EMEA Electronic Grade Isopropyl Alcohol Market - Outlook 2020-2034

EMEA Electronic Grade Isopropyl Alcohol Market is segmented by Application (Semiconductor Manufacturing, Electronics Cleaning, Pharmaceuticals, Personal Care, Chemical Intermediates), Type (High Purity IPA, Standard Purity IPA, Denatured IPA), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Market Definition

- •Electronic Grade Isopropyl Alcohol is a high-purity solvent tailored specifically for electronic and semiconductor industry applications, with very strict impurity limits and moisture content control.

- •It excludes technical grade or industrial grade IPA used in broader chemical or household cleaning industries to focus on high-specification applications.

- •By Type

- ◦High Purity IPA

- ◦Standard Purity IPA

- ◦Denatured IPA

- •By Application

- ◦Semiconductor Manufacturing

- ◦Electronics Cleaning

- ◦Pharmaceuticals

- ◦Personal Care

- ◦Chemical Intermediates

- •By Packaging and Distribution

- ◦Bulk Supply

- ◦Packaged Containers

- ◦Custom Blends

Drivers

The surge in semiconductor manufacturing across EMEA is a clear driver for electronic grade IPA. As chip fabrication plants expand or modernize, demand for ultra-pure solvents rises to meet contamination control standards. But adoption rates vary; some smaller fabs still use less pure alternatives, slowing uniform market growth. Also, pharmaceutical production growth in the region contributes, with IPA serving as a cleaning and solvent agent in drug manufacturing. Regulatory pressure to reduce volatile organic compounds pushes producers toward higher quality IPA grades, though enforcement and compliance can differ between countries, creating uneven market impacts. Overall, rising electronics and pharma sectors pull IPA consumption upward, but market maturity levels fluctuate across EMEA, leading to patchy demand patterns.

Trends

A notable trend is the shift toward more sustainable and environmentally friendly IPA production processes, driven by European regulations and customer demand. Some manufacturers have started using bio-based feedstocks or recycling solvent streams, but scale remains limited. Another trend is the increasing preference for denatured IPA in certain non-critical electronic cleaning applications, offering cost advantages despite slightly lower purity. There’s also an emerging pattern of supply chain diversification post-pandemic, with buyers seeking multiple sources to avoid disruptions, though this raises challenges around consistent quality. While innovations in packaging for safer handling and reduced contamination risks gain attention, uptake is uneven across the market.

Opportunities

Growth in emerging EMEA markets such as Eastern Europe and the Middle East presents clear opportunities, where semiconductor and pharmaceutical industries are still developing and require better quality solvents. Expanding low-cost local production facilities could capture these untapped segments. Additionally, rising demand for personal care products that use electronic grade IPA as a solvent opens another avenue, particularly in Western Europe’s mature markets. There’s also scope in customized blends tailored for niche applications, offering differentiation. However, realizing these opportunities depends heavily on navigating varying regulatory environments and establishing reliable distribution networks across diverse EMEA countries.

Challenges

One ongoing challenge is the inconsistent regulatory framework across EMEA nations, which complicates compliance and slows market standardization. For example, purity requirements and environmental regulations differ between EU countries and non-EU markets, creating complexity for producers and buyers alike. Supply chain disruptions, including raw material shortages or transportation delays, have periodically affected market availability, especially post-pandemic, and these issues persist intermittently. The price volatility of raw materials also affects profitability, making long-term planning difficult. Moreover, some end users remain reluctant to switch to higher purity grades due to cost concerns, limiting growth in certain segments.

Market Entropy

The EMEA electronic grade IPA market exhibits a fair amount of fluctuation and unpredictability. While demand generally rises with semiconductor and pharmaceutical sectors, actual uptake is uneven. Some regions advance rapidly with new fabs and stricter quality standards, while others lag behind, sticking to older solvent grades for cost reasons. Supply chains are fragmented, with producers scattered across Western Europe, the Middle East, and newer Eastern European players, leading to variations in pricing and quality assurance. Market entry barriers can be high due to certification demands and capital costs, yet smaller local producers sometimes fill gaps, increasing competitive noise. Furthermore, geopolitical tensions and trade policies occasionally disrupt supply flows, adding to the market’s unstable patterns. It’s not a straightforward, linear progression; rather, a patchwork of growth pockets and occasional setbacks.

Merger & Acquisition News

Regional Analysis

Within EMEA, Germany holds a lead thanks to its strong chemical manufacturing base and concentration of semiconductor firms demanding high purity IPA. The UK is catching up quickly, fueled by investments in chip fabrication and pharmaceutical hubs, showing the fastest growth rate in recent years. France, Italy, and Spain follow with mixed adoption levels—France has advanced pharma sectors, while Italy and Spain show slower uptake in electronics cleaning. Eastern Europe and the Middle East remain smaller markets but are gaining interest from suppliers due to emerging industries and infrastructure projects. Supply chain logistics fluctuate widely across these regions, with Western Europe benefiting from established transport and regulatory frameworks, whereas other areas face higher operational challenges. Overall, the regional picture is fragmented, with pockets of rapid advancement amidst slower zones.

Regulatory Landscape

The regulatory environment across EMEA governing electronic grade IPA is somewhat patchy. The EU sets stringent directives on chemical purity, VOC emissions, and worker safety, which many member states enforce rigorously. This pushes manufacturers to maintain high-quality standards and invest in cleaner production methods. However, countries outside the EU, such as those in the Middle East or Eastern Europe, may have less stringent or uneven enforcement, leading to market inconsistencies. REACH regulations impact raw material sourcing and chemical registrations, adding compliance layers for producers. Environmental policies targeting solvent emissions and waste disposal also shape production techniques. On the flip side, the multiplicity of national regulations complicates cross-border trade and raises costs. Some producers struggle with certification delays or divergent testing protocols, which restrains market fluidity. Overall, the regulatory patchwork creates both compliance challenges and incentives to improve product quality.

Investment and Funding Scenario

Recent years have seen modest but targeted investments in IPA production capacity upgrades within EMEA, mainly in Western Europe, where manufacturers focus on cleaner, more efficient processes. Venture capital interest is limited but growing in startups exploring bio-based IPA alternatives, aligning with sustainability trends. Public funding supports some chemical innovation projects under EU green initiatives, though direct funding for IPA-specific ventures is sparse. Overall, the funding landscape is cautious; investors weigh regulatory risks and market fragmentation against steady demand growth. Expansion plans often hinge on securing long-term supply contracts with semiconductor or pharmaceutical clients. While no major new greenfield IPA plants have been announced post-2025, incremental capacity improvements and technology upgrades remain ongoing.

Competitive Innovation Radar

Competition in the EMEA electronic grade IPA market is marked by a mix of established chemical giants and regional specialists. Innovation focuses on improving purity levels, reducing environmental impact, and enhancing supply reliability. Some players experiment with bio-based feedstocks to differentiate their offerings, though these are early-stage and not yet mainstream. Packaging innovations aimed at contamination prevention and safer handling are gaining traction, especially among semiconductor customers. Digital tools to track quality and batch consistency are also being introduced. However, pricing pressures remain intense, limiting the scope for some advanced technologies. The competitive landscape is fragmented, with no single dominant player, and companies often compete on the basis of service quality and supply chain flexibility as much as product specs. Collaboration with end-users to tailor IPA grades is an emerging approach to build loyalty.

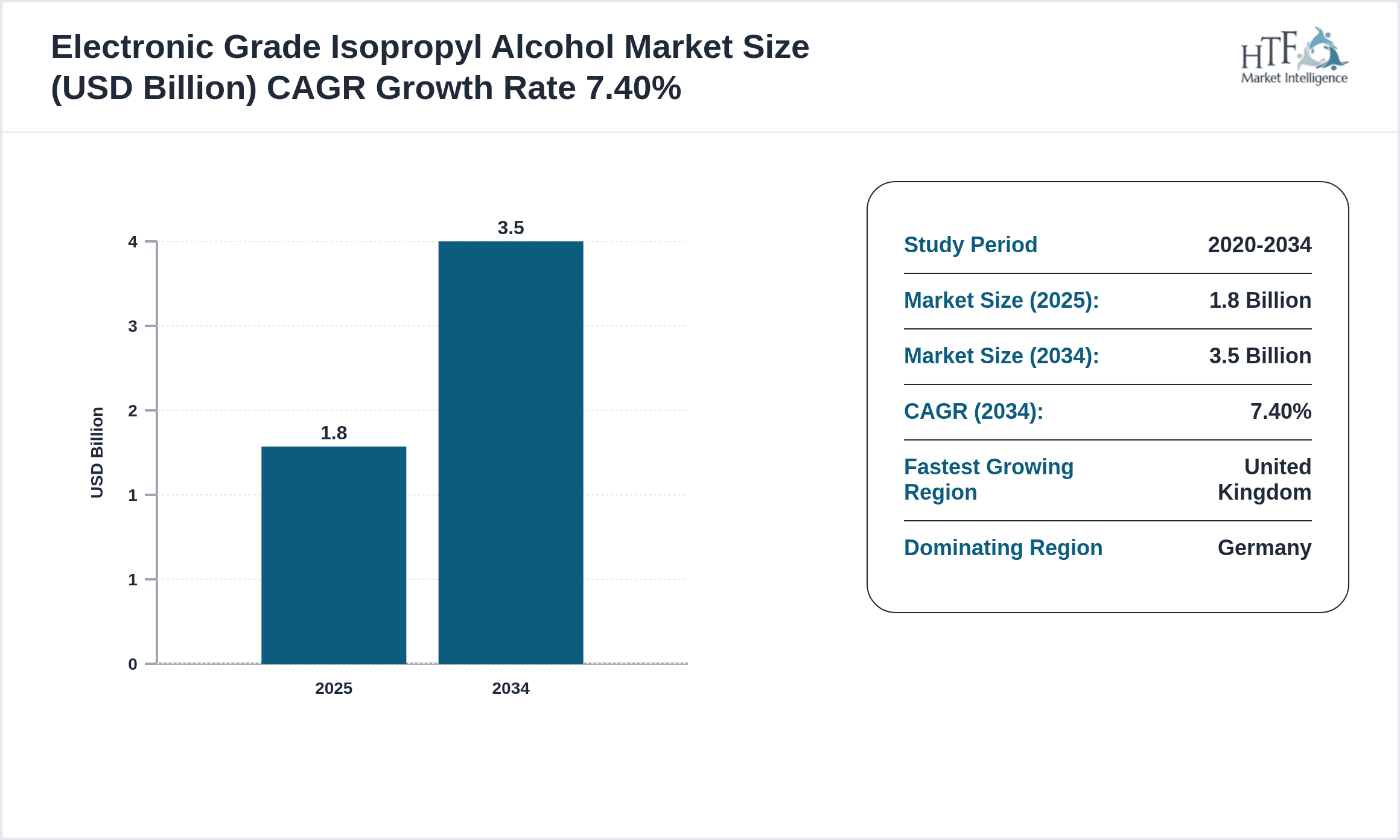

Market Size & Growth Table for EMEA Electronic Grade Isopropyl Alcohol

- •2020 Market Size: USD 1.2 Billion

- •2025 Market Size: USD 1.8 Billion

- •2034 Market Size: USD 3.5 Billion

- •CAGR: 7.4%

- •Year-on-Year Growth: 7.1%

Regional Performance Analysis

- •Dominating Country: Germany

- •Fastest Growing Country: United Kingdom

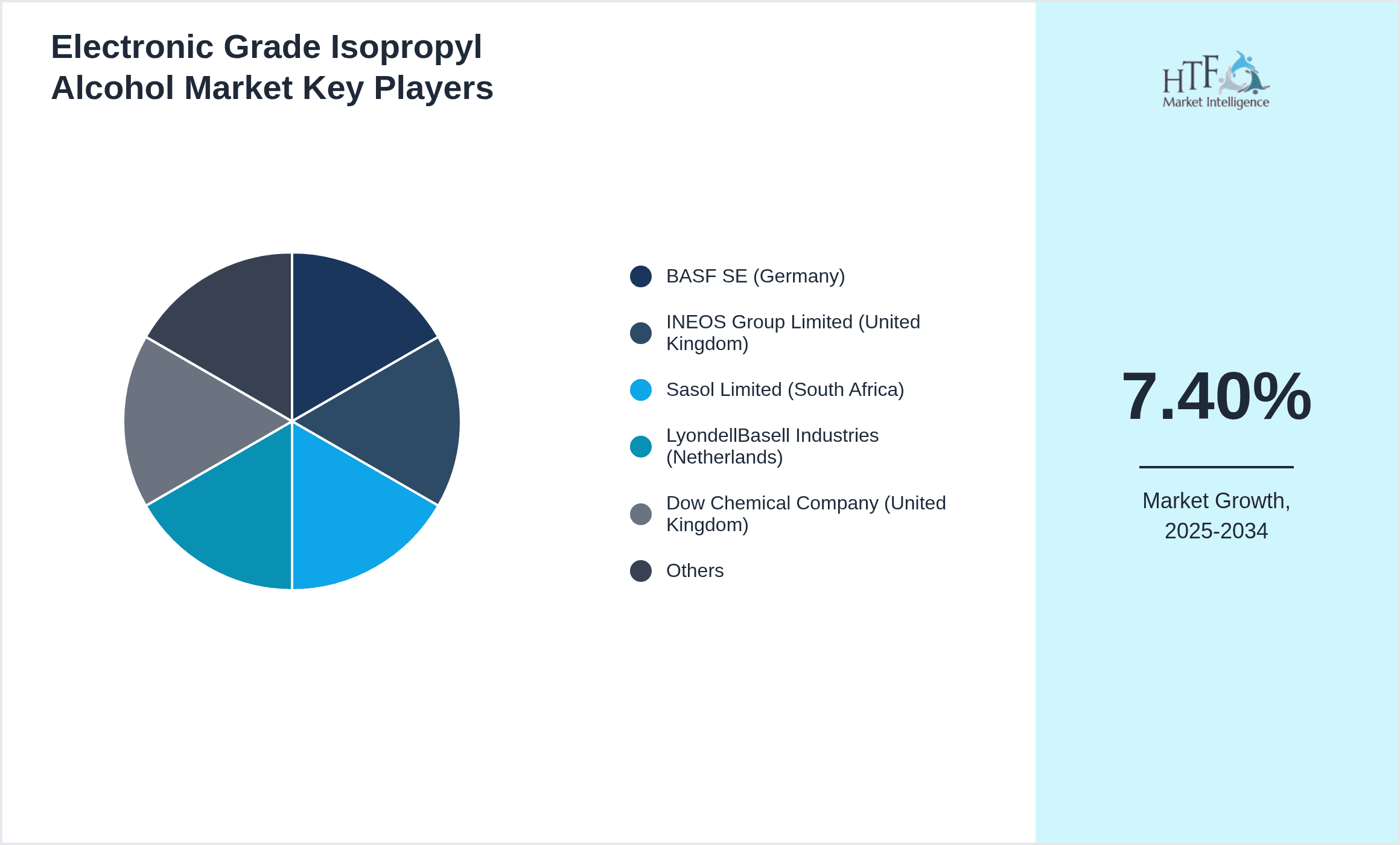

Players List of EMEA Electronic Grade Isopropyl Alcohol

- •BASF SE (Germany)

- •INEOS Group Limited (United Kingdom)

- •Sasol Limited (South Africa)

- •LyondellBasell Industries (Netherlands)

- •Dow Chemical Company (United Kingdom)

- •Evonik Industries AG (Germany)

- •Shell Chemicals Europe (Netherlands)

- •Arkema S.A. (France)

- •Clariant AG (Switzerland)

- •Sasol Chemicals Europe (United Kingdom)

- •SABIC Europe (Netherlands)

- •TotalEnergies Petrochemicals (France)

- •Solvay S.A. (Belgium)

- •Eastman Chemical Company (United Kingdom)

- •Perstorp Holding AB (Sweden)

- •Wacker Chemie AG (Germany)

- •Covestro AG (Germany)

- •Lanxess AG (Germany)

- •Mitsubishi Chemical Europe (Germany)

- •ExxonMobil Chemical Europe (United Kingdom)

- •Celanese Corporation (United Kingdom)

- •INEOS Oxide (Belgium)

- •INEOS Phenol (France)

- •Kemira Oyj (Finland)

- •Huntsman Corporation Europe (Switzerland)

Competitive Analysis

Competition in the EMEA electronic grade IPA market is relatively fragmented, with no single player holding overwhelming dominance. Major chemical companies leverage their integrated supply chains and broad geographic presence to maintain steady market shares. However, regional producers and niche specialists chip away at market segments by offering tailored solutions or localized distribution. Pricing battles are frequent given the commodity-like nature of IPA, but service reliability and product consistency remain critical differentiators. Some firms invest in sustainability and production efficiency to capture environmentally conscious buyers, though the cost premium limits broad impact. Partnerships with semiconductor fabs and pharmaceutical manufacturers are key strategic moves to lock in long-term demand. Overall, the market feels competitive but pragmatic, with players balancing innovation investments against tight margins and regulatory compliance costs.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Kingdom is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 3.5 Billion |

| CAGR | 7.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.1% |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | BASF SE (Germany), INEOS Group Limited (United Kingdom), Sasol Limited (South Africa), LyondellBasell Industries (Netherlands), Dow Chemical Company (United Kingdom), Evonik Industries AG (Germany), Shell Chemicals Europe (Netherlands), Arkema S.A. (France), Clariant AG (Switzerland), Sasol Chemicals Europe (United Kingdom), SABIC Europe (Netherlands), TotalEnergies Petrochemicals (France), Solvay S.A. (Belgium), Eastman Chemical Company (United Kingdom), Perstorp Holding AB (Sweden), Wacker Chemie AG (Germany), Covestro AG (Germany), Lanxess AG (Germany), Mitsubishi Chemical Europe (Germany), ExxonMobil Chemical Europe (United Kingdom), Celanese Corporation (United Kingdom), INEOS Oxide (Belgium), INEOS Phenol (France), Kemira Oyj (Finland), Huntsman Corporation Europe (Switzerland) |

EMEA Electronic Grade Isopropyl Alcohol Market - Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.