United States DRAM Aging Repair Equipment Market - Outlook 2025-2034

United States DRAM Aging Repair Equipment Market is segmented by Type (Automated Repair Systems, Manual Repair Tools, Inspection Equipment, Thermal Aging Chambers, Diagnostic Software), Application (Memory Testing, Failure Analysis, Repair Process, Quality Control, Research & Development), End User (Semiconductor Manufacturers, Outsourced Repair Services, Research Institutions), Distribution Channel (Direct Sales, Distributors, Online Platforms), and Geography (Northeast, Southwest, The South, The Midwest)

Pricing

Report Overview

Executive Summary

- •The United States DRAM Aging Repair Equipment Market consists of specialized tools and systems used for detecting, testing, and repairing aging-related defects in DRAM memory devices during manufacturing and post-production phases.

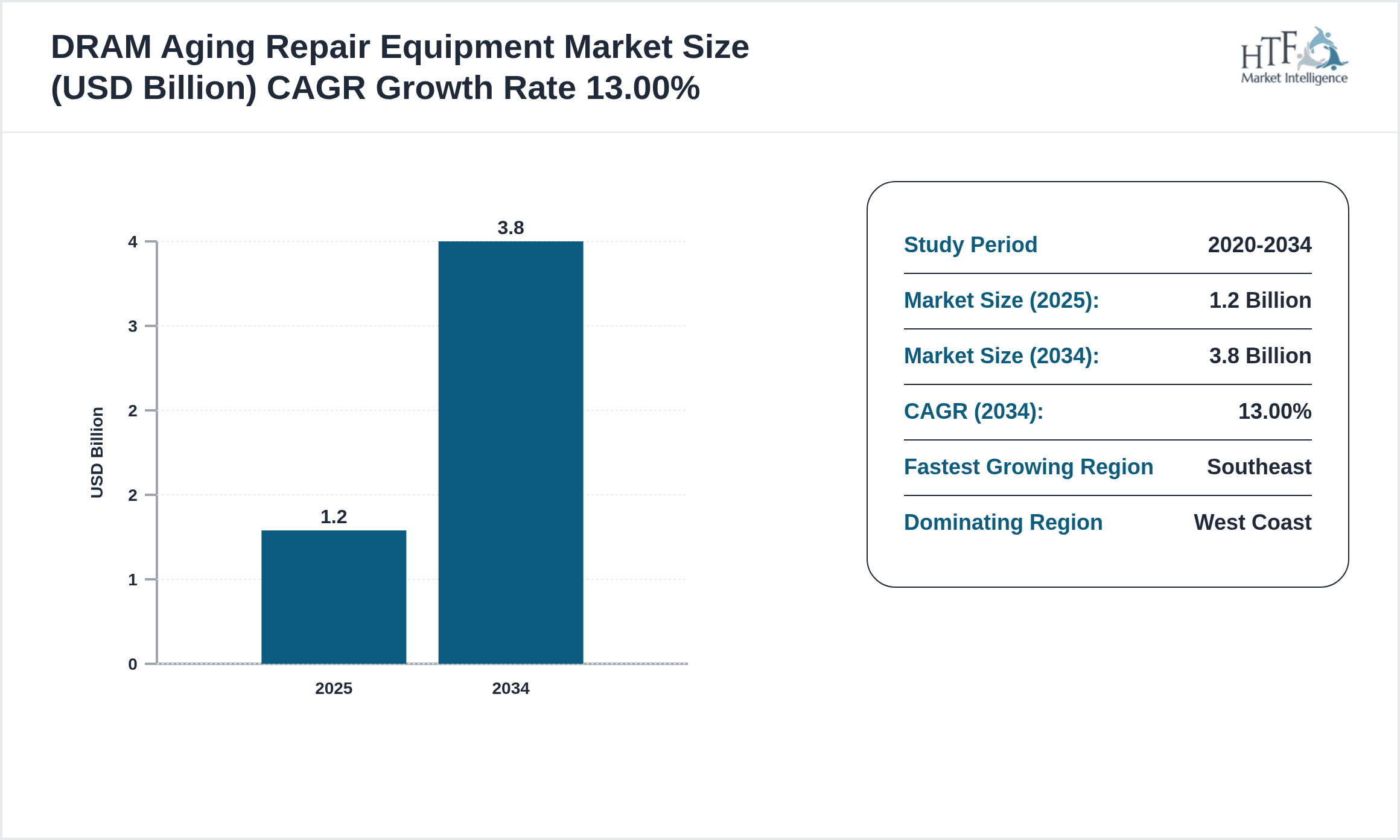

- •The market is characterized by rapid technological advancements such as automated repair systems and thermal aging chambers, which enhance repair precision and device reliability, contributing to market growth with a projected CAGR of 13.0% through 2034.

- •This market serves key stakeholders including semiconductor manufacturers, outsourced repair service providers, and research institutions, playing a vital role in improving DRAM yield, performance, and operational lifespan in the competitive U.S. semiconductor industry.

Competitive Landscape

The United States DRAM Aging Repair Equipment Market features intense competition driven by innovation, advanced technology adoption, and strategic partnerships. Leading companies focus on developing automated and precise repair technologies, leveraging software integration for diagnostics and repair optimization. The rivalry centers on delivering high-yield solutions with reduced turnaround times and enhanced accuracy. Market players invest heavily in R&D to differentiate products and expand service capabilities, while alliances and collaborations with semiconductor manufacturers strengthen market positioning. The competitive landscape is also shaped by emerging startups offering niche solutions and the increasing demand for customization tailored to evolving DRAM architectures. Overall, the market is marked by continuous technological evolution, aggressive marketing strategies, and a strong emphasis on customer-centric product development.

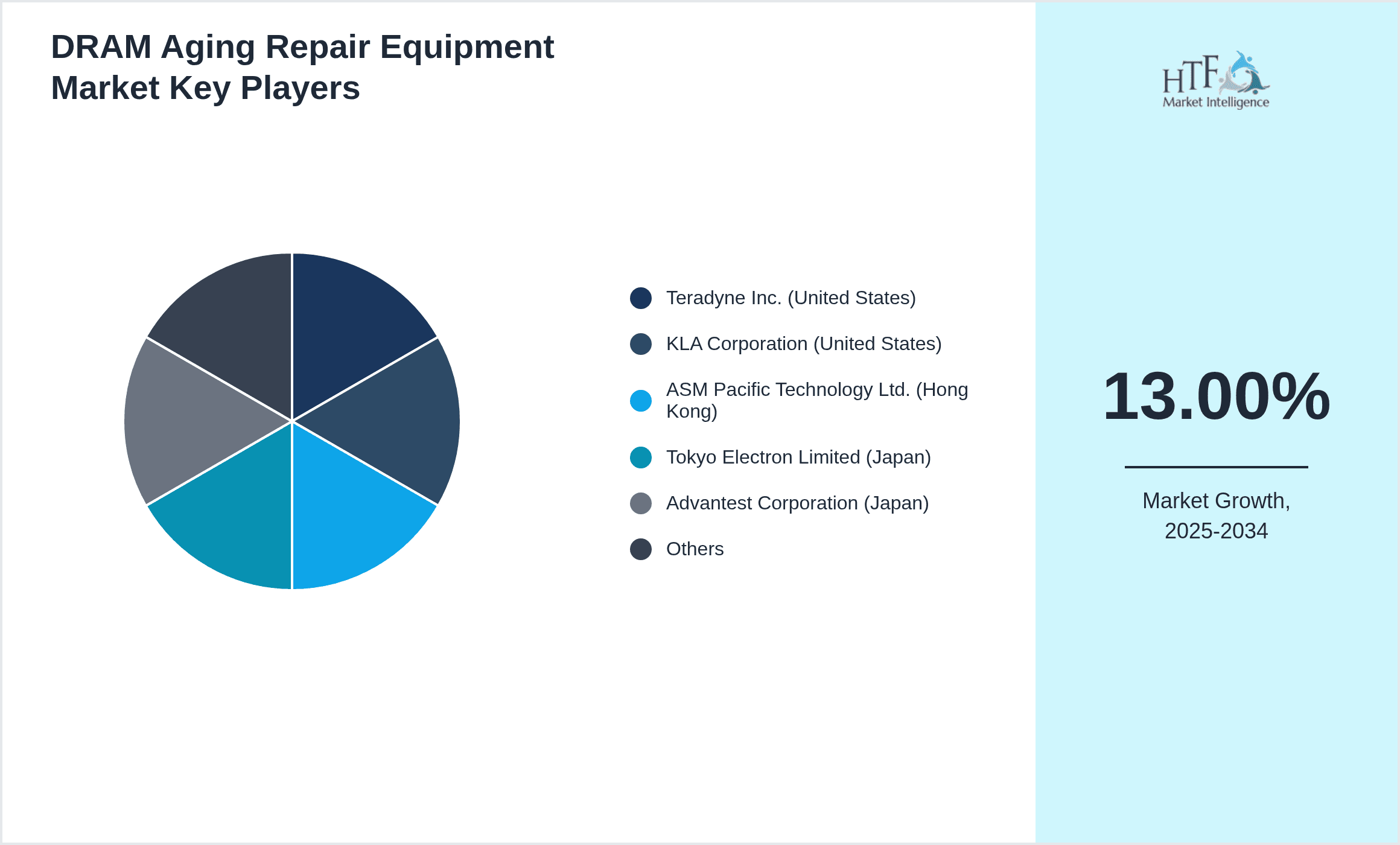

Leading Companies in DRAM Aging Repair Equipment Market

- •Teradyne Inc. (United States)

- •KLA Corporation (United States)

- •ASM Pacific Technology Ltd. (Hong Kong)

- •Tokyo Electron Limited (Japan)

- •Advantest Corporation (Japan)

- •Lam Research Corporation (United States)

- •SCREEN Holdings Co., Ltd. (Japan)

- •Hitachi High-Technologies Corporation (Japan)

- •Onto Innovation Inc. (United States)

- •Nordson Corporation (United States)

- •Ultratech, Inc. (United States)

- •Applied Materials, Inc. (United States)

- •Veeco Instruments Inc. (United States)

- •FormFactor, Inc. (United States)

- •MKS Instruments, Inc. (United States)

- •Cohu, Inc. (United States)

- •ASM International N.V. (Netherlands)

- •Advantest America, Inc. (United States)

- •FormFactor Asia Pacific, Inc. (Singapore)

- •Teradyne GmbH (Germany)

- •Hitachi High-Tech Analytical Science America, Inc. (United States)

- •Nikon Corporation (Japan)

- •Screen Semiconductor Solutions Co., Ltd. (Japan)

- •Tokyo Seimitsu Co., Ltd. (Japan)

- •Xcerra Corporation (United States)

Market Breakdown

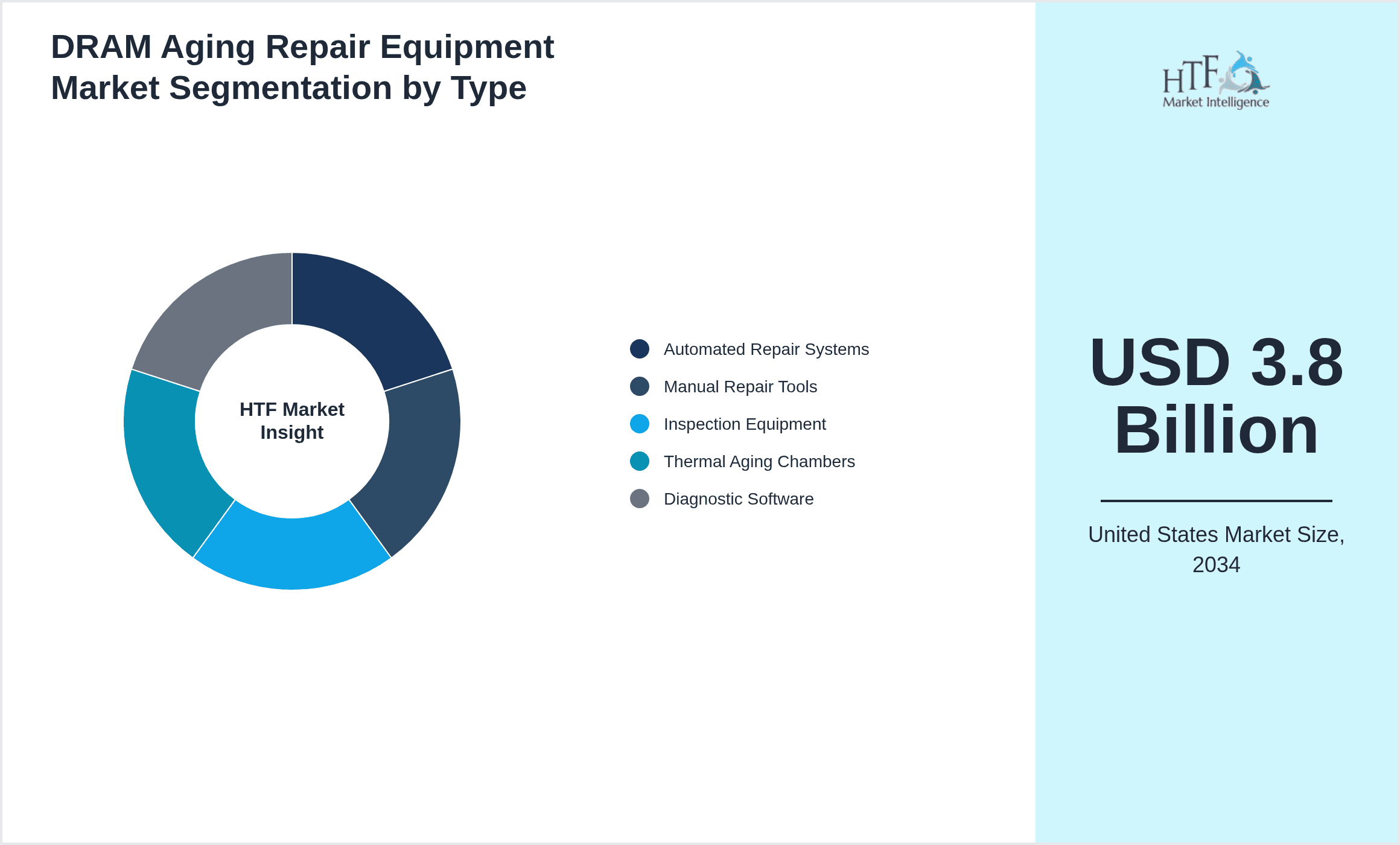

- •By Type

- ◦Automated Repair Systems

- ◦Manual Repair Tools

- ◦Inspection Equipment

- ◦Thermal Aging Chambers

- ◦Diagnostic Software

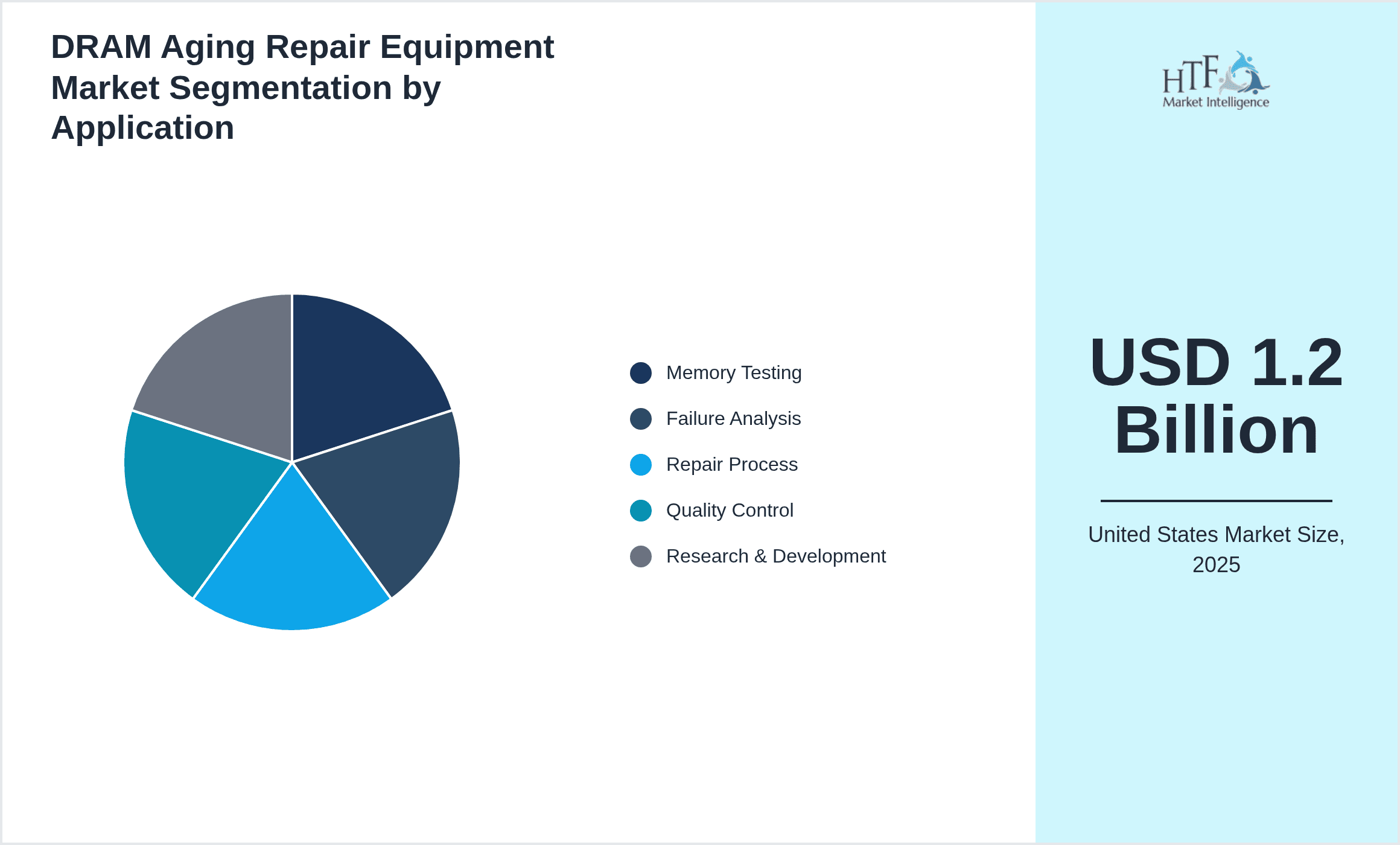

- •By Application

- ◦Memory Testing

- ◦Failure Analysis

- ◦Repair Process

- ◦Quality Control

- ◦Research & Development

- •By End User

- ◦Semiconductor Manufacturers

- ◦Outsourced Repair Services

- ◦Research Institutions

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

Growth Drivers

- •Rising demand for high-performance DRAM in consumer electronics and data centers drives the need for advanced aging repair equipment to improve memory reliability and lifespan.

- •Technological advancements in automated repair systems enhance repair accuracy and reduce processing time, fueling market growth.

- •Increasing semiconductor manufacturing activities and the push for yield enhancement in the United States stimulate equipment adoption.

- •Growing investments in R&D for new memory architectures necessitate specialized aging repair solutions to address emerging challenges.

- •Stringent quality control standards in semiconductor fabrication require precise aging repair equipment to minimize defects and failures.

Market Trends

- •Integration of AI and machine learning in diagnostic software enables predictive maintenance and more efficient aging repair processes.

- •Shift towards fully automated repair systems reduces human error and enhances throughput in DRAM aging repair workflows.

- •Adoption of thermal aging chambers for accelerated stress testing is becoming widespread to simulate long-term durability rapidly.

- •Collaborations between equipment manufacturers and semiconductor fabs increase customization and co-development of aging repair technologies.

- •Growing emphasis on sustainability drives development of energy-efficient and eco-friendly repair equipment solutions.

Market Restraints

- •High capital expenditure and operational costs associated with advanced aging repair equipment limit adoption among smaller manufacturers.

- •Complexity in integrating new repair technologies with existing semiconductor fabrication lines poses technical challenges.

- •Short lifecycle of DRAM products can reduce the return on investment for costly repair equipment upgrades.

- •Limited availability of skilled technicians to operate sophisticated repair systems restricts market expansion in certain regions.

- •Stringent regulatory requirements increase compliance costs for equipment manufacturers and users.

Market Opportunities

- •Development of modular and scalable repair equipment enables customization for diverse DRAM production scales and architectures.

- •Expansion into emerging regional zones within the United States, such as the Southeast, offers growth through untapped manufacturing hubs.

- •Advancements in AI-driven diagnostic tools present opportunities for enhancing repair precision and reducing downtime.

- •Strategic partnerships between repair equipment providers and semiconductor manufacturers accelerate innovation and market penetration.

- •Increasing demand for memory repair solutions in automotive and IoT applications opens new revenue streams.

Market Challenges

- •Rapid technological changes in DRAM architectures require continual equipment upgrades, increasing operational complexity and costs.

- •Intense competition from global players necessitates constant innovation and price optimization to maintain market share.

- •Supply chain disruptions can delay equipment delivery and impact production schedules for semiconductor manufacturers.

- •Ensuring compatibility of repair equipment with diverse DRAM technologies and fabrication processes remains a technical hurdle.

- •Cybersecurity concerns related to diagnostic software integration require robust data protection measures to prevent intellectual property loss.

Regulatory Framework

- •The U.S. Environmental Protection Agency (EPA) regulations from 2020 to 2025 have tightened emissions and waste disposal requirements for semiconductor equipment manufacturers, impacting the design and operation of DRAM aging repair systems.

- •Occupational Safety and Health Administration (OSHA) guidelines updated in 2023 mandate enhanced safety protocols for operators of thermal aging chambers and manual repair tools to reduce workplace hazards.

- •Federal Communications Commission (FCC) regulations introduced in 2021 require compliance for diagnostic software communications to prevent interference with other semiconductor facility equipment.

- •California’s Proposition 65 enforcement in 2022 impacts materials used in repair tools, requiring manufacturers to disclose chemical hazards and seek safer alternatives where possible.

- •Export control policies implemented in 2024 affect the distribution of advanced repair equipment technology, requiring compliance verification for international sales and technology transfers.

Market Intelligence

- •15th February 2025, Teradyne Inc. launched its next-generation automated DRAM repair system featuring AI-powered diagnostics and enhanced thermal aging capabilities aimed at reducing repair cycle times by 30%. This innovation is targeted at major U.S. semiconductor fabs seeking to improve yield and reliability of high-density DRAM chips. The system integrates seamlessly with existing fabrication lines, offering scalable solutions for diverse production volumes. Teradyne’s strategic objective is to reinforce its leadership in the DRAM repair equipment segment by combining automation and predictive analytics to meet growing industry demands. Source: Teradyne Official Press Release

- •10th October 2024, KLA Corporation introduced advanced diagnostic software with machine learning capabilities designed to optimize failure analysis in DRAM aging repair processes. This software enhances defect detection accuracy and enables real-time repair decision-making, significantly boosting operational efficiency. The product launch aligns with KLA’s commitment to integrating AI technologies into semiconductor manufacturing equipment, catering to evolving memory technology challenges. The software is already being piloted by several U.S.-based semiconductor manufacturers, indicating strong market acceptance and potential for widespread adoption. Source: KLA Corporation Press Release

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Mergers & Acquisitions

- •In June 2024, Advantest Corporation completed the acquisition of a U.S.-based semiconductor diagnostic software firm specializing in AI-driven aging repair solutions. This strategic move aims to bolster Advantest’s portfolio with cutting-edge machine learning technologies, enhancing their DRAM repair equipment offerings. The acquisition is expected to accelerate innovation cycles and expand market reach within the United States by integrating advanced diagnostics capabilities into existing product lines. This consolidation reflects growing industry emphasis on software-enabled hardware solutions to address DRAM aging challenges effectively.

- •In March 2023, Lam Research Corporation merged with a domestic manual repair tool manufacturer to diversify its product range within the DRAM aging repair market. The merger enables Lam Research to offer comprehensive repair equipment solutions, combining automated systems with precision manual tools tailored for niche applications. This integration supports the company’s growth strategy focused on providing end-to-end aging repair technologies to semiconductor manufacturers across North America. The combined entity leverages shared R&D resources and expanded customer networks to strengthen competitive positioning.

Recent Industry News

- •12th January 2025, Onto Innovation Inc. announced a strategic partnership with a leading U.S. semiconductor manufacturer to jointly develop next-generation thermal aging chambers optimized for emerging DRAM architectures. This collaboration aims to accelerate innovation cycles and tailor equipment features to specific production needs, enhancing stress testing accuracy and throughput. The partnership signifies growing alignment between equipment suppliers and semiconductor fabs to meet increasing demands for memory reliability and yield improvements. Source: Onto Innovation Press Release

- •5th March 2025, SCREEN Holdings Co., Ltd. expanded its manufacturing facility in the United States to increase production capacity for inspection equipment used in DRAM aging repair. The expansion is driven by rising demand from domestic semiconductor fabs investing in quality control enhancements. The new facility incorporates advanced automation and quality management systems to ensure timely delivery and superior product performance. This move strengthens SCREEN’s commitment to supporting U.S. semiconductor industry growth and technological advancement. Source: SCREEN Holdings Corporate Announcement

- •20th May 2025, FormFactor, Inc. launched a cloud-enabled diagnostic software platform that integrates with automated repair systems for real-time data analytics in DRAM aging repair processes. The platform enhances decision-making efficiency, reduces repair cycle times, and supports predictive maintenance. This innovation is expected to transform aging repair workflows by enabling seamless data sharing and remote monitoring capabilities. The launch underscores FormFactor’s strategic focus on digital transformation within semiconductor equipment markets. Source: FormFactor Press Release

- •30th July 2025, MKS Instruments, Inc. announced the acquisition of a U.S.-based startup specializing in eco-friendly thermal aging chambers. The acquisition aims to expand MKS’s product portfolio with sustainable equipment solutions, responding to increasing environmental regulations and customer demand for green technologies. This move positions MKS as a leader in delivering energy-efficient aging repair equipment and aligns with broader industry trends towards sustainability in semiconductor manufacturing. Source: MKS Instruments Official Statement

Market Statistics

- •CAGR by 2034: 13.0%

- •Market Size by 2034: USD 3.8 Billion

- •Market Size in 2025: USD 1.2 Billion

- •Dominating Type: Automated Repair Systems

- •Next-following Type: Thermal Aging Chambers

- •Dominating Application: Memory Testing

- •Next-following Application: Failure Analysis

- •Dominating Region: West Coast

- •Second-leading Region: Northeast

- •Region with Highest Growth Rate: Southeast

- •Dominating Country: United States

Market Share Table

- •Market Share (%) by Type: Automated Repair Systems - 45%, Thermal Aging Chambers - 25%

- •Market Share (%) by Application: Memory Testing - 40%, Failure Analysis - 30%

- •Growth Rate (%) by Type: Automated Repair Systems - 12%, Thermal Aging Chambers - 15.5%

- •Growth Rate (%) by Application: Memory Testing - 13%, Failure Analysis - 11%

Top 5 Global Players

- •Teradyne Inc. (United States)

- •KLA Corporation (United States)

- •Tokyo Electron Limited (Japan)

- •Advantest Corporation (Japan)

- •Lam Research Corporation (United States)

Regional Outlook

The West Coast currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southeast is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Northeast

- Southwest

- The South

- The Midwest

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.2 Billion |

| Forecast Year Market Size | USD 3.8 Billion |

| CAGR | 13% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.3% |

| Scope of Report | Market is segmented by Type (Automated Repair Systems, Manual Repair Tools, Inspection Equipment, Thermal Aging Chambers, Diagnostic Software), Application (Memory Testing, Failure Analysis, Repair Process, Quality Control, Research & Development), End User (Semiconductor Manufacturers, Outsourced Repair Services, Research Institutions), Distribution Channel (Direct Sales, Distributors, Online Platforms) |

| Regions Covered | Northeast, Southwest, The South, The Midwest |

| Key Companies | Teradyne Inc. (United States), KLA Corporation (United States), ASM Pacific Technology Ltd. (Hong Kong), Tokyo Electron Limited (Japan), Advantest Corporation (Japan), Lam Research Corporation (United States), SCREEN Holdings Co., Ltd. (Japan), Hitachi High-Technologies Corporation (Japan), Onto Innovation Inc. (United States), Nordson Corporation (United States), Ultratech, Inc. (United States), Applied Materials, Inc. (United States), Veeco Instruments Inc. (United States), FormFactor, Inc. (United States), MKS Instruments, Inc. (United States), Cohu, Inc. (United States), ASM International N.V. (Netherlands), Advantest America, Inc. (United States), FormFactor Asia Pacific, Inc. (Singapore), Teradyne GmbH (Germany), Hitachi High-Tech Analytical Science America, Inc. (United States), Nikon Corporation (Japan), Screen Semiconductor Solutions Co., Ltd. (Japan), Tokyo Seimitsu Co., Ltd. (Japan), Xcerra Corporation (United States) |

United States DRAM Aging Repair Equipment Market - Outlook 2025-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.