Europe Gypsum Boards Market - Europe Size & Outlook 2025-2034

Europe Gypsum Boards Market is segmented by Type (Standard Gypsum Board, Moisture-Resistant Gypsum Board, Fire-Resistant Gypsum Board, Soundproof Gypsum Board, Mold-Resistant Gypsum Board), Application (Residential Construction, Commercial Buildings, Renovation & Remodeling, Institutional Buildings, Industrial Facilities), End User (Contractors, Architects & Designers, Real Estate Developers, Government & Public Sector), Distribution Channel (Direct Sales, Distributors & Wholesalers, Retail Stores, Online Channels), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Gypsum Boards market consists of gypsum-based panels used primarily in interior construction for walls and ceilings. It covers diverse product types including standard, moisture-resistant, fire-resistant, soundproof, and mold-resistant boards. Applications span residential, commercial, institutional, and industrial buildings. The market's scope includes raw material sourcing, manufacturing processes, and distribution within major European countries such as Germany, France, UK, Italy, and Spain. Gypsum boards offer benefits like fire protection, moisture control, and acoustic insulation, making them critical for modern building standards and regulations. The industry supports sustainable construction practices and aligns with evolving safety norms across Europe.

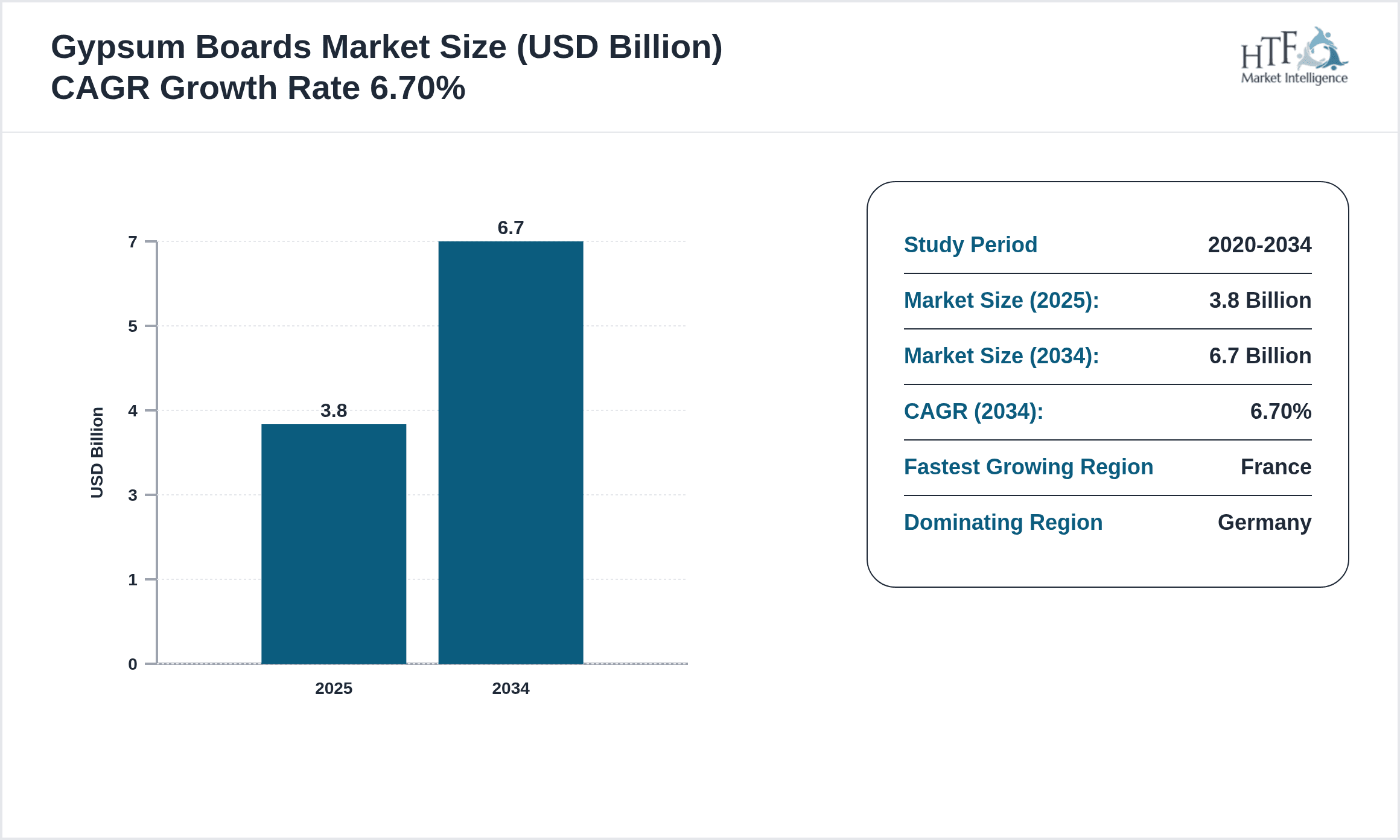

- •The market is projected to grow from USD 3.8 Billion in 2025 to USD 6.7 Billion by 2034, exhibiting a CAGR of 6.7%. Germany dominates with a 24% market share, followed by France and the UK. Standard gypsum boards lead product demand, while moisture-resistant variants are the fastest growing due to increasing construction in humid environments. Rising urbanization, renovation activities, and regulatory emphasis on fire and moisture safety drive market expansion.

- •Gypsum boards represent a strategic construction material in Europe, offering cost-effective, sustainable, and versatile solutions for building interiors. Their importance spans multiple sectors, enabling compliance with stringent European building codes. Industry stakeholders benefit from ongoing innovation in product types and manufacturing technologies, positioning gypsum boards as a vital component of Europe's evolving construction landscape.

Competitive Landscape

Competition in the Europe Gypsum Boards market is characterized by a mix of multinational corporations and regional manufacturers focusing on product innovation, quality enhancement, and sustainability. Leading companies invest heavily in R&D to develop advanced gypsum boards offering superior fire resistance, moisture protection, and acoustic performance. Market rivalry centers on expanding distribution networks and strategic partnerships with construction firms. Pricing strategies balance cost competitiveness with premium product offerings addressing niche segments like mold-resistant boards. Regional players capitalize on localized supply chains and customization capabilities to serve diverse European markets. Mergers, acquisitions, and collaborations are frequent, enabling companies to consolidate market share and enhance technological capabilities. The competitive environment also reflects stringent regulatory compliance, pushing companies toward greener manufacturing practices. Overall, innovation, quality differentiation, and strategic alliances shape the competitive dynamics within the European gypsum boards industry.

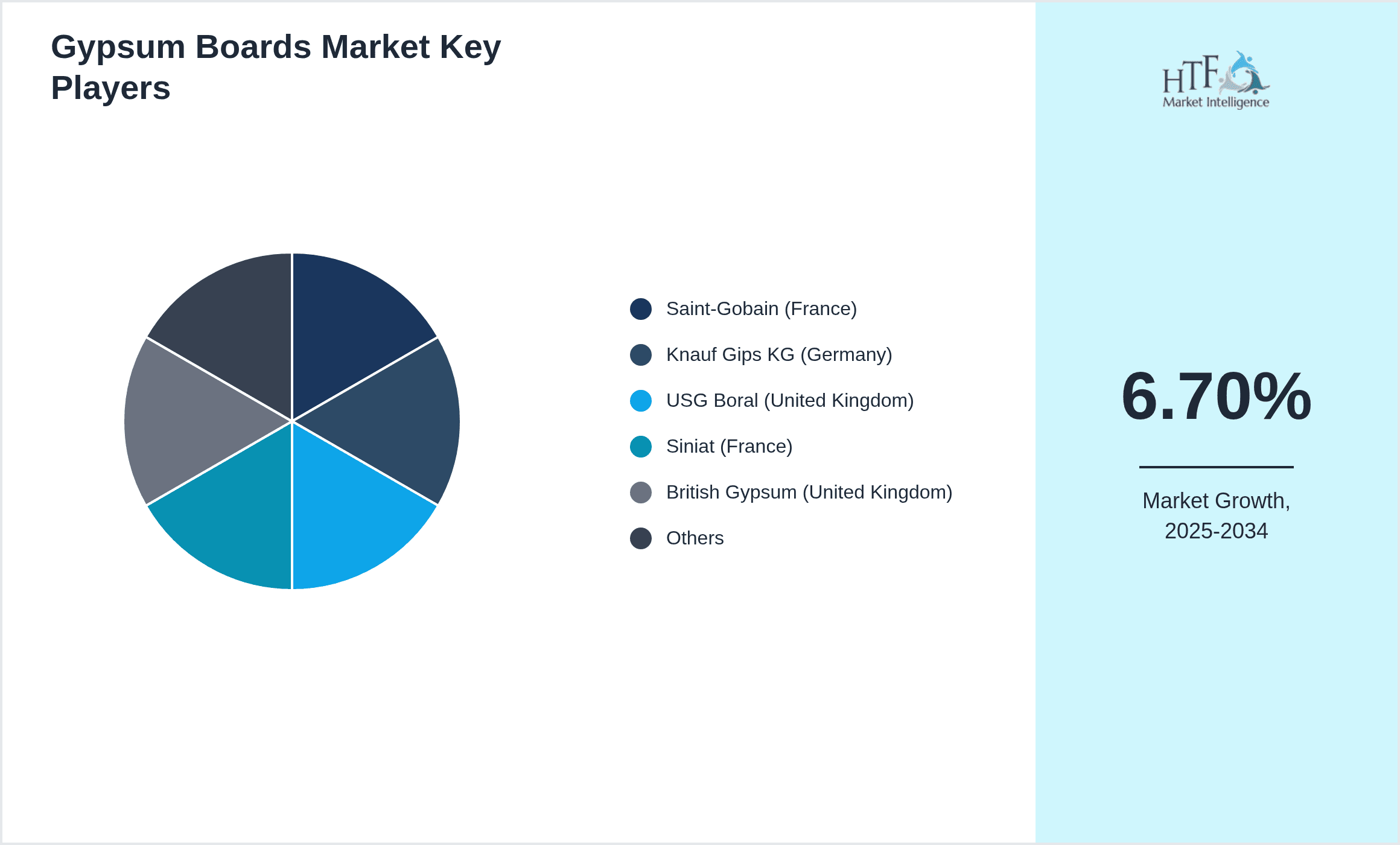

Leading Companies in Gypsum Boards Market

- •Saint-Gobain (France)

- •Knauf Gips KG (Germany)

- •USG Boral (United Kingdom)

- •Siniat (France)

- •British Gypsum (United Kingdom)

- •Etex Group (Belgium)

- •National Gypsum Company (Germany)

- •Rigips (Germany)

- •Fermacell (Austria)

- •Gyproc (United Kingdom)

- •Knauf Insulation (Germany)

- •LafargeHolcim (Switzerland)

- •Saint-Gobain Weber (France)

- •Fermacell GmbH (Austria)

- •Gypsum Industries (South Africa)

- •Gyproc Saint-Gobain (France)

- •Siniat GmbH (Germany)

- •British Plasterboard Ltd (United Kingdom)

- •Knauf AMF (Germany)

- •Etex Building Performance (Belgium)

- •Rigips GmbH (Germany)

- •USG Corporation (United States)

- •Siniat SA (France)

- •British Gypsum Ltd (United Kingdom)

- •Gyproc UK (United Kingdom)

Market Breakdown

- •By Type

- ◦Standard Gypsum Board

- ◦Moisture-Resistant Gypsum Board

- ◦Fire-Resistant Gypsum Board

- ◦Soundproof Gypsum Board

- ◦Mold-Resistant Gypsum Board

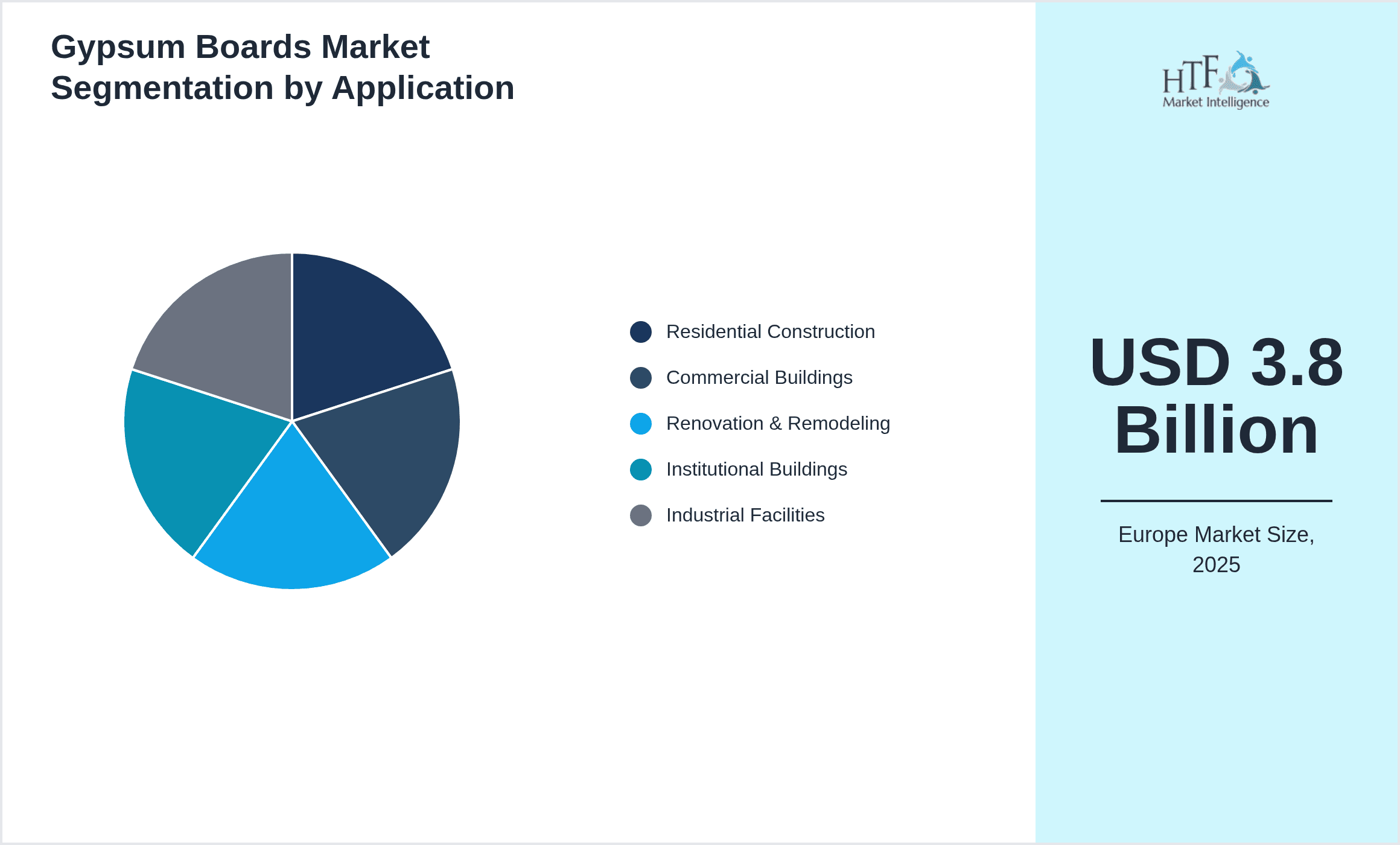

- •By Application

- ◦Residential Construction

- ◦Commercial Buildings

- ◦Renovation & Remodeling

- ◦Institutional Buildings

- ◦Industrial Facilities

- •By End User

- ◦Contractors

- ◦Architects & Designers

- ◦Real Estate Developers

- ◦Government & Public Sector

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Wholesalers

- ◦Retail Stores

- ◦Online Channels

Growth Drivers

The Europe Gypsum Boards market growth is driven by rising urbanization and increasing construction activities within residential and commercial sectors. Demand for fire-resistant and moisture-resistant boards is propelled by stringent European building regulations emphasizing safety and durability. Renovation and remodeling projects in mature markets like Germany and the UK fuel steady demand. Technological advancements improving board performance and ease of installation also stimulate uptake. Additionally, growing awareness about sustainable construction materials enhances gypsum boards' appeal due to their recyclability and low environmental impact. Government incentives promoting energy-efficient buildings further accelerate market expansion. The rising preference for interior design flexibility and acoustic insulation in commercial and institutional buildings supports product adoption. Overall, these factors collectively underpin a robust growth trajectory for gypsum boards across Europe.

Market Trends

Current trends in the Europe Gypsum Boards market include increasing integration of eco-friendly raw materials and adoption of circular economy principles by manufacturers. There is a growing emphasis on developing lightweight, high-performance boards with enhanced fire and moisture resistance tailored for diverse applications. Digitalization in manufacturing processes improves quality control and production efficiency. The rise of prefabricated construction and modular building techniques boosts the demand for standardized gypsum products. Industry players focus on expanding sustainable product portfolios to meet evolving consumer and regulatory demands. Additionally, partnerships between gypsum manufacturers and construction companies promote innovative building solutions. The trend towards smart buildings with improved insulation and soundproofing also drives customization and technological innovation in gypsum boards.

Restraints

Challenges restraining the Europe Gypsum Boards market include fluctuating raw material prices, particularly gypsum and additives, which can impact manufacturing costs. Supply chain disruptions due to geopolitical tensions and logistics constraints affect timely product availability. The market faces competition from alternative interior materials such as cement boards and fiber cement panels, which offer different performance characteristics. High energy consumption and CO2 emissions associated with gypsum board production pose environmental concerns, potentially leading to stricter regulations and increased operational costs. Additionally, skilled labor shortages in the construction sector may slow project execution, affecting demand. Variability in regional building codes and standards across European countries complicate product standardization and market penetration efforts. These factors collectively constrain market growth momentum.

Market Opportunities

Emerging opportunities in the Europe Gypsum Boards market arise from rising investments in green building projects emphasizing sustainable materials. Growing demand for enhanced fire and moisture-resistant gypsum boards in healthcare and educational facilities presents new applications. Expansion in refurbishment and retrofit projects across aging European infrastructure drives replacement demand. Technological innovations enabling thinner, lighter boards with improved strength open avenues in modular and prefabricated construction. Increasing adoption of digital tools for customized product specifications facilitates tailored solutions for architects and builders. Opportunities also exist in expanding distribution channels, including e-commerce platforms, enhancing market accessibility. Collaborations between manufacturers and construction technology firms to integrate smart features in gypsum boards offer future growth potential. Regulatory support for energy-efficient materials further incentivizes market expansion.

Market Challenges

The Europe Gypsum Boards market faces challenges including intense competition among established players, leading to pricing pressures and margin erosion. Adherence to diverse and evolving regional regulatory requirements increases compliance complexity and costs. Environmental concerns regarding gypsum mining and waste disposal necessitate significant investments in sustainable practices. Fluctuations in construction activity due to economic uncertainties or pandemics can lead to demand volatility. The complexity of integrating new technologies into traditional manufacturing processes poses operational hurdles. Limited awareness among smaller contractors and end-users about advanced gypsum board benefits slows adoption. Furthermore, transportation costs and carbon footprint considerations affect distribution strategies. Addressing these challenges requires strategic innovation, regulatory alignment, and market education initiatives.

Regulatory Framework

From 2020 to 2025, Europe has implemented stringent regulations impacting gypsum boards, including the Construction Products Regulation (CPR) mandating harmonized standards for fire performance and safety across member states. Countries enforce specific requirements for moisture and mold resistance aligned with EU environmental directives focusing on indoor air quality and sustainability. The EcoDesign Directive influences manufacturing processes by setting energy efficiency and emission reduction targets for building materials. Waste management regulations promote recycling of gypsum waste, encouraging circular economy models. National building codes in Germany, France, and the UK have updated guidelines for acoustic insulation and thermal performance, directly affecting gypsum board specifications. Compliance with REACH regulations ensures safe use of chemical substances in gypsum products. These evolving regulatory frameworks shape product development, certification, and market entry strategies across Europe.

Market Intelligence

- •In March 2024, Saint-Gobain launched an innovative moisture-resistant gypsum board designed for high-humidity environments, targeting residential and commercial construction segments. This product integrates advanced water-repellent technologies improving durability and reducing installation time. The launch reinforces Saint-Gobain's market leadership in Europe by addressing growing demand for specialized boards amid increasing renovation projects in coastal and humid regions. The company also emphasized sustainability aspects with a 30% reduction in embodied carbon compared to conventional boards, aligning with European green building initiatives. This strategic introduction is expected to accelerate adoption in France, Germany, and the UK.

- •In November 2023, Knauf Gips KG expanded its production capacity in Germany with a new state-of-the-art gypsum board manufacturing facility. The expansion aims to meet rising demand for fire-resistant and soundproof boards driven by regulatory changes and urbanization. The facility incorporates Industry 4.0 technologies for enhanced efficiency and quality control, positioning Knauf to capitalize on emerging market opportunities. The investment reflects the company’s commitment to sustainable manufacturing practices, including waste reduction and energy optimization.

Mergers & Acquisitions

- •In July 2023, Etex Group completed the acquisition of Fermacell GmbH, a leading Austrian gypsum board manufacturer specializing in high-performance construction panels. This strategic move expanded Etex’s product portfolio and strengthened its foothold in Central Europe’s gypsum boards market. The acquisition enables synergies in R&D and distribution, accelerating innovation in moisture-resistant and fireproof products. It also enhances Etex’s ability to serve large-scale infrastructure and renovation projects across Europe, aligning with sustainable construction trends and regulatory compliance requirements.

- •In January 2022, USG Boral merged with a regional gypsum panel producer in the UK to consolidate its market position in Europe. The merger facilitated expanded manufacturing capacity and improved supply chain efficiencies. It allowed the combined entity to introduce new product lines targeting specific applications such as institutional buildings and industrial facilities. The alignment of technological expertise and distribution networks has enhanced competitive advantage against other major European players, supporting long-term growth objectives.

Recent Industry News

- •In May 2024, Saint-Gobain announced a partnership with a leading European construction technology firm to develop smart gypsum boards embedded with sensors for real-time monitoring of moisture and structural integrity. This innovation aims to enhance building safety and maintenance efficiency, particularly in public infrastructure and commercial buildings. The collaboration combines advanced materials science with digital technology, positioning both companies at the forefront of smart construction solutions in Europe. Source: Saint-Gobain Official Press Release

- •In September 2023, Knauf Gips KG inaugurated a new logistics hub in Rotterdam, Netherlands, to streamline gypsum board distribution across Western Europe. The facility utilizes automated inventory management and eco-friendly transport options, reducing delivery times and carbon emissions. This expansion supports Knauf's growth strategy focused on improving customer service and sustainability. Source: Knauf Corporate News

- •In February 2022, British Gypsum launched a new line of fire-resistant gypsum boards specifically designed for healthcare facilities, complying with updated EU fire safety regulations. The product features enhanced durability and quick installation benefits, addressing the increasing demand for hospital construction and renovation projects across the UK and Europe. Source: British Gypsum Industry Update

- •In August 2021, Etex Group announced the expansion of its R&D center in Belgium focused on developing next-generation gypsum boards with improved acoustic and thermal insulation properties. The investment supports innovation targeting green building certifications and energy-efficient construction trends prevalent in Europe. Source: Etex Group Annual Report

Market Statistics

- •CAGR by 2034: 6.7%

- •Market Size by 2034: USD 6.7 Billion

- •Market Size in 2025: USD 3.8 Billion

- •Dominating Type: Standard Gypsum Board

- •Next-Following Type: Moisture-Resistant Gypsum Board

- •Dominating Application: Residential Construction

- •Next-Following Application: Commercial Buildings

- •Dominating Region: Germany

- •Second-Leading Region: France

- •Region with Highest Growth Rate: France (8.4% CAGR)

- •Dominating Country: Germany

Market Share Table

- •Market Share (%) - Standard Gypsum Board: 45%, Moisture-Resistant Gypsum Board: 25%

- •Market Share (%) - Residential Construction: 40%, Commercial Buildings: 30%

- •Growth Rate (%) - Standard Gypsum Board: 5.8%, Moisture-Resistant Gypsum Board: 9.3%

- •Growth Rate (%) - Residential Construction: 6.0%, Commercial Buildings: 7.2%

Top 5 Global Players

- •Saint-Gobain (France)

- •Knauf Gips KG (Germany)

- •USG Boral (United Kingdom)

- •Siniat (France)

- •British Gypsum (United Kingdom)

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.8 Billion |

| Forecast Year Market Size | USD 6.7 Billion |

| CAGR | 6.7% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6.5% |

| Scope of Report | Market is segmented by Type (Standard Gypsum Board, Moisture-Resistant Gypsum Board, Fire-Resistant Gypsum Board, Soundproof Gypsum Board, Mold-Resistant Gypsum Board), Application (Residential Construction, Commercial Buildings, Renovation & Remodeling, Institutional Buildings, Industrial Facilities), End User (Contractors, Architects & Designers, Real Estate Developers, Government & Public Sector), Distribution Channel (Direct Sales, Distributors & Wholesalers, Retail Stores, Online Channels) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Saint-Gobain (France), Knauf Gips KG (Germany), USG Boral (United Kingdom), Siniat (France), British Gypsum (United Kingdom), Etex Group (Belgium), National Gypsum Company (Germany), Rigips (Germany), Fermacell (Austria), Gyproc (United Kingdom), Knauf Insulation (Germany), LafargeHolcim (Switzerland), Saint-Gobain Weber (France), Fermacell GmbH (Austria), Gypsum Industries (South Africa), Gyproc Saint-Gobain (France), Siniat GmbH (Germany), British Plasterboard Ltd (United Kingdom), Knauf AMF (Germany), Etex Building Performance (Belgium), Rigips GmbH (Germany), USG Corporation (United States), Siniat SA (France), British Gypsum Ltd (United Kingdom), Gyproc UK (United Kingdom) |

Europe Gypsum Boards Market - Europe Size & Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.