Europe Spelt Wheat Market Scope & Changing Dynamics 2024-2034

Europe Spelt Wheat Market is segmented by Type (Whole Grain Spelt, Hulled Spelt, Spelt Flour, Organic Spelt, Conventional Spelt), Application (Food & Beverage, Animal Feed, Brewing Industry, Functional Foods, Others), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Spelt Wheat market involves the cultivation, processing, and commercialization of various spelt wheat types including whole grain, hulled, and organic variants, catering to food, feed, and brewing industries across key European countries.

- •Market growth is driven by increasing consumer demand for organic and functional foods, growing awareness of spelt wheat's health benefits, and expanding applications in both food and animal feed sectors.

- •The market's value proposition lies in offering a sustainable, nutritious grain alternative favored by health-conscious consumers, with strategic importance for food manufacturers and agricultural stakeholders navigating evolving regulatory landscapes in Europe.

Competitive Landscape

Competition within the Europe Spelt Wheat market is shaped by a diverse mix of large agribusinesses and specialized organic grain producers. Market leaders capitalize on innovation in sustainable farming and processing technologies to differentiate their offerings. The rivalry intensifies as companies focus on product diversification, quality certifications, and expanding distribution networks across Europe. Strategic partnerships and supply chain optimization are common to ensure fresh and organic spelt wheat availability. Pricing strategies balance premium organic positioning with competitive conventional options. The market also experiences regional competition driven by country-specific agricultural policies and consumer preferences. Future competition is expected to pivot on technological advancements in crop yield improvement and enhanced traceability systems to meet stringent European food safety standards.

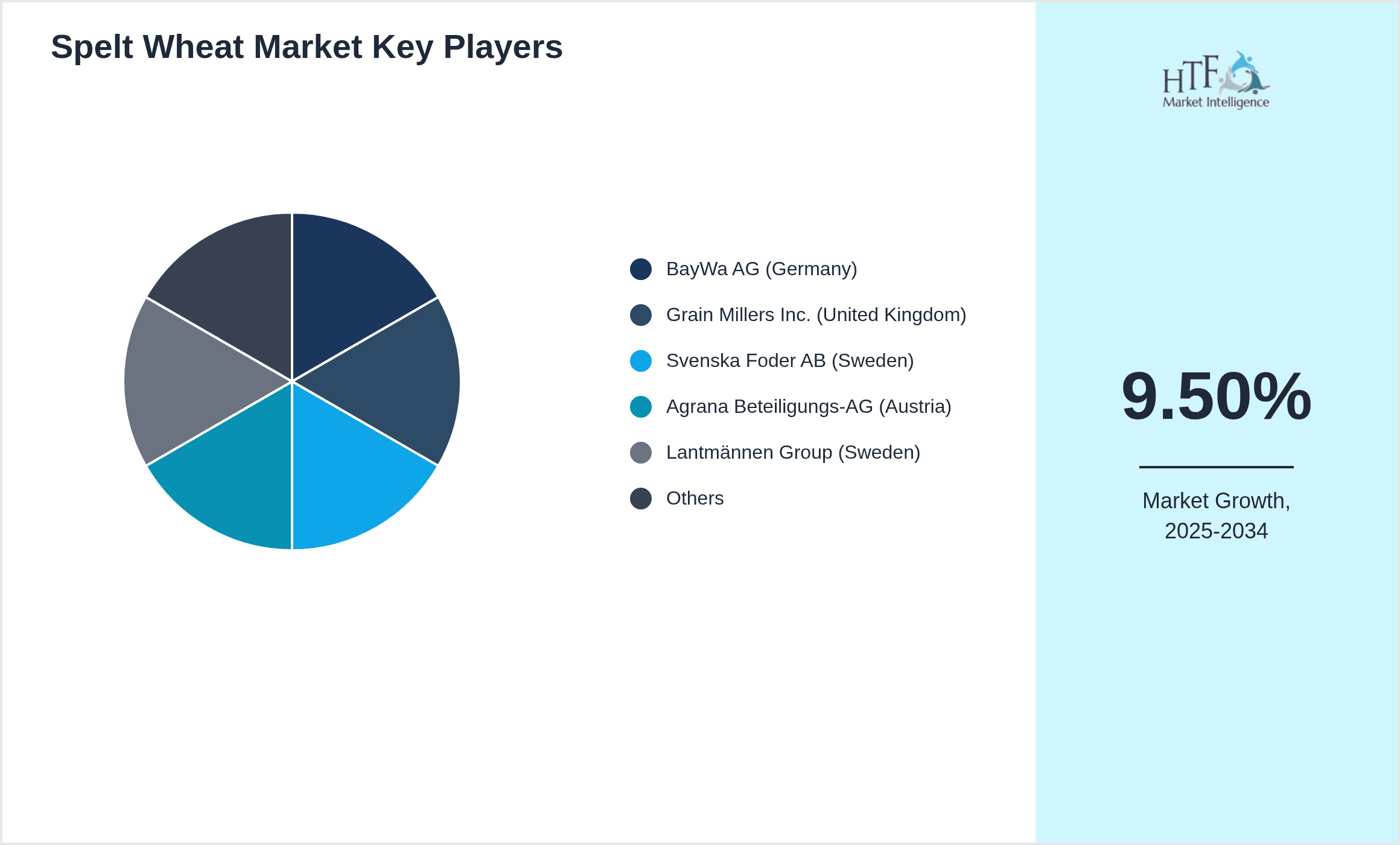

Leading Companies in Europe Spelt Wheat Market

- •BayWa AG (Germany)

- •Grain Millers Inc. (United Kingdom)

- •Svenska Foder AB (Sweden)

- •Agrana Beteiligungs-AG (Austria)

- •Lantmännen Group (Sweden)

- •Archer Daniels Midland Company (Germany)

- •KWS SAAT SE & Co. KGaA (Germany)

- •Bioland e.V. (Germany)

- •Cargill, Incorporated (Belgium)

- •Barilla Group (Italy)

- •Bühler Group (Switzerland)

- •Doves Farm Foods Ltd (United Kingdom)

- •EcorNaturaSì (Italy)

- •GoodMills Group (Austria)

- •Hochland SE (Germany)

- •Jordans & Ryvita Company (United Kingdom)

- •Kamut International Ltd. (Switzerland)

- •Lallemand Inc. (France)

- •Mühle Lauenburg GmbH (Germany)

- •Natracare Ltd (United Kingdom)

- •Ökoland eG (Germany)

- •Puratos Group (Belgium)

- •Sachsenmilch GmbH (Germany)

- •Tate & Lyle PLC (United Kingdom)

- •Vandemoortele NV (Belgium)

Europe Spelt Wheat Market Segmentation

- •By Type

- ◦Whole Grain Spelt

- ◦Hulled Spelt

- ◦Spelt Flour

- ◦Organic Spelt

- ◦Conventional Spelt

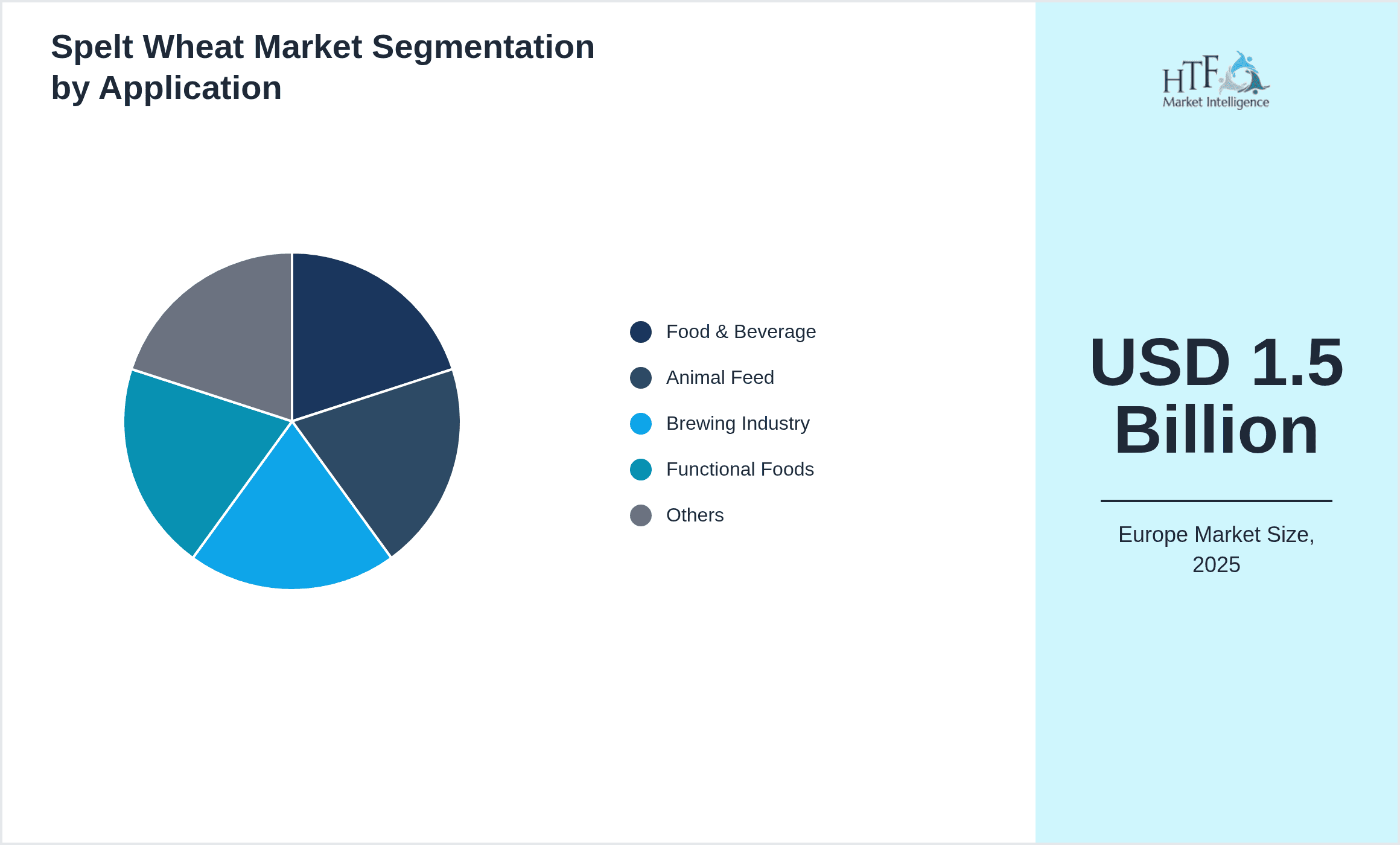

- •By Application

- ◦Food & Beverage

- ◦Animal Feed

- ◦Brewing Industry

- ◦Functional Foods

- ◦Others

- •By Distribution Channel

- ◦Supermarkets & Hypermarkets

- ◦Specialty Stores

- ◦Online Retail

- ◦Direct Sales

- •By Farming Method

- ◦Conventional Farming

- ◦Organic Farming

- ◦Sustainable Farming

Growth Drivers

Rising consumer preference for organic and ancient grains significantly propels the Europe Spelt Wheat market growth. Increasing awareness of spelt's nutritional benefits such as high fiber and protein content fuels demand in health-conscious demographics. Expansion of functional food products incorporating spelt wheat enhances market penetration. Additionally, growing adoption of gluten-sensitive diets, where spelt is preferred over common wheat, supports sustained consumption. The European Union’s emphasis on sustainable agriculture and organic farming incentivizes producers to cultivate spelt wheat, further boosting supply. Moreover, increasing investments in modern farming technologies improve yield and quality, enabling market players to meet rising demand efficiently. These drivers collectively contribute to the robust CAGR forecasted through 2034, positioning spelt wheat as a vital component in Europe’s cereal grain sector.

Market Trends

The Europe Spelt Wheat market is witnessing a surge in product innovation, particularly in organic spelt flour and gluten-reduced formulations catering to niche dietary needs. There is an increasing trend of integrating spelt wheat into bakery and snack categories, enhancing flavor and nutrition profiles. Retailers are expanding online platforms dedicated to organic and specialty grains, improving consumer access. Furthermore, collaborations between farmers and food processors aim to strengthen traceability and quality assurance. Sustainability remains a key trend, with emphasis on reducing carbon footprint through eco-friendly farming practices. The rise in craft brewing utilizing spelt wheat for unique flavor profiles also marks a growing niche application. These evolving trends reflect a dynamic marketplace aligned with shifting consumer preferences and environmental considerations.

Market Restraints

Despite growth, the Europe Spelt Wheat market faces challenges such as relatively higher production costs compared to conventional wheat, impacting pricing competitiveness. Limited consumer awareness in certain regions restricts broader adoption. The grain’s lower yield and susceptibility to diseases compared to modern wheat varieties pose cultivation risks for farmers. Supply chain complexities, including seasonal variability and storage requirements, add operational burdens. Additionally, regulatory compliance for organic certification introduces administrative overheads. Price volatility in agricultural commodities further affects profitability for producers and suppliers. These restraints collectively temper rapid market expansion and necessitate strategic interventions to optimize cost structures and enhance market education.

Market Opportunities

Emerging opportunities in Europe’s functional food segment present significant growth avenues for spelt wheat, driven by demand for natural, nutrient-rich ingredients. Expanding organic farming acreage supported by EU subsidies offers prospects for increased production volumes. Innovations in processing technologies to improve spelt wheat digestibility and shelf life can unlock new consumer segments. Growth in online retail channels facilitates direct-to-consumer sales, enhancing market reach. Cross-sector collaborations for developing spelt-based beverages and gluten-sensitive products provide diversification potential. Moreover, increasing export possibilities to health-conscious global markets create additional revenue streams. These opportunities encourage stakeholders to invest in R&D and marketing, fostering market expansion.

Market Challenges

Key challenges include managing spelt wheat’s agronomic limitations like lower yield and higher susceptibility to environmental stresses compared to common wheat. Ensuring consistent quality and meeting stringent EU organic certification standards require substantial investment and expertise. Market fragmentation and competition from other ancient grains challenge market share growth. Consumer misconceptions regarding spelt’s gluten content limit acceptance among celiac disease patients. Price sensitivity in price-competitive European markets pressures margins. Additionally, supply chain disruptions due to climate change and geopolitical factors pose risks to steady market supply. Overcoming these challenges demands technological advances, robust quality control, and targeted consumer education initiatives.

Regulatory Overview

Recent regulatory updates in Europe emphasize organic certification and sustainable agriculture standards impacting the spelt wheat market. The European Union has reinforced controls under the Organic Production Regulation (EU) 2018/848, requiring stringent compliance for organic labeling and traceability. Additionally, new pesticide usage restrictions and soil health guidelines under the EU Green Deal influence farming practices. Food safety regulations under the European Food Safety Authority (EFSA) mandate rigorous testing for contaminants and allergen declarations, directly affecting spelt wheat processing and packaging. These evolving regulations aim to ensure consumer safety, environmental sustainability, and market transparency, posing compliance challenges but also enhancing product credibility. Producers and suppliers are adapting through improved documentation, certification processes, and sustainable sourcing strategies.

Industry Insights

In March 2023, Agrana Beteiligungs-AG launched a new line of organic spelt flour with enhanced nutritional profiles targeting health-conscious consumers in Central Europe. This product integrates innovative milling techniques that preserve essential grain nutrients and flavor. The launch reflects growing demand for premium ancient grain products in bakery and functional food sectors. In November 2022, Lantmännen Group expanded its spelt wheat cultivation program across Nordic countries to increase organic acreage, responding to rising consumer demand for sustainable and organic cereals. This strategic move supports supply chain stability and aligns with EU sustainability goals, positioning Lantmännen as a leader in organic grain production. These initiatives underscore the market’s focus on innovation and sustainability.

Mergers & Acquisitions

- •In April 2023, BayWa AG acquired a majority stake in a German organic grain cooperative specializing in spelt wheat production. This acquisition strengthens BayWa’s position in the organic cereals market, expanding its supply base and processing capabilities. The move aligns with BayWa’s strategy to enhance sustainable agriculture offerings in Europe and meet growing consumer demand for organic products. Integration of the cooperative’s network enables improved traceability and quality assurance across the supply chain.

- •In September 2022, Archer Daniels Midland Company (ADM) completed the acquisition of a French specialty grain processor focused on spelt wheat and ancient grains. This strategic acquisition enables ADM to broaden its product portfolio within the European spelt wheat market, leveraging advanced processing technologies and expanding distribution in key markets such as France, Germany, and the UK. The deal enhances ADM’s innovation capabilities and strengthens its competitive edge in the organic and functional food segments.

Recent Industry News

- •15th May 2024, Bühler Group announced the launch of a new milling technology designed specifically for spelt wheat processing. This technology enhances flour yield and preserves nutritional content, addressing key industry challenges in spelt wheat production. The innovation supports manufacturers in producing higher-quality spelt-based products with improved shelf life, meeting growing consumer demand in Europe. Bühler aims to collaborate with major European grain processors to implement this technology across the region. Source: Bühler official press release.

- •20th October 2023, GoodMills Group expanded its organic spelt wheat supply chain by partnering with farmers in the BeNeLux region. This partnership focuses on sustainable farming practices and quality assurance, ensuring consistent supply for GoodMills’ organic product lines. The initiative supports the growing demand for organic and ancient grains in European markets, reinforcing GoodMills’ position as a leading sustainable grain supplier. Source: GoodMills Group website.

- •12th February 2022, Barilla Group introduced a new range of spelt wheat pasta products incorporating organic spelt flour sourced from European farmers. This launch targets consumers seeking healthier alternatives to traditional pasta with enhanced fiber and protein content. Barilla's initiative reflects rising interest in ancient grains within mainstream food categories and aligns with sustainability goals. The company also invested in supply chain transparency to guarantee organic certification compliance. Source: Barilla corporate news.

- •5th August 2021, Cargill, Incorporated launched a research collaboration with European agricultural institutes to improve spelt wheat crop resilience and yield. The project focuses on breeding techniques and sustainable farming practices to enhance spelt’s adaptability to climate change. Outcomes aim to benefit grain producers and processors by securing stable supply and quality. This collaboration represents a strategic investment in innovation to support the long-term growth of the European spelt wheat market. Source: Cargill press statement.

Market Statistics

- •CAGR by 2034: 9.5%

- •Market Size by 2034: USD 3.8 Billion

- •Market Size in 2025: USD 1.65 Billion

- •Dominating Type: Whole Grain Spelt

- •Next-Following Type: Organic Spelt

- •Dominating Application: Food & Beverage

- •Next-Following Application: Animal Feed

- •Dominating Region: Germany

- •Second-Leading Region: France

- •Region with Highest Growth Rate: France

- •Dominating Country: Germany

Market Share Table

- •Market Share (%) of Dominating vs Followed Type

- ◦Whole Grain Spelt: 45%

- ◦Organic Spelt: 30%

- •Market Share (%) of Dominating vs Followed Application

- ◦Food & Beverage: 55%

- ◦Animal Feed: 25%

- •Growth Rate (%) of Dominating vs Followed Type

- ◦Whole Grain Spelt: 8.7%

- ◦Organic Spelt: 12.4%

- •Growth Rate (%) of Dominating vs Followed Application

- ◦Food & Beverage: 9.2%

- ◦Animal Feed: 7.8%

Top Companies Profiled in Europe Spelt Wheat Market

- •BayWa AG (Germany)

- •Lantmännen Group (Sweden)

- •Agrana Beteiligungs-AG (Austria)

- •Cargill, Incorporated (Belgium)

- •Barilla Group (Italy)

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.5 Billion |

| Forecast Year Market Size | USD 3.8 Billion |

| CAGR | 9.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.1% |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | BayWa AG (Germany), Grain Millers Inc. (United Kingdom), Svenska Foder AB (Sweden), Agrana Beteiligungs-AG (Austria), Lantmännen Group (Sweden), Archer Daniels Midland Company (Germany), KWS SAAT SE & Co. KGaA (Germany), Bioland e.V. (Germany), Cargill, Incorporated (Belgium), Barilla Group (Italy), Bühler Group (Switzerland), Doves Farm Foods Ltd (United Kingdom), EcorNaturaSì (Italy), GoodMills Group (Austria), Hochland SE (Germany), Jordans & Ryvita Company (United Kingdom), Kamut International Ltd. (Switzerland), Lallemand Inc. (France), Mühle Lauenburg GmbH (Germany), Natracare Ltd (United Kingdom), Ökoland eG (Germany), Puratos Group (Belgium), Sachsenmilch GmbH (Germany), Tate & Lyle PLC (United Kingdom), Vandemoortele NV (Belgium) |

Europe Spelt Wheat Market Scope & Changing Dynamics 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.