GCC Cloud Computing for Autonomous Driving Market Size, Growth & Revenue 2025-2034

GCC Cloud Computing for Autonomous Driving Market is segmented by Cloud Service Type (Public Cloud, Private Cloud, Hybrid Cloud, Edge Computing, Cloud Storage), Application (Real-time Data Processing, Vehicle-to-Everything Communication, Autonomous Fleet Management, Predictive Maintenance, In-car Infotainment), Deployment Model (On-premises, Cloud-based, Hybrid), End-User Segment (Automotive OEMs, Telecommunication Providers, Government & Municipalities, Technology Service Providers), and Geography (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates)

Pricing

Report Overview

Executive Summary

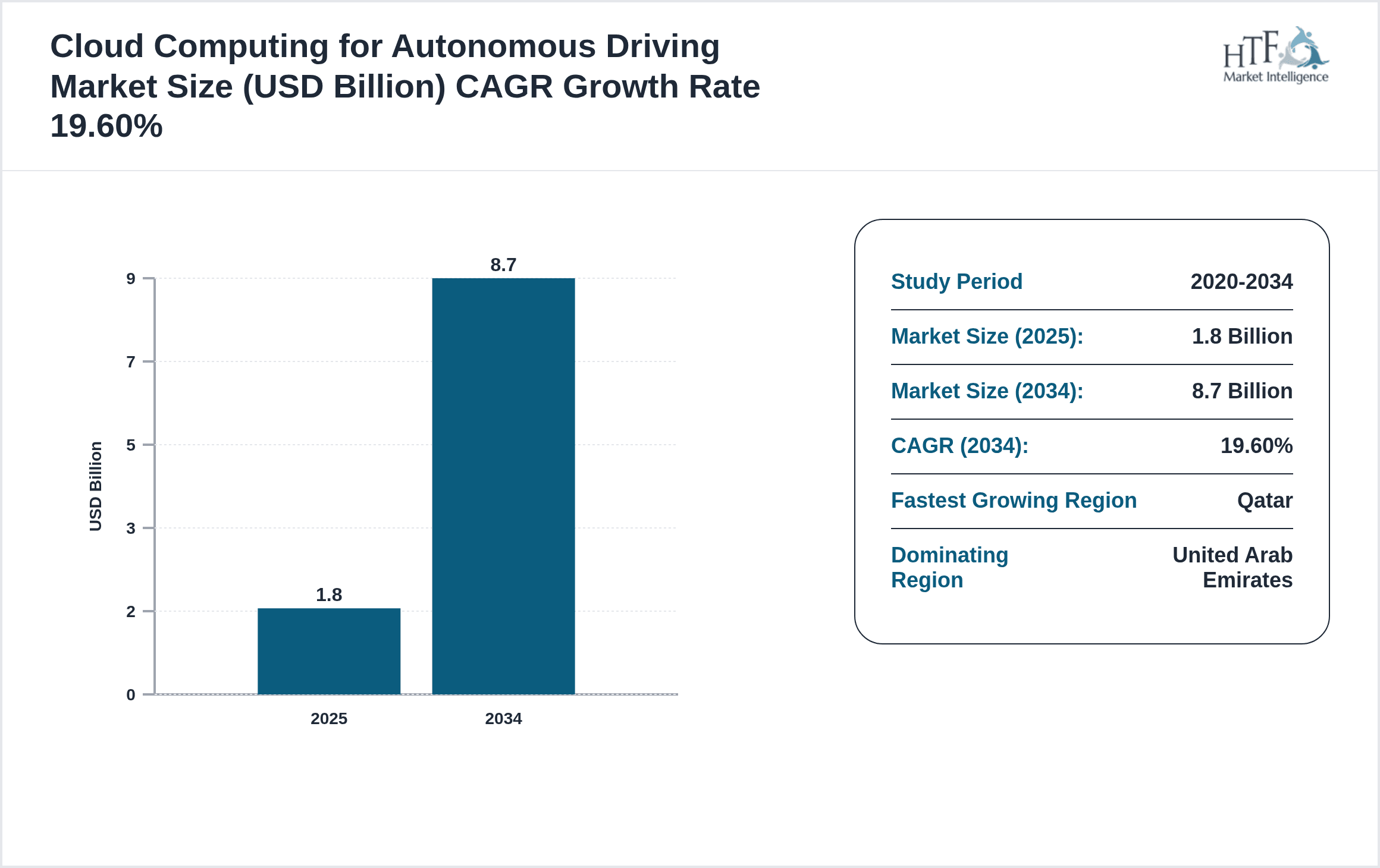

- •The GCC Cloud Computing for Autonomous Driving market integrates cloud technologies to facilitate autonomous vehicle functions including real-time sensor data processing, V2X communication, and autonomous fleet management. It leverages public, private, hybrid, and edge cloud platforms to meet stringent latency and reliability requirements critical for safe autonomous driving. This market caters to automotive OEMs, technology firms, and government initiatives promoting smart cities and intelligent transportation within GCC countries.

- •Key market highlights include a base market size of USD 1.8 Billion in 2025, projected to reach USD 8.7 Billion by 2034, reflecting a CAGR of 19.6%. The UAE dominates the regional market with a 38% share, while Qatar exhibits the fastest growth at a CAGR of 24.2%. Leading product types include Public Cloud services, whereas Edge Computing is the fastest growing technology segment.

- •Cloud computing for autonomous driving offers significant value by enabling scalable data management, enhanced computational power, and seamless connectivity essential for autonomous vehicle operations. This market is strategically important for advancing GCC’s vision of smart mobility, contributing to improved road safety, traffic efficiency, and reduction of emissions through autonomous vehicle adoption.

Competitive Landscape

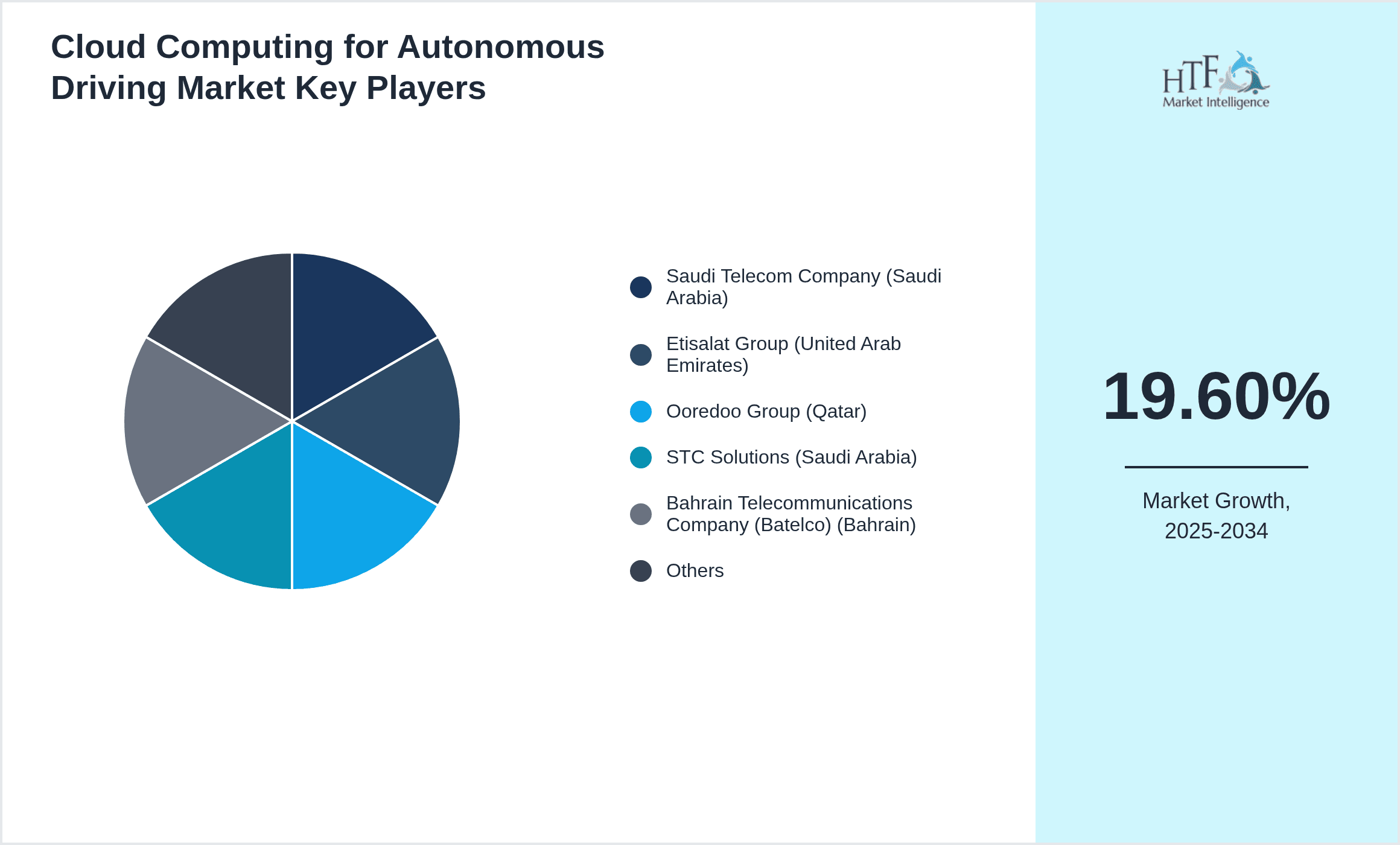

The GCC Cloud Computing for Autonomous Driving market is characterized by a dynamic competitive environment featuring global cloud service providers, automotive technology firms, and regional telecommunication companies. Competitive strategies are focused on technological innovation, strategic partnerships, and localized service offerings to meet GCC-specific regulatory and infrastructural requirements. Companies are investing in edge computing and AI-enhanced analytics to reduce latency and improve autonomous driving safety. Market positioning emphasizes comprehensive cloud platforms integrating data security, V2X communication, and scalable infrastructure. Mergers and acquisitions are sporadic but targeted towards expanding cloud capabilities and geographic presence within GCC. Pricing strategies balance premium service offerings with competitive subscription models. Distribution channels include direct sales to automotive OEMs and collaborations with governmental smart city projects. The adoption of 5G networks and regional regulatory frameworks further intensify competition, driving continuous innovation and market consolidation. Regional competition varies, with UAE and Saudi Arabia leading in infrastructure deployment while emerging markets like Qatar focus on rapid adoption and pilot programs. Future trends include increased integration of AI and blockchain for data integrity, expansion of hybrid cloud models, and growth in autonomous fleet cloud management solutions.

Prominent Players in GCC Cloud Computing for Autonomous Driving Market

- •Saudi Telecom Company (Saudi Arabia)

- •Etisalat Group (United Arab Emirates)

- •Ooredoo Group (Qatar)

- •STC Solutions (Saudi Arabia)

- •Bahrain Telecommunications Company (Batelco) (Bahrain)

- •Zain Group (Kuwait)

- •Du Telecom (United Arab Emirates)

- •Omantel (Oman)

- •IBM Middle East (Regional Headquarters in UAE)

- •Microsoft Gulf (Regional Headquarters in UAE)

- •Google Cloud (Regional Operations in UAE)

- •Oracle Corporation (Regional Office in UAE)

- •Honeywell Middle East (Regional HQ in UAE)

- •NVIDIA Corporation (Regional Office in UAE)

- •Cisco Systems (Regional HQ in UAE)

- •Amazon Web Services (AWS) Middle East (Regional HQ in UAE)

- •Huawei Technologies (Regional Office in Saudi Arabia)

- •Samsung SDS (Middle East Office in UAE)

- •Accenture Middle East (Regional HQ in UAE)

- •Dell Technologies (Regional HQ in UAE)

- •Siemens Middle East (Regional HQ in UAE)

- •Bosch Middle East (Regional HQ in UAE)

- •Nokia Middle East (Regional HQ in UAE)

- •Ericsson Middle East (Regional HQ in UAE)

- •SAP Middle East (Regional HQ in UAE)

Market Breakdown

- •By Cloud Service Type

- ◦Public Cloud

- ◦Private Cloud

- ◦Hybrid Cloud

- ◦Edge Computing

- ◦Cloud Storage

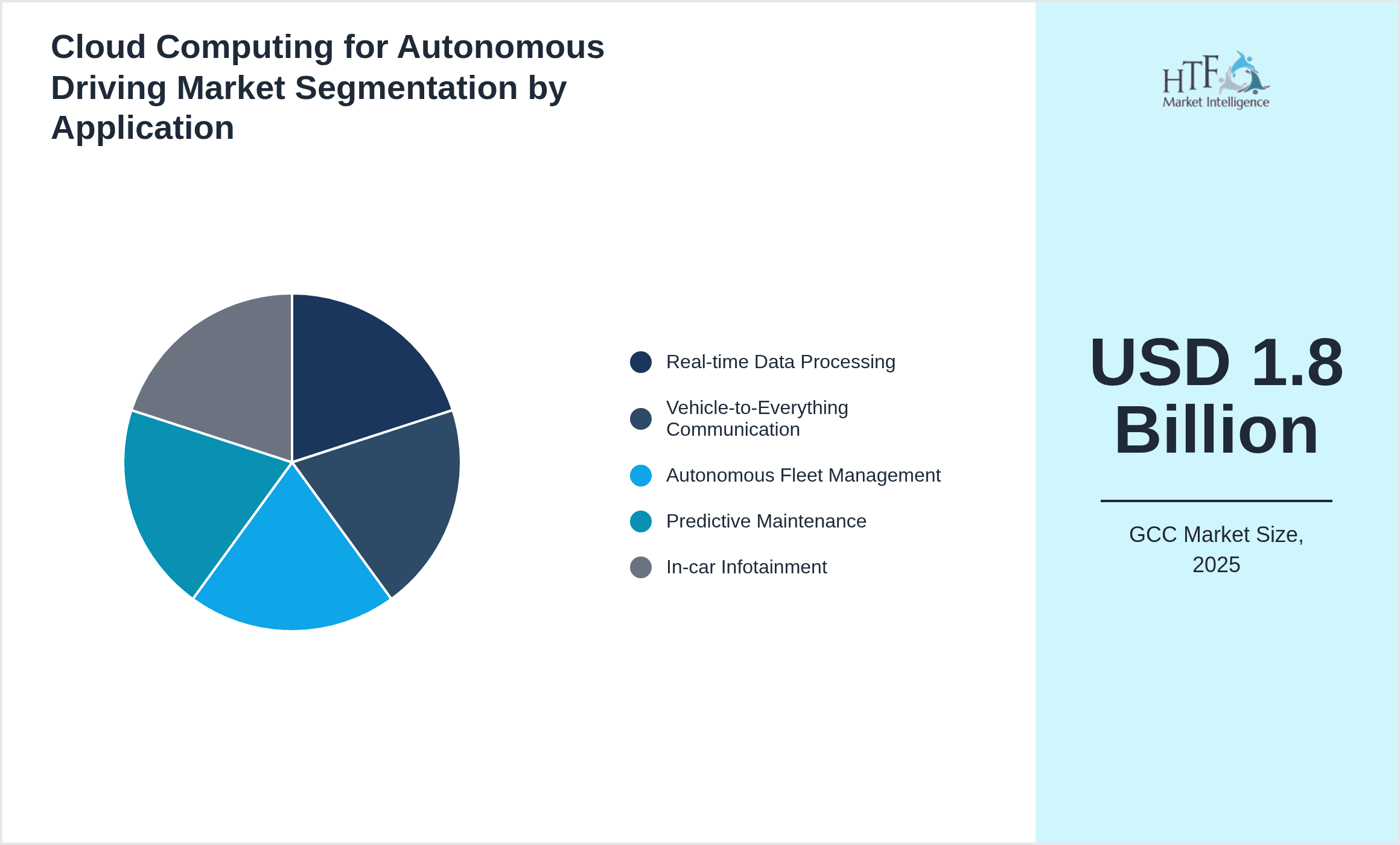

- •By Application

- ◦Real-time Data Processing

- ◦Vehicle-to-Everything Communication

- ◦Autonomous Fleet Management

- ◦Predictive Maintenance

- ◦In-car Infotainment

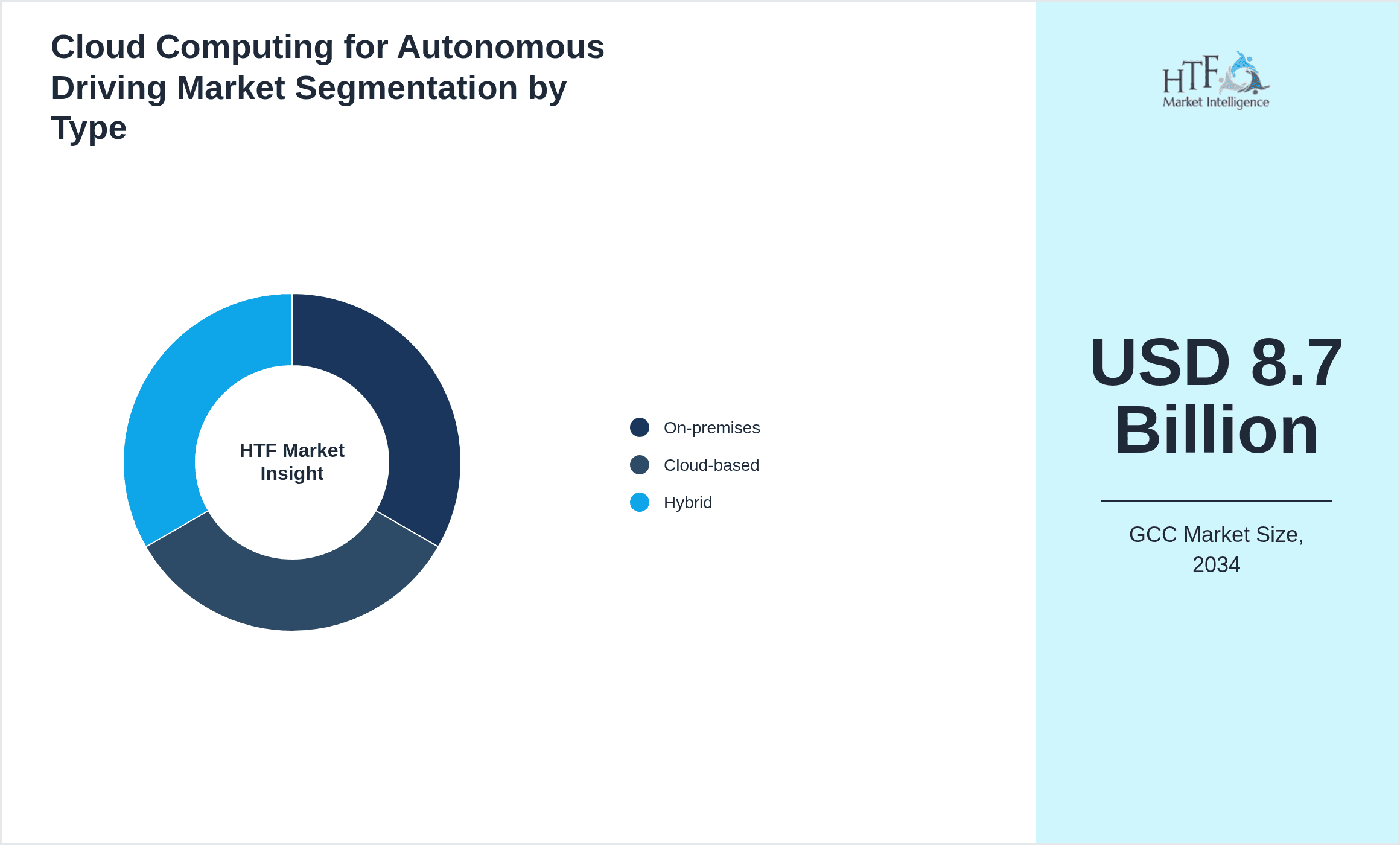

- •By Deployment Model

- ◦On-premises

- ◦Cloud-based

- ◦Hybrid

- •By End-User Segment

- ◦Automotive OEMs

- ◦Telecommunication Providers

- ◦Government & Municipalities

- ◦Technology Service Providers

Growth Dynamics

- •The GCC market growth is driven by massive government investments in smart city initiatives and autonomous vehicle pilot projects, especially in UAE and Saudi Arabia, which are pushing cloud infrastructure deployments to support autonomous driving applications with high computational power and scalability.

- •Advancements in 5G networks throughout the GCC enable low latency and reliable V2X communication, which is critical for real-time autonomous driving cloud services, further accelerating market adoption and expansion.

- •Increasing partnerships between cloud service providers and automotive OEMs facilitate the integration of cloud computing with autonomous driving technologies, fostering innovation in data analytics, AI, and edge computing to enhance vehicle safety and operational efficiency.

- •Rising consumer demand for autonomous vehicles and connected car services, along with supportive regulatory frameworks, incentivizes players to invest in scalable cloud solutions capable of handling massive sensor data and vehicle coordination in GCC cities.

- •The adoption of hybrid and edge computing models addresses latency and data privacy concerns in autonomous driving, enabling localized data processing and reducing cloud dependency, which is gaining traction among GCC stakeholders.

Market Trends

- •Integration of AI-driven analytics within cloud platforms is enabling predictive maintenance and autonomous fleet optimization, allowing GCC operators to reduce downtime and improve safety metrics in real-time.

- •Edge computing adoption is growing rapidly as GCC companies seek to reduce latency and bandwidth costs by processing data closer to vehicles, supporting critical autonomous driving functions with minimal delay.

- •Cloud-native microservices architectures are being implemented to enhance scalability and flexibility of autonomous driving cloud platforms, enabling faster deployment of new features and updates in GCC markets.

- •Collaborations between telecom operators and cloud providers are increasing to leverage 5G capabilities for autonomous vehicle connectivity, promoting ecosystem development and service innovation across the GCC region.

- •Sustainability trends are influencing cloud infrastructure choices with GCC stakeholders prioritizing energy-efficient data centers and green cloud practices to align with regional environmental goals.

Market Opportunities

- •Expanding autonomous vehicle pilot programs in Qatar and Oman present untapped opportunities for cloud service providers to deploy customized solutions addressing local regulatory and operational requirements, enabling rapid market penetration.

- •Increasing government incentives for smart mobility and digital infrastructure investments across GCC countries create favorable conditions for cloud computing adoption in autonomous driving applications, attracting new entrants and partnerships.

- •The rising adoption of hybrid cloud and edge computing models offers growth potential for innovative service offerings that balance data privacy, latency, and scalability demands unique to autonomous driving in GCC urban environments.

- •Collaborations with regional telecom operators to leverage 5G networks for vehicle connectivity can unlock new service models and revenue streams, enhancing cloud platform capabilities for real-time data exchange and analytics.

- •Development of localized cloud infrastructure to comply with emerging GCC data sovereignty regulations can differentiate providers and build trust among automotive and government stakeholders.

Market Challenges

- •The high capital expenditure required to deploy and maintain sophisticated cloud infrastructure tailored for autonomous driving limits entry for smaller providers and slows market expansion within the GCC region.

- •Regulatory ambiguities and evolving compliance requirements related to data privacy, cybersecurity, and autonomous vehicle operation create uncertainty for cloud service providers and automotive companies operating in GCC countries.

- •Latency and reliability challenges remain critical for GCC’s autonomous driving cloud solutions, especially in regions with underdeveloped telecommunication infrastructure, hindering seamless real-time data processing and communication.

- •Integration complexities arise due to heterogeneous vehicle platforms, cloud architectures, and communication standards, requiring extensive customization and interoperability efforts for GCC deployments.

- •Talent shortage in cloud computing, AI, and autonomous vehicle technology domains within the GCC limits innovation pace and operational scalability, necessitating investments in skill development and international partnerships.

Regulatory Framework

- •Between 2020 and 2025, GCC countries have introduced data protection laws such as UAE’s Federal Decree-Law No. 45 of 2021 on Personal Data Protection, mandating stringent data privacy and security requirements impacting cloud computing services for autonomous driving.

- •Saudi Arabia’s National Cybersecurity Authority established regulations addressing critical infrastructure protection including autonomous vehicle cloud platforms, enforcing compliance with security standards to mitigate cyber threats.

- •GCC governments have enacted policies to promote 5G network deployment and spectrum allocation, enabling enhanced connectivity essential for autonomous driving cloud applications, while ensuring adherence to regional telecommunication norms.

- •Autonomous vehicle testing and operation regulations have been progressively introduced across the GCC, including licensing frameworks and safety standards, directly influencing cloud computing requirements for data handling and V2X communication.

- •Regional initiatives such as the Gulf Cooperation Council Standardization Organization (GSO) collaborate on harmonizing technical standards and regulatory guidelines to facilitate cross-border autonomous vehicle cloud service interoperability within the GCC.

Market Intelligence

- •15th February 2025, Etisalat Group announced the launch of a dedicated cloud computing platform optimized for autonomous driving applications in the UAE, featuring integrated AI analytics and edge computing capabilities designed to support real-time vehicle data processing and V2X communication. This initiative aims to accelerate autonomous vehicle adoption in the region by providing scalable, low-latency cloud services tailored to GCC infrastructure needs. Source: Etisalat official press release.

- •10th April 2025, Saudi Telecom Company (STC) unveiled a strategic partnership with Microsoft Gulf to develop hybrid cloud solutions for autonomous fleet management across Saudi Arabia. The collaboration focuses on combining STC’s 5G network with Microsoft’s Azure cloud services to enable secure, efficient, and scalable cloud platforms supporting autonomous vehicle operations. This partnership strengthens STC's position as a leading cloud provider in the GCC autonomous driving market. Source: STC corporate announcement.

- •28th June 2025, Ooredoo Group launched an edge computing pilot project in Qatar targeting autonomous vehicle data processing to reduce latency and enhance safety-critical applications. The project integrates Ooredoo’s network infrastructure with cloud services from IBM Middle East, aiming to establish Qatar as a hub for autonomous driving innovation within the GCC. Source: Ooredoo official press release.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The United Arab Emirates currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Qatar is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Bahrain

- Kuwait

- Oman

- Qatar

- Saudi Arabia

- United Arab Emirates

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 8.7 Billion |

| CAGR | 19.6% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 19.3% |

| Scope of Report | Market is segmented by Cloud Service Type (Public Cloud, Private Cloud, Hybrid Cloud, Edge Computing, Cloud Storage), Application (Real-time Data Processing, Vehicle-to-Everything Communication, Autonomous Fleet Management, Predictive Maintenance, In-car Infotainment), Deployment Model (On-premises, Cloud-based, Hybrid), End-User Segment (Automotive OEMs, Telecommunication Providers, Government & Municipalities, Technology Service Providers) |

| Regions Covered | Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates |

| Key Companies | Saudi Telecom Company (Saudi Arabia), Etisalat Group (United Arab Emirates), Ooredoo Group (Qatar), STC Solutions (Saudi Arabia), Bahrain Telecommunications Company (Batelco) (Bahrain) |

GCC Cloud Computing for Autonomous Driving Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.