GCC Medical Refrigerators And Freezers Market - Middle East Size & Outlook 2020-2034

GCC Medical Refrigerators And Freezers Market is segmented by Application (Hospitals, Diagnostic Laboratories, Blood Banks, Pharmaceutical Companies, Research Institutes), Type (Vaccine Refrigerators, Pharmacy Refrigerators, Blood Bank Refrigerators, Laboratory Refrigerators, Ultra-Low Temperature Freezers), and Geography (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates)

Pricing

Report Overview

Market Definition

- •The GCC Medical Refrigerators And Freezers market covers specialized refrigeration units designed specifically for medical and pharmaceutical cold storage needs. These products ensure critical temperature control for vaccines, blood, pharmaceuticals, and biological samples to maintain efficacy and safety.

- •Excluded from this market are general commercial refrigeration appliances, consumer-grade refrigerators, and cold storage solutions not dedicated to medical or pharmaceutical uses.

- •By Type

- ◦Vaccine Refrigerators

- ◦Pharmacy Refrigerators

- ◦Blood Bank Refrigerators

- ◦Laboratory Refrigerators

- ◦Ultra-Low Temperature Freezers

- •By Application

- ◦Hospitals

- ◦Diagnostic Laboratories

- ◦Blood Banks

- ◦Pharmaceutical Companies

- ◦Research Institutes

- •By Service Model

- ◦Sales of New Equipment

- ◦Rental and Leasing Services

- ◦Maintenance and Repair Services

Growth Drivers

Increasing government focus on healthcare infrastructure development across GCC countries is pushing demand for reliable medical refrigeration. Vaccination drives and growing pharmaceutical manufacturing are fueling needs for temperature-controlled storage. Yet adoption patterns vary; some public hospitals lag behind private sector upgrades. The importance of preserving vaccine efficacy especially post-COVID has made vaccine refrigerators a priority, but real-world deployment often faces delays due to budget constraints or supply chain bottlenecks. Blood banks are expanding, but not always with state-of-the-art freezers, reflecting uneven infrastructure investment. Also, rising chronic disease rates lead to higher demand for refrigerated medicines. However, the pace of modernization differs widely between countries like Saudi Arabia and Bahrain. The surge in clinical research activities in the region also contributes to demand, but research institutes sometimes rely on older equipment due to funding cycles. Overall, healthcare modernization policies and heightened awareness about cold chain integrity remain key growth engines despite these inconsistencies.

Market Trends

A notable trend is the gradual shift toward ultra-low temperature freezers supporting mRNA vaccine storage, which is still patchy across GCC. While UAE leads in adoption, other nations show slower uptake. Integration of IoT-enabled monitoring systems for real-time temperature tracking is emerging but uneven. Private sector players adopt these innovations faster than public counterparts, where regulatory approvals and budget cycles can slow things down. Another trend is growing preference for energy-efficient refrigeration solutions amid rising electricity costs, but implementation varies based on local incentives. Moreover, partnerships between medical device suppliers and healthcare providers are increasing to enhance cold chain reliability. Still, in some settings, manual temperature logging remains prevalent. The market also witnesses increased interest in rental and leasing models to reduce upfront costs, though this is not widespread yet.

Market Opportunities

Growing healthcare expenditure in GCC countries creates opportunities for advanced refrigeration technologies tailored to regional needs. Expansion of vaccination programs opens recurring demand for vaccine refrigerators. There is untapped potential in smaller clinics and rural healthcare centers where cold storage remains rudimentary. Demand for ultra-low temperature freezers is expected to grow with increasing biotech research and clinical trials. Also, digitalization of cold chain monitoring can offer new service lines. Opportunities exist for market players to provide integrated solutions combining equipment with maintenance and remote monitoring services. Moreover, GCC governments’ push for localization of manufacturing offers chances for regional production partnerships. Yet market players must navigate inconsistent adoption rates and varying regulatory requirements across countries.

Market Challenges

Fragmented healthcare infrastructure across GCC poses a challenge for uniform adoption of advanced refrigeration equipment. Budgetary constraints in some public health sectors delay upgrades. Supply chain disruptions and import dependencies sometimes cause delays and increase costs. Moreover, lack of trained personnel for maintenance and monitoring impacts equipment reliability. Regulatory variations and certification complexities across GCC countries add to compliance burdens. Energy consumption concerns are rising, but transitioning to energy-efficient models requires upfront investments that are not always feasible. Additionally, fluctuating demand due to seasonal vaccination cycles complicates inventory management. These challenges combine to slow down expected market penetration rates despite evident needs.

Market Entropy

The GCC medical refrigeration market shows a certain degree of unpredictability stemming from inconsistent healthcare investment patterns and shifting policy priorities. While Saudi Arabia pushes large-scale infrastructure projects, smaller GCC countries sometimes lack continuous funding, causing uneven equipment upgrades. Demand for ultra-low temperature freezers spikes with new vaccine introductions but then plateaus. Adoption of IoT and digital solutions is enthusiastic in some urban centers but minimal elsewhere. Supply chains remain vulnerable to geopolitical tensions and global logistics challenges, impacting product availability and pricing. Moreover, the coexistence of modern and outdated refrigeration equipment within the same facilities leads to operational inefficiencies and maintenance complexities. This churn makes forecasting volatile and complicates long-term planning for suppliers and buyers alike.

Merger & Acquisition News

Regional Analysis

Saudi Arabia dominates the GCC medical refrigerators and freezers market driven by its large healthcare infrastructure and government spending. The kingdom’s Vision 2030 initiative has accelerated modernization, boosting demand for advanced refrigeration units. UAE follows closely with rapid adoption of innovative cold storage technologies and strong private healthcare sector investments. Kuwait and Qatar show steady growth but with slower technology turnover. Bahrain and Oman represent smaller but growing markets focusing on upgrading public health cold chain capabilities. Differences in regulatory frameworks, healthcare policies, and funding cycles across these countries lead to uneven adoption rates. Urban centers exhibit higher penetration of smart, energy-efficient models compared to peripheral areas. Regional collaborations and cross-border healthcare initiatives offer potential to harmonize standards and facilitate market growth.

Regulatory Landscape

The GCC medical refrigeration market operates under a complex regulatory environment with each member country enforcing its own standards and certification procedures. Saudi Food and Drug Authority (SFDA) mandates strict compliance for medical cold storage equipment, emphasizing performance and safety. UAE’s Ministry of Health and Prevention requires registration and adherence to Gulf Cooperation Council Standardization Organization (GSO) guidelines. Kuwait and Qatar have evolving regulations focusing on quality assurance and energy efficiency. Import regulations and customs procedures also vary, impacting lead times. Compliance with international standards such as ISO 13485 and WHO PQS (Performance, Quality and Safety) is increasingly expected, especially for vaccine refrigerators. However, regulatory fragmentation creates hurdles for manufacturers and suppliers trying to standardize products across the region. Ongoing efforts to harmonize GSO regulations may reduce barriers in future but are yet to be fully realized.

Investment and Funding Scenario

Investment in the GCC medical refrigeration sector is growing, primarily driven by government initiatives and increased healthcare budgets. Saudi Arabia leads with significant allocations under Vision 2030 for healthcare infrastructure including cold chain enhancements. The UAE is attracting private investments and international partnerships focusing on innovation and sustainability in medical refrigeration. However, funding availability for smaller GCC markets like Bahrain and Oman is more constrained, leading to reliance on external suppliers and leasing models. Venture capital interest in IoT-enabled monitoring solutions and energy-efficient refrigeration technologies is emerging but still in early stages. Public-private partnerships are considered crucial to bridge financing gaps. Overall, while capital inflow is strengthening, access disparities remain across the GCC affecting uniform market development.

Competitive Innovation Radar

Competition in the GCC medical refrigerators and freezers market is intensifying with players focusing on innovation to differentiate. Major manufacturers are integrating IoT sensors for continuous temperature monitoring and remote diagnostics, which appeal to large hospital networks. Energy efficiency improvements are a priority given rising operational costs; some companies offer solar-powered or hybrid refrigeration units to cater to off-grid locations. Modular and customizable designs enabling flexibility for diverse healthcare settings are gaining traction. Local distributors and service providers compete on maintenance quality and after-sales support, critical for high uptime. However, innovation adoption is uneven, with private sector clients often ahead of public institutions. Strategic collaborations between global manufacturers and regional partners aim to localize production and tailor products to GCC climates and regulatory requirements.

Market Size & Growth Table for GCC Medical Refrigerators And Freezers

- •Year, Market Size (USD Billion)

- •2020, 0.34

- •2025, 0.48

- •2034, 1.05

- •CAGR (2025-2034), 8.9%

- •Year-on-Year Growth, 8.6%

Regional Performance Analysis

- •Dominating Country: Saudi Arabia

- •Fastest Growing Country: United Arab Emirates

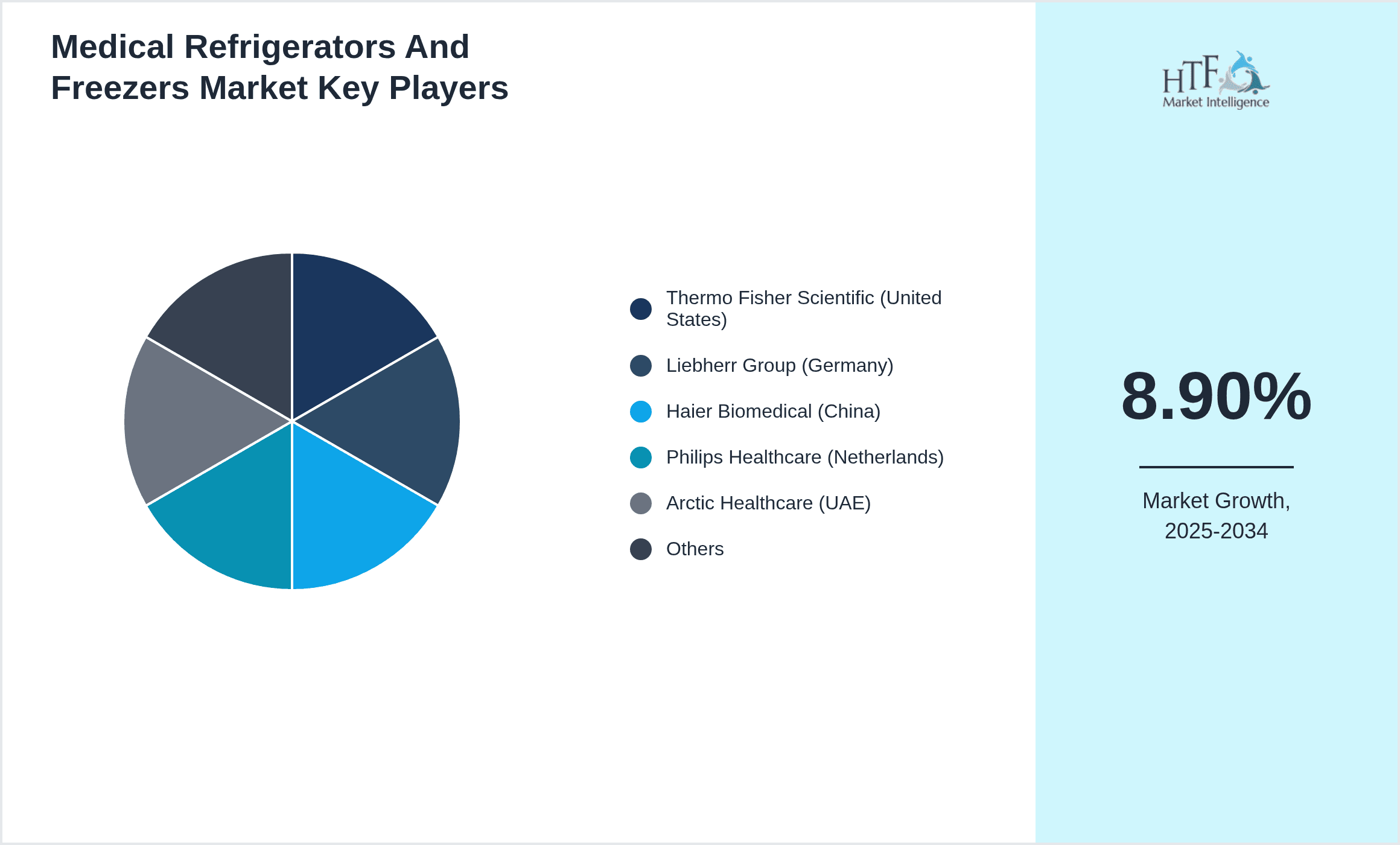

Players List of GCC Medical Refrigerators And Freezers with Head Quarter operating in GCC market

- •Thermo Fisher Scientific (United States)

- •Liebherr Group (Germany)

- •Haier Biomedical (China)

- •Philips Healthcare (Netherlands)

- •Arctic Healthcare (UAE)

- •Vestfrost Solutions (Denmark)

- •Panasonic Healthcare (Japan)

- •Dometic Group (Sweden)

- •B Medical Systems (Luxembourg)

- •Mettler-Toledo International (Switzerland)

- •Fisher & Paykel Healthcare (New Zealand)

- •Haier Middle East (UAE)

- •Al Safa Medical Equipment (KSA)

- •Gulf Medical Refrigeration (Kuwait)

- •Qatar Medical Refrigeration Co. (Qatar)

- •Oman Medical Supplies (Oman)

- •Bahrain Medical Refrigeration Services (Bahrain)

- •Al Jazeera Medical Equipment (UAE)

- •Medisafe Group (Saudi Arabia)

- •Al Mulla Medical Systems (Kuwait)

- •Emirates Medical Solutions (UAE)

- •Al Nahda Medical Supplies (Saudi Arabia)

- •HealthTech Solutions (Dubai, UAE)

- •Kuwait Medical Devices Co.

- •Desert Chill Medical Refrigeration (Oman)

Competitive Analysis

The GCC medical refrigeration market reflects a competitive environment where global multinational firms dominate due to their advanced technology and extensive service networks. However, regional players and distributors are carving niches by offering localized support and competitive pricing. Innovation tends to focus on integrating IoT and energy efficiency, but uptake varies widely across client segments. While large hospitals prefer premium, feature-rich units, smaller facilities often opt for cost-effective basic models. Competitors also differentiate through maintenance contracts and rapid service response, which is crucial given the sensitivity of medical products. Barriers to entry are moderate due to regulatory complexities and the need for specialized product certification. Partnerships and alliances between international manufacturers and GCC-based firms are common to improve market access and comply with local standards. Pricing remains competitive but constrained by buyers’ budget limitations, especially in public healthcare.

Regional Outlook

The Saudi Arabia currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Bahrain

- Kuwait

- Oman

- Qatar

- Saudi Arabia

- United Arab Emirates

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.48 Billion |

| Forecast Year Market Size | USD 1.05 Billion |

| CAGR | 8.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.6% |

| Regions Covered | Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates |

| Key Companies | Growing healthcare expenditure in GCC countries creates opportunities for advanced refrigeration technologies tailored to regional needs. Expansion of vaccination programs opens recurring demand for vaccine refrigerators. There is untapped potential in smaller clinics and rural healthcare centers where cold storage remains rudimentary. Demand for ultra-low temperature freezers is expected to grow with increasing biotech research and clinical trials. Also, digitalization of cold chain monitoring can offer new service lines. Opportunities exist for market players to provide integrated solutions combining equipment with maintenance and remote monitoring services. Moreover, GCC governments’ push for localization of manufacturing offers chances for regional production partnerships. Yet market players must navigate inconsistent adoption rates and varying regulatory requirements across countries. |

GCC Medical Refrigerators And Freezers Market - Middle East Size & Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.