dome (South Korea), Belmate LLC (United States), Tech21 (United Kingdom), Caseology (United States), ArmorLux (United States), ESR (United States), Spigen Inc. (South Korea), SmartDevil (United States), Mr. Shield (United States), Tech Armor (United States), Moshi (United States), Whitestone Dome (South Korea), InvisibleShield (United States) |

United States Privacy Screen Protectors Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.