Asia-Pacific Phase Change Heat Storage Material Market - Outlook 2025-2034

Asia-Pacific Phase Change Heat Storage Material Market is segmented by Type (Organic PCM, Inorganic PCM, Eutectic PCM, Bio-based PCM, Composite PCM), Application (Building HVAC, Industrial Waste Heat Recovery, Solar Energy Storage, Cold Chain Logistics, Electronics Cooling), and Geography (Japan, China, Southeast Asia, India, Australia, South Korea, Others)

Pricing

Report Overview

Executive Summary

- •The Asia-Pacific Phase Change Heat Storage Material market covers materials that store and release heat through phase changes, mainly solid-liquid transformations. These materials are integral in thermal management across industries such as HVAC, solar energy, and cold storage, aiming to enhance energy efficiency and reduce costs. The market includes organic, inorganic, eutectic, bio-based, and composite materials, each with unique thermal and chemical characteristics, suited to different temperature ranges and applications. The scope spans from raw material production to integration in end-use systems, reflecting a complex value chain influenced by regional industrial dynamics and energy policies.

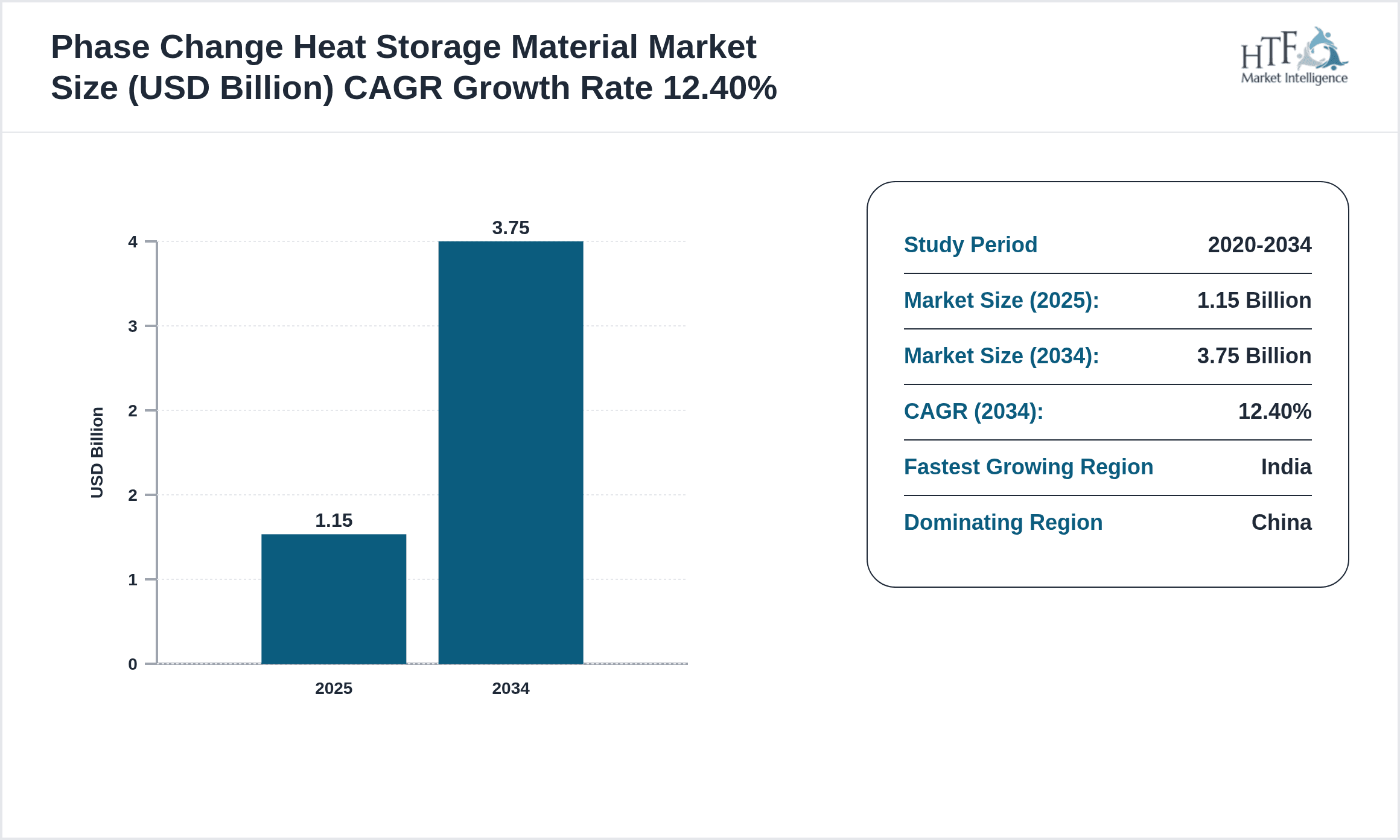

- •Market growth is propelled by increasing demand for energy-efficient solutions in industrial and residential sectors, government incentives promoting renewable energy storage, and rising adoption in emerging economies like India and Southeast Asia. However, uneven adoption rates are observed due to varying infrastructure readiness and cost sensitivity. While China dominates market share, India leads in growth rate, driven by ambitious solar energy projects and waste heat recovery initiatives. The market value is projected to expand from USD 1.15 Billion in 2025 to USD 3.75 Billion by 2034, reflecting a CAGR of 12.4%.

- •Phase change heat storage materials present strategic value in decarbonizing energy systems and enabling grid stability amid renewable energy integration. Stakeholders ranging from material manufacturers to end users in construction, manufacturing, and logistics benefit from reduced energy costs and enhanced operational efficiency. The market landscape is characterized by innovation in bio-based materials and composites, regulatory support particularly in China and India, and growing awareness about sustainable thermal management solutions.

Competitive Landscape

Competition in the Asia-Pacific phase change heat storage material market is fairly intense, with a mix of global conglomerates and regional specialists vying for market share. Innovation focuses strongly on improving thermal conductivity and cycling stability, with companies differentiating through proprietary formulations and composite materials. Strategic partnerships and collaborations are common to accelerate product development and market penetration. Market positioning often hinges on technological leadership, pricing strategies, and localized production capabilities. Rivalry is also shaped by emerging players introducing bio-based materials, challenging traditional inorganic and organic PCMs. Despite the growing market, barriers like high production costs and application-specific customization requirements temper aggressive expansion. Companies increasingly invest in R&D and pilot projects to validate efficacy in diverse Asia-Pacific climates and applications, signaling a dynamic but cautious competitive environment.

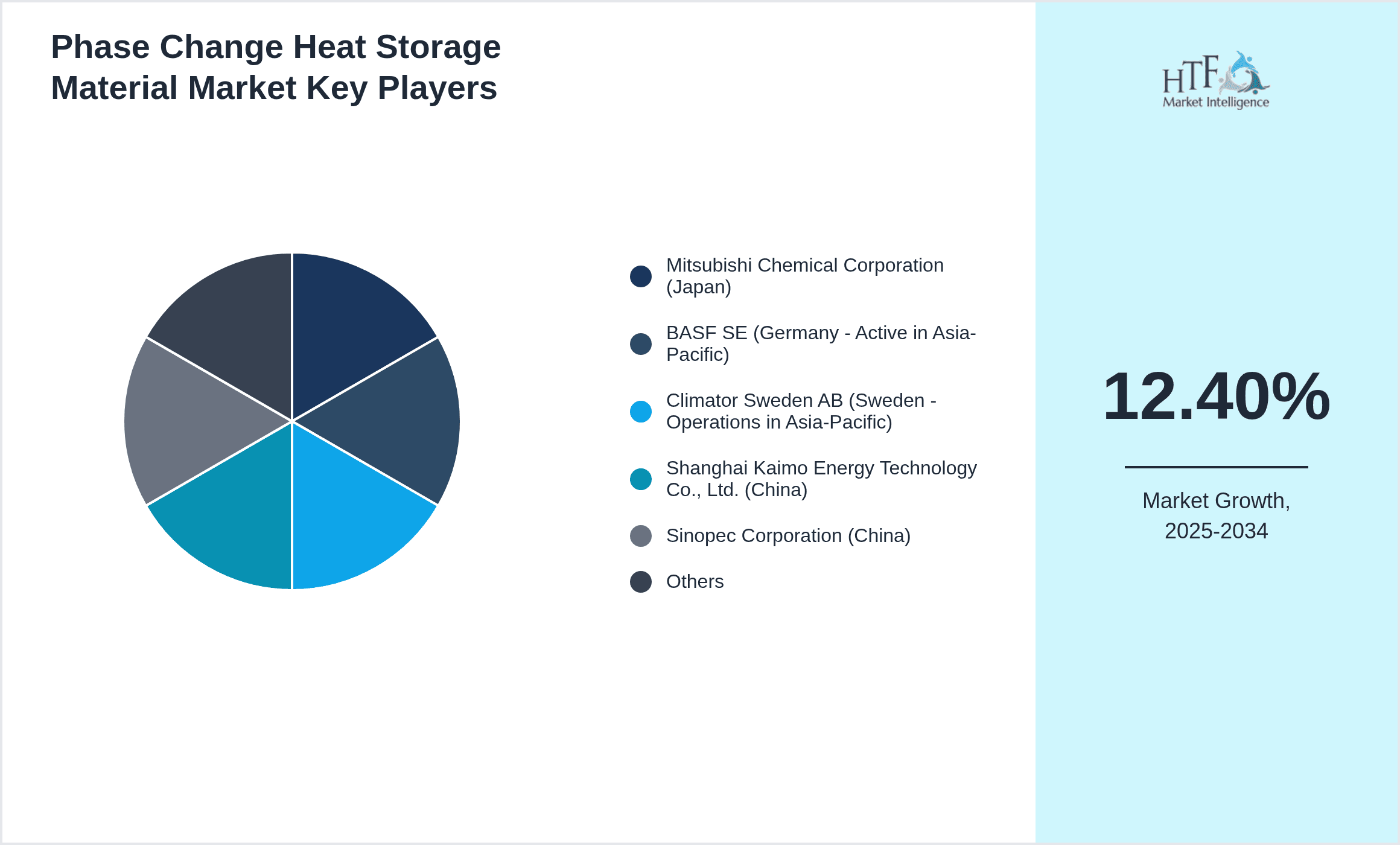

Leading Companies in Asia-Pacific Phase Change Heat Storage Material Market

- •Mitsubishi Chemical Corporation (Japan)

- •BASF SE (Germany - Active in Asia-Pacific)

- •Climator Sweden AB (Sweden - Operations in Asia-Pacific)

- •Shanghai Kaimo Energy Technology Co., Ltd. (China)

- •Sinopec Corporation (China)

- •LG Chem Ltd. (South Korea)

- •Nippon Oil Corporation (Japan)

- •Indmax Limited (India)

- •MGC Pure Chemicals (Japan)

- •Sundrive New Energy Technology Co., Ltd. (China)

- •Sino PCM Energy Technology Co., Ltd. (China)

- •Thermochemie GmbH (Germany - Asia-Pacific presence)

- •Süd-Chemie AG (Germany - Active in Asia-Pacific)

- •Heat Matrix Group (Singapore)

- •Dalian Bosu Energy Technology Co., Ltd. (China)

- •Ceres Power Holdings plc (UK - Operations in Asia-Pacific)

- •Sumitomo Chemical Co., Ltd. (Japan)

- •Changzhou Trunsun Energy Technology Co., Ltd. (China)

- •Mitsui Chemicals, Inc. (Japan)

- •KCC Corporation (South Korea)

- •Shanghai New Material Company Limited (China)

- •Guangzhou Yasheng Thermal Material Co., Ltd. (China)

- •Jiangsu Sofun Thermal Energy Technology Co., Ltd. (China)

- •Thermal Energy Storage Systems Pvt Ltd (India)

- •Ecomate Co., Ltd. (South Korea)

Market Breakdown

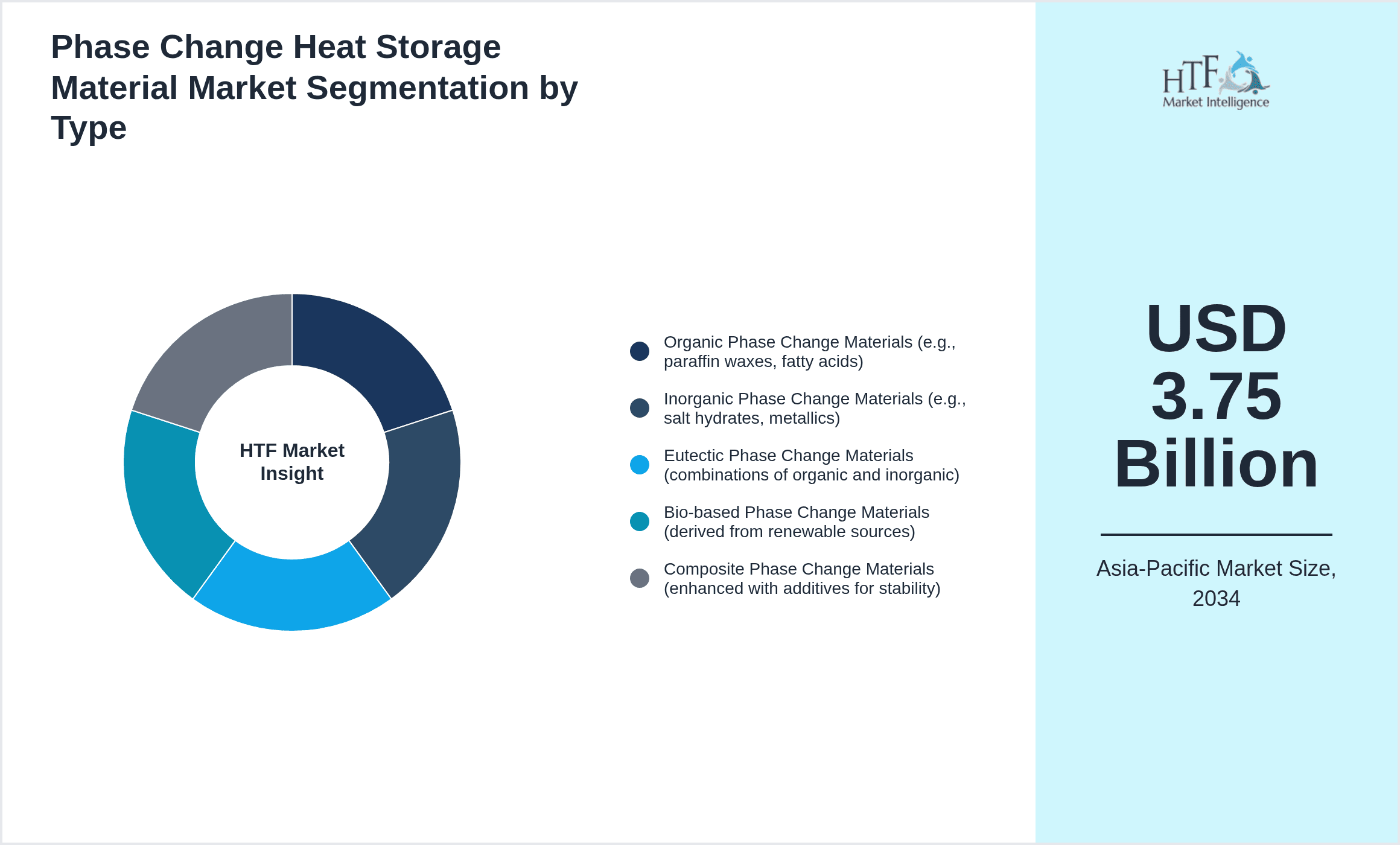

- •By Type

- ◦Organic Phase Change Materials (e.g., paraffin waxes, fatty acids)

- ◦Inorganic Phase Change Materials (e.g., salt hydrates, metallics)

- ◦Eutectic Phase Change Materials (combinations of organic and inorganic)

- ◦Bio-based Phase Change Materials (derived from renewable sources)

- ◦Composite Phase Change Materials (enhanced with additives for stability)

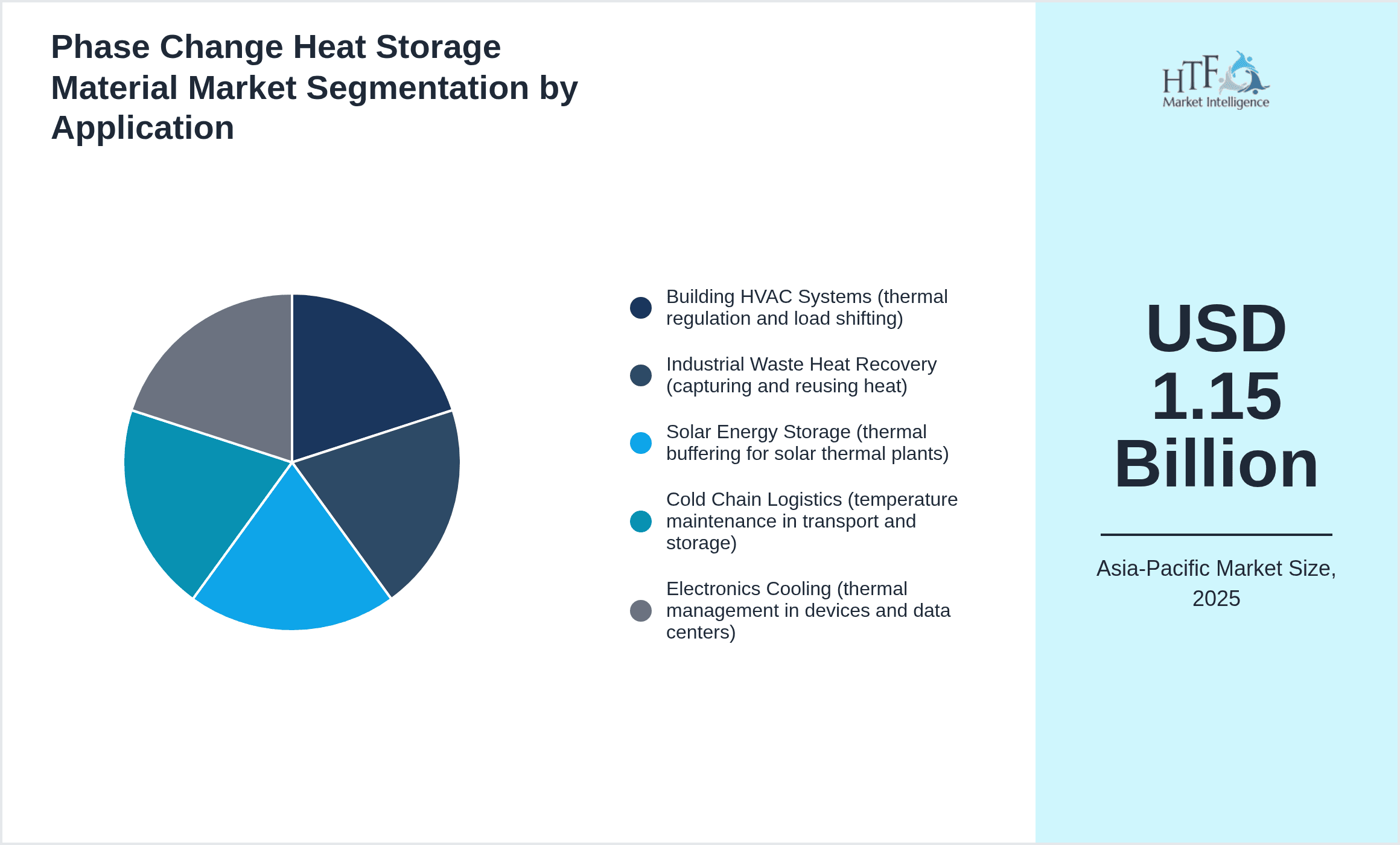

- •By Application

- ◦Building HVAC Systems (thermal regulation and load shifting)

- ◦Industrial Waste Heat Recovery (capturing and reusing heat)

- ◦Solar Energy Storage (thermal buffering for solar thermal plants)

- ◦Cold Chain Logistics (temperature maintenance in transport and storage)

- ◦Electronics Cooling (thermal management in devices and data centers)

- •By End-User Sector

- ◦Residential and Commercial Construction

- ◦Manufacturing and Process Industries

- ◦Renewable Energy Sector

- ◦Transportation and Logistics

- ◦Electronics and Semiconductor Industry

- •By Technology

- ◦Microencapsulation Techniques

- ◦Shape-stabilized PCM Technologies

- ◦Thermally Enhanced Composites

- ◦Nano-enhanced PCM Solutions

Growth Drivers

- •Rising energy costs and stringent government regulations in Asia-Pacific countries like China and India drive adoption of phase change heat storage materials to improve building energy efficiency and reduce carbon footprint.

- •Growing renewable energy installations in the region, especially solar thermal plants, create demand for reliable heat storage solutions to manage intermittent energy supply.

- •Industrial sectors increasingly focus on waste heat recovery to lower operational costs, fueling interest in high-performance PCMs capable of withstanding harsh environments.

- •Advancements in bio-based and composite PCMs attract investments, promising sustainable and cost-effective alternatives to conventional materials.

- •Urbanization and infrastructure development in Southeast Asia and India expand opportunities for thermal energy storage in building HVAC applications.

Market Trends

- •There is a notable shift towards bio-based PCMs reflecting sustainability trends, although their performance consistency under varied climatic conditions is still under evaluation.

- •Integration of nano-materials into PCMs for enhanced thermal conductivity is gaining traction but faces scalability and cost barriers in Asia-Pacific markets.

- •Solar energy storage applications dominate recent deployments, yet cold chain logistics adoption is rising faster than expected, especially in pharmaceutical transport.

- •Regulatory incentives and subsidies in China have created uneven adoption patterns, with some provinces advancing rapidly while others lag due to infrastructure gaps.

- •Collaborations between chemical manufacturers and construction firms are becoming more frequent to tailor PCMs for local building codes and climatic needs.

Market Opportunities

- •Untapped potential exists in emerging Southeast Asian markets where industrialization is accelerating but energy storage solutions remain nascent.

- •Development of low-cost, scalable bio-based PCM products could unlock broad adoption in residential and commercial segments sensitive to upfront costs.

- •Expansion into electronics cooling represents a growing niche, especially with increasing data center deployments across Asia-Pacific requiring efficient thermal management.

- •Strategic partnerships with renewable energy project developers may enhance market penetration, leveraging integrated thermal storage solutions in hybrid energy systems.

- •Government initiatives promoting green building certifications create demand for advanced PCM technologies integrated into building envelopes.

Market Challenges

- •High production and material costs limit widespread PCM adoption, especially in cost-sensitive markets such as India and Southeast Asia where cheaper alternatives prevail.

- •Thermal cycling stability and long-term reliability remain concerns, with some PCMs degrading faster than anticipated in real-world Asian climatic conditions.

- •Lack of standardized testing protocols and certification hinders trust and slows procurement decisions among key end users.

- •Infrastructure limitations and inconsistent power supply in certain Asia-Pacific regions reduce the effectiveness and appeal of PCM-based storage systems.

- •Competition from established thermal energy storage technologies such as molten salts challenges PCM market growth, especially in large-scale industrial applications.

Regulatory Overview

- •Between 2020 and 2025, China implemented updated energy efficiency standards mandating increased use of thermal energy storage materials in new constructions, boosting PCM demand.

- •India's National Solar Mission introduced guidelines promoting thermal storage integration in solar plants, with subsidies available for PCM-based solutions since 2023.

- •Japan revised its Building Energy Efficiency Act in 2024, encouraging adoption of advanced heat storage materials to meet stricter carbon neutrality targets by 2030.

- •South Korea established safety and environmental regulations for PCM manufacturing in 2022, focusing on chemical stability and recyclability of materials.

- •Southeast Asian countries, including Malaysia and Thailand, are developing voluntary green building codes that incentivize PCM integration but lack enforceable mandates as of 2025.

Industry Insights

- •In March 2024, Mitsubishi Chemical Corporation launched a new line of bio-based phase change materials designed for tropical climates, aiming to improve thermal regulation in Southeast Asian buildings. The product features enhanced cycling stability and eco-friendly sourcing, reflecting market demand for sustainable solutions in the region. This launch is expected to accelerate PCM adoption in residential and commercial construction sectors.

- •In November 2023, Shanghai Kaimo Energy Technology announced a strategic partnership with a major Indian solar energy developer to supply eutectic PCMs for large-scale thermal storage projects. This collaboration addresses the growing need for reliable heat storage in India's expanding solar infrastructure and signals increased cross-border industry cooperation within Asia-Pacific.

Mergers & Acquisitions

- •In July 2024, BASF SE acquired a majority stake in Dalian Bosu Energy Technology Co., Ltd., a Chinese PCM manufacturer specializing in inorganic and composite materials. This acquisition aims to strengthen BASF's foothold in Asia-Pacific by expanding its product portfolio and accelerating localized manufacturing capabilities. The move reflects BASF's strategic intent to capitalize on rising demand for thermal energy storage solutions across industrial and construction sectors in the region.

- •In February 2025, LG Chem Ltd. finalized the acquisition of a controlling interest in Indmax Limited, an Indian company focused on bio-based phase change material development. This M&A activity supports LG Chem's diversification into sustainable energy storage materials and leverages Indmax's innovative bio-materials technology to address the growing Asia-Pacific market for eco-friendly PCM solutions.

Recent Industry News

- •15th January 2025, Mitsubishi Chemical Corporation announced the commercial launch of its enhanced composite phase change materials tailored for electronics cooling applications in Asia-Pacific. The products integrate nano-enhanced additives to improve thermal conductivity, targeting the burgeoning semiconductor and data center markets in China and South Korea. This launch aligns with increased demand for efficient thermal management amid rapid digital infrastructure expansion. Source: Mitsubishi Chemical Official Press Release.

- •22nd March 2025, Shanghai Kaimo Energy Technology expanded its manufacturing facility in Shanghai to triple production capacity of eutectic PCMs, aiming to meet rising orders from renewable energy projects across India and Southeast Asia. The facility upgrade includes advanced quality control systems and sustainable manufacturing practices to reduce carbon footprint. This expansion underscores growing confidence in the Asia-Pacific PCM market growth trajectory. Source: Industry Weekly Asia.

- •10th May 2025, BASF SE and a leading Japanese construction firm initiated a joint pilot project deploying organic PCMs in commercial buildings for thermal load shifting. The project focuses on validating energy savings and occupant comfort improvements under diverse climatic conditions. Early results indicate promising performance, potentially setting new regional benchmarks for PCM application in green building projects. Source: BASF Corporate News.

- •5th August 2025, LG Chem Ltd. signed a strategic collaboration agreement with a South Korean data center operator to integrate bio-based phase change materials into cooling systems. The initiative aims to reduce energy consumption and carbon emissions by leveraging PCM's latent heat storage capabilities. This partnership reflects increasing industry interest in sustainable thermal management solutions within Asia-Pacific's fast-growing digital economy. Source: LG Chem Press Release.

Market Statistics

- •CAGR by 2034: 12.4%

- •Market Size by 2034: USD 3.75 Billion

- •Market Size in 2025: USD 1.15 Billion

- •Dominating Type: Organic Phase Change Materials

- •Next-Following Type: Inorganic Phase Change Materials

- •Dominating Application: Building HVAC Systems

- •Next-Following Application: Industrial Waste Heat Recovery

- •Dominating Region: China

- •Second-Leading Region: India

- •Region with Highest Growth Rate: India

- •Dominating Country: China

Market Share Table

- •Market Share (%) - Organic PCM: 45%, Inorganic PCM: 28%

- •Market Share (%) - Building HVAC: 40%, Industrial Waste Heat Recovery: 25%

- •Growth Rate (%) - Organic PCM: 11.5%, Inorganic PCM: 9.8%

- •Growth Rate (%) - Building HVAC: 12.2%, Industrial Waste Heat Recovery: 10.1%

Top 5 Global Players

- •Mitsubishi Chemical Corporation (Japan)

- •BASF SE (Germany - Asia-Pacific operations)

- •LG Chem Ltd. (South Korea)

- •Shanghai Kaimo Energy Technology Co., Ltd. (China)

- •Climator Sweden AB (Sweden - Asia-Pacific presence)

Regional Outlook

The China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, India is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Japan

- China

- Southeast Asia

- India

- Australia

- South Korea

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.15 Billion |

| Forecast Year Market Size | USD 3.75 Billion |

| CAGR | 12.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12% |

| Regions Covered | Japan, China, Southeast Asia, India, Australia, South Korea, Others |

| Key Companies | Mitsubishi Chemical Corporation (Japan), BASF SE (Germany - Active in Asia-Pacific), Climator Sweden AB (Sweden - Operations in Asia-Pacific), Shanghai Kaimo Energy Technology Co., Ltd. (China), Sinopec Corporation (China), LG Chem Ltd. (South Korea), Nippon Oil Corporation (Japan), Indmax Limited (India), MGC Pure Chemicals (Japan), Sundrive New Energy Technology Co., Ltd. (China), Sino PCM Energy Technology Co., Ltd. (China), Thermochemie GmbH (Germany - Asia-Pacific presence), Süd-Chemie AG (Germany - Active in Asia-Pacific), Heat Matrix Group (Singapore), Dalian Bosu Energy Technology Co., Ltd. (China), Ceres Power Holdings plc (UK - Operations in Asia-Pacific), Sumitomo Chemical Co., Ltd. (Japan), Changzhou Trunsun Energy Technology Co., Ltd. (China), Mitsui Chemicals, Inc. (Japan), KCC Corporation (South Korea), Shanghai New Material Company Limited (China), Guangzhou Yasheng Thermal Material Co., Ltd. (China), Jiangsu Sofun Thermal Energy Technology Co., Ltd. (China), Thermal Energy Storage Systems Pvt Ltd (India), Ecomate Co., Ltd. (South Korea) |

Asia-Pacific Phase Change Heat Storage Material Market - Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.