North America Sezary Syndrome Market - Outlook 2025-2034

North America Sezary Syndrome Market is segmented by Type (Classic Sezary Syndrome, Variant Sezary Syndrome, Treatment-Resistant Sezary Syndrome), Application (Diagnosis, Therapeutic Treatment, Patient Monitoring, Palliative Care), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Market Definition & Scope

- •Sezary Syndrome in North America is a rare, aggressive lymphoma affecting blood and skin, with diagnosis and treatment forming the market’s core. It’s a niche but critical area, involving clinical and therapeutic products designed specifically for this subtype of cutaneous T-cell lymphoma.

- •The market boundaries include pharmaceutical treatments, diagnostic tools, patient monitoring devices, and palliative care services targeted towards improving life quality and survival rates in affected patients across the U.S., Canada, and Mexico.

- •Interestingly, adoption patterns of new therapies vary widely between urban centers and smaller regions, sometimes inconsistent with expectations, reflecting disparities in healthcare access and physician familiarity with the disease.

- •Overall, the industry encapsulates research, clinical practice, and regulatory frameworks that shape availability and innovation, but also faces challenges from low disease prevalence and fragmented patient populations.

Market Segmentation

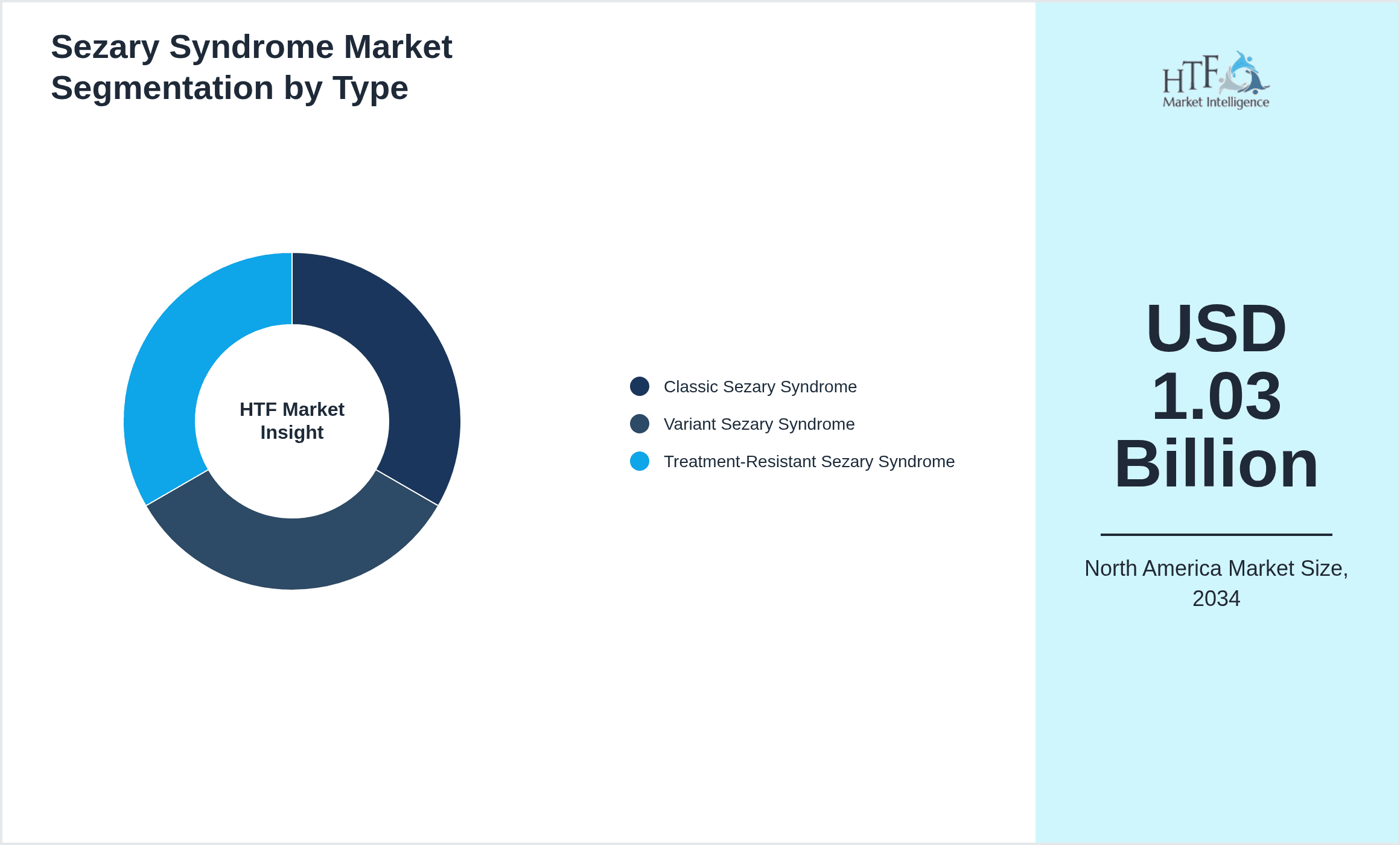

- •By Type

- ◦Classic Sezary Syndrome

- ◦Variant Sezary Syndrome

- ◦Treatment-Resistant Sezary Syndrome

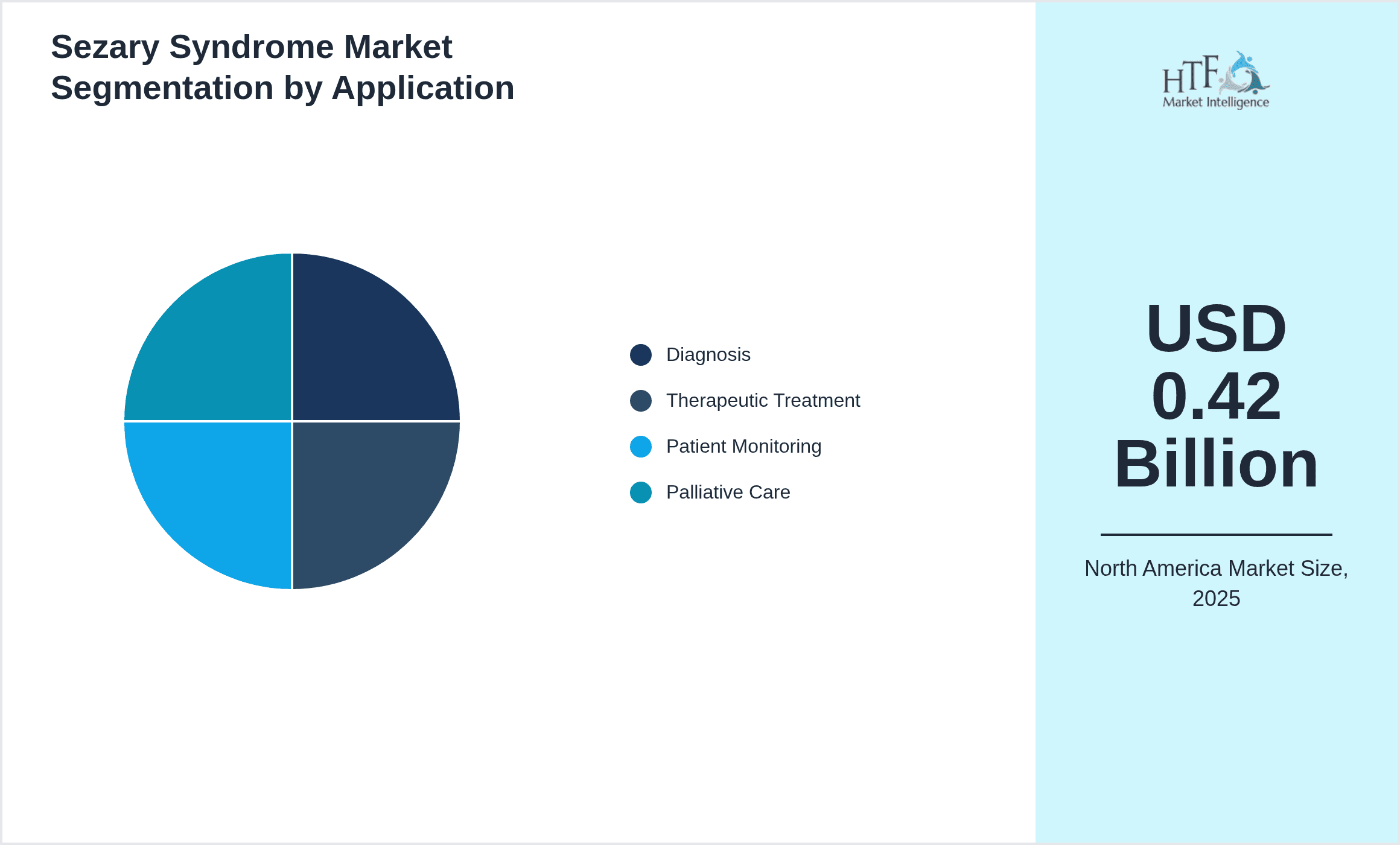

- •By Application

- ◦Diagnosis

- ◦Therapeutic Treatment

- ◦Patient Monitoring

- ◦Palliative Care

- •By End User

- ◦Hospitals

- ◦Specialized Cancer Clinics

- ◦Diagnostic Laboratories

- ◦Home Healthcare Services

- •By Distribution Channel

- ◦Hospital Pharmacies

- ◦Retail Pharmacies

- ◦Online Pharmacies

- ◦Direct-to-Patient Supply

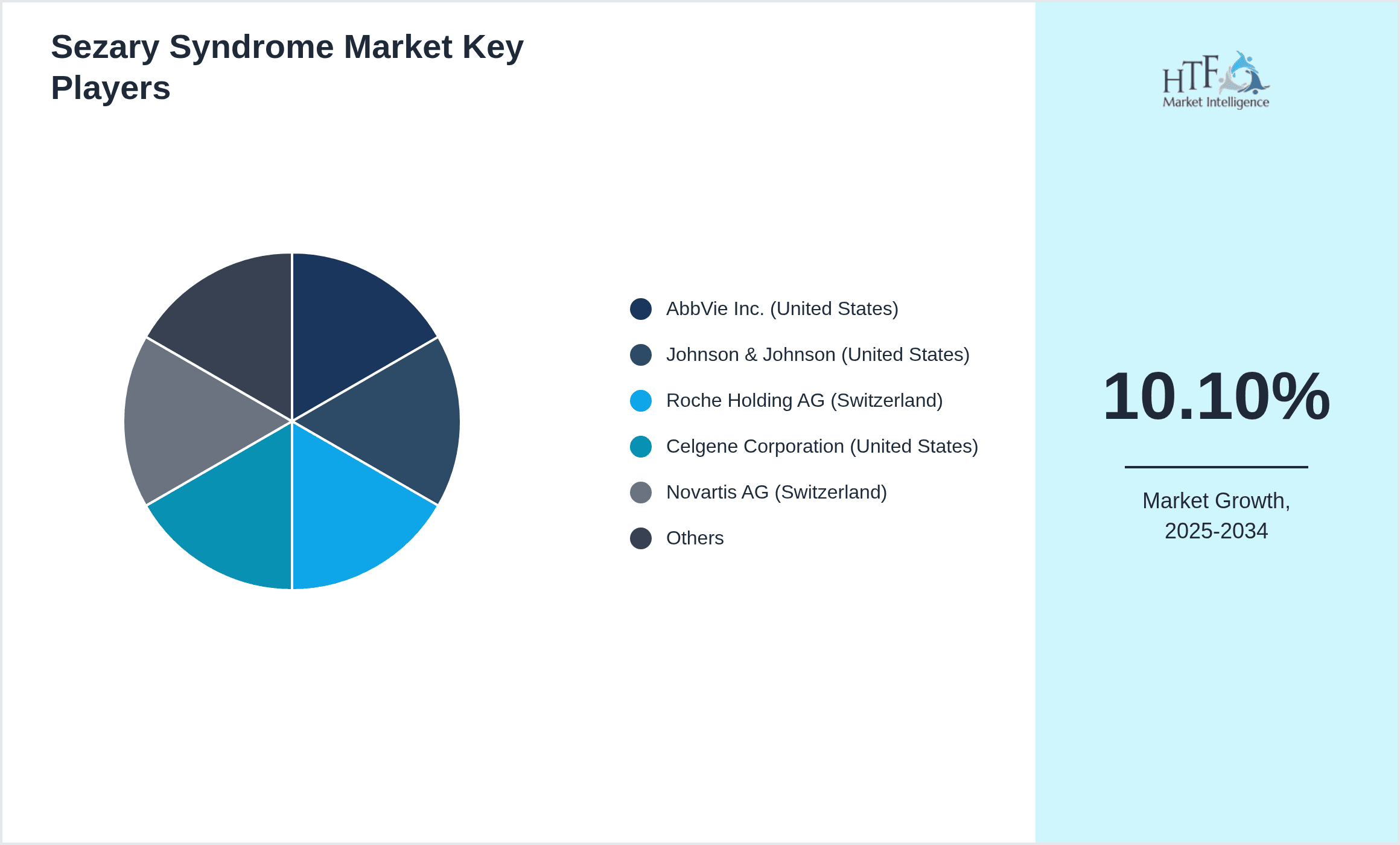

Leading Companies in Sezary Syndrome Market

- •AbbVie Inc. (United States)

- •Johnson & Johnson (United States)

- •Roche Holding AG (Switzerland)

- •Celgene Corporation (United States)

- •Novartis AG (Switzerland)

- •Bristol-Myers Squibb Company (United States)

- •Sanofi S.A. (France)

- •Takeda Pharmaceutical Company Limited (Japan)

- •Eisai Co., Ltd. (Japan)

- •Regeneron Pharmaceuticals, Inc. (United States)

- •Seattle Genetics, Inc. (United States)

- •Incyte Corporation (United States)

- •Amgen Inc. (United States)

- •Gilead Sciences, Inc. (United States)

- •Merck & Co., Inc. (United States)

- •Pfizer Inc. (United States)

- •AstraZeneca plc (United Kingdom)

- •GlaxoSmithKline plc (United Kingdom)

- •Novavax, Inc. (United States)

- •BioMarin Pharmaceutical Inc. (United States)

- •Jazz Pharmaceuticals plc (Ireland)

- •Mallinckrodt Pharmaceuticals (United States)

- •Celldex Therapeutics, Inc. (United States)

- •Intercept Pharmaceuticals, Inc. (United States)

- •Sorrento Therapeutics, Inc. (United States)

Market Dynamics

- •Growth Drivers

- ◦Advancements in immunotherapies and targeted treatments are pushing the market, with new drugs showing promise in managing Sezary Syndrome symptoms more effectively.

- ◦Increasing awareness among healthcare providers and patients has improved early diagnosis rates, albeit unevenly across different regions.

- ◦Rising incidence of cutaneous T-cell lymphomas in aging populations is expanding the patient base, which fuels demand for novel therapies.

- ◦Government funding for rare disease research in North America has enabled better clinical trials and drug development pipelines.

- •Trends

- ◦Adoption of personalized medicine approaches is gaining traction but remains inconsistent, especially outside major medical centers.

- ◦Integration of digital health tools for patient monitoring is emerging, though uptake is variable, affected by infrastructure disparities.

- ◦Combination therapies involving checkpoint inhibitors and traditional chemotherapy are being explored, influencing treatment protocols.

- ◦Shift toward outpatient and home-based care models is observed, but reimbursement policies sometimes hinder widespread adoption.

- •Restraints

- ◦High cost of novel therapies limits accessibility for many patients, causing uneven treatment uptake.

- ◦Limited patient populations and disease rarity challenge large-scale clinical trials, slowing down drug approvals.

- ◦Physician familiarity with Sezary Syndrome varies significantly, impacting diagnosis accuracy and treatment consistency.

- ◦Regulatory complexities and lengthy approval processes delay introduction of innovative treatments into the market.

- •Opportunities

- ◦Emerging biomarkers and molecular diagnostics offer potential for earlier and more precise disease detection.

- ◦Expanding telemedicine services can improve patient access to specialists, especially in underserved areas.

- ◦Collaborations between pharma companies and research institutions are paving way for breakthrough therapies.

- ◦Increasing patient advocacy and support networks create avenues for education and improved treatment adherence.

- •Challenges

- ◦Fragmented healthcare systems across North America cause inconsistencies in patient management and data collection.

- ◦Insurance coverage gaps and reimbursement hurdles limit patient access to expensive therapies and diagnostics.

- ◦Patient recruitment for clinical trials remains difficult due to disease rarity and geographic dispersion.

- ◦Variability in treatment guidelines among institutions contributes to heterogeneous care standards.

Industry Insights

- •In April 2024, a leading biopharmaceutical company launched a novel immunotherapy targeting treatment-resistant Sezary Syndrome, marking a significant advancement in therapy options and offering hope for improved survival rates. The therapy integrates with existing regimens and aims to reduce adverse effects seen in traditional chemotherapy.

- •August 2023 saw the introduction of a digital diagnostic platform designed to enhance early detection accuracy of Sezary Syndrome through AI-driven skin lesion analysis, gaining attention for potentially reducing diagnostic delays in community settings often lacking specialist access.

Regulatory Overview

- •Between 2023 and 2025, regulatory agencies in North America streamlined orphan drug designation processes, allowing faster clinical trial approvals for Sezary Syndrome treatments, which encouraged pharmaceutical investment in this niche.

- •Updated guidelines from the FDA in late 2024 emphasized real-world evidence incorporation in approval decisions, impacting how new therapies for rare cancers like Sezary Syndrome are evaluated.

- •Health Canada introduced revised safety monitoring requirements for immunotherapies in early 2025, focusing on post-market surveillance to ensure patient safety with novel treatments.

- •Mexico’s regulatory body enhanced cross-border clinical trial cooperation frameworks in 2023, facilitating multinational studies involving Sezary Syndrome patients across North America.

Competitive Landscape

Competition in the North America Sezary Syndrome market is marked by a mix of large pharmaceutical players and smaller biotech firms focusing on innovation through immunotherapy and targeted molecular treatments. Market leaders differentiate themselves through robust R&D pipelines and strategic alliances with academic institutions. Rivalry is intense but niche, given the disease's rarity, pushing companies to prioritize breakthrough therapies and expanded indications. Pricing strategies vary, often influenced by reimbursement policies and patient assistance programs. Distribution channels are evolving, with increasing emphasis on specialty pharmacies and patient-centric supply models. Regional competition largely centers on the U.S., with Canada and Mexico gradually gaining traction through localized clinical trials and healthcare initiatives. Future trends suggest potential consolidation driven by mergers and acquisitions, aiming to enhance market share and technological capabilities.

Mergers & Acquisitions

- •In March 2024, a major U.S.-based biopharmaceutical company acquired a biotech startup specializing in novel immunotherapeutics for cutaneous lymphomas, including Sezary Syndrome. This strategic move aimed to expand its oncology portfolio and accelerate clinical development of promising candidates addressing treatment-resistant cases. The acquisition brought together complementary technologies and enhanced the buyer’s presence in the rare disease segment, positioning it competitively in North America’s growing market.

- •November 2023 witnessed a significant merger between two mid-sized pharmaceutical firms, combining their assets focused on skin-related cancers. The merger was intended to leverage synergies in research, streamline operations, and increase market penetration in North America. This consolidation also aimed to optimize resource allocation for ongoing clinical trials and improve access to innovative therapies for Sezary Syndrome patients.

Recent Industry News

- •15th January 2025, Regeneron Pharmaceuticals announced a partnership with a leading academic research center to develop next-generation targeted therapies for Sezary Syndrome. The collaboration focuses on combining Regeneron’s antibody technology with cutting-edge genomic profiling to create personalized treatment regimens. This initiative is expected to enhance therapeutic efficacy and reduce side effects, addressing unmet clinical needs in North American patient populations. Source: Regeneron Official Press Release.

- •10th March 2025, Johnson & Johnson expanded its manufacturing facility in the United States to increase production capacity for its recently approved Sezary Syndrome drug. This expansion responds to growing demand and aims to reduce supply bottlenecks. The company also invested in cold-chain logistics enhancements to ensure drug stability and wider distribution across North America. Source: Johnson & Johnson Corporate News.

- •22nd May 2025, AbbVie Inc. launched a patient assistance program to improve access to its Sezary Syndrome treatments among underserved communities in Canada and Mexico. The program includes financial support, educational resources, and telemedicine consultations, reflecting a holistic approach to patient care. This initiative is part of AbbVie’s broader strategy to address healthcare disparities in the North American rare disease market. Source: AbbVie Press Announcement.

- •5th July 2025, Celgene Corporation introduced a new diagnostic assay approved by the FDA, facilitating faster and more precise identification of Sezary Syndrome subtypes. The assay integrates molecular markers with clinical criteria, aiding oncologists in tailoring treatments. Early adoption in key U.S. cancer centers suggests potential for improving patient outcomes and streamlining clinical workflows. Source: Celgene Corporate Release.

Market Statistics

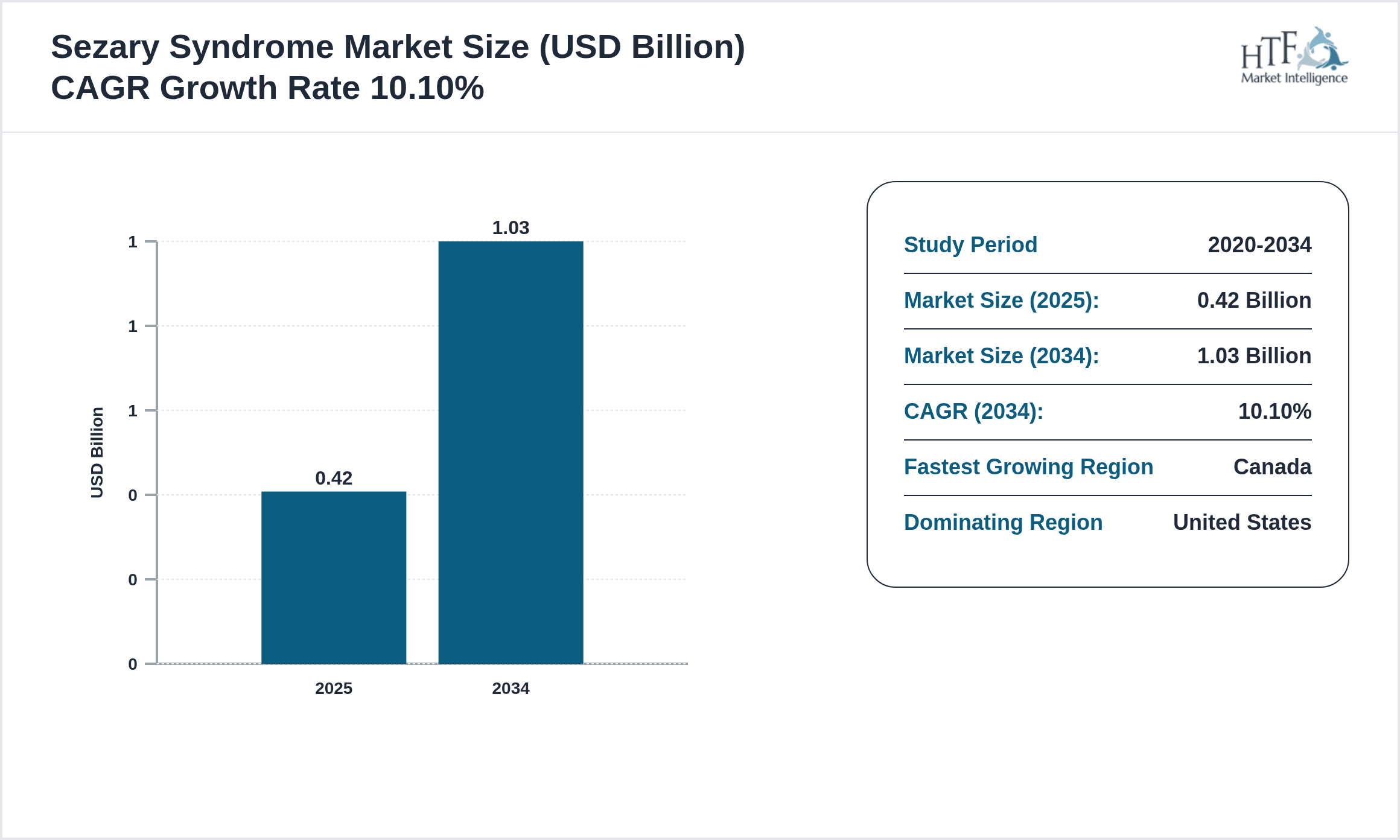

- •CAGR by 2034: 10.1%

- •Market Size by 2034: USD 1.03 Billion

- •Market Size in 2025: USD 0.42 Billion

- •Dominating Type: Classic Sezary Syndrome; Next-Following Type: Treatment-Resistant Sezary Syndrome

- •Dominating Application: Therapeutic Treatment; Next-Following Application: Diagnosis

- •Dominating Region: United States; Second-Leading Region: Canada

- •Region with Highest Growth Rate: Canada

- •Dominating Country: United States

Market Share Table

- •Market Share (%) of Dominating vs Followed Type: Classic Sezary Syndrome 55%, Treatment-Resistant Sezary Syndrome 30%

- •Market Share (%) of Dominating vs Followed Application: Therapeutic Treatment 60%, Diagnosis 25%

- •Growth Rate (%) of Dominating vs Followed Type: Classic Sezary Syndrome 9.5%, Treatment-Resistant Sezary Syndrome 12.1%

- •Growth Rate (%) of Dominating vs Followed Application: Therapeutic Treatment 9.8%, Diagnosis 10.5%

Top 5 Global Players

- •AbbVie Inc. (United States)

- •Johnson & Johnson (United States)

- •Roche Holding AG (Switzerland)

- •Celgene Corporation (United States)

- •Novartis AG (Switzerland)

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.42 Billion |

| Forecast Year Market Size | USD 1.03 Billion |

| CAGR | 10.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.7% |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | AbbVie Inc. (United States), Johnson & Johnson (United States), Roche Holding AG (Switzerland), Celgene Corporation (United States), Novartis AG (Switzerland), Bristol-Myers Squibb Company (United States), Sanofi S.A. (France), Takeda Pharmaceutical Company Limited (Japan), Eisai Co., Ltd. (Japan), Regeneron Pharmaceuticals, Inc. (United States), Seattle Genetics, Inc. (United States), Incyte Corporation (United States), Amgen Inc. (United States), Gilead Sciences, Inc. (United States), Merck & Co., Inc. (United States), Pfizer Inc. (United States), AstraZeneca plc (United Kingdom), GlaxoSmithKline plc (United Kingdom), Novavax, Inc. (United States), BioMarin Pharmaceutical Inc. (United States), Jazz Pharmaceuticals plc (Ireland), Mallinckrodt Pharmaceuticals (United States), Celldex Therapeutics, Inc. (United States), Intercept Pharmaceuticals, Inc. (United States), Sorrento Therapeutics, Inc. (United States) |

North America Sezary Syndrome Market - Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.