Middle East Orthopedic Braces & Support Casting & Splint Market Size, Growth & Revenue 2024-2034

Middle East Orthopedic Braces & Support Casting & Splint Market is segmented by Type (Rigid Braces, Soft Braces, Semi-Rigid Braces, Casting Materials, Splints), Application (Fracture Management, Joint Support, Post-Surgical Care, Rehabilitation, Sports Injuries), End User (Hospitals, Orthopedic Clinics, Rehabilitation Centers, Home Care), Distribution Channel (Direct Sales, Medical Distributors, Online Retailers, Pharmacies), and Geography (Turkey, Egypt, United Arab Emirates, Saudi Arabia, Israel, Others)

Pricing

Report Overview

Executive Summary

- •The Middle East Orthopedic Braces & Support Casting & Splint market involves medical devices designed to support, immobilize, or correct musculoskeletal injuries, including rigid and soft braces, casting materials, and splints used primarily in fracture management, joint support, post-surgical care, rehabilitation, and sports injury treatment.

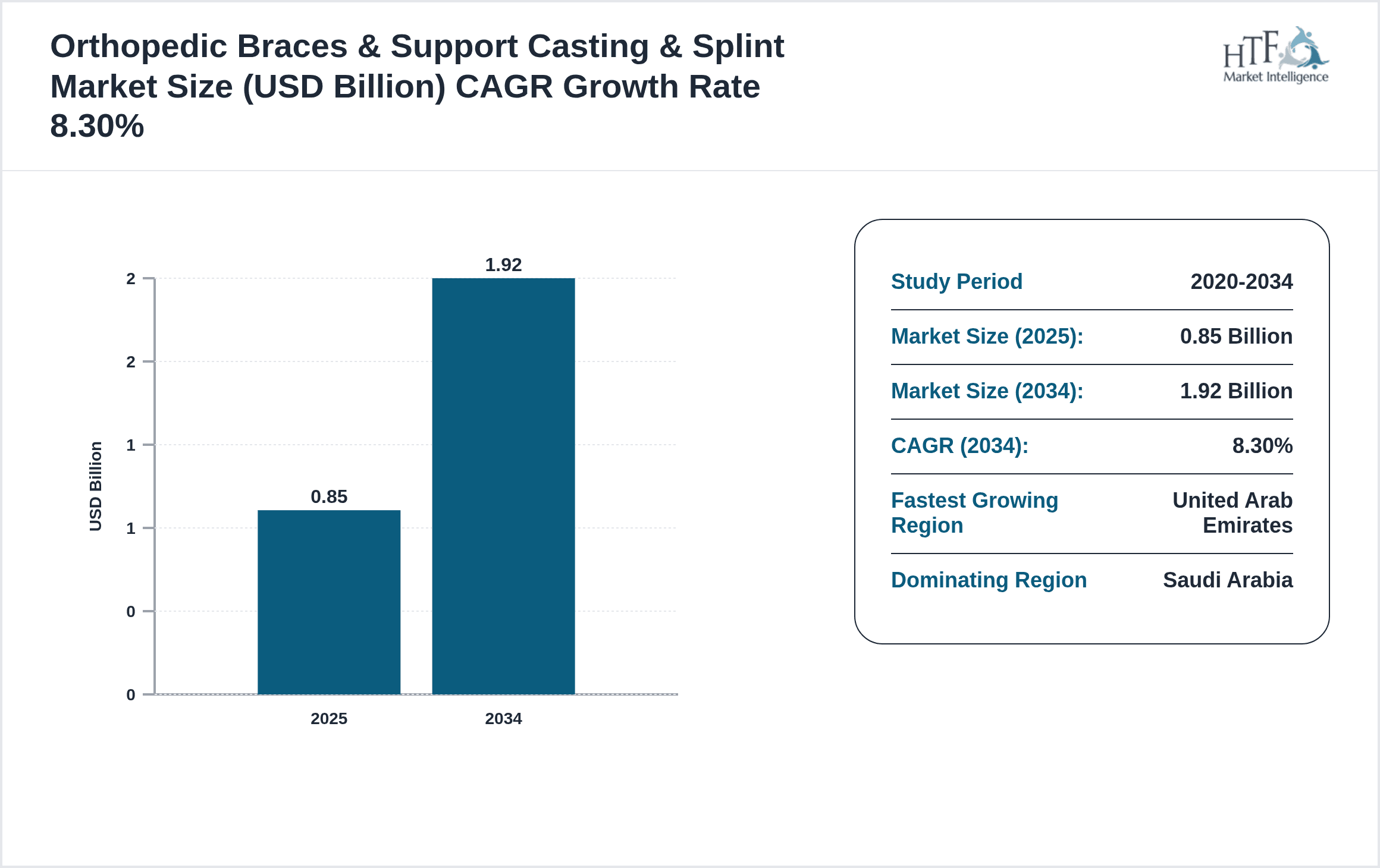

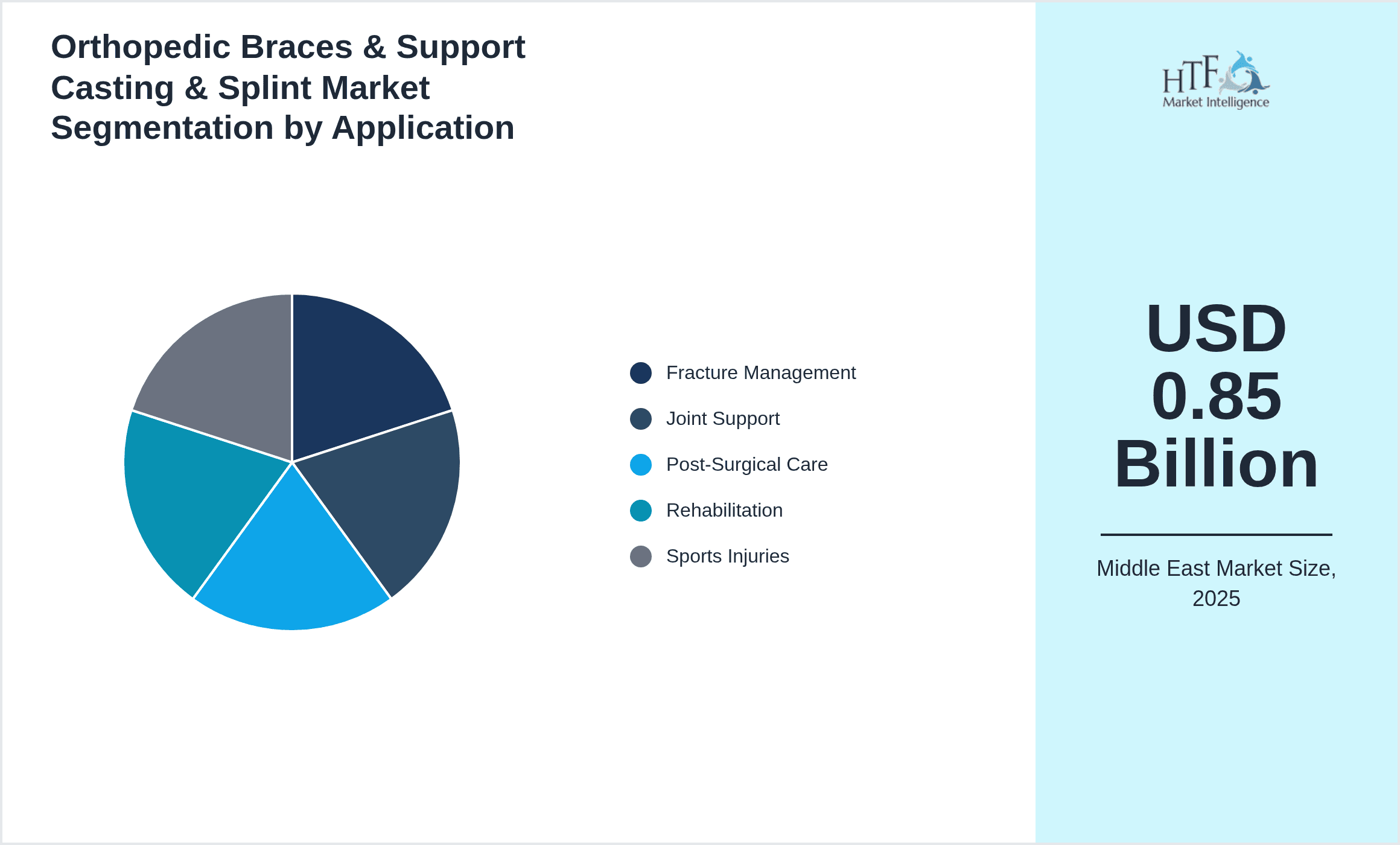

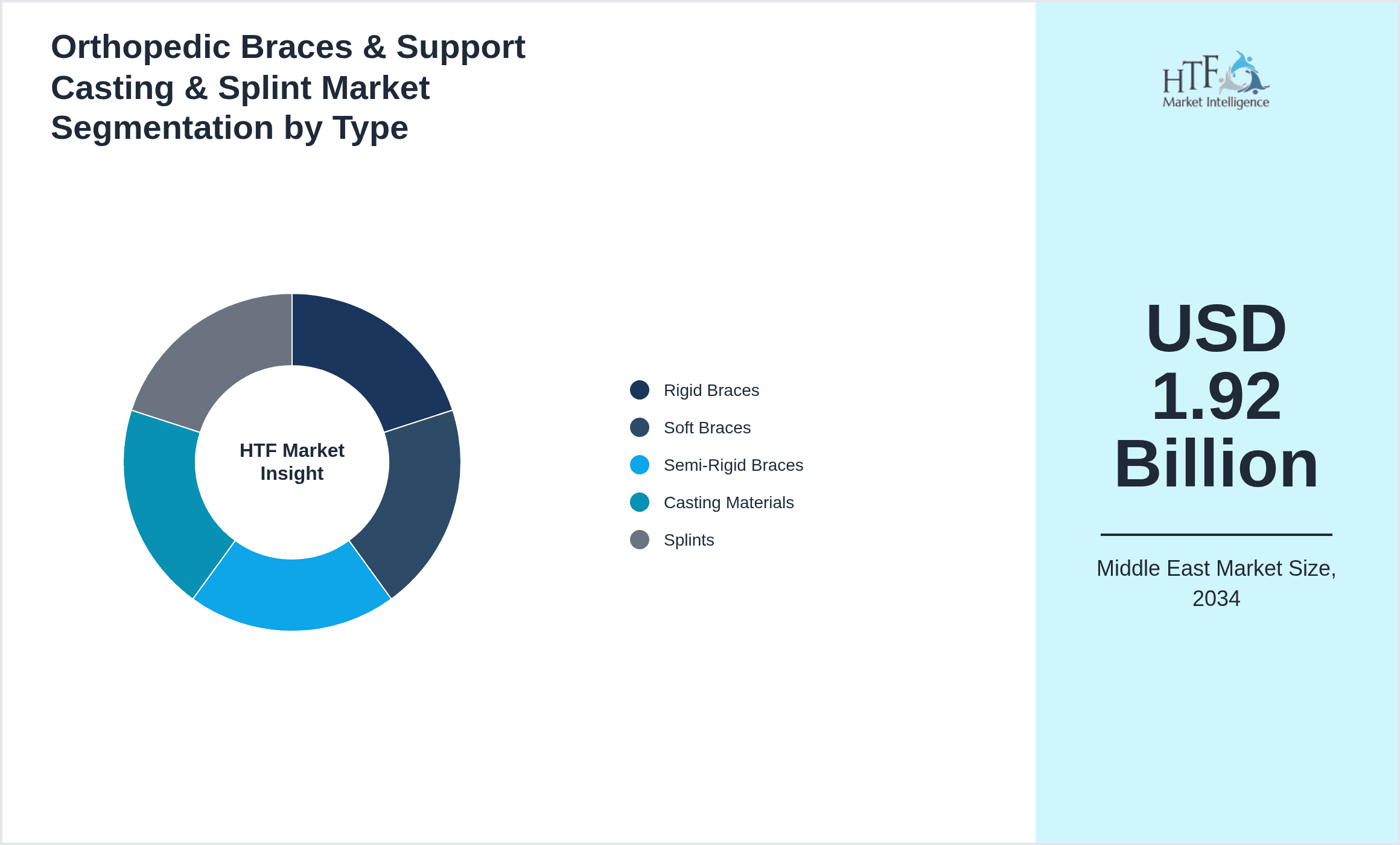

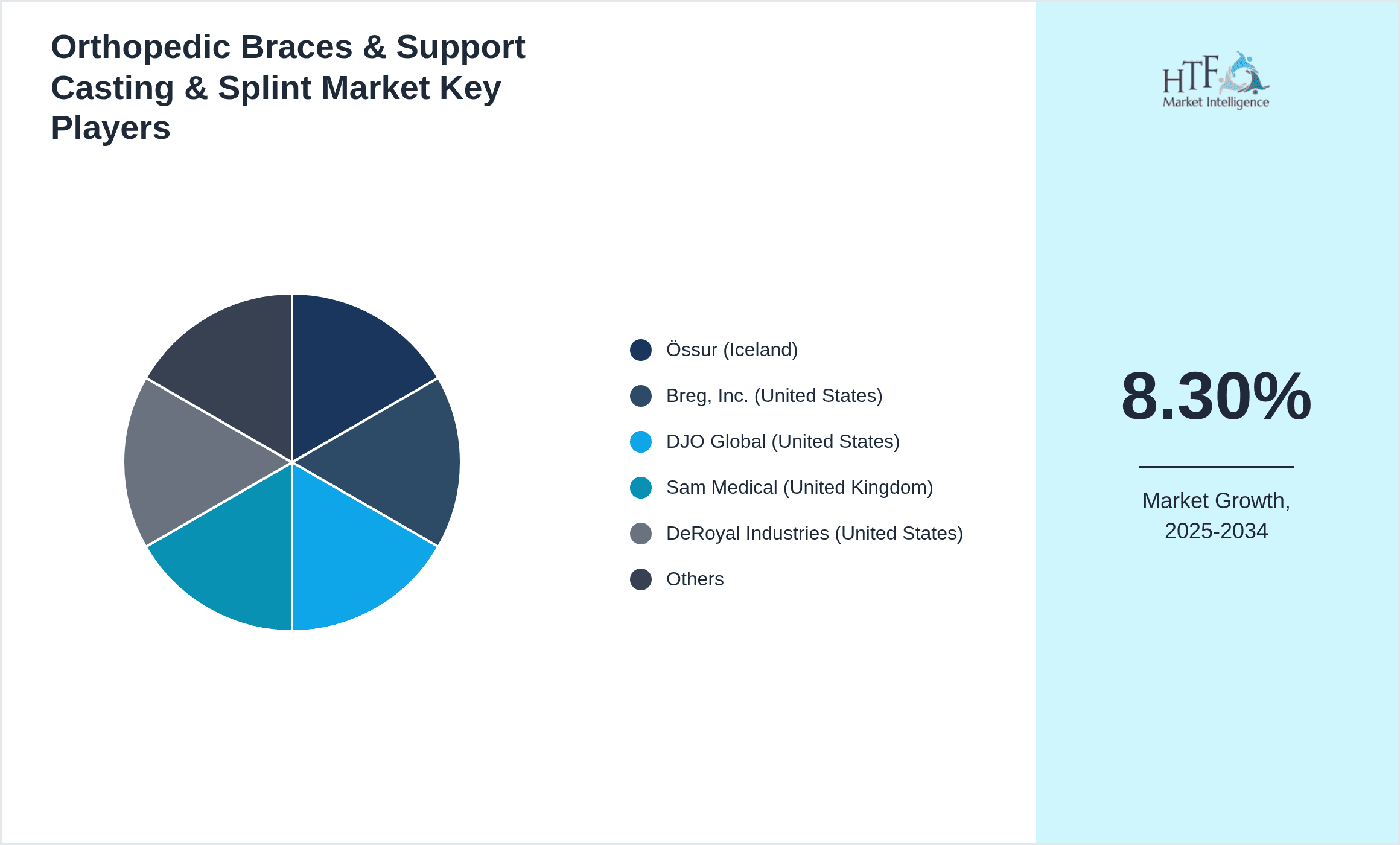

- •Key market highlights include a base market size of USD 0.85 Billion in 2024, projected to reach USD 1.92 Billion by 2034, with a CAGR of 8.3%, driven by rising orthopedic conditions and technological innovations in product design and materials.

- •The market's strategic importance lies in enhancing patient recovery and mobility across healthcare facilities in major Middle Eastern countries such as Saudi Arabia and UAE, supporting growth in orthopedic care infrastructure and personalized treatment solutions.

Competitive Landscape

Competition within the Middle East Orthopedic Braces & Support Casting & Splint market is characterized by a mix of international and regional players focusing on product innovation, strategic partnerships, and localized manufacturing. Companies compete on technological advancements, customization capabilities, and distribution networks to enhance market share. The rivalry encourages continuous development of lightweight, durable, and patient-friendly devices. Market positioning is driven by brand reputation, regulatory compliance, and service support. Innovation approaches include integration of smart materials and comfort-enhancing designs. The market experiences moderate entry barriers due to regulatory requirements and the need for clinical validation. Regional competition is intensified by rapid healthcare infrastructure growth in GCC countries, while companies leverage strategic alliances to expand footprints and optimize supply chains.

Leading Companies in Orthopedic Braces & Support Casting & Splint Market

- •Össur (Iceland)

- •Breg, Inc. (United States)

- •DJO Global (United States)

- •Sam Medical (United Kingdom)

- •DeRoyal Industries (United States)

- •Medline Industries (United States)

- •Orthofix International (United States)

- •Allard USA (United States)

- •Zimmer Biomet Holdings, Inc. (United States)

- •Hely & Weber (Germany)

- •BSN Medical (Germany)

- •Porplastic (United Kingdom)

- •Beijing Kangyi Medical (China)

- •Al Hayat Pharmaceuticals (Middle East)

- •Al Zahrawi Medical Supplies (Middle East)

Market Breakdown

- •By Type

- ◦Rigid Braces

- ◦Soft Braces

- ◦Semi-Rigid Braces

- ◦Casting Materials

- ◦Splints

- •By Application

- ◦Fracture Management

- ◦Joint Support

- ◦Post-Surgical Care

- ◦Rehabilitation

- ◦Sports Injuries

- •By End User

- ◦Hospitals

- ◦Orthopedic Clinics

- ◦Rehabilitation Centers

- ◦Home Care

- •By Distribution Channel

- ◦Direct Sales

- ◦Medical Distributors

- ◦Online Retailers

- ◦Pharmacies

Growth Drivers

- •Increasing prevalence of orthopedic disorders such as fractures, arthritis, and sports injuries in Middle East populations is driving demand for orthopedic braces and support devices, supported by growing geriatric demographics and rising accident rates.

- •Advancements in lightweight, durable materials and customizable braces and splints enhance patient comfort and efficacy, attracting healthcare providers and patients to adopt innovative orthopedic support solutions.

- •Expansion of healthcare infrastructure and orthopedic specialty clinics in GCC countries like Saudi Arabia and UAE is boosting accessibility and adoption of advanced orthopedic support devices.

- •Government initiatives promoting healthcare modernization and increased healthcare expenditure in Middle Eastern countries stimulate market growth by improving availability and reimbursement for orthopedic care.

- •Rising awareness about non-surgical orthopedic treatments and rehabilitation practices encourages patients and clinicians to prefer braces and splints for effective management of musculoskeletal conditions.

Market Trends

- •Adoption of 3D printing technology to produce patient-specific orthopedic braces and splints is gaining traction, enabling enhanced fit, lightweight designs, and faster production cycles in the Middle East market.

- •Integration of smart sensors and wearable technology in braces to monitor patient movement and compliance is an emerging trend, improving treatment outcomes and remote patient management.

- •Increasing partnerships between global orthopedic device manufacturers and regional distributors facilitate market penetration and tailored product offerings for the Middle East healthcare sector.

- •Growth in sports medicine and fitness sectors is driving demand for advanced joint support braces among athletes and active populations in urban centers of the Middle East.

- •Sustainability concerns are encouraging manufacturers to develop eco-friendly casting materials and recyclable splints, aligning with regional environmental initiatives.

Market Restraints

- •High cost of advanced orthopedic braces and casting materials limits accessibility among lower-income populations in some Middle Eastern countries, constraining widespread adoption.

- •Lack of skilled orthopedic specialists and technicians in rural areas reduces the effective deployment and fitting of orthopedic support devices, impacting market growth.

- •Stringent regulatory approval processes and variations across Middle Eastern countries delay product launches and increase compliance costs for manufacturers.

- •Cultural preferences and lack of awareness about non-surgical orthopedic treatments in certain regions hinder demand for braces and splints relative to surgical interventions.

- •Competition from low-cost local manufacturers offering basic orthopedic support products affects pricing and margins of international brands.

Market Opportunities

- •Increasing investments in telemedicine and remote orthopedic care open opportunities for smart braces integrated with digital monitoring to improve patient adherence and outcomes.

- •Expanding orthopedic rehabilitation centers and home care services in the Middle East create demand for portable, easy-to-use braces and splints designed for outpatient use.

- •Untapped markets in emerging Middle Eastern countries like Oman and Kuwait offer growth prospects for manufacturers through tailored product portfolios and localized marketing strategies.

- •Collaborations with sports medicine clinics and fitness centers provide channels to introduce advanced joint support solutions targeting injury prevention and recovery.

- •Development of biodegradable and skin-friendly materials for casting and splinting aligns with patient comfort trends and regulatory emphasis on environmental sustainability.

Market Challenges

- •Ensuring consistent quality and safety standards across diverse suppliers and distributors in the Middle East remains a key challenge for market stakeholders.

- •Managing the diverse regulatory requirements and certification processes across multiple Middle Eastern countries complicates product approvals and market entry strategies.

- •High dependency on imports for advanced orthopedic braces and casting materials exposes the market to supply chain disruptions and currency fluctuations.

- •Limited patient education and awareness about the benefits and correct usage of orthopedic support devices reduce treatment adherence and market penetration.

- •Competition from alternative treatment methods, such as pharmaceutical interventions and surgical options, poses challenges for orthopedic brace manufacturers in gaining market share.

Regulatory Framework

- •Between 2019 and 2024, several Middle Eastern countries including Saudi Arabia and UAE updated medical device regulations to align with international standards, focusing on safety, efficacy, and post-market surveillance for orthopedic devices.

- •New compliance mandates require manufacturers to obtain Gulf Cooperation Council (GCC) conformity certificates and register devices with regional health authorities, increasing market entry rigor and transparency.

- •Regulations emphasize traceability and quality management systems for casting materials and braces to ensure patient safety and reduce counterfeit products in the supply chain.

- •Countries like Saudi Arabia have introduced expedited approval pathways for innovative orthopedic technologies, encouraging local adoption of advanced braces and splints.

- •Government policies promoting localization of medical device production aim to reduce dependence on imports and support regional manufacturing capabilities.

Industry Insights

- •In March 2024, DJO Global launched a new line of customizable soft braces designed specifically for the Middle East market, featuring breathable materials suited to the regional climate and enhanced patient comfort. This innovation aims to capture growing demand in sports injury management and rehabilitation sectors.

- •In November 2023, Össur expanded its distribution partnership with a leading GCC medical distributor to improve product accessibility and after-sales support across Saudi Arabia, UAE, and Qatar, reinforcing its market presence amid rising orthopedic care investments.

Mergers & Acquisitions

- •In September 2024, Breg, Inc. completed the acquisition of a regional orthopedic support device manufacturer based in Dubai, enhancing its product portfolio with localized casting and splint solutions tailored for the Middle Eastern market. This strategic move strengthens Breg's supply chain and distribution channels in the GCC region, enabling faster time-to-market and better customer engagement.

- •In February 2023, Medline Industries acquired a medical supplies company operating in Saudi Arabia, expanding its footprint in the Middle East orthopedic support segment. The acquisition facilitates Medline’s access to key hospital networks and orthopedic clinics, facilitating growth through integrated product and service offerings tailored to regional healthcare demands.

Recent Industry News

- •15th January 2025, Sam Medical announced a strategic partnership with a leading UAE healthcare provider to launch a specialized orthopedic brace fitting and rehabilitation program across major hospitals. This initiative aims to enhance patient outcomes through customized support devices and expert clinical guidance, positioning Sam Medical as a key innovator in Middle Eastern orthopedic care. Source: Company Press Release

- •22nd March 2025, DeRoyal Industries opened a new manufacturing facility in Riyadh, Saudi Arabia, dedicated to producing advanced casting materials and splints for the Middle East market. This expansion supports regional supply chain resilience and enables faster delivery of products designed to meet local clinical requirements. Source: Industry Publication

- •10th May 2025, Zimmer Biomet introduced a smart brace embedded with motion sensors that provide real-time feedback to patients and clinicians, tailored for post-surgical rehabilitation in the Middle East. The product launch was supported by clinical trials conducted in Dubai, highlighting its potential to improve recovery rates through digital monitoring. Source: Official Company Announcement

- •5th July 2025, Al Hayat Pharmaceuticals expanded its orthopedic device portfolio by signing a distribution agreement with a global leader in splint manufacturing, aiming to increase availability across Gulf countries. This collaboration is expected to accelerate adoption of innovative splinting solutions in rehabilitation centers and home care. Source: Regional Medical News

Regional Outlook

The Saudi Arabia currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Turkey

- Egypt

- United Arab Emirates

- Saudi Arabia

- Israel

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.85 Billion |

| Forecast Year Market Size | USD 1.92 Billion |

| CAGR | 8.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8% |

| Regions Covered | Turkey, Egypt, United Arab Emirates, Saudi Arabia, Israel, Others |

| Key Companies | Össur (Iceland), Breg, Inc. (United States), DJO Global (United States), Sam Medical (United Kingdom), DeRoyal Industries (United States), Medline Industries (United States), Orthofix International (United States), Allard USA (United States), Zimmer Biomet Holdings, Inc. (United States), Hely & Weber (Germany), BSN Medical (Germany), Porplastic (United Kingdom), Beijing Kangyi Medical (China), Al Hayat Pharmaceuticals (Middle East), Al Zahrawi Medical Supplies (Middle East) |

Middle East Orthopedic Braces & Support Casting & Splint Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.