GCC Medical Superabsorbent Polymer Market - Outlook 2025-2034

GCC Medical Superabsorbent Polymer Market is segmented by Type (Cross-linked Polyacrylate, Cross-linked Polyacrylamide, Sodium Polyacrylate, Other SAP Types), Application (Medical Dressings, Surgical Pads, Incontinence Products, Wound Care, Other Medical Applications), End User (Hospitals, Clinics, Home Healthcare, Specialty Care Centers), Distribution Channel (Direct Sales, Distributors, Online Platforms, Medical Supply Chains), and Geography (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates)

Pricing

Report Overview

Executive Summary

- •The GCC Medical Superabsorbent Polymer market includes high-performance polymeric materials specialized for fluid absorption in medical uses such as wound care, surgical dressings, and incontinence products, essential for patient hygiene and treatment efficacy.

- •The market is witnessing robust growth driven by rising healthcare investments, increasing chronic disease prevalence, and technological innovations in polymer formulations enhancing absorbency and biocompatibility.

- •These polymers offer critical value to healthcare providers and manufacturers by improving medical product performance, reducing infection risks, and supporting expanding healthcare infrastructure across GCC countries.

Competitive Landscape

The GCC Medical Superabsorbent Polymer market is characterized by intense competition among global and regional manufacturers focusing on innovation, product differentiation, and strategic partnerships. Companies invest heavily in R&D to develop polymers with enhanced absorption capacity and biocompatibility tailored to evolving medical needs. Market players leverage regional distribution networks and collaborations with healthcare providers to strengthen their market presence. Competitive strategies include expanding product portfolios, improving cost efficiencies, and navigating regulatory compliance. The rivalry fosters continuous product improvements, while new entrants drive competitive pressures, compelling established players to sustain technological leadership and responsive customer service to maintain and grow market share.

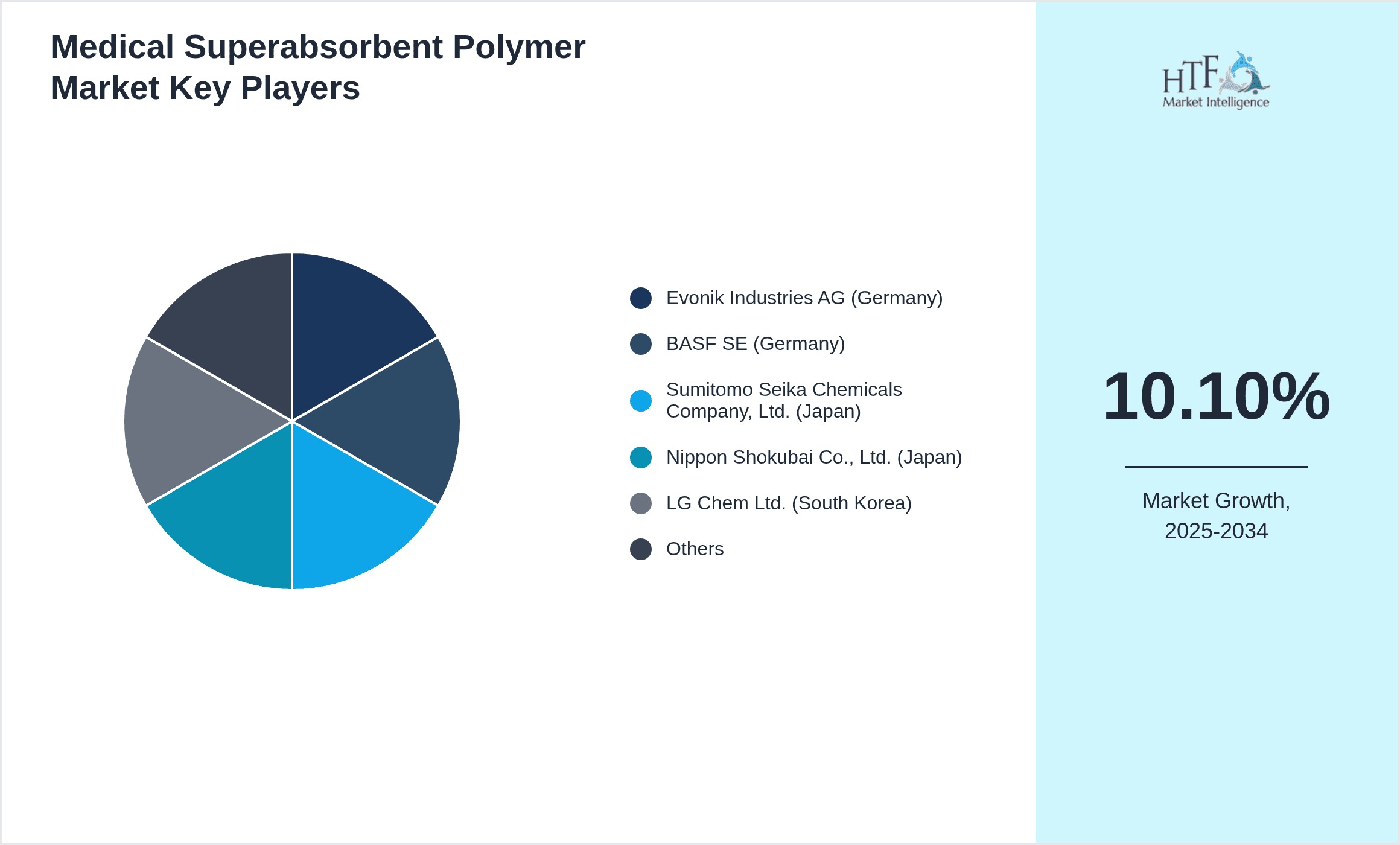

Leading Companies in GCC Medical Superabsorbent Polymer Market

- •Evonik Industries AG (Germany)

- •BASF SE (Germany)

- •Sumitomo Seika Chemicals Company, Ltd. (Japan)

- •Nippon Shokubai Co., Ltd. (Japan)

- •LG Chem Ltd. (South Korea)

- •FMC Corporation (United States)

- •Kuraray Co., Ltd. (Japan)

- •Asahi Kasei Corporation (Japan)

- •Reliance Industries Limited (India)

- •Sinopec Corporation (China)

- •Formosa Plastics Corporation (Taiwan)

- •Mitsui Chemicals, Inc. (Japan)

- •Nouryon (Netherlands)

- •Wanhua Chemical Group Co., Ltd. (China)

- •Shandong Dongyue Chemical Co., Ltd. (China)

- •Huntsman Corporation (United States)

- •Sumitomo Chemical Co., Ltd. (Japan)

- •Suzhou Huasu New Materials Co., Ltd. (China)

- •Honeywell International Inc. (United States)

- •Clariant AG (Switzerland)

- •Dow Inc. (United States)

- •Toray Industries, Inc. (Japan)

- •CIPLA Ltd. (India)

- •Hubei Yihua Group Co., Ltd. (China)

- •BASF Middle East FZE (UAE)

Market Breakdown

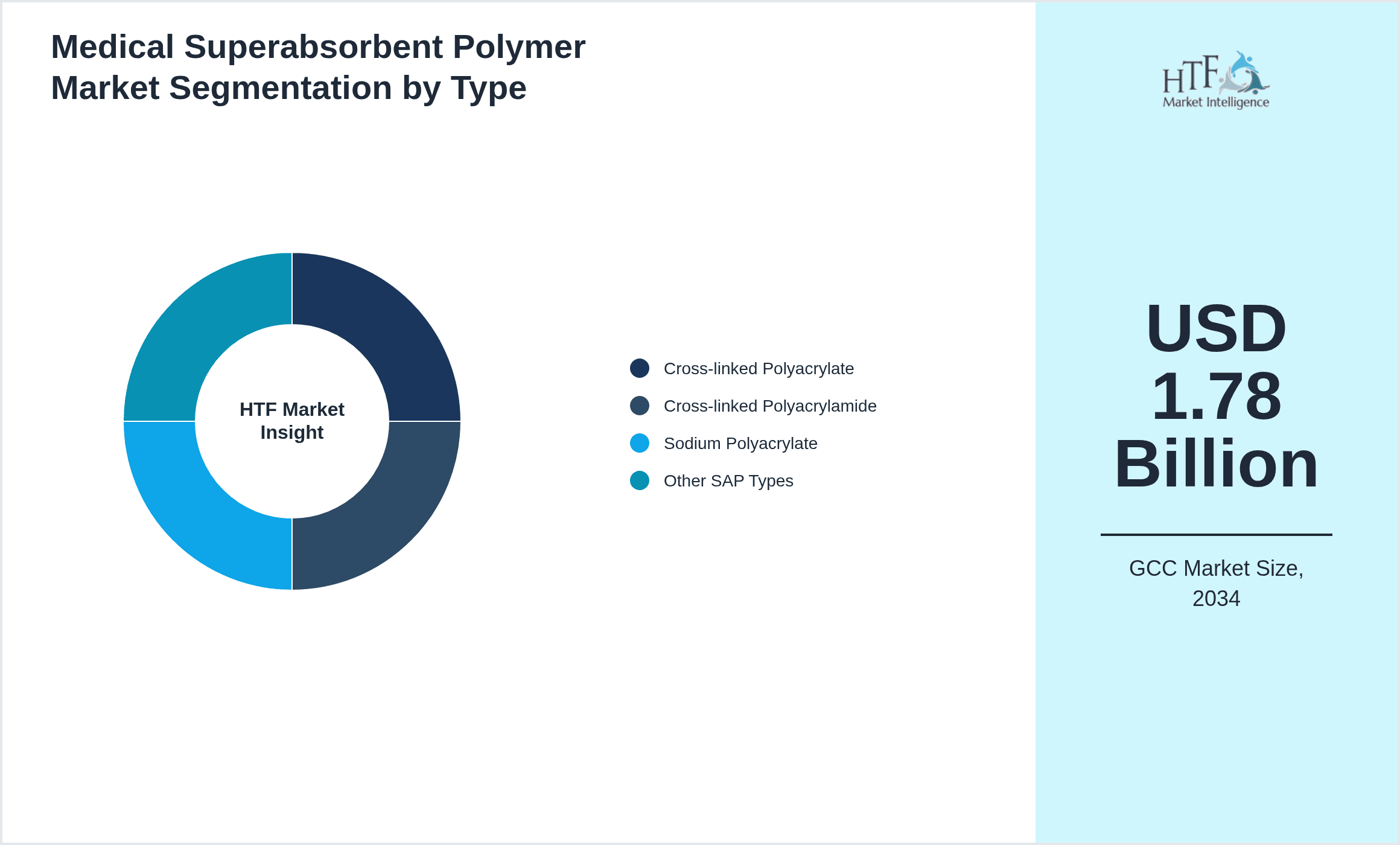

- •By Type

- ◦Cross-linked Polyacrylate

- ◦Cross-linked Polyacrylamide

- ◦Sodium Polyacrylate

- ◦Other SAP Types

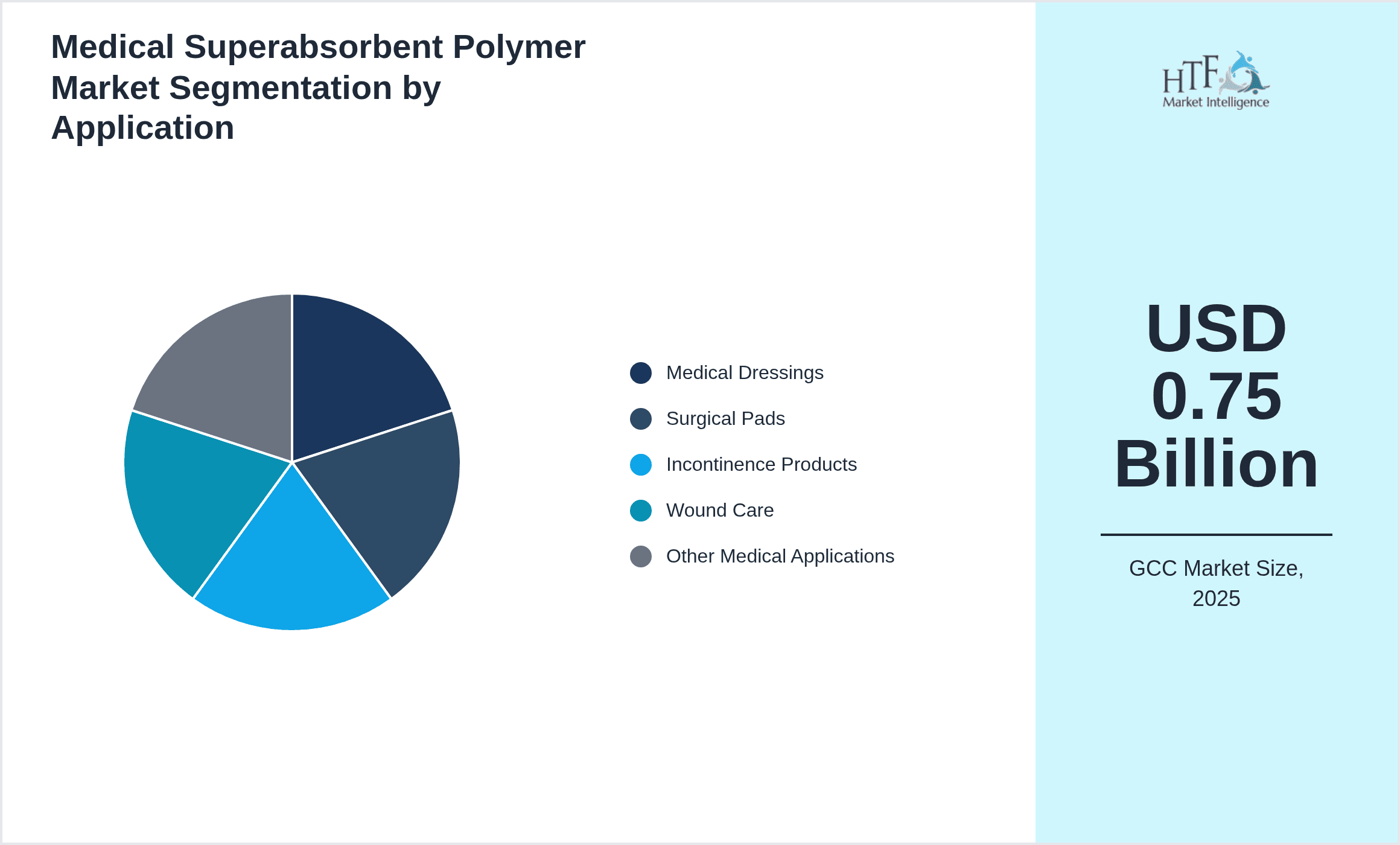

- •By Application

- ◦Medical Dressings

- ◦Surgical Pads

- ◦Incontinence Products

- ◦Wound Care

- ◦Other Medical Applications

- •By End User

- ◦Hospitals

- ◦Clinics

- ◦Home Healthcare

- ◦Specialty Care Centers

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

- ◦Medical Supply Chains

Growth Drivers

- •Increasing prevalence of chronic diseases such as diabetes and obesity in GCC countries is driving demand for advanced wound care products incorporating superabsorbent polymers, boosting market growth significantly.

- •Expanding healthcare infrastructure and rising government healthcare expenditure in the GCC enhance accessibility and adoption of medical SAPs across hospitals and clinics region-wide.

- •Technological advancements improving absorption efficiency, biocompatibility, and polymer sustainability are enabling manufacturers to introduce innovative SAP-based medical products, attracting broader healthcare usage.

- •Growing geriatric population in the GCC increases demand for incontinence products and wound dressings, positively impacting the superabsorbent polymer market segment.

- •Rising awareness about infection control and hygiene standards in medical settings fuels adoption of high-quality SAP materials, reinforcing market expansion.

Market Trends

- •Shift towards eco-friendly and biodegradable superabsorbent polymers is gaining momentum, driven by environmental regulations and sustainability goals within GCC healthcare sectors.

- •Integration of nanotechnology in SAP formulations is emerging to enhance antimicrobial properties and fluid retention, setting new benchmarks for medical applications.

- •Increasing partnerships between polymer manufacturers and medical device companies in the GCC enable customized SAP solutions tailored to regional healthcare needs.

- •Digital transformation and e-commerce expansion in the GCC facilitate broader distribution and faster adoption of SAP-based medical consumables.

- •Government-led initiatives promoting local manufacturing of medical polymers aim to reduce import dependency and stimulate regional industry growth.

Market Restraints

- •High production costs of advanced superabsorbent polymers limit affordability and slow adoption, especially among smaller healthcare providers in the GCC region.

- •Stringent regulatory approval processes for new SAP formulations delay product launches and increase compliance expenses for manufacturers.

- •Limited recycling infrastructure for SAP waste in GCC countries raises environmental concerns restricting large-scale adoption of non-biodegradable variants.

- •Dependence on imports for raw materials exposes the market to supply chain disruptions and price volatility impacting production stability.

- •Lack of widespread awareness among end users regarding benefits of high-performance SAP medical products results in slower market penetration in some GCC areas.

Market Opportunities

- •Rising investments in healthcare infrastructure modernization across GCC countries open new avenues for SAP manufacturers to expand product offerings and market reach.

- •Development of biodegradable and eco-friendly SAPs presents opportunities to capture environmentally conscious healthcare segments and comply with emerging regulations.

- •Increasing demand for home healthcare and outpatient wound care solutions creates potential for SAP-based products tailored for remote patient use.

- •Collaborations with regional healthcare providers for customized SAP formulations can enhance product differentiation and customer loyalty.

- •Expansion into adjacent markets such as veterinary healthcare and hygiene products offers diversification paths for SAP manufacturers in the GCC.

Market Challenges

- •Navigating complex regulatory landscapes across different GCC countries requires significant resources and expertise, posing challenges for market entrants.

- •Ensuring consistent product quality and meeting diverse healthcare standards regionally complicate manufacturing and supply chain management.

- •Competition from low-cost imports and generic SAP products pressures pricing and profitability margins for premium manufacturers.

- •Addressing environmental concerns related to SAP disposal demands innovation in recycling and material lifecycle management.

- •Limited skilled workforce specialized in polymer technology within the GCC restricts rapid technology transfer and adoption.

Regulatory Framework

- •Between 2023 and 2025, GCC countries have increasingly aligned medical material regulations with international standards such as ISO 10993 for biocompatibility, ensuring safety and efficacy of superabsorbent polymers used in medical devices.

- •Recent mandates require enhanced traceability and documentation for SAP-based medical products, improving quality control and post-market surveillance within the region.

- •Environmental regulations targeting reduction of non-biodegradable medical waste have led to incentives for developing eco-friendly SAP alternatives in GCC markets.

- •The GCC Health Ministers Council has introduced unified guidelines to streamline approval processes for innovative medical polymers, facilitating faster market entry across member states.

- •Government initiatives promoting local manufacturing and technology transfer include subsidies and tax benefits for companies investing in SAP production within the GCC.

Industry Insights

The GCC Medical Superabsorbent Polymer market has seen strategic product launches aimed at enhancing wound care efficacy. In March 2024, a leading polymer manufacturer introduced a new biodegradable SAP variant optimized for surgical pads, improving absorption and environmental impact. In October 2023, a regional healthcare supplier partnered with a global SAP producer to launch advanced incontinence products tailored for the GCC demographic, combining comfort and high absorbency. These innovations reflect the market’s focus on sustainability and patient-centric design, aligning with regional healthcare modernization efforts and increasing demand for high-quality medical consumables.

Mergers & Acquisitions

- •In June 2024, a major global chemical company acquired a regional SAP manufacturer based in the UAE to expand its footprint in the GCC medical polymers market. This acquisition enhances the acquiring company’s production capabilities and distribution networks, enabling faster delivery of customized superabsorbent polymers to healthcare providers across the Gulf region. The deal strategically positions the company to capitalize on rising healthcare investments and increasing demand for advanced medical SAPs, supporting long-term growth objectives in a high-potential regional market.

- •In November 2023, a leading Japanese SAP producer entered into a joint venture with a Saudi Arabian healthcare materials firm, combining technological expertise with local market knowledge. This collaboration focuses on developing innovative SAP products tailored for GCC medical applications, including wound care and incontinence management. The joint venture aims to accelerate product development cycles, enhance regional manufacturing capacity, and strengthen compliance with GCC regulatory frameworks, fostering competitive advantages in a rapidly evolving market landscape.

Recent Industry News

- •15th January 2025, BASF Middle East FZE announced the launch of a new line of cross-linked polyacrylate superabsorbent polymers designed specifically for medical dressings in the GCC. These SAPs feature enhanced absorption rates and improved biocompatibility, targeting hospitals and clinics in Saudi Arabia and UAE. The product launch aligns with regional healthcare modernization plans and environmental guidelines promoting sustainable materials. BASF aims to strengthen its leadership in the GCC medical polymer market by addressing growing demand and regulatory requirements. Source: BASF Official Press Release

- •5th March 2025, Evonik Industries AG expanded its manufacturing facility in Dubai to increase production capacity of superabsorbent polymers for surgical pads and wound care applications. The expansion includes investment in advanced polymerization technology to improve product consistency and reduce environmental footprint. This move supports rising consumption in the GCC healthcare market and enables faster delivery to regional clients. Evonik plans to collaborate with local healthcare suppliers to customize SAP products for specific medical needs. Source: Evonik Corporate Announcement

- •20th May 2025, Sumitomo Seika Chemicals launched an innovative SAP variant with integrated antimicrobial properties targeting incontinence products used in GCC elder care facilities. This formulation reduces infection risks and enhances patient comfort. The company partnered with regional medical device manufacturers to co-develop new product lines, aiming to capture growing market segments driven by the aging population. The launch reflects increasing emphasis on patient safety and product differentiation in the GCC healthcare sector. Source: Industry Publication

- •30th July 2025, LG Chem Ltd. announced a strategic partnership with a UAE-based healthcare distributor to expand the reach of its sodium polyacrylate SAP products across the Gulf region. This partnership focuses on enhancing supply chain efficiency and introducing next-generation SAP solutions tailored for medical dressings and wound care. The collaboration is part of LG Chem’s regional growth strategy to leverage GCC healthcare infrastructure investments and sustainability initiatives. Source: LG Chem Press Release

Regional Outlook

The Saudi Arabia currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Bahrain

- Kuwait

- Oman

- Qatar

- Saudi Arabia

- United Arab Emirates

| Feature | Details |

|---|---|

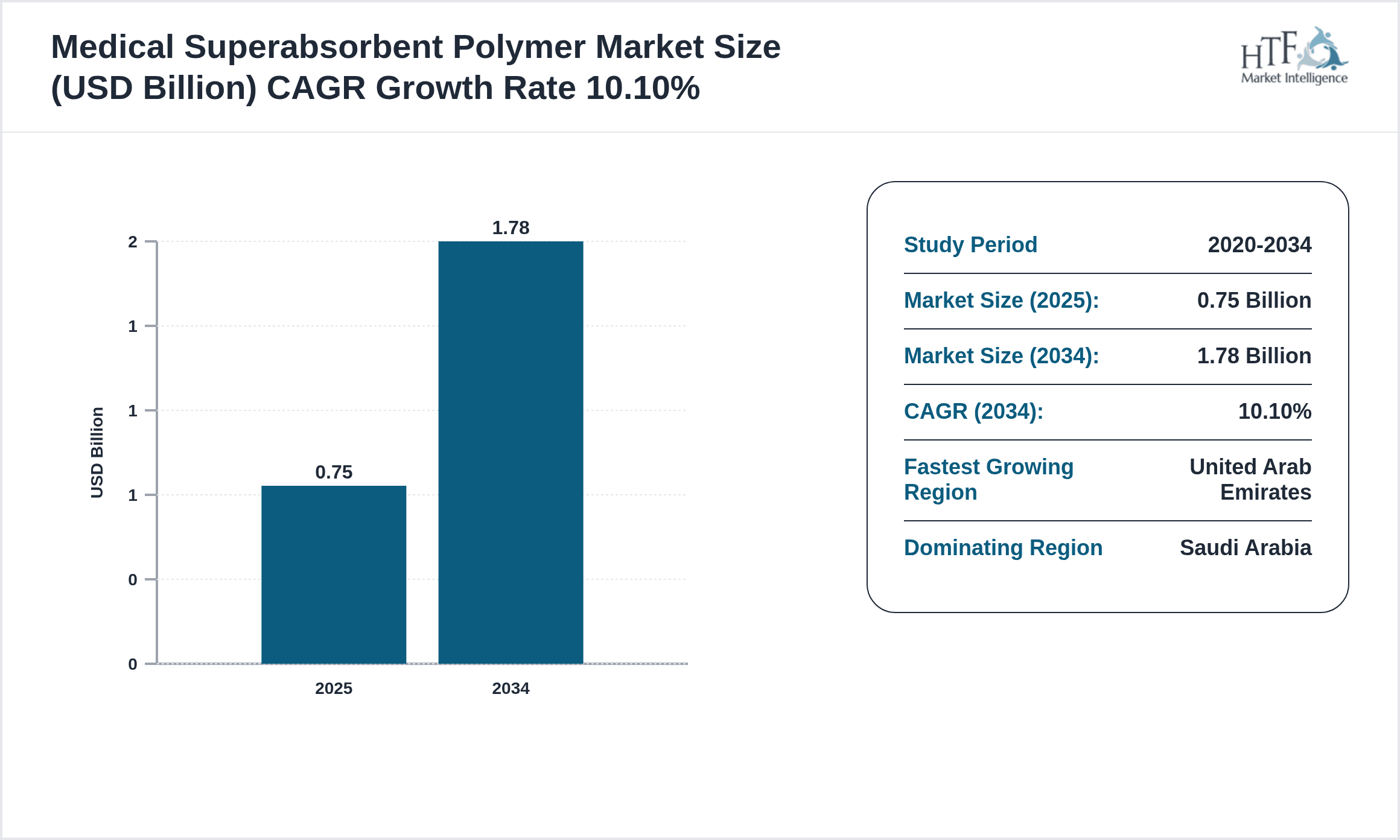

| Base Year Market Size | USD 0.75 Billion |

| Forecast Year Market Size | USD 1.78 Billion |

| CAGR | 10.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.7% |

| Scope of Report | Market is segmented by Type (Cross-linked Polyacrylate, Cross-linked Polyacrylamide, Sodium Polyacrylate, Other SAP Types), Application (Medical Dressings, Surgical Pads, Incontinence Products, Wound Care, Other Medical Applications), End User (Hospitals, Clinics, Home Healthcare, Specialty Care Centers), Distribution Channel (Direct Sales, Distributors, Online Platforms, Medical Supply Chains) |

| Regions Covered | Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates |

| Key Companies | Evonik Industries AG (Germany), BASF SE (Germany), Sumitomo Seika Chemicals Company, Ltd. (Japan), Nippon Shokubai Co., Ltd. (Japan), LG Chem Ltd. (South Korea), FMC Corporation (United States), Kuraray Co., Ltd. (Japan), Asahi Kasei Corporation (Japan), Reliance Industries Limited (India), Sinopec Corporation (China), Formosa Plastics Corporation (Taiwan), Mitsui Chemicals, Inc. (Japan), Nouryon (Netherlands), Wanhua Chemical Group Co., Ltd. (China), Shandong Dongyue Chemical Co., Ltd. (China), Huntsman Corporation (United States), Sumitomo Chemical Co., Ltd. (Japan), Suzhou Huasu New Materials Co., Ltd. (China), Honeywell International Inc. (United States), Clariant AG (Switzerland), Dow Inc. (United States), Toray Industries, Inc. (Japan), CIPLA Ltd. (India), Hubei Yihua Group Co., Ltd. (China), BASF Middle East FZE (UAE) |

GCC Medical Superabsorbent Polymer Market - Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.