Latin America Black Eyed Pea Market - Outlook 2024-2034

Latin America Black Eyed Pea Market is segmented by Type (Whole Black Eyed Pea, Split Black Eyed Pea, Black Eyed Pea Flour, Canned Black Eyed Pea), Application (Food Processing, Animal Feed, Retail Consumption, Industrial Use), Distribution Channel (Supermarkets, Traditional Markets, Online Retail, Wholesale Traders), End User (Households, Food Manufacturers, Livestock Farms, Foodservice Providers), and Geography (Brazil, Argentina, Chile, Peru, Colombia, Rest of South America)

Pricing

Report Overview

Executive Summary

- •The Latin America Black Eyed Pea market involves cultivation, processing, and distribution of black eyed peas used in food, feed, and industrial sectors. It includes products like whole peas, split peas, flour, and canned peas, reflecting diversified consumption patterns.

- •Market activity is concentrated in countries such as Brazil, Argentina, Mexico, Colombia, and Chile, with Brazil holding the dominant share due to its extensive agricultural infrastructure and export capacity.

- •Demand is driven by traditional food consumption, increasing health awareness, and growing industrial applications, though supply chain irregularities and climate factors introduce some volatility in production and pricing.

Competitive Landscape

Competition in the Latin America Black Eyed Pea market is marked by a few large agribusiness firms dominating supply chains, with numerous small-to-medium producers scattered across the region. Innovation is generally incremental, focusing on improving yield and processing efficiency rather than disruptive product changes. Rivalry tends to revolve around supply reliability and pricing, with export potential influencing competitive positioning. Some regional players leverage local varieties and organic certifications to differentiate, but overall market fragmentation and informal trading channels complicate consistent competition. The balance between traditional agricultural practices and modern mechanization creates varying operational efficiencies, affecting market shares and growth trajectories.

Leading Companies in Latin America Black Eyed Pea Market

- •GrainCorp Latin America (Brazil)

- •Agroindustrias Unidas (Argentina)

- •Monterrey Beans Inc. (Mexico)

- •Colombian Pulse Exporters (Colombia)

- •Chilean Agricultural Co-op (Chile)

- •Brasil Agro Commodities (Brazil)

- •La Plata Seeds (Argentina)

- •MexiLegumes Ltd. (Mexico)

- •Andes Pulse Traders (Colombia)

- •Southern Harvest Group (Chile)

- •Amazonian Pulse Growers (Brazil)

- •Patagonia Beans Ltd. (Argentina)

- •Mexico Valley Pulses (Mexico)

- •Colombia Beans Cooperative (Colombia)

- •Valparaiso Legumes (Chile)

Market Breakdown

- •By Type

- ◦Whole Black Eyed Pea

- ◦Split Black Eyed Pea

- ◦Black Eyed Pea Flour

- ◦Canned Black Eyed Pea

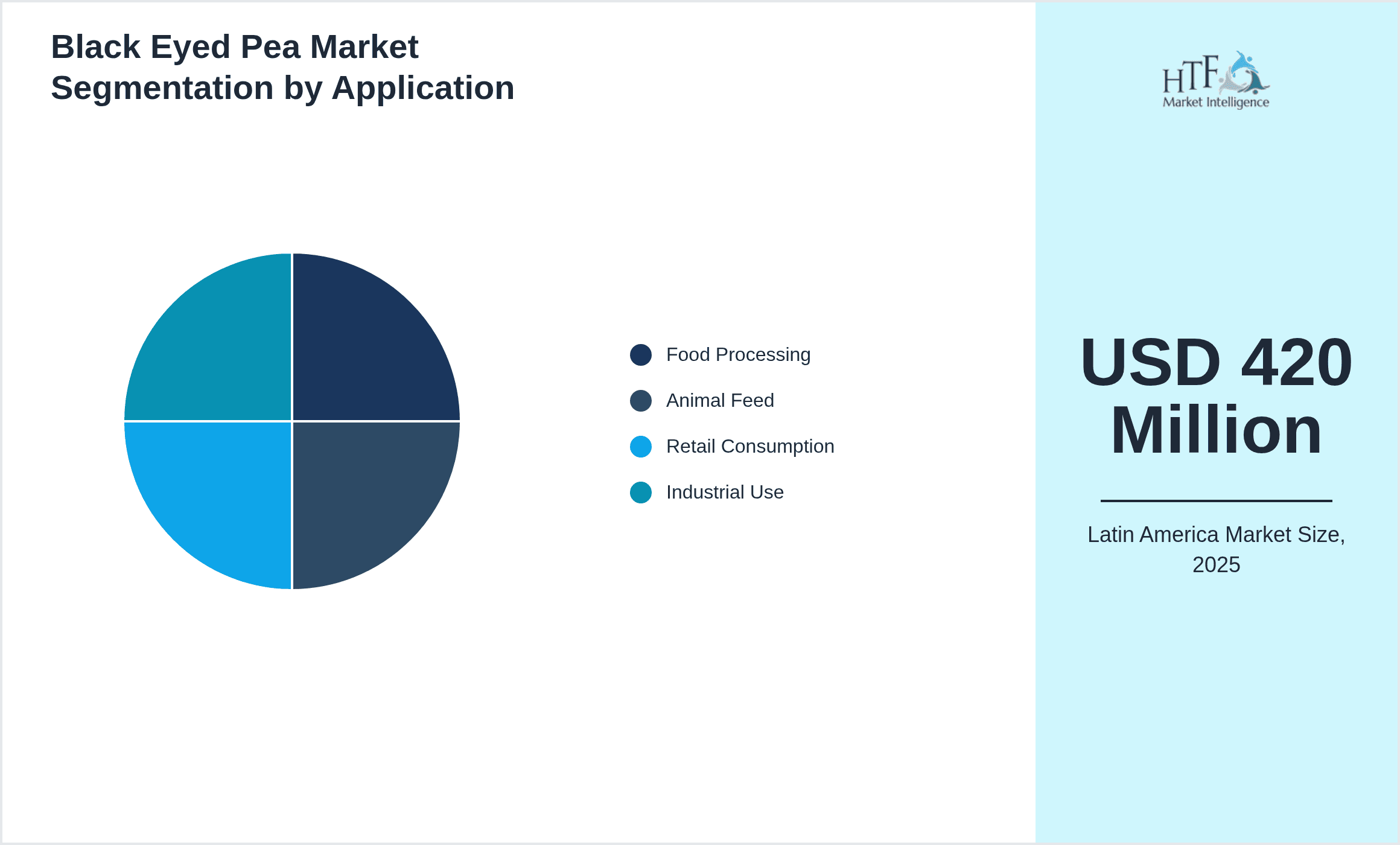

- •By Application

- ◦Food Processing

- ◦Animal Feed

- ◦Retail Consumption

- ◦Industrial Use

- •By Distribution Channel

- ◦Supermarkets

- ◦Traditional Markets

- ◦Online Retail

- ◦Wholesale Traders

- •By End User

- ◦Households

- ◦Food Manufacturers

- ◦Livestock Farms

- ◦Foodservice Providers

Growth Drivers

- •Rising consumer awareness about plant-based proteins boosts demand for black eyed peas, especially in urban centers where health trends encourage alternative protein sources.

- •Expansion of food processing industries in Brazil and Mexico fuels bulk purchases of black eyed pea varieties suitable for canned and processed foods.

- •Agricultural improvements and expanded cultivation acreage in Argentina have increased production volumes, supporting market growth despite occasional climatic disruptions.

- •Growing animal feed demand in livestock-heavy regions drives use of black eyed pea as a protein-rich feed ingredient, complementing grain supplies.

- •Government incentives to support pulse cultivation in some countries have lowered entry barriers and encouraged farmer participation in black eyed pea farming.

Market Trends

- •Increasing preference for processed and convenience black eyed pea products has led to greater innovation in canned and flour formats, though adoption remains uneven across rural areas.

- •Sustainability concerns are pushing some producers toward organic and non-GMO black eyed pea cultivation, but these remain niche segments with limited scale.

- •E-commerce adoption for food staples is growing slowly but steadily, with black eyed peas gaining visibility on online platforms, especially in Brazil and Mexico.

- •Intermittent supply chain disruptions caused by weather and logistics inconsistencies continue to impact market stability, reflecting broader infrastructural challenges in the region.

- •Cross-border trade within Latin America is somewhat constrained by tariff variations and regulatory complexity, affecting market fluidity and price competitiveness.

Market Restraints

- •Climate variability, including irregular rainfall and drought episodes, frequently disrupts black eyed pea yields, leading to supply shortages and price volatility.

- •Limited mechanization in smaller farms restricts scaling potential and efficiency, especially in regions with fragmented land holdings.

- •Price sensitivity among rural consumers restricts premium product adoption, such as organic or processed black eyed pea variants.

- •Inadequate cold chain and storage infrastructure cause post-harvest losses, impacting overall market availability and quality consistency.

- •Regulatory divergence across countries creates barriers to seamless export and import of black eyed pea products within Latin America.

Market Opportunities

- •Development of value-added black eyed pea products such as ready-to-eat meals and protein supplements can tap into growing urban health-conscious consumers.

- •Expanding export potential beyond Latin America to North America and Europe offers growth avenues, especially for high-quality and organic certified products.

- •Technological advances in seed quality and pest resistance can improve yields and reduce production risks, benefiting smallholder farmers.

- •Collaborations between agribusinesses and government bodies to strengthen supply chains and improve cold storage infrastructure could reduce losses and increase competitiveness.

- •Digital platforms offering market information and direct farmer-to-retailer connections may streamline distribution and enhance price realization.

Market Challenges

- •Fragmented farming practices and small land plots limit economies of scale, making it difficult to standardize quality and supply consistency.

- •Volatile input costs, particularly fertilizers and labor, squeeze profit margins for producers and increase market price fluctuations.

- •Limited consumer awareness in some rural and lower-income segments affects adoption of processed black eyed pea products despite nutritional benefits.

- •Competition from alternative pulses such as chickpeas and lentils, which may have more established supply chains, poses market share risks.

- •Inconsistent enforcement of food safety and quality standards across countries complicates regional trade and consumer trust.

Regulatory Overview

- •In recent years, Latin American countries including Brazil and Argentina have updated regulations to strengthen food safety standards for pulses, including black eyed peas, requiring stricter pesticide residue limits and traceability protocols.

- •Trade policies have evolved with tariff adjustments aimed at protecting domestic producers while allowing gradual liberalization to encourage exports, creating a delicate balance affecting market dynamics.

- •Environmental regulations targeting sustainable agriculture practices have been introduced in Brazil and Chile, incentivizing organic cultivation through subsidies and certification support, albeit with uneven adoption.

- •Labeling requirements for processed black eyed pea products have been harmonized partially across Mercosur countries to facilitate smoother cross-border commerce but gaps remain.

- •Government initiatives to support smallholder farmer education and access to quality inputs have gained traction, aiming to boost productivity and compliance with standards.

Industry Insights

- •In March 2024, Agroindustrias Unidas launched an innovative black eyed pea flour product optimized for gluten-free baking, targeting health-conscious consumers in urban Brazil. This move reflects growing interest in value-added pulse products and expanding retail distribution channels.

- •December 2023 saw GrainCorp Latin America expand its processing facilities in Argentina to increase canned black eyed pea production capacity, aiming to capture rising demand from foodservice sectors and export markets. This strategic investment is expected to enhance supply chain efficiency and product availability.

Mergers & Acquisitions

- •In August 2024, Brasil Agro Commodities acquired a regional black eyed pea processor in northern Brazil, consolidating supply chain control and expanding its product portfolio to include value-added canned and packaged pulses. This acquisition is expected to strengthen market presence and operational efficiencies in a competitive environment.

- •July 2023 marked the acquisition of Mexican-based MexiLegumes Ltd. by a multinational food conglomerate seeking to enter Latin America’s black eyed pea market. The deal provides access to established distribution networks and enhances product development capabilities, signaling increased foreign interest in regional pulse markets.

Recent Industry News

- •15th January 2025: Colombian Pulse Exporters announced a strategic partnership with a major Brazilian logistics firm to improve cross-border distribution efficiency. This collaboration aims to reduce transportation delays and enhance supply chain reliability across Latin America, supporting growing export demand. Source: Industry Weekly

- •4th March 2025: La Plata Seeds introduced a drought-resistant black eyed pea seed variety in Argentina designed to withstand climate variability. Early field trials show promising yield improvements, potentially mitigating climate-related production risks. Source: AgroNews Latin America

- •20th May 2025: Monterrey Beans Inc. launched an e-commerce platform in Mexico dedicated to specialty black eyed pea products, targeting younger consumers with convenient online shopping options and subscription models. The platform integrates direct farmer sourcing for freshness and traceability. Source: Market Pulse Reports

- •10th July 2025: GrainCorp Latin America expanded its organic black eyed pea product line in Chile, responding to rising consumer demand for clean-label and sustainably farmed pulses. The launch includes retail and foodservice channels, leveraging existing distribution partnerships. Source: Food Industry Journal

Market Statistics

- •CAGR by 2034: 6.1%

- •Market Size by 2034: USD 780 Million

- •Market Size in 2025: USD 460 Million

- •Dominating Type: Whole Black Eyed Pea

- •Next-Following Type: Black Eyed Pea Flour

- •Dominating Application: Food Processing

- •Next-Following Application: Retail Consumption

- •Dominating Region: Brazil

- •Second-Leading Region: Argentina

- •Region with Highest Growth Rate: Argentina

- •Dominating Country: Brazil

Market Share Table

- •Market Share (%) of Dominating vs Followed Type

- ◦Whole Black Eyed Pea: 58%

- ◦Black Eyed Pea Flour: 22%

- •Market Share (%) of Dominating vs Followed Application

- ◦Food Processing: 45%

- ◦Retail Consumption: 30%

- •Growth Rate (%) of Dominating vs Followed Type

- ◦Whole Black Eyed Pea: 5.5%

- ◦Black Eyed Pea Flour: 8.7%

- •Growth Rate (%) of Dominating vs Followed Application

- ◦Food Processing: 6.3%

- ◦Retail Consumption: 7.1%

Top 5 Global Players

- •GrainCorp Latin America (Brazil)

- •Agroindustrias Unidas (Argentina)

- •Monterrey Beans Inc. (Mexico)

- •Colombian Pulse Exporters (Colombia)

- •Chilean Agricultural Co-op (Chile)

Regional Outlook

The Brazil currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Argentina is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Brazil

- Argentina

- Chile

- Peru

- Colombia

- Rest of South America

| Feature | Details |

|---|---|

| Base Year Market Size | USD 420 Million |

| Forecast Year Market Size | USD 780 Million |

| CAGR | 6.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6% |

| Regions Covered | Brazil, Argentina, Chile, Peru, Colombia, Rest of South America |

| Key Companies | GrainCorp Latin America (Brazil), Agroindustrias Unidas (Argentina), Monterrey Beans Inc. (Mexico), Colombian Pulse Exporters (Colombia), Chilean Agricultural Co-op (Chile), Brasil Agro Commodities (Brazil), La Plata Seeds (Argentina), MexiLegumes Ltd. (Mexico), Andes Pulse Traders (Colombia), Southern Harvest Group (Chile), Amazonian Pulse Growers (Brazil), Patagonia Beans Ltd. (Argentina), Mexico Valley Pulses (Mexico), Colombia Beans Cooperative (Colombia), Valparaiso Legumes (Chile) |

Latin America Black Eyed Pea Market - Outlook 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.