Middle East Dysphagia Market - Outlook 2020-2034

Middle East Dysphagia Market is segmented by Product Type (Therapeutic Devices including Neuromuscular Stimulators, Diagnostic Tools such as Videofluoroscopic Equipment, Feeding Tubes (Nasogastric, Gastrostomy), Rehabilitation Software Platforms, Medication for Swallowing Disorders), Application (Hospitals, Rehabilitation Centers, Home Care Settings, Long-term Care Facilities, Diagnostic Clinics), Service Model (Inpatient Care, Outpatient Care, Tele-rehabilitation, Home-based Care), End-User Type (Geriatric Patients, Neurological Disorder Patients, Post-Surgical Patients, Pediatric Patients), and Geography (Turkey, Egypt, United Arab Emirates, Saudi Arabia, Israel, Others)

Pricing

Report Overview

Executive Summary

- •Dysphagia in the Middle East is gaining recognition as a significant healthcare challenge, with rising patient numbers mainly driven by aging populations and increasing neurological disorders. The market spans diagnostic tools, therapeutic devices, feeding aids, and rehabilitation solutions, targeting hospitals, rehab centers, and home care.

- •Market growth is steady but uneven. Some countries adopt advanced rehabilitation software rapidly, while others lag behind due to infrastructure and affordability issues. Therapeutic devices dominate currently, but software solutions show promising fast growth.

- •The value proposition lies in improving patient quality of life and reducing hospitalization duration. However, variations in healthcare policies and reimbursement frameworks across the Middle East affect consistent uptake and service delivery.

Competitive Landscape

The Middle East Dysphagia market features a mix of global medical device leaders and regional players, with competition focusing on product innovation, strategic partnerships, and localized service models. Companies leverage collaborations with healthcare providers to enhance market penetration. Pricing strategies vary widely, reflecting economic diversity. Innovation centers around integrating digital rehabilitation and telehealth services, but adoption depends heavily on local healthcare readiness. Distribution is uneven, with urban centers better served than rural areas. Competitive advantages often arise from customizable solutions and after-sales support, while barriers include regulatory heterogeneity and supply chain complexities. Future trends suggest intensified mergers and partnerships to consolidate market positions and expand service portfolios.

Leading Companies in Dysphagia Market

- •Medtronic (United States)

- •Fresenius Kabi AG (Germany)

- •Abbott Laboratories (United States)

- •Boston Scientific Corporation (United States)

- •Cook Medical (United States)

- •Neurosoft Inc. (United States)

- •Atos Medical AB (Sweden)

- •Natus Medical Incorporated (United States)

- •Smiths Medical (United Kingdom)

- •Neuro Rehab Group (United Kingdom)

- •Halyard Health, Inc. (United States)

- •B. Braun Melsungen AG (Germany)

- •Teleflex Incorporated (United States)

- •CareFusion Corporation (United States)

- •ConvaTec Group PLC (United Kingdom)

- •Advanced Bionics LLC (United States)

- •Otsuka Pharmaceutical Co., Ltd. (Japan)

- •Johnson & Johnson (United States)

- •GE Healthcare (United States)

- •Philips Healthcare (Netherlands)

- •Siemens Healthineers (Germany)

- •ResMed Inc. (United States)

- •Zebra Medical Vision (Israel)

- •Innova Medical Group (United Arab Emirates)

- •Al Hayat Pharmaceuticals (Saudi Arabia)

Market Breakdown

- •By Product Type

- ◦Therapeutic Devices including Neuromuscular Stimulators

- ◦Diagnostic Tools such as Videofluoroscopic Equipment

- ◦Feeding Tubes (Nasogastric, Gastrostomy)

- ◦Rehabilitation Software Platforms

- ◦Medication for Swallowing Disorders

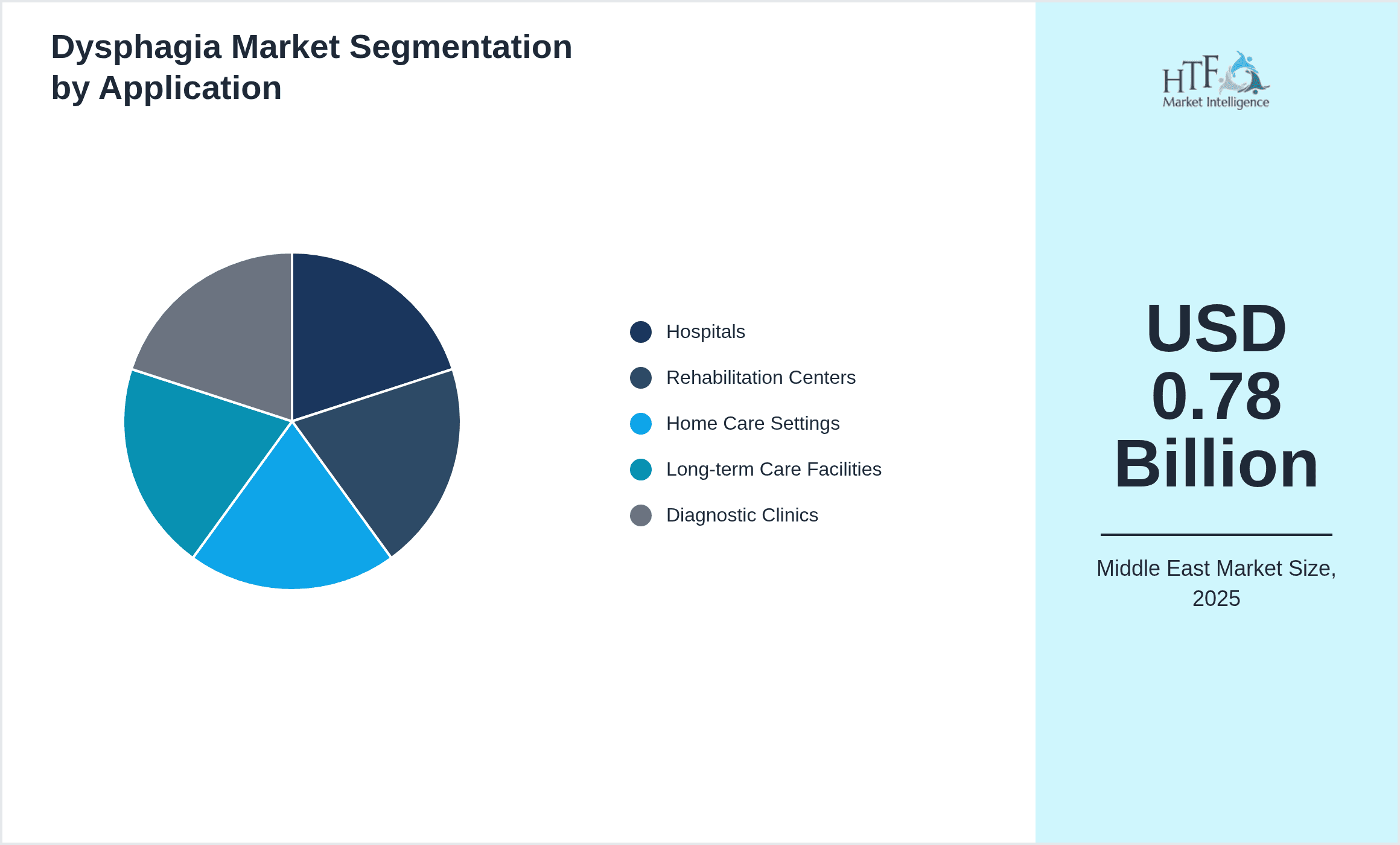

- •By Application

- ◦Hospitals

- ◦Rehabilitation Centers

- ◦Home Care Settings

- ◦Long-term Care Facilities

- ◦Diagnostic Clinics

- •By Service Model

- ◦Inpatient Care

- ◦Outpatient Care

- ◦Tele-rehabilitation

- ◦Home-based Care

- •By End-User Type

- ◦Geriatric Patients

- ◦Neurological Disorder Patients

- ◦Post-Surgical Patients

- ◦Pediatric Patients

Growth Dynamics

- •Increasing prevalence of neurological diseases such as stroke and Parkinson’s in aging Middle Eastern populations is a key growth driver, pushing demand for specialized dysphagia management solutions.

- •Government initiatives to improve healthcare infrastructure in countries like UAE and Saudi Arabia support market expansion, although uneven implementation affects regional uptake.

- •Rising awareness among clinicians and caregivers about the risks of untreated dysphagia is driving adoption of diagnostic and therapeutic products, albeit at inconsistent rates across the region.

- •Technological advancements in non-invasive rehabilitation software and telehealth platforms open new avenues for managing dysphagia remotely, especially in areas with limited specialist access.

- •Economic constraints in lower-income Middle Eastern countries limit access to advanced treatment modalities, impacting uniform market growth across the region.

Market Trends

- •Growing integration of AI-driven diagnostic tools is emerging, yet adoption remains patchy due to varying digital maturity in healthcare facilities across Middle Eastern countries.

- •Shift towards home-based and tele-rehabilitation services for dysphagia management is noticeable, accelerated partly due to the COVID-19 pandemic's impact on healthcare delivery models.

- •Increased collaboration between device manufacturers and software developers is fostering hybrid solutions combining hardware and digital rehabilitation, although market penetration is uneven.

- •Patient-centric care models focusing on quality of life rather than just clinical outcomes are influencing product development and service offerings in the region.

Market Opportunities

- •Expanding geriatric population offers a growing patient base requiring comprehensive dysphagia solutions, presenting opportunities for tailored therapeutic and diagnostic products.

- •Untapped rural and semi-urban markets in Middle East countries represent significant growth potential due to low current penetration of specialized dysphagia care.

- •Rising use of telemedicine and digital health platforms creates openings for innovative remote monitoring and rehabilitation products addressing accessibility challenges.

- •Partnerships between global medical companies and local distributors could accelerate market reach and adaptation to regional needs and preferences.

Market Challenges

- •Fragmented healthcare systems and inconsistent reimbursement policies across Middle Eastern countries hinder uniform adoption and scaling of dysphagia treatment solutions.

- •Limited trained specialists in dysphagia diagnosis and management restrict market expansion, especially in less developed healthcare settings.

- •Cultural factors and patient awareness gaps sometimes delay diagnosis and treatment initiation, impacting overall market demand.

- •High cost of advanced devices and software solutions limits affordability and market penetration among lower-income patient groups.

Market Entropy

The Middle East dysphagia market is a mixed bag of progress and setbacks. While some urban centers like Dubai and Riyadh show robust uptake of cutting-edge diagnostics and tele-rehab platforms, many areas lag behind with patchy adoption. The disparity isn’t just economic; it’s also about awareness, infrastructure, and healthcare culture. Sometimes, even where technology is available, clinical adoption is slow because of lack of trained personnel or ingrained traditional care models. The market feels a bit disjointed — pockets of innovation exist alongside regions struggling with basic dysphagia care access. Regulatory complexity adds to this; rules vary widely between countries, and that confuses manufacturers and providers. So, the market is growing but with a kind of uneven rhythm, not a smooth curve. This inconsistency means stakeholders must navigate a landscape where assumptions about uptake and growth can break down unexpectedly. It’s a reminder that local nuances hugely impact what otherwise looks like a straightforward growth story.

Merger & Acquisition News

Regional Analysis

The Middle East region presents a complex patchwork of healthcare maturity. Saudi Arabia leads by market size, driven by heavy investments in healthcare infrastructure and government support programs. UAE is the fastest growing market, heavily focused on technology adoption and telehealth innovation. Egypt, while large in population, faces challenges with affordability and infrastructure, slowing market growth. Qatar and Kuwait show moderate growth but benefit from concentrated urban healthcare centers. The regional healthcare gap between wealthier Gulf Cooperation Council (GCC) countries and others like Egypt is stark, leading to fragmented market dynamics. Variations in regulatory environments and reimbursement policies further complicate uniform market development, making regional strategies essential for success.

Regulatory Landscape

Regulatory frameworks across the Middle East from 2020 to 2025 have evolved with varying pace. GCC countries like Saudi Arabia and the UAE have implemented updated medical device regulations aligning with international standards, facilitating faster approvals and market entry. However, other countries exhibit slower regulatory progress, often lacking clear guidelines specific to dysphagia devices and related software. Compliance requirements differ, with some markets emphasizing safety and efficacy while others focus on import controls. The lack of harmonized regulations poses challenges for manufacturers seeking regional distribution. Additionally, reimbursement policies remain inconsistent, impacting commercial viability. Efforts toward regional regulatory harmonization are underway but remain in early phases, leaving market participants to navigate a complex patchwork of rules and standards.

Investment and Funding Scenario

Competitive Innovation Radar

Innovation in the Middle East dysphagia market increasingly centers on combining hardware with digital solutions, such as wearable neuromuscular stimulators integrated with smartphone apps for remote monitoring. Companies are exploring AI-powered diagnostics to improve early detection, though these technologies remain largely in pilot phases within the region. Tele-rehabilitation platforms have gained traction, accelerated by pandemic-driven shifts in care delivery. However, the pace of innovation adoption is uneven, with high-tech solutions concentrated in wealthier urban areas. Regional startups and health tech firms are beginning to contribute novel software tools tailored to local languages and cultural contexts, offering promising growth avenues. Overall, innovation is vibrant but fragmented, reflecting the market’s uneven healthcare landscape.

Market Size & Growth Table of Middle East Dysphagia

- •Base Year Market Size: USD 0.78 Billion

- •Historical Year Market Size (2020): USD 0.48 Billion

- •Forecast Year Market Size (2034): USD 1.85 Billion

- •Compound Annual Growth Rate (CAGR): 9.3%

- •Year-on-Year Growth (YoY): 8.9%

Regional Performance Analysis

- •Dominating Region: Saudi Arabia

- •Fastest Growing Region: United Arab Emirates

Regional Outlook

The Saudi Arabia currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Turkey

- Egypt

- United Arab Emirates

- Saudi Arabia

- Israel

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.78 Billion |

| Forecast Year Market Size | USD 1.85 Billion |

| CAGR | 9.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.9% |

| Scope of Report | Market is segmented by Product Type (Therapeutic Devices including Neuromuscular Stimulators, Diagnostic Tools such as Videofluoroscopic Equipment, Feeding Tubes (Nasogastric, Gastrostomy), Rehabilitation Software Platforms, Medication for Swallowing Disorders), Application (Hospitals, Rehabilitation Centers, Home Care Settings, Long-term Care Facilities, Diagnostic Clinics), Service Model (Inpatient Care, Outpatient Care, Tele-rehabilitation, Home-based Care), End-User Type (Geriatric Patients, Neurological Disorder Patients, Post-Surgical Patients, Pediatric Patients) |

| Regions Covered | Turkey, Egypt, United Arab Emirates, Saudi Arabia, Israel, Others |

| Key Companies | Medtronic (United States), Fresenius Kabi AG (Germany), Abbott Laboratories (United States), Boston Scientific Corporation (United States), Cook Medical (United States) |

Middle East Dysphagia Market - Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.