Middle East Electrocardiogram Equipment Market Size, Growth & Revenue 2025-2034

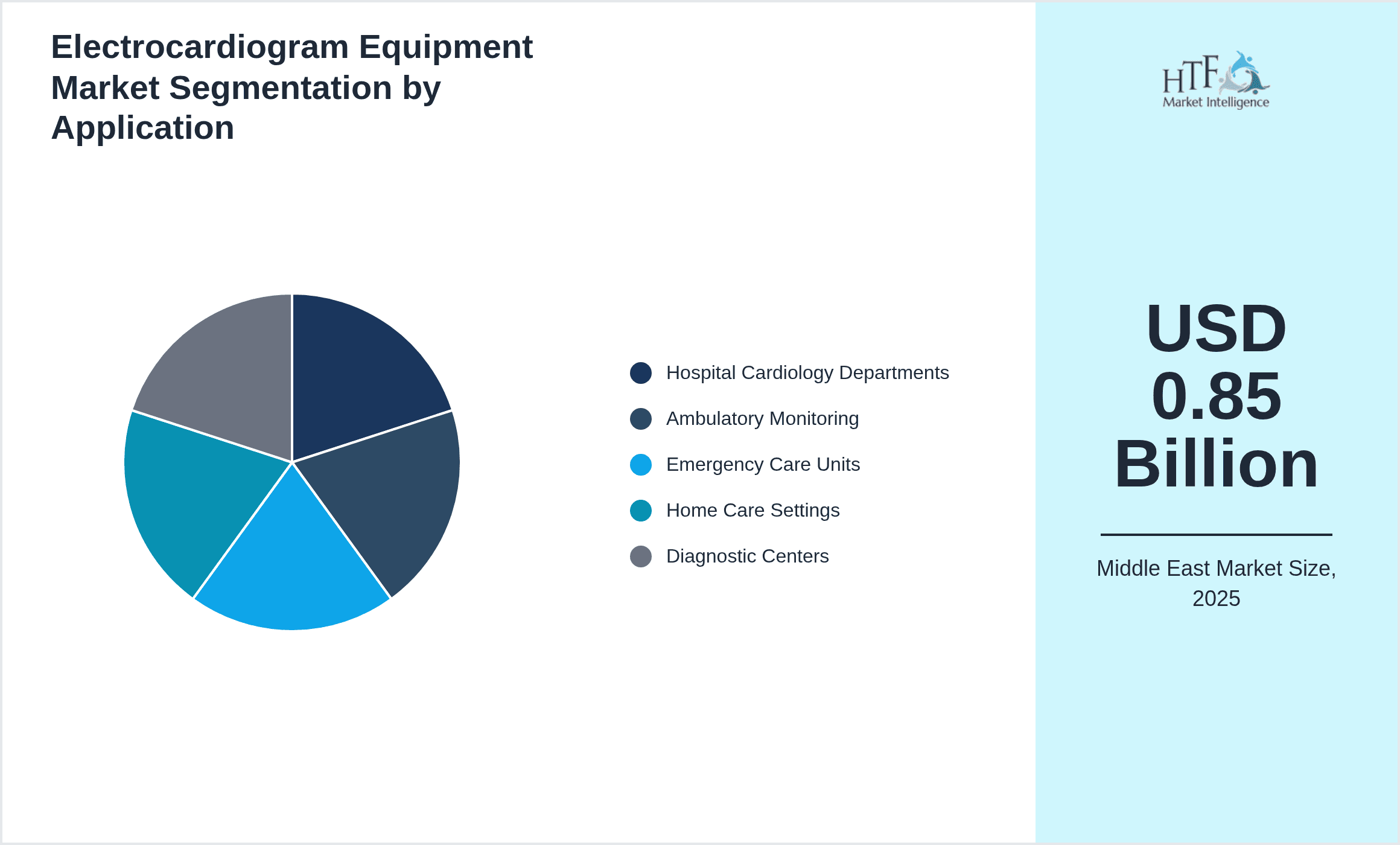

Middle East Electrocardiogram Equipment Market is segmented by Type (Resting ECG Devices, Stress ECG Devices, Holter Monitors, Event Monitors, Telemetry Systems), Application (Hospital Cardiology Departments, Ambulatory Monitoring, Emergency Care Units, Home Care Settings, Diagnostic Centers), End-User (Hospitals, Cardiology Clinics, Ambulatory Surgical Centers, Home Healthcare Providers, Diagnostic Laboratories), Technology (Wired ECG Systems, Wireless ECG Systems, AI-Enabled ECG Devices), and Geography (Turkey, Egypt, United Arab Emirates, Saudi Arabia, Israel, Others)

Pricing

Report Overview

Executive Summary

- •The Middle East Electrocardiogram Equipment market comprises devices that record cardiac electrical activity to diagnose heart conditions. The market covers Resting ECG, Stress ECG, Holter monitors, Event monitors, and Telemetry systems used in hospitals, ambulatory care, emergency services, home care, and diagnostic centers. Rising cardiovascular disease incidence and healthcare modernization drive market importance.

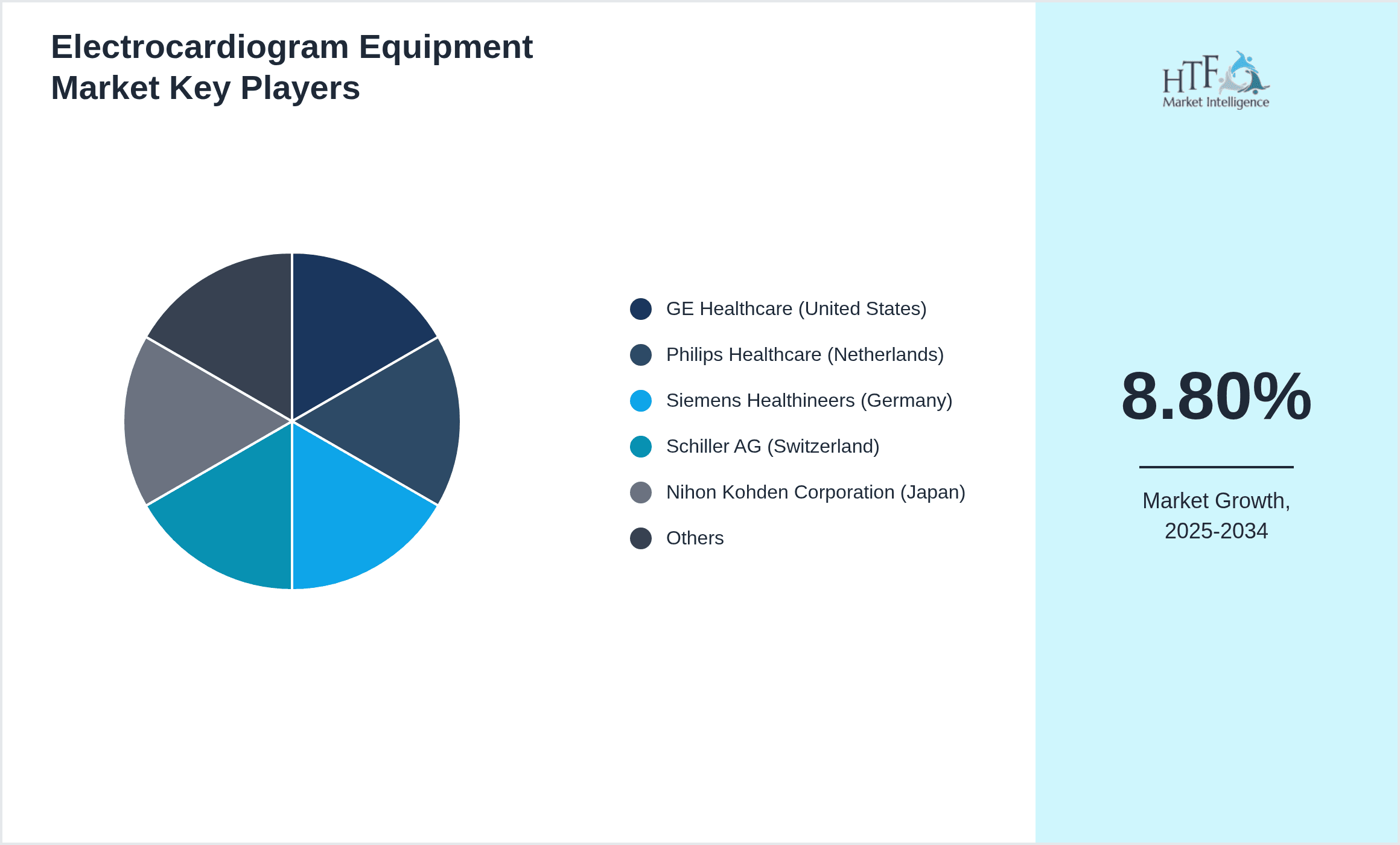

- •Key highlights include a base market size of USD 0.85 Billion in 2025 with a forecast to reach USD 1.78 Billion by 2034 at a CAGR of 8.8%. Saudi Arabia dominates with 34% market share, while the United Arab Emirates leads growth at 12.3% CAGR. Resting ECG leads product types; Telemetry Systems show fastest growth.

- •The market offers critical value by enabling early cardiac disease diagnosis, supporting clinical decision-making, and enhancing patient monitoring capabilities. It is strategically vital for healthcare providers, technology vendors, and policymakers seeking to improve cardiovascular health outcomes in the Middle East.

Competitive Landscape

Companies in the Middle East Electrocardiogram Equipment market utilize strategies such as innovation in wireless and telemetry technology, strategic partnerships with healthcare providers, and regional expansions to enhance presence. Product differentiation through integration of AI and cloud-based analytics supports competitive advantage. Collaborations with local distributors and government health sectors facilitate market penetration. Continuous R&D investments target improving device portability and diagnostic accuracy. Pricing strategies balance affordability with advanced features to capture diverse healthcare settings from tertiary hospitals to home care. Regulatory compliance and certifications ensure market access and trust. Mergers and acquisitions focus on consolidating technological capabilities and expanding regional footprints to sustain growth amid rising competition and evolving healthcare demands.

Leading Companies in Electrocardiogram Equipment Market

- •GE Healthcare (United States)

- •Philips Healthcare (Netherlands)

- •Siemens Healthineers (Germany)

- •Schiller AG (Switzerland)

- •Nihon Kohden Corporation (Japan)

- •Mindray Medical International (China)

- •Edan Instruments, Inc. (China)

- •Mortara Instrument, Inc. (United States)

- •BPL Medical Technologies (India)

- •Welch Allyn (United States)

- •Cardiac Science Corporation (United States)

- •Contec Medical Systems (China)

- •Schiller Middle East LLC (United Arab Emirates)

- •Spacelabs Healthcare (United States)

- •Fukuda Denshi Co., Ltd. (Japan)

- •AliveCor, Inc. (United States)

- •Nihon Kohden Middle East (United Arab Emirates)

- •Natus Medical Incorporated (United States)

- •Biocare Medical (United Arab Emirates)

- •Omron Healthcare (Japan)

Market Breakdown

- •By Type

- ◦Resting ECG Devices

- ◦Stress ECG Devices

- ◦Holter Monitors

- ◦Event Monitors

- ◦Telemetry Systems

- •By Application

- ◦Hospital Cardiology Departments

- ◦Ambulatory Monitoring

- ◦Emergency Care Units

- ◦Home Care Settings

- ◦Diagnostic Centers

- •By End-User

- ◦Hospitals

- ◦Cardiology Clinics

- ◦Ambulatory Surgical Centers

- ◦Home Healthcare Providers

- ◦Diagnostic Laboratories

- •By Technology

- ◦Wired ECG Systems

- ◦Wireless ECG Systems

- ◦AI-Enabled ECG Devices

Market Drivers

Increasing prevalence of cardiovascular diseases in the Middle East significantly propels demand for electrocardiogram equipment. Governments across Saudi Arabia, UAE, and Qatar invest heavily in upgrading healthcare infrastructure, expanding cardiology services, and adopting advanced diagnostic tools. Rising awareness of early cardiac condition detection among populations fuels ambulatory and home monitoring device sales. Recent launches of wireless and AI-integrated ECG devices by companies like GE Healthcare and Philips Healthcare enhance real-time diagnostics, driving adoption in emergency and outpatient care. For instance, Saudi Arabia’s Vision 2030 initiative includes large-scale healthcare modernization projects incorporating telemedicine and remote cardiac monitoring, boosting market growth. Additionally, the growing geriatric population with higher cardiac risk elevates the need for continuous monitoring solutions, further stimulating market expansion. Technological advancements offering portability and improved accuracy enable wider use across primary care and home settings, reinforcing sustained market momentum.

Market Trends

The Middle East electrocardiogram equipment market experiences rapid integration of wireless telemetry and AI-driven diagnostic platforms, enhancing cardiac health management. Telemetry systems with cloud connectivity offer seamless remote monitoring, aligning with digital health initiatives prominent in UAE and Saudi Arabia. Companies increasingly adopt AI algorithms for arrhythmia detection and predictive analytics, reducing diagnostic errors and enabling preventive care. Growing partnerships between technology providers and healthcare institutions facilitate deployment of comprehensive ECG solutions in ambulatory and emergency settings. The trend towards miniaturized wearable ECG devices expands patient-centric monitoring, supporting chronic disease management outside hospital environments. Additionally, government reimbursement policies in countries like Qatar incentivize adoption of advanced cardiac diagnostic devices. These technological and regulatory shifts facilitate market evolution toward personalized, data-driven cardiac care, promising improved clinical outcomes and operational efficiencies in the Middle East healthcare sector.

Market Opportunities

Expanding telehealth adoption in the Middle East presents significant opportunities for ECG equipment manufacturers to supply remote cardiac monitoring devices. Increasing investments in digital infrastructure by governments enable integration of AI-enabled ECG systems with electronic health records, enhancing diagnostic workflows. Untapped potential exists in home care ECG devices targeting elderly populations managing chronic heart conditions. Rising private healthcare spending and medical tourism growth in UAE and Saudi Arabia create demand for advanced diagnostic technologies in premium facilities. Companies innovating in portable and wireless ECG solutions gain competitive advantage by meeting emerging needs for continuous patient monitoring during pandemic recovery phases. Collaborations between local distributors and global technology firms facilitate market penetration in emerging Middle Eastern countries with developing healthcare ecosystems. These factors collectively provide a fertile landscape for product diversification, geographic expansion, and technology-driven value propositions in the Middle East electrocardiogram equipment market.

Market Challenges

High costs associated with advanced ECG devices and maintenance restrain adoption in certain Middle Eastern countries with budget limitations. Variability in regulatory requirements across the region complicates market entry and product approvals, increasing time-to-market and compliance costs for manufacturers. Limited awareness among rural and underserved populations restricts demand for ambulatory and home monitoring ECG solutions. Supply chain disruptions caused by geopolitical tensions and global semiconductor shortages affect device availability and lead times. Companies face challenges in integrating legacy hospital systems with modern ECG technologies, hindering seamless data interoperability. For example, smaller clinics in Oman and Kuwait report difficulties in adopting AI-enabled ECG systems due to infrastructure gaps. Furthermore, shortage of trained cardiac technicians limits effective utilization of sophisticated ECG equipment, impacting service quality. These challenges necessitate strategic investments in education, regulatory harmonization, and cost-effective technology development to sustain market growth.

Regulatory Framework

The Middle East electrocardiogram equipment market operates under stringent regulatory frameworks established in the last five years to ensure device safety and efficacy. Countries like Saudi Arabia have implemented the Saudi Food and Drug Authority’s medical device regulations aligning with international standards such as ISO 13485. The UAE’s Ministry of Health enforces comprehensive medical device registration processes mandating clinical evaluation and quality certifications. Qatar introduced updated health technology assessment guidelines in 2021, requiring robust clinical evidence for ECG device approvals. These regulations promote patient safety and encourage manufacturers to maintain high compliance levels. Regional harmonization efforts across Gulf Cooperation Council countries aim to streamline approvals and facilitate cross-border trade of cardiac diagnostic equipment. Compliance with data privacy laws, particularly for telemetry systems transmitting patient information, further shapes product design and deployment strategies in the Middle East.

Recent Industry Insights

Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Recent Merger and Acquisition

Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Saudi Arabia currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Turkey

- Egypt

- United Arab Emirates

- Saudi Arabia

- Israel

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.85 Billion |

| Forecast Year Market Size | USD 1.78 Billion |

| CAGR | 8.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.5% |

| Scope of Report | Market is segmented by Type (Resting ECG Devices, Stress ECG Devices, Holter Monitors, Event Monitors, Telemetry Systems), Application (Hospital Cardiology Departments, Ambulatory Monitoring, Emergency Care Units, Home Care Settings, Diagnostic Centers), End-User (Hospitals, Cardiology Clinics, Ambulatory Surgical Centers, Home Healthcare Providers, Diagnostic Laboratories), Technology (Wired ECG Systems, Wireless ECG Systems, AI-Enabled ECG Devices) |

| Regions Covered | Turkey, Egypt, United Arab Emirates, Saudi Arabia, Israel, Others |

| Key Companies | GE Healthcare (United States), Philips Healthcare (Netherlands), Siemens Healthineers (Germany), Schiller AG (Switzerland), Nihon Kohden Corporation (Japan), Mindray Medical International (China), Edan Instruments, Inc. (China), Mortara Instrument, Inc. (United States), BPL Medical Technologies (India), Welch Allyn (United States), Cardiac Science Corporation (United States), Contec Medical Systems (China), Schiller Middle East LLC (United Arab Emirates), Spacelabs Healthcare (United States), Fukuda Denshi Co., Ltd. (Japan), AliveCor, Inc. (United States), Nihon Kohden Middle East (United Arab Emirates), Natus Medical Incorporated (United States), Biocare Medical (United Arab Emirates), Omron Healthcare (Japan) |

Middle East Electrocardiogram Equipment Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.