China Automotive Steering Torque Sensors Market Shaping Ahead to Long-Term Value

China Automotive Steering Torque Sensors Market is segmented by Type (Contactless Torque Sensors, Strain Gauge Torque Sensors, Magnetoelastic Torque Sensors, Fiber Optic Torque Sensors, Piezoelectric Torque Sensors), Application (Passenger Vehicles, Commercial Vehicles, Electric Vehicles, Autonomous Vehicles, Aftermarket), Vehicle Type (Light-Duty Vehicles, Heavy-Duty Vehicles, Electric Light Vehicles, Commercial Electric Vehicles), Technology (Analog Torque Sensing, Digital Torque Sensing, Wireless Torque Sensors), and Geography (North China, Northeast China, East China, South Central China, Southwest China, Northwest China)

Pricing

Report Overview

Executive Summary

- •The China Automotive Steering Torque Sensors Market involves devices that measure torque in vehicle steering, integral for safety, control, and ADAS functions. It includes various sensor types like contactless and strain gauge, applied across passenger, commercial, electric, and autonomous vehicles. The market excludes unrelated sensors and purely software-based solutions.

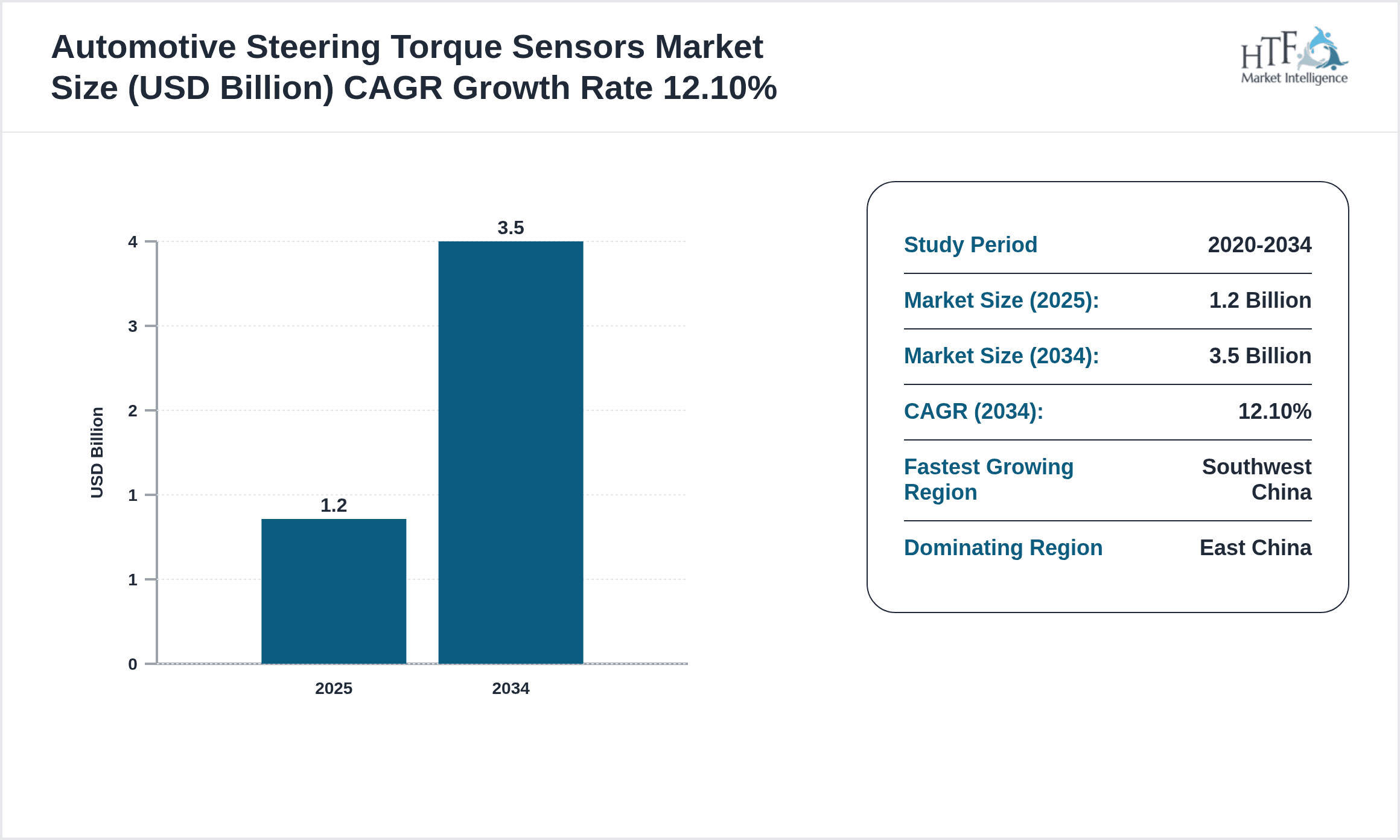

- •Market growth is driven by increasing demand for advanced driver-assistance systems, electric vehicle penetration, and stricter safety regulations in China, with a projected CAGR of 12.1% through 2034 from a base size of USD 1.2 Billion in 2025 to USD 3.5 Billion.

- •This market holds strategic value for automotive manufacturers, sensor suppliers, and technology innovators due to growing vehicle electrification, regional technological adoption disparities, and evolving consumer safety expectations across China’s diverse regions.

Competitive Landscape

Competition in the China Automotive Steering Torque Sensors Market is robust, with a mix of global sensor manufacturers and local Chinese firms jockeying for position. Innovation largely focuses on sensor accuracy, miniaturization, and integration with vehicle electronics. The market sees moderate rivalry; some players leverage strategic partnerships with automakers, while others invest heavily in R&D to differentiate. Pricing pressures exist due to cost-sensitive segments, but premium sensors for electric and autonomous vehicles command higher margins. Regional competition varies, with East China hosting many key manufacturing hubs, whereas emerging regions are attracting new entrants. Overall, companies balance between innovation and cost efficiency to maintain or grow market share amid evolving automotive technologies and government regulations.

Leading Companies in China Automotive Steering Torque Sensors Market

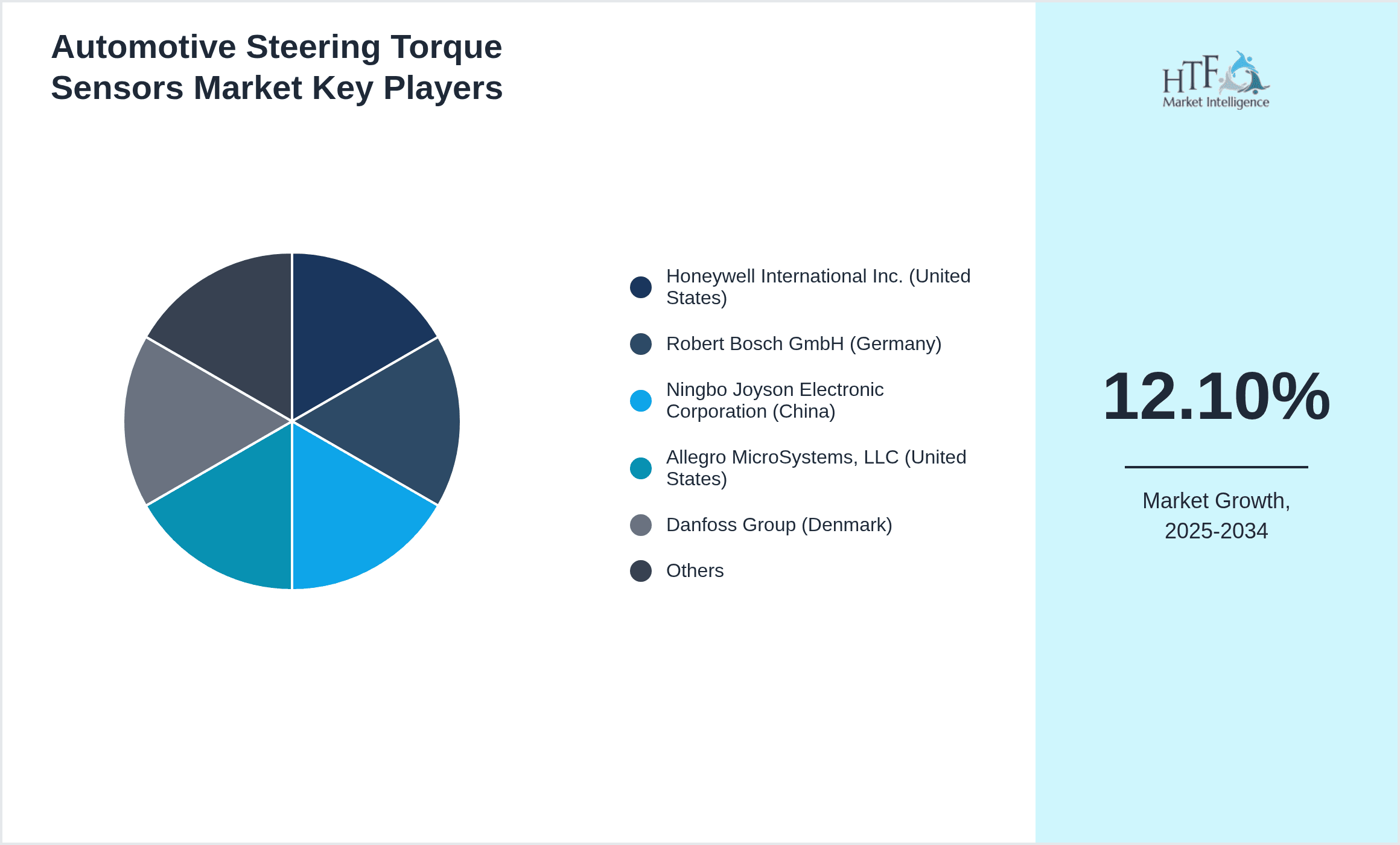

- •Honeywell International Inc. (United States)

- •Robert Bosch GmbH (Germany)

- •Ningbo Joyson Electronic Corporation (China)

- •Allegro MicroSystems, LLC (United States)

- •Danfoss Group (Denmark)

- •ZF Friedrichshafen AG (Germany)

- •NXP Semiconductors N.V. (Netherlands)

- •Alps Alpine Co., Ltd. (Japan)

- •China Automotive Systems, Inc. (China)

- •Sensata Technologies Holding plc (United States)

- •Texas Instruments Incorporated (United States)

- •TE Connectivity Ltd. (Switzerland)

- •Murata Manufacturing Co., Ltd. (Japan)

- •Melexis NV (Belgium)

- •Infineon Technologies AG (Germany)

- •Continental AG (Germany)

- •KYB Corporation (Japan)

- •Valeo SA (France)

- •Autoliv Inc. (Sweden)

- •Shanghai Huayu Automotive Electronics Co., Ltd. (China)

Market Breakdown

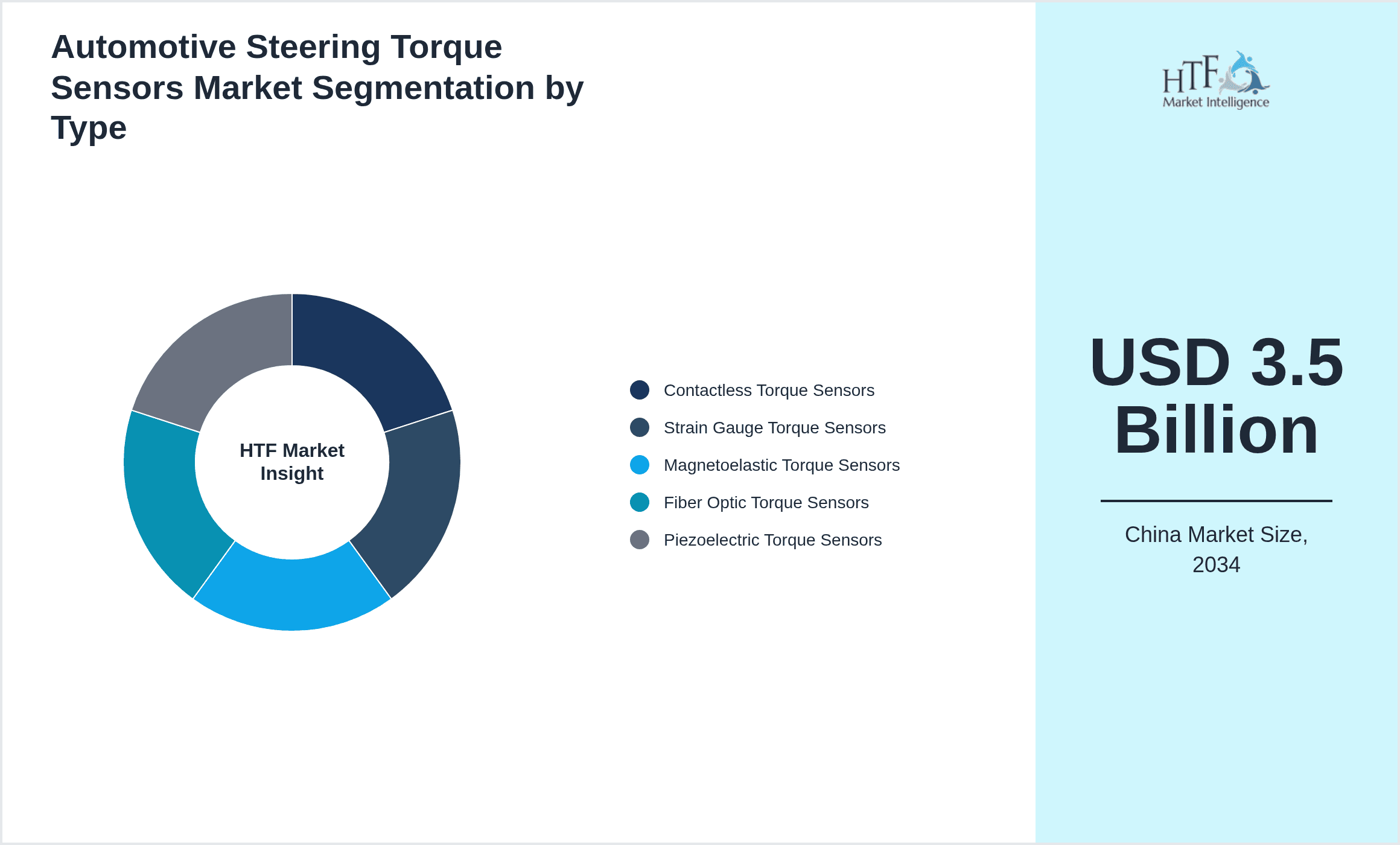

- •By Type

- ◦Contactless Torque Sensors

- ◦Strain Gauge Torque Sensors

- ◦Magnetoelastic Torque Sensors

- ◦Fiber Optic Torque Sensors

- ◦Piezoelectric Torque Sensors

- •By Application

- ◦Passenger Vehicles

- ◦Commercial Vehicles

- ◦Electric Vehicles

- ◦Autonomous Vehicles

- ◦Aftermarket

- •By Vehicle Type

- ◦Light-Duty Vehicles

- ◦Heavy-Duty Vehicles

- ◦Electric Light Vehicles

- ◦Commercial Electric Vehicles

- •By Technology

- ◦Analog Torque Sensing

- ◦Digital Torque Sensing

- ◦Wireless Torque Sensors

Growth Dynamics

- •Growth Drivers: The increasing adoption of electric and autonomous vehicles in China is a major push for steering torque sensor demand. These vehicles need precise steering feedback for safety and control, and torque sensors provide that critical input. Also, government safety regulations mandating advanced driver assistance systems (ADAS) are accelerating sensor integration. Interestingly, despite the push, some lower-end commercial vehicles lag in adoption due to cost concerns, creating uneven market growth. The broad push for vehicle electrification and smart mobility boosts sensor innovation; however, infrastructure and production inconsistencies in certain Chinese regions temper overall growth rates.

- •Trends: There's a clear shift toward contactless torque sensors because of their durability and lower maintenance, which suits electric vehicles well. Fiber optic sensors are emerging as a niche but fast-growing technology due to their immunity to electromagnetic interference, especially in autonomous vehicle applications. However, traditional strain gauge sensors still dominate many segments due to cost-effectiveness. Another trend is the integration of torque sensors with other vehicle control systems, pushing the demand for digital and wireless sensor technologies. Regional preferences vary; for example, East China shows faster digital sensor adoption compared to Northwest China, reflecting industrial maturity differences.

- •Restraints: High sensor costs, especially for advanced types like fiber optic, limit adoption in price-sensitive segments. Manufacturing complexities and the need for precise calibration create barriers for smaller suppliers. Additionally, inconsistent quality standards across Chinese manufacturers cause market fragmentation and slow overall trust in locally made sensors. Regulatory delays in updating safety standards for newer sensor technologies sometimes stall market growth. Also, the aftermarket segment remains underdeveloped, with many vehicles using legacy mechanical systems, limiting sensor penetration beyond new vehicle production.

- •Opportunities: Growing electric vehicle penetration offers a huge opportunity for advanced torque sensors, especially in regions like South China and Southwest China where EV adoption is accelerating. The rising focus on autonomous driving opens demand for sensors with higher precision and integration capabilities. Aftermarket upgrades for steering systems in commercial fleets provide a niche growth area. Technological collaborations between Chinese companies and global sensor manufacturers can spur innovation and cost reduction. Furthermore, digitalization trends in automotive manufacturing present chances to embed torque sensors early in vehicle design cycles, enhancing market reach and product differentiation.

- •Challenges: The uneven industrial development across China’s regions creates adoption inconsistencies, with some zones lagging in sensor integration due to infrastructure or economic factors. Intense price competition pressures margins, especially for local manufacturers. Rapid technology changes require continuous R&D investment, which strains smaller players. Supply chain disruptions, especially for key sensor materials and semiconductors, have occasionally hampered production schedules. Also, navigating the complex regulatory landscape and achieving compliance with evolving safety standards demands significant resources from companies, slowing down product launches and market entry.

Market Trends

- •The market is seeing a gradual but steady shift toward digital and wireless torque sensors, driven by the need for real-time data in connected vehicles. This trend is uneven, with premium vehicle segments adopting faster while budget vehicles stick with analog sensors longer. Manufacturers are increasingly focusing on sensor miniaturization and multi-functionality to reduce vehicle weight and enhance system integration. There's also rising collaboration between sensor makers and automotive OEMs to tailor solutions for electric and autonomous vehicles. Environmental concerns push sensor designs to be more energy-efficient, aligning with China's broader green mobility goals.

- •Another trend is regional variation in sensor technology adoption—East and South China lead in advanced sensor integration due to stronger automotive clusters, while Northwest and Central China rely more on traditional technologies. The aftermarket segment shows slow but emerging interest in sensor upgrades, particularly in commercial vehicles aiming for better fuel efficiency and safety compliance. Additionally, the rise of AI-assisted steering systems is influencing sensor development toward higher accuracy and faster response times.

Market Opportunities

- •The growing electric vehicle market in China offers significant opportunities for torque sensor manufacturers to supply advanced, reliable sensors optimized for EV steering systems. With government incentives supporting EV adoption, manufacturers can capitalize on this expanding segment.

- •Increasing demand for autonomous vehicles presents a chance to develop high-precision, integrated torque sensors that support complex steering control algorithms and safety systems, positioning companies as key enablers of future mobility.

- •Regional expansion into underpenetrated zones like Southwest and Northwest China can unlock new customer bases, especially as infrastructure and vehicle electrification improve in these areas.

- •Aftermarket sensor upgrades for commercial fleets aiming to comply with safety regulations and improve operational efficiency represent a niche but growing market segment.

Market Challenges

- •High production costs for advanced sensor technologies like fiber optic and magnetoelastic sensors limit widespread adoption, especially in cost-sensitive vehicle segments, constraining market growth and vendor profitability.

- •Fragmented quality standards among Chinese manufacturers create trust issues, causing some OEMs to prefer imported sensors despite higher costs, thus challenging local supplier growth.

- •Supply chain vulnerabilities, particularly for semiconductor components and rare materials, have disrupted production timelines, increasing operational risks for sensor manufacturers in China.

- •Regulatory uncertainty and delays in formalizing sensor-related safety standards slow product approvals and market entry, impacting innovation cycles and investment returns.

Regulatory Overview

Between 2020 and 2025, China introduced stricter vehicle safety regulations mandating integration of advanced driver-assistance systems (ADAS), indirectly boosting demand for steering torque sensors. Compliance requirements emphasize sensor accuracy, reliability, and environmental resilience, pushing manufacturers to upgrade designs. Recent updates in 2024 refined testing protocols for sensor calibration and electromagnetic compatibility, aiming to harmonize domestic standards with international norms. These regulatory shifts have increased certification complexity but also enhanced product quality and market confidence. Additionally, government incentives for electric vehicle production include mandates for sensor-equipped steering systems, further driving market growth.

Market Intelligence

- •12th January 2024, Honeywell International Inc. unveiled its latest contactless steering torque sensor designed specifically for electric vehicles with improved precision and lower power consumption. This sensor incorporates advanced digital output capabilities to facilitate integration with ADAS platforms. Targeting the Chinese EV market, Honeywell aims to partner with key OEMs to accelerate adoption. The product promises enhanced durability under China’s varied climate conditions, addressing a common challenge in sensor reliability. Strategic objectives include establishing Honeywell as a leader in China’s rapidly growing torque sensor segment. Source: Honeywell Press Release

- •3rd September 2024, China Automotive Systems, Inc. introduced a new fiber optic torque sensor tailored for autonomous vehicles, featuring immunity to electromagnetic interference and high-speed real-time data transmission. This innovation supports China’s push toward autonomous mobility by enabling safer and more responsive steering control. The company plans collaborations with local autonomous vehicle developers and government-backed pilot programs. The launch reflects broader trends of integrating high-tech sensors into next-gen vehicles while addressing regional technical challenges. Source: Company Website

- •Market Intelligence: Recent developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Mergers & Acquisitions

- •In June 2024, Ningbo Joyson Electronic Corporation acquired a majority stake in a local torque sensor startup specializing in fiber optic technology. This move aims to bolster Joyson’s product portfolio in advanced sensor systems for electric and autonomous vehicles. The acquisition brings complementary R&D capabilities and access to emerging sensor technologies, enhancing competitiveness against global players. The strategic rationale hinges on accelerating innovation cycles and expanding market share within China’s rapidly evolving automotive sector. Post-acquisition, Joyson plans to integrate the startup’s technologies into its mainstream production lines while exploring joint ventures with OEMs. This consolidation reflects a broader trend of domestic companies strengthening their foothold through targeted acquisitions.

- •In November 2023, Robert Bosch GmbH completed the acquisition of a Chinese sensor manufacturer focused on strain gauge torque sensors optimized for commercial vehicles. The deal enhances Bosch’s manufacturing capacity within China and aligns with its strategy to deepen local market penetration. Bosch intends to leverage the acquired company’s client base and regional expertise to accelerate product deployment and customization. The acquisition also facilitates compliance with Chinese localization policies and improves supply chain resilience amid global uncertainties. Bosch’s approach exemplifies how multinational corporations adapt through strategic acquisitions to maintain leadership in competitive automotive components markets.

Recent Industry News

- •15th February 2025, Sensata Technologies Holding plc announced a strategic partnership with Shanghai Huayu Automotive Electronics to co-develop next-generation contactless torque sensors tailored for electric and autonomous vehicles in China. The collaboration focuses on integrating advanced sensor technologies with automotive-grade electronics to meet increasing safety and performance demands. This alliance aims to leverage Sensata’s global expertise and Shanghai Huayu’s local market knowledge to accelerate product launches and expand market reach. Expected outcomes include enhanced sensor reliability and cost optimization, addressing key challenges in China’s automotive sensor landscape. Source: Sensata Press Release

- •28th March 2025, Allegro MicroSystems, LLC expanded its manufacturing footprint in China by inaugurating a new production facility dedicated to steering torque sensors. The investment supports growing demand driven by electric vehicle proliferation and advanced driver-assistance systems adoption. The facility incorporates Industry 4.0 technologies to optimize production efficiency and quality control. Allegro aims to reduce lead times and strengthen supply chain resilience for Chinese OEMs and Tier 1 suppliers. This expansion signals confidence in China’s automotive market growth and reinforces Allegro’s commitment to localizing supply chains. Source: Allegro Corporate Announcement

- •10th May 2025, Infineon Technologies AG launched a digital torque sensor platform designed for integration with smart steering systems in passenger and commercial vehicles. The platform offers enhanced accuracy and noise immunity, supporting China’s push for autonomous driving technologies. Infineon plans to collaborate with local automotive manufacturers to customize sensor solutions addressing regional vehicle requirements. The product launch aligns with increasing government mandates on vehicle safety and emissions reduction, positioning Infineon as a key player in China’s evolving sensor market. Source: Infineon Press Release

- •22nd June 2025, ZF Friedrichshafen AG announced the expansion of its R&D center in Shanghai focusing on innovative steering torque sensor technologies for electric and autonomous vehicles. The center will accelerate development of sensor fusion and AI-enabled steering systems, supporting China’s smart mobility objectives. ZF’s investment reflects growing recognition of China as a strategic market and innovation hub. The initiative aims to shorten product development cycles and enhance collaboration with local OEMs and technology firms. This move underscores the importance of localized innovation in maintaining competitive advantage. Source: ZF Corporate Communication

Market Statistics

- •CAGR by 2034: 12.1%

- •Market Size by 2034: USD 3.5 Billion

- •Market Size in 2025: USD 1.2 Billion

- •Dominating Type: Contactless Torque Sensors

- •Next-Following Type: Strain Gauge Torque Sensors

- •Dominating Application: Passenger Vehicles

- •Next-Following Application: Electric Vehicles

- •Dominating Region: East China

- •Second-Leading Region with Highest Growth Rate: Southwest China

- •Dominating Country: China

Market Share Table

- •Market Share (%) of Dominating vs Followed Type

- ◦Contactless Torque Sensors: 45%

- ◦Strain Gauge Torque Sensors: 30%

- •Market Share (%) of Dominating vs Followed Application

- ◦Passenger Vehicles: 50%

- ◦Electric Vehicles: 28%

- •Growth Rate (%) of Dominating vs Followed Type

- ◦Contactless Torque Sensors: 13.5%

- ◦Strain Gauge Torque Sensors: 10.2%

- •Growth Rate (%) of Dominating vs Followed Application

- ◦Passenger Vehicles: 11.8%

- ◦Electric Vehicles: 14.0%

Top 5 Global Players

- •Honeywell International Inc. (United States)

- •Robert Bosch GmbH (Germany)

- •Ningbo Joyson Electronic Corporation (China)

- •Allegro MicroSystems, LLC (United States)

- •Danfoss Group (Denmark)

Regional Outlook

The East China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southwest China is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North China

- Northeast China

- East China

- South Central China

- Southwest China

- Northwest China

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.2 Billion |

| Forecast Year Market Size | USD 3.5 Billion |

| CAGR | 12.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12% |

| Scope of Report | Market is segmented by Type (Contactless Torque Sensors, Strain Gauge Torque Sensors, Magnetoelastic Torque Sensors, Fiber Optic Torque Sensors, Piezoelectric Torque Sensors), Application (Passenger Vehicles, Commercial Vehicles, Electric Vehicles, Autonomous Vehicles, Aftermarket), Vehicle Type (Light-Duty Vehicles, Heavy-Duty Vehicles, Electric Light Vehicles, Commercial Electric Vehicles), Technology (Analog Torque Sensing, Digital Torque Sensing, Wireless Torque Sensors) |

| Regions Covered | North China, Northeast China, East China, South Central China, Southwest China, Northwest China |

| Key Companies | Honeywell International Inc. (United States), Robert Bosch GmbH (Germany), Ningbo Joyson Electronic Corporation (China), Allegro MicroSystems, LLC (United States), Danfoss Group (Denmark), ZF Friedrichshafen AG (Germany), NXP Semiconductors N.V. (Netherlands), Alps Alpine Co., Ltd. (Japan), China Automotive Systems, Inc. (China), Sensata Technologies Holding plc (United States), Texas Instruments Incorporated (United States), TE Connectivity Ltd. (Switzerland), Murata Manufacturing Co., Ltd. (Japan), Melexis NV (Belgium), Infineon Technologies AG (Germany), Continental AG (Germany), KYB Corporation (Japan), Valeo SA (France), Autoliv Inc. (Sweden), Shanghai Huayu Automotive Electronics Co., Ltd. (China) |

China Automotive Steering Torque Sensors Market Shaping Ahead to Long-Term Value - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.