EMEA Melamine Resin Market - Europe Industry Size & Growth Analysis 2025-2034

EMEA Melamine Resin Market is segmented by Type (Standard Melamine Resin, Modified Melamine Resin, Melamine Formaldehyde, Melamine Urea Formaldehyde, Other Specialty Resins), Application (Laminates, Adhesives, Molding Compounds, Coatings, Electrical Insulation), End-Use Industry (Construction, Automotive, Furniture & Interior, Electrical & Electronics, Packaging), Form (Liquid, Powder, Solid), Distribution Channel (Direct Sales, Distributors, Online Sales), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

- •The EMEA Melamine Resin market comprises the manufacture and application of melamine-based thermosetting polymers used extensively in laminates, adhesives, molding compounds, and coatings. These resins provide superior hardness, heat resistance, and chemical stability essential for sectors such as construction, automotive, and furniture manufacturing. The scope spans standard and modified melamine resins developed to meet evolving industrial and environmental regulations across Europe, the Middle East, and Africa. Rapid urbanization and industrial infrastructure growth drive demand for durable, high-performance materials, making melamine resins vital in modern manufacturing. Increased emphasis on sustainable production processes and formaldehyde reduction further defines market trends and innovation priorities.

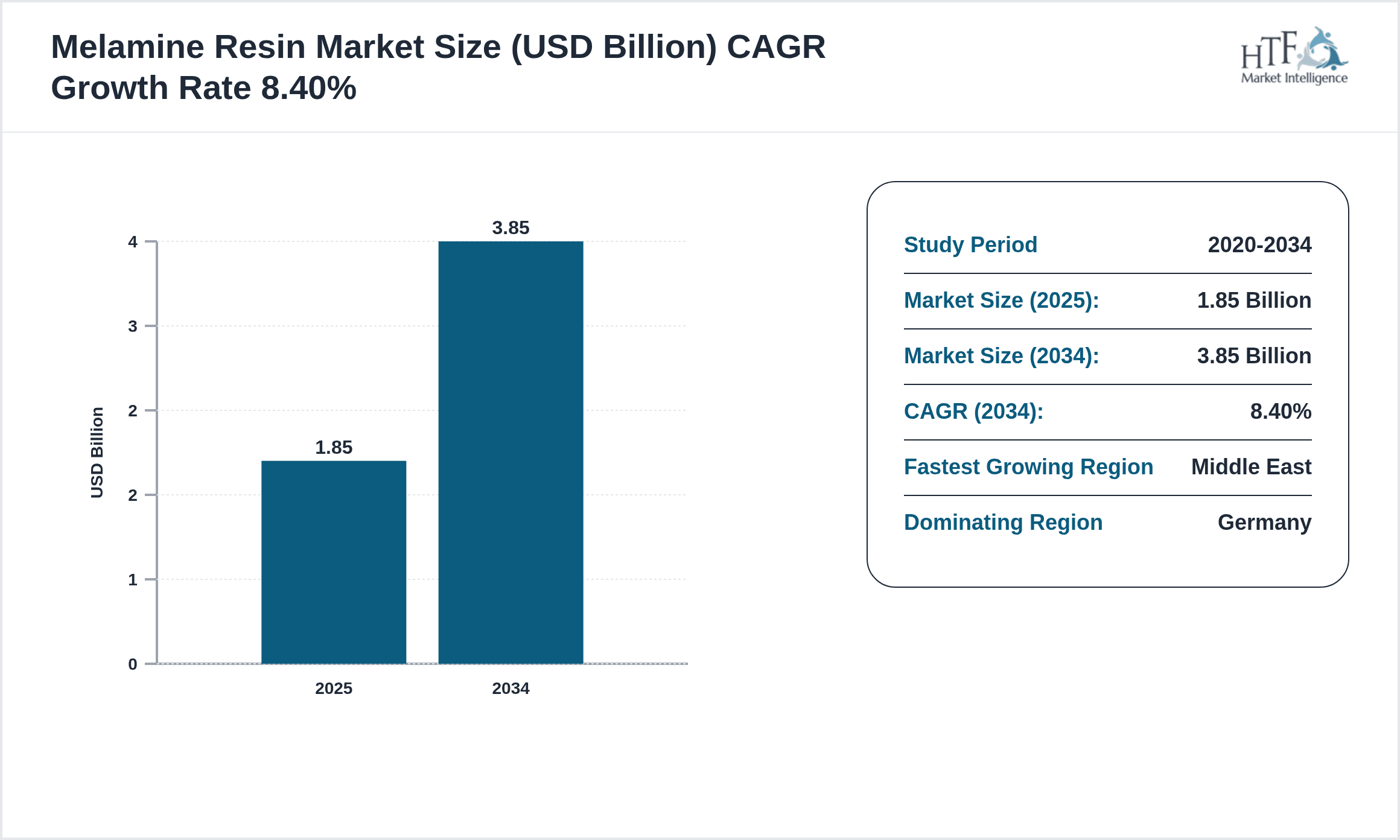

- •The market is valued at USD 1.85 Billion in 2025 and is forecasted to reach USD 3.85 Billion by 2034, registering a CAGR of 8.4%. Germany dominates the market with a 28% share, while the Middle East exhibits the fastest growth at 12.3% CAGR. Standard Melamine Resin leads product segments, but Modified Melamine Resin shows the highest growth potential. Key applications driving market volume include laminates and adhesives, reflecting strong demand in construction and automotive industries throughout EMEA.

- •The EMEA Melamine Resin market offers strategic value by enhancing product durability and aesthetic appeal across multiple industries. Stakeholders benefit from technological innovations, increasing formaldehyde-free resin adoption, and expanding infrastructure projects. The market’s growth aligns with environmental compliance and consumer preferences, positioning melamine resins as indispensable components in advanced manufacturing and sustainable product development within the region.

Competitive Landscape

Companies in the EMEA Melamine Resin market adopt multifaceted strategies including global expansion, strategic partnerships, and continuous product innovation to strengthen their market position. Adoption of eco-friendly technologies and reformulation to reduce formaldehyde emissions remain key approaches in product development. Firms actively collaborate with raw material suppliers and end-users to tailor resin properties for specific applications. Expansion into emerging Middle Eastern and African markets complements established European operations, leveraging regional infrastructure growth. Technological adoption such as advanced polymerization techniques and digital process controls enhances operational efficiency and product quality. Competitive pricing combined with diversified product portfolios enables players to address varying customer requirements while meeting stringent regulatory standards. Mergers and acquisitions are utilized to consolidate market share and expand technological capabilities. Overall, companies focus on sustainability, innovation, and regional market penetration to maintain and enhance their competitive edge in the EMEA melamine resin landscape.

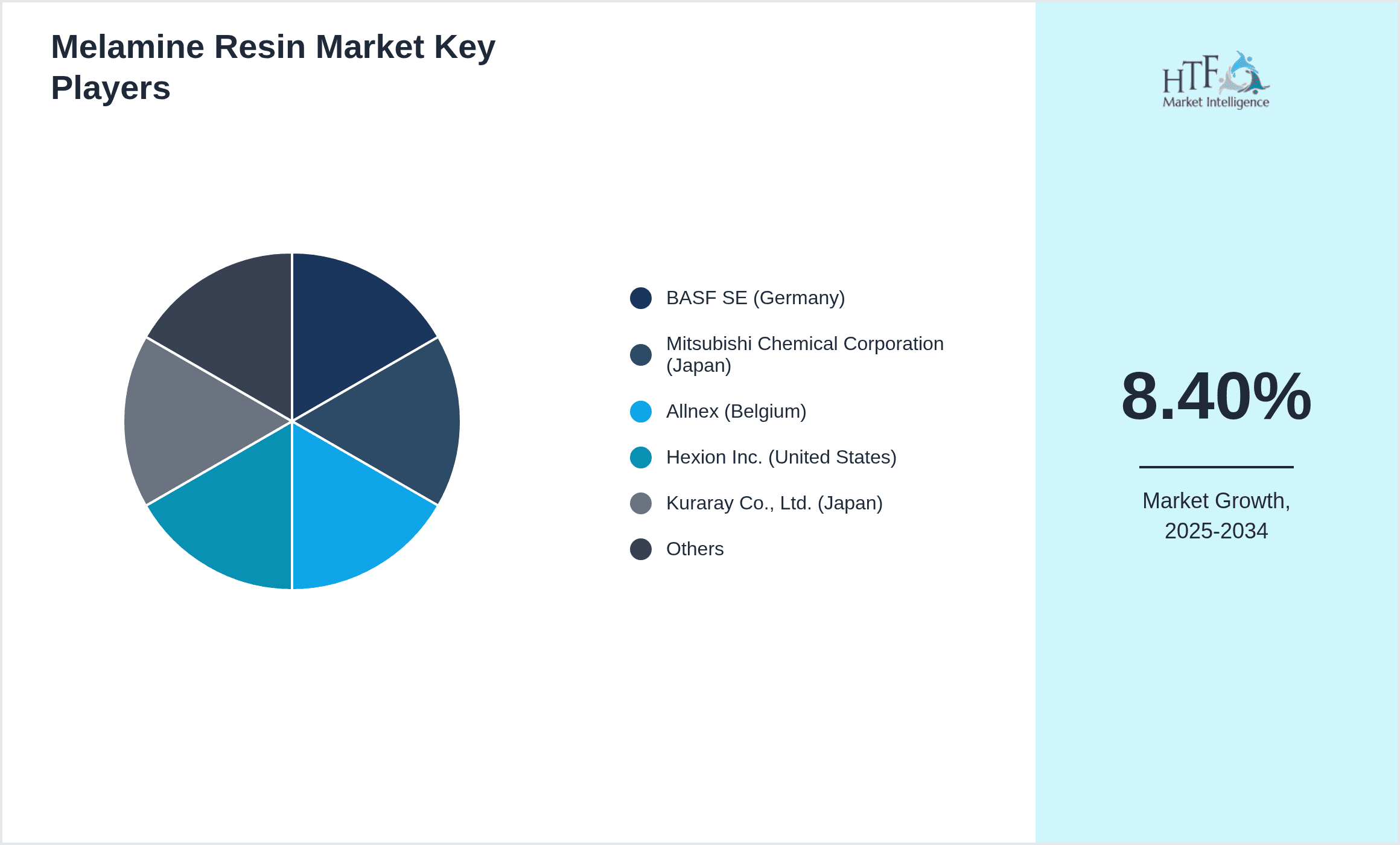

Leading Companies in Melamine Resin Market

- •BASF SE (Germany)

- •Mitsubishi Chemical Corporation (Japan)

- •Allnex (Belgium)

- •Hexion Inc. (United States)

- •Kuraray Co., Ltd. (Japan)

- •Trinseo S.A. (United States)

- •LG Chem Ltd. (South Korea)

- •DIC Corporation (Japan)

- •Sumitomo Bakelite Company Limited (Japan)

- •Cymit Quimica SA (Spain)

- •Huntsman Corporation (United States)

- •Sika AG (Switzerland)

- •Polynt-Reichhold Group (Italy)

- •Sekisui Chemical Co., Ltd. (Japan)

- •DSM-Niaga (Netherlands)

- •AkzoNobel N.V. (Netherlands)

- •Covestro AG (Germany)

- •Wanhua Chemical Group (China)

- •Synthomer plc (United Kingdom)

- •Momentive Performance Materials Inc. (United States)

Market Segments

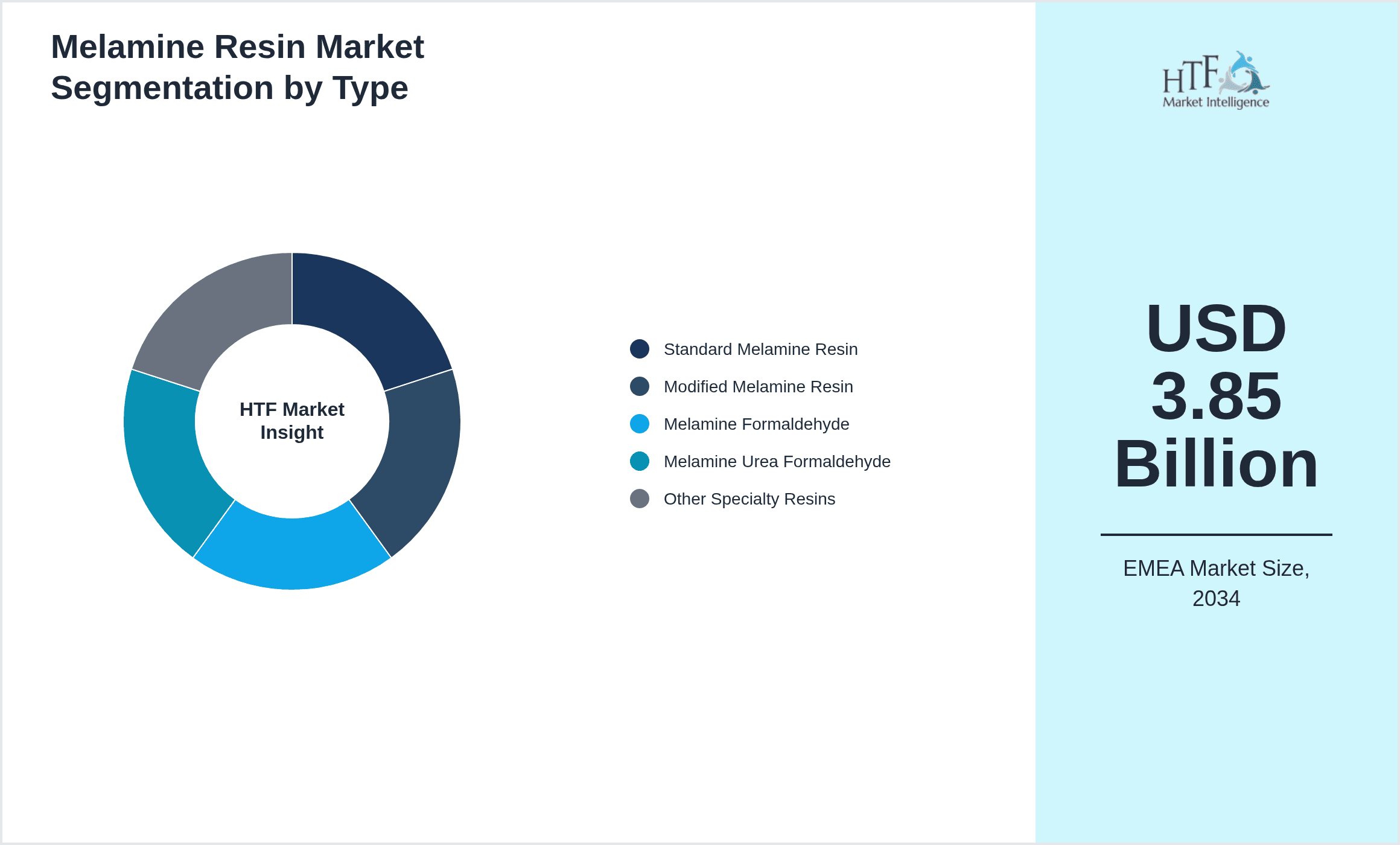

- •By Type

- ◦Standard Melamine Resin

- ◦Modified Melamine Resin

- ◦Melamine Formaldehyde

- ◦Melamine Urea Formaldehyde

- ◦Other Specialty Resins

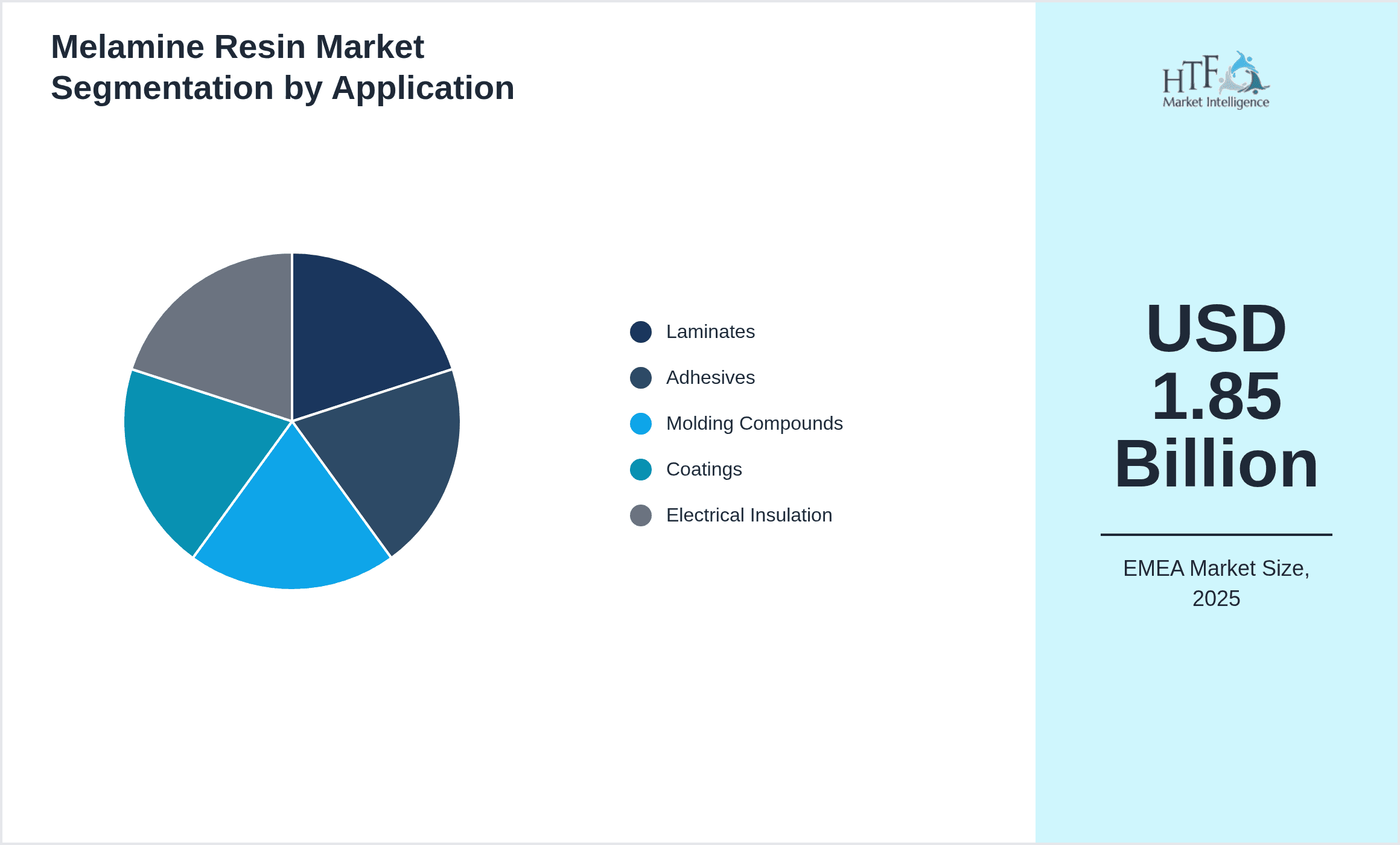

- •By Application

- ◦Laminates

- ◦Adhesives

- ◦Molding Compounds

- ◦Coatings

- ◦Electrical Insulation

- •By End-Use Industry

- ◦Construction

- ◦Automotive

- ◦Furniture & Interior

- ◦Electrical & Electronics

- ◦Packaging

- •By Form

- ◦Liquid

- ◦Powder

- ◦Solid

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Sales

Market Drivers

Rapid urbanization and infrastructure development across EMEA significantly increase demand for melamine resin-based laminates and adhesives, which offer superior durability and resistance properties critical for building materials. The automotive industry's expansion in Germany and France boosts demand for molding compounds and coatings, enhancing vehicle interiors and exteriors. Recent advancements by companies such as BASF SE in developing formaldehyde-reduced melamine resins align with stringent environmental regulations, propelling market growth. Additionally, rising consumer preference for sustainable and long-lasting furniture in the United Kingdom and Italy drives the use of melamine resins with improved scratch and heat resistance. Industrial investments in Middle Eastern countries further expand application scope, supporting the fastest growth in this sub-region. Introduction of innovative resin blends by players like Allnex enhances product versatility, meeting diversified industrial requirements. These factors collectively stimulate the EMEA melamine resin market, with continuous innovation and regional demand underpinning sustained growth.

Market Trend

The EMEA Melamine Resin market shows a rising trend toward eco-friendly and formaldehyde-free resin formulations driven by heightened regulatory pressures and consumer awareness. Companies actively invest in research and development to create bio-based and low-emission melamine resins, as seen in recent product launches by Sika AG and Covestro AG. Digitalization in manufacturing processes enables precision polymerization, improving product consistency and reducing waste. The expansion of smart laminates with integrated functionalities, such as antimicrobial and self-cleaning properties, is gaining traction in healthcare and hospitality sectors across Europe. Strategic collaborations between resin producers and end-user industries foster customized solutions, enhancing market penetration. Regional diversification into emerging African markets opens new avenues for application in construction and furniture industries. These trends reflect the market's shift toward sustainability, innovation, and regional expansion, positioning EMEA as a dynamic landscape for melamine resin advancements.

Market Opportunities

Expanding construction activities and infrastructure modernization projects in Middle Eastern countries and Africa provide substantial opportunities for melamine resin suppliers, particularly in laminates and adhesives sectors. The increasing adoption of green building standards across Europe drives demand for formaldehyde-free and environmentally compliant melamine resins, encouraging innovation in eco-friendly products. Growth in automotive production in Germany and Italy promotes the use of advanced molding compounds and coatings that enhance vehicle durability and aesthetics. Emerging applications in electrical insulation and packaging sectors reveal untapped potential for melamine resin formulations with improved fire resistance and mechanical strength. Collaborations between resin manufacturers and technology firms facilitate the development of smart materials, opening new market segments. Furthermore, digitization of supply chains and direct-to-customer sales models improve market reach and operational efficiency. These opportunities position the EMEA melamine resin market for robust expansion, supported by evolving industrial needs and sustainability priorities.

Market Challenges

Strict environmental regulations limiting formaldehyde emissions challenge manufacturers to reformulate melamine resins without compromising performance, necessitating costly R&D investments. Supply chain disruptions in raw materials due to geopolitical tensions in the Middle East and Africa create volatility in production costs and delivery schedules. High energy prices in Europe increase operational expenses, impacting profit margins across the resin production value chain. Intense competition from alternative resin types, such as urea-formaldehyde and phenolic resins, pressures market share and pricing flexibility. Recent recalls of laminates with substandard formaldehyde content in certain European countries highlight quality control challenges and potential reputational risks. Additionally, fluctuating demand in automotive and construction sectors due to economic uncertainties slows growth momentum. These challenges require manufacturers to enhance innovation capabilities, optimize supply chain resilience, and ensure stringent quality assurance to sustain competitive advantage in the EMEA melamine resin market.

Regulatory Framework

The EMEA melamine resin industry complies with multiple regulations targeting formaldehyde emissions and product safety introduced between 2020 and 2025. The European Chemicals Agency’s REACH regulation enforces strict limits on formaldehyde content in melamine resins, compelling manufacturers to adopt low-emission formulations. The EU’s Construction Products Regulation mandates certification of resin-based building materials to ensure environmental and health safety. Middle Eastern countries increasingly align with international standards, implementing formaldehyde emission thresholds and environmental compliance frameworks to regulate resin usage in construction and furniture industries. Additionally, the European Biocidal Products Regulation affects coatings and adhesives containing melamine resin by requiring authorization and risk assessments. These regulatory developments drive technological innovation and promote sustainable practices among market players, ensuring product safety and environmental stewardship in the EMEA region.

Recent Industry Insights

Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Recent Merger and Acquisition

Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Middle East is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.85 Billion |

| Forecast Year Market Size | USD 3.85 Billion |

| CAGR | 8.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.1% |

| Scope of Report | Market is segmented by Type (Standard Melamine Resin, Modified Melamine Resin, Melamine Formaldehyde, Melamine Urea Formaldehyde, Other Specialty Resins), Application (Laminates, Adhesives, Molding Compounds, Coatings, Electrical Insulation), End-Use Industry (Construction, Automotive, Furniture & Interior, Electrical & Electronics, Packaging), Form (Liquid, Powder, Solid), Distribution Channel (Direct Sales, Distributors, Online Sales) |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | BASF SE (Germany), Mitsubishi Chemical Corporation (Japan), Allnex (Belgium), Hexion Inc. (United States), Kuraray Co., Ltd. (Japan), Trinseo S.A. (United States), LG Chem Ltd. (South Korea), DIC Corporation (Japan), Sumitomo Bakelite Company Limited (Japan), Cymit Quimica SA (Spain), Huntsman Corporation (United States), Sika AG (Switzerland), Polynt-Reichhold Group (Italy), Sekisui Chemical Co., Ltd. (Japan), DSM-Niaga (Netherlands), AkzoNobel N.V. (Netherlands), Covestro AG (Germany), Wanhua Chemical Group (China), Synthomer plc (United Kingdom), Momentive Performance Materials Inc. (United States) |

EMEA Melamine Resin Market - Europe Industry Size & Growth Analysis 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.