EMEA Acoustical PET Panel Market Size, Growth & Revenue 2024-2034

EMEA Acoustical PET Panel Market is segmented by Type (Standard PET Acoustic Panels, Enhanced PET Acoustic Panels, Fire-Retardant PET Panels, Recycled PET Acoustic Panels, Custom PET Panels), Application (Commercial Buildings, Residential Buildings, Industrial Facilities, Transportation, Public Infrastructure), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

- •The EMEA Acoustical PET Panel market involves manufacturing and supplying PET-based acoustical panels designed for sound absorption and noise reduction across commercial, residential, industrial, transportation, and public infrastructure applications. It covers a broad spectrum of panel types including standard, enhanced, fire-retardant, recycled, and custom variants, catering to diverse functional and environmental needs.

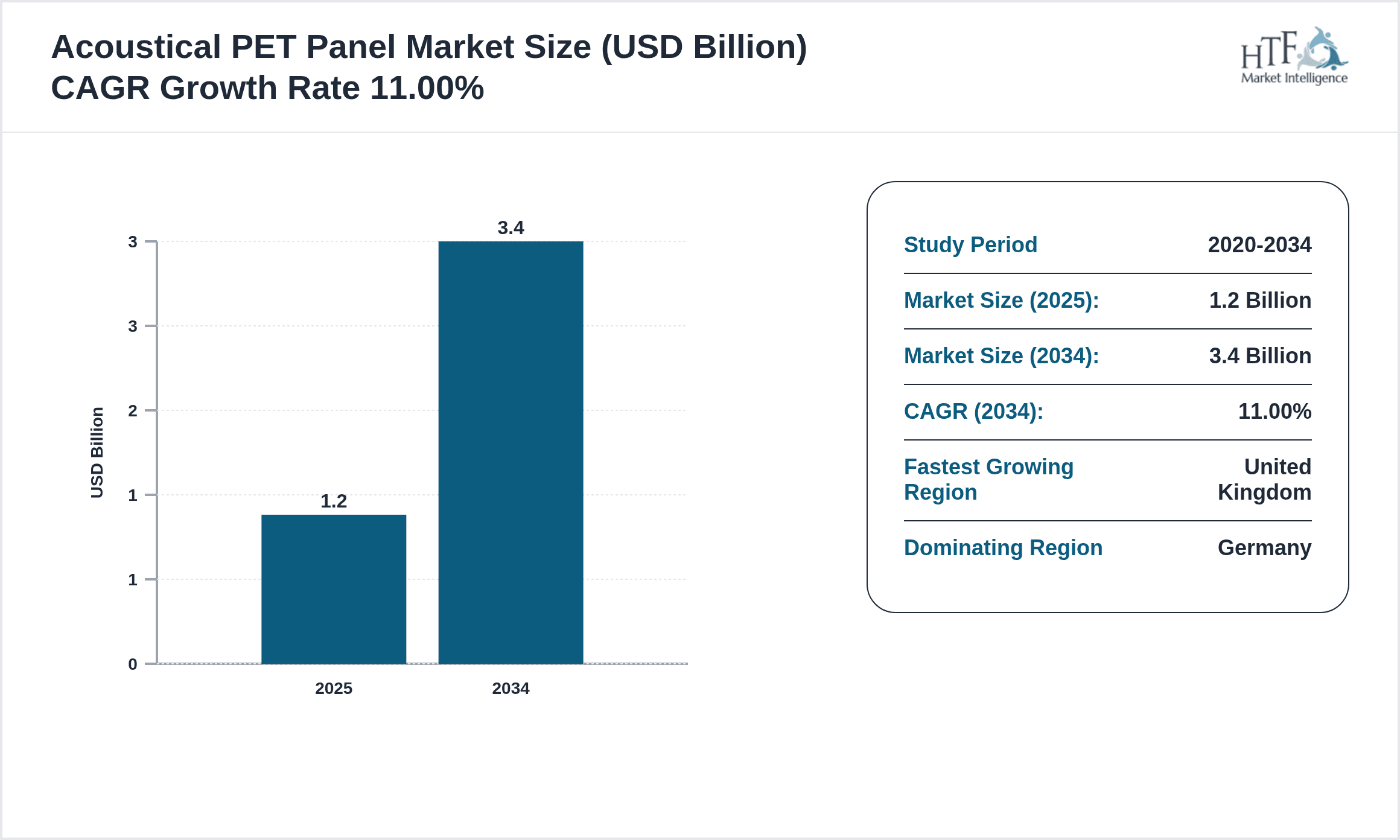

- •Key market highlights include a base market size of USD 1.2 Billion in 2024, projected to grow to USD 3.4 Billion by 2034 at a CAGR of 11%, driven by increasing construction activities, sustainability mandates, and urbanization across the EMEA region.

- •The market holds strategic importance for stakeholders such as architects, builders, and facility managers focused on improving indoor acoustics while adhering to evolving environmental regulations, thereby enhancing urban living and working environments throughout EMEA.

Competitive Landscape

Competition in the EMEA Acoustical PET Panel market is characterized by a mix of global corporations and regional specialists focusing on innovation in material composition, sustainability, and acoustic performance. Companies compete through product differentiation, including fire-retardancy and recycled content, and via strategic partnerships to expand geographic reach. Rivalry is intensified by increasing demand for eco-friendly solutions and tightening regulatory standards, prompting continuous R&D investments. Market players strategically utilize diversified distribution networks and tailor solutions to country-specific building codes and acoustic requirements. Technological advancements in panel design and manufacturing efficiency further shape competitive dynamics, while mergers and acquisitions are commonly employed to consolidate market position and access new customer segments. Overall, the competitive landscape is vibrant, with innovation and regional adaptability being critical success factors.

Leading Companies in EMEA Acoustical PET Panel Market

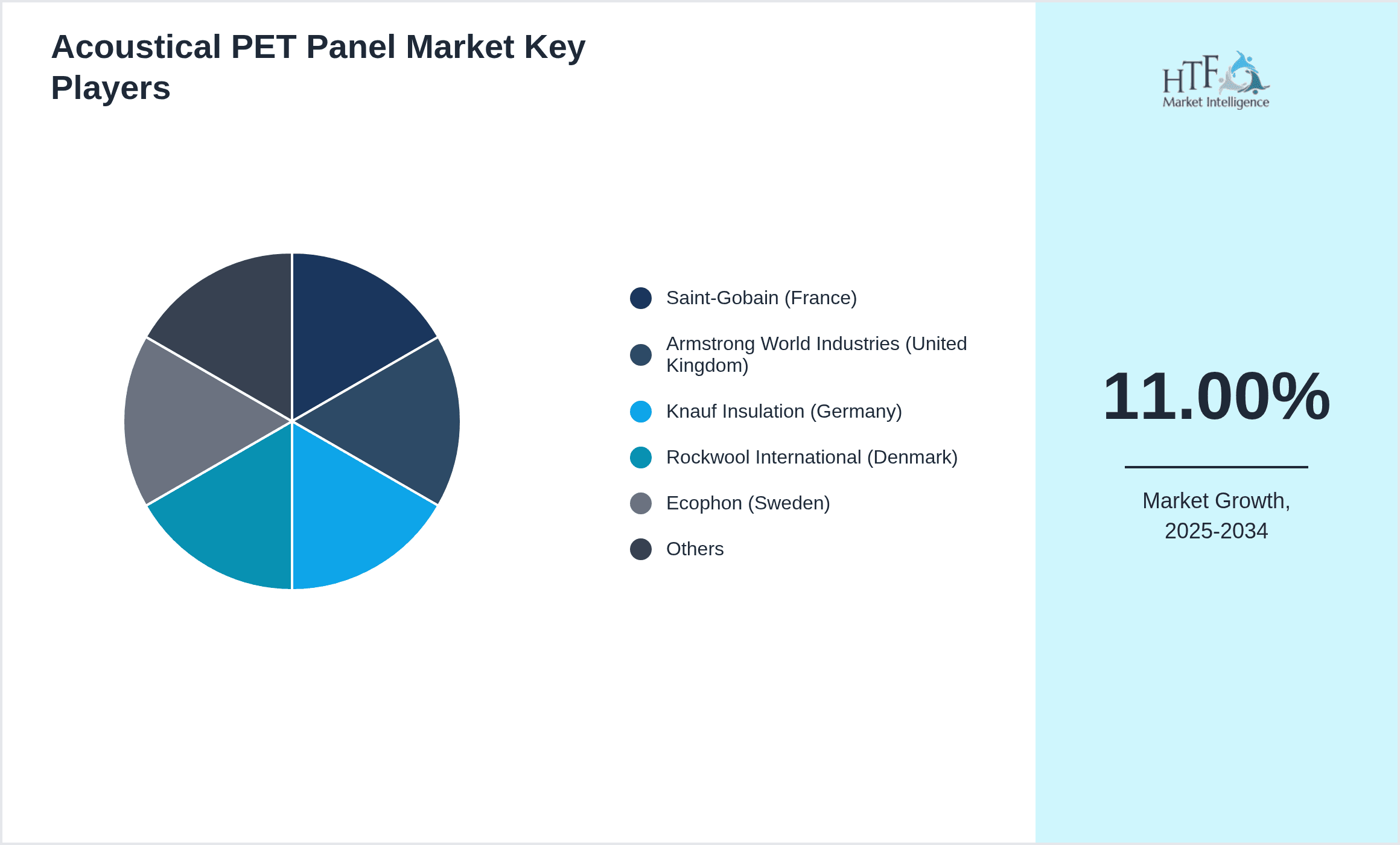

- •Saint-Gobain (France)

- •Armstrong World Industries (United Kingdom)

- •Knauf Insulation (Germany)

- •Rockwool International (Denmark)

- •Ecophon (Sweden)

- •Acoustical Surfaces Europe (United Kingdom)

- •Fakro Group (Poland)

- •Decoustics (France)

- •Basotect GmbH (Germany)

- •Unilin Insulation (Belgium)

- •Armacell (Germany)

- •Mitsubishi Polyester Film GmbH (Germany)

- •Interface Inc. (Netherlands)

- •JSP Group (United Kingdom)

- •Knauf AMF (Germany)

- •Ecowave (Italy)

- •Sonae Indústria (Portugal)

- •Finsa (Spain)

- •Isover Saint-Gobain (France)

- •BASF SE (Germany)

Market Breakdown

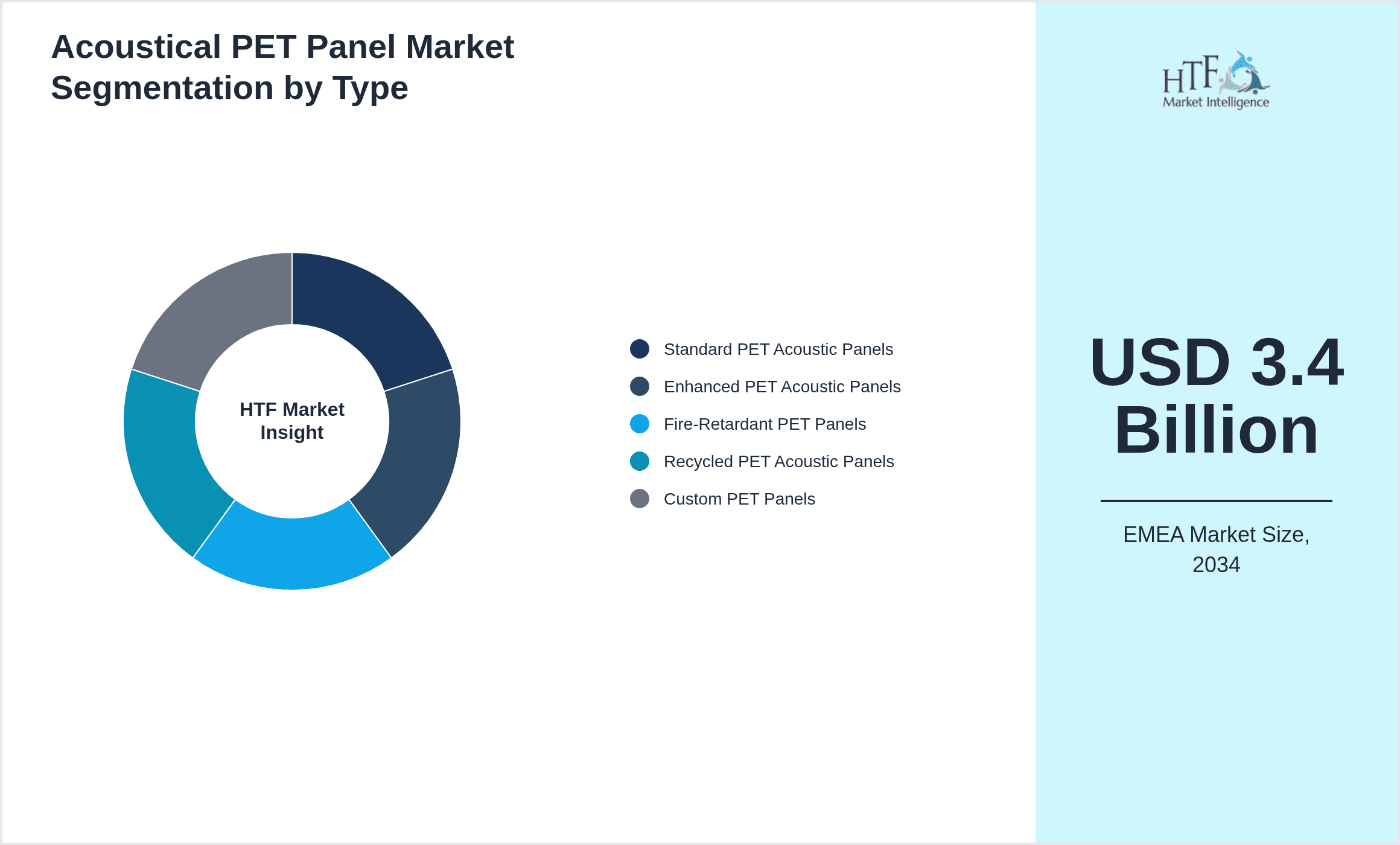

- •By Type

- ◦Standard PET Acoustic Panels

- ◦Enhanced PET Acoustic Panels

- ◦Fire-Retardant PET Panels

- ◦Recycled PET Acoustic Panels

- ◦Custom PET Panels

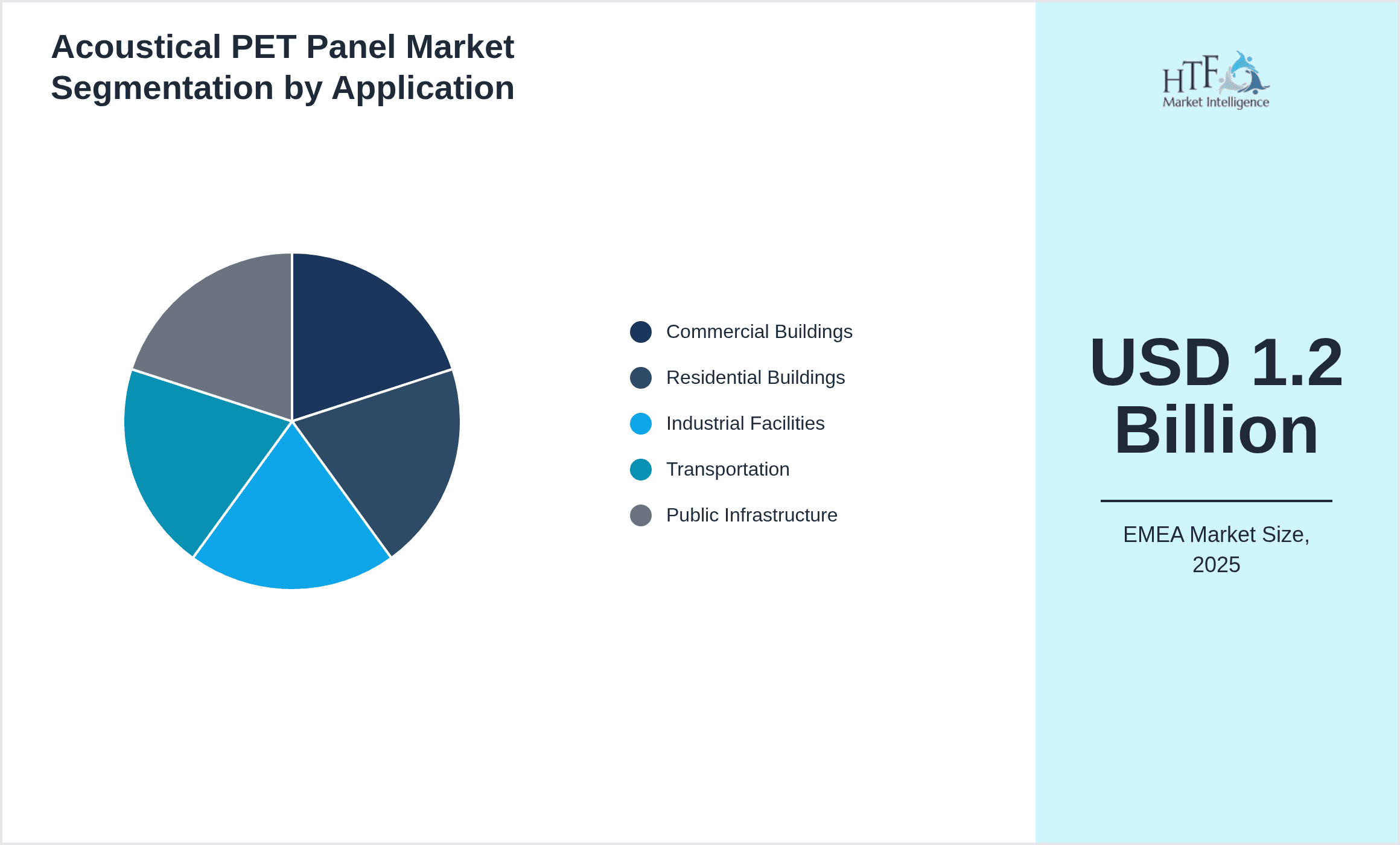

- •By Application

- ◦Commercial Buildings

- ◦Residential Buildings

- ◦Industrial Facilities

- ◦Transportation

- ◦Public Infrastructure

- •By End User

- ◦Construction Companies

- ◦Architectural Firms

- ◦Facility Management

- ◦Government and Public Sector

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Sales

- ◦Retailers

Growth Drivers

- •The EMEA Acoustical PET Panel market growth is primarily fueled by rising construction and urbanization trends in Europe and Middle East, with increasing demand for noise control solutions in commercial and residential infrastructure. Government regulations promoting green building standards encourage adoption of sustainable PET panels, especially recycled variants, contributing significantly to market expansion.

- •Technological advancements in PET panel manufacturing, including enhanced fire-retardant and acoustic performance, increase product applicability and compliance with stringent building codes. This innovation attracts architects and builders seeking efficient, regulation-compliant materials, thereby driving market uptake.

- •The growing awareness of indoor environmental quality and occupant comfort in workplaces and homes stimulates demand for acoustical solutions that reduce noise pollution, boosting consumption of PET acoustic panels across diverse applications.

- •Increasing investments in public infrastructure projects across the EMEA region, particularly in transportation hubs and educational institutions, create large-scale opportunities for acoustical panel implementation, further accelerating market growth.

- •Sustainability initiatives and circular economy adoption in Europe drive preference for recycled PET panels, enabling manufacturers to meet eco-conscious consumer demands and regulatory expectations, positively impacting market trajectory.

Market Trends

- •A key trend in the EMEA market is the shift towards eco-friendly acoustical panels incorporating recycled PET materials, driven by stringent environmental policies and consumer preference for sustainable building products.

- •Integration of smart acoustical solutions combining PET panels with sensor technologies to monitor and adapt to ambient noise levels is emerging, reflecting innovation in the sector aimed at enhancing user experience.

- •The adoption of modular and customizable PET acoustic panels tailored for aesthetic and functional needs is gaining traction, enabling architects to blend design with acoustical performance seamlessly.

- •Digitalization of sales and distribution channels, including online platforms offering detailed product specifications and customization options, is transforming buyer engagement and market accessibility.

- •Collaborations between PET panel manufacturers and construction firms to co-develop integrated acoustical solutions are increasing, fostering innovation and faster market penetration.

Market Restraints

- •High raw material costs and price volatility for PET resins pose significant barriers to market growth, affecting manufacturers’ profitability and pricing strategies in EMEA.

- •Limited awareness among small and medium construction enterprises regarding the benefits and applications of acoustical PET panels restricts market penetration in certain EMEA countries.

- •Stringent fire safety regulations vary by country within EMEA, complicating product certification processes and delaying market entry for new panel types.

- •Competition from alternative acoustical materials such as mineral wool and fiberglass panels, which are well-established and sometimes cost-effective, constrains PET panel market share.

- •Challenges in recycling and waste management infrastructure in some Middle Eastern and African countries limit the adoption of recycled PET acoustic panels region-wide.

Market Opportunities

- •Expanding adoption of green building certifications like LEED and BREEAM in Europe offers significant opportunities for manufacturers to promote sustainable acoustical PET panels aligned with these standards.

- •Emerging markets within the Middle East and Africa with increasing infrastructure investments present untapped potential for acoustical PET panel deployment, especially in commercial and public sectors.

- •Advancements in PET material science enabling improved fire-retardant and sound absorption properties create scope for new product introductions catering to stringent building codes.

- •Collaborations with architectural and interior design firms to develop aesthetically versatile acoustical panels can open new market segments and enhance product differentiation.

- •Digital marketing and e-commerce platforms tailored for the construction materials sector can enhance direct-to-customer sales and broaden market outreach across EMEA.

Market Challenges

- •Navigating diverse regulatory requirements across the multiple countries within EMEA complicates compliance and slows product launches, requiring significant investment in certification and testing.

- •Supply chain disruptions caused by geopolitical tensions and trade barriers within the region impact raw material availability and increase lead times for PET panel manufacturers.

- •Intense price competition from established alternative acoustical products pressures margins and reduces incentives for innovation among smaller manufacturers.

- •Limited skilled workforce for specialized PET panel manufacturing and installation in certain EMEA countries constrains the ability to meet rising demand effectively.

- •Consumer hesitation towards adopting newer, recycled PET materials due to perceived performance concerns inhibits market expansion, necessitating increased education and demonstration projects.

Industry Insights

- •The EMEA Acoustical PET Panel market has witnessed notable innovation with the launch of fire-retardant recycled PET panels by several manufacturers in late 2023, combining sustainability with enhanced safety features. This development aligns with growing regional emphasis on green construction and stringent fire codes. Additionally, in mid-2022, a leading European panel producer introduced a modular acoustic system that integrates PET panels with smart noise monitoring sensors, targeting commercial and public infrastructure segments to enhance indoor environmental quality. These innovations reflect the market’s trajectory towards multifunctional, eco-friendly, and technologically advanced solutions, positioning EMEA as a leading adopter of next-generation acoustical materials.

- •Furthermore, strategic partnerships between PET panel manufacturers and architectural firms have intensified in 2023, focusing on co-developing customizable panels with superior acoustic and aesthetic properties. This trend is expected to accelerate market adoption in premium commercial and residential projects, providing competitive differentiation and meeting sophisticated design requirements across EMEA.

Regulatory Overview

Recent years have seen the enforcement of stricter fire safety regulations in EMEA, particularly in the European Union, mandating higher fire-resistance ratings for building materials including acoustical panels. The EU Construction Products Regulation (CPR) updates between 2020 and 2024 require manufacturers to provide enhanced product labeling and performance data. Simultaneously, sustainability directives emphasize the use of recycled materials and lifecycle assessments, pushing the market towards eco-friendly PET panels. Countries such as Germany and France have implemented additional national standards that influence product certification and installation practices, shaping the compliance landscape and encouraging innovation in material formulations to meet these evolving requirements.

Mergers & Acquisitions

- •In November 2023, Saint-Gobain expanded its acoustical materials portfolio by acquiring a regional PET panel manufacturer based in Poland. This strategic acquisition enhances Saint-Gobain’s capacity to supply customized and sustainable acoustical PET panels across Central and Eastern Europe, strengthening its market leadership and facilitating entry into emerging markets within the EMEA region. The deal supports technology transfer and broadens the product offering to include advanced fire-retardant and recycled PET panels, aligning with regional regulatory trends and customer demand.

- •In March 2022, Knauf Insulation completed the acquisition of a UK-based acoustical panel specialist, augmenting its presence in the United Kingdom and Northern Europe markets. This move allows Knauf to integrate innovative PET-based acoustic solutions into its insulation product range, offering comprehensive noise control systems to commercial and residential sectors. The acquisition accelerates Knauf’s growth strategy focused on sustainability and product innovation, addressing the rising demand for environmentally responsible building materials within EMEA.

Recent Industry News

- •15th January 2024, Armstong World Industries launched a new line of enhanced PET acoustical panels featuring improved fire-retardant properties and up to 50% recycled content. The product targets commercial building applications with a focus on meeting stringent European fire safety and sustainability standards, aiming to capture growing demand across key EMEA markets. Source: Armstrong World Industries Official Press Release

- •30th June 2023, Ecophon announced a strategic partnership with a leading Middle Eastern construction firm to supply acoustical PET panels for multiple public infrastructure projects, including airports and hospitals. This collaboration enhances Ecophon’s market penetration in the Gulf Cooperation Council (GCC) region by leveraging the partner’s extensive local network and expertise. Source: Ecophon Corporate Website

- •20th September 2022, Basotect GmbH introduced an innovative modular acoustical panel system integrating PET materials with active noise cancellation technology, designed for industrial facilities and transportation hubs. The product launch is expected to set new standards in acoustic performance and adaptability within EMEA markets. Source: Basotect GmbH Industry News

- •5th March 2021, Unilin Insulation expanded its manufacturing capacity in Belgium to meet increasing demand for recycled PET acoustic panels, reinforcing its commitment to sustainability and circular economy principles. The expansion supports supply chain efficiency and accelerates delivery timelines across European markets. Source: Unilin Insulation Annual Report

Market Statistics

- •CAGR by 2034: 11.0%

- •Market Size by 2034: USD 3.4 Billion

- •Market Size in 2025: USD 1.35 Billion

- •Dominating Type: Standard PET Acoustic Panels

- •Next-Following Type: Recycled PET Acoustic Panels

- •Dominating Application: Commercial Buildings

- •Next-Following Application: Residential Buildings

- •Dominating Region: Germany

- •Second-Leading Region: France

- •Region with Highest Growth Rate: United Kingdom

- •Dominating Country: Germany

Market Share Table

- •Market Share (%) of Dominating vs Followed Type: Standard PET Acoustic Panels (55%) vs Recycled PET Acoustic Panels (25%)

- •Market Share (%) of Dominating vs Followed Application: Commercial Buildings (45%) vs Residential Buildings (30%)

- •Growth Rate (%) of Dominating vs Followed Type: Standard PET Acoustic Panels (10.2%) vs Recycled PET Acoustic Panels (13.5%)

- •Growth Rate (%) of Dominating vs Followed Application: Commercial Buildings (10.8%) vs Residential Buildings (11.3%)

Top 5 Global Players

- •Saint-Gobain (France)

- •Armstrong World Industries (United Kingdom)

- •Knauf Insulation (Germany)

- •Rockwool International (Denmark)

- •Ecophon (Sweden)

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Kingdom is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.2 Billion |

| Forecast Year Market Size | USD 3.4 Billion |

| CAGR | 11% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10.5% |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | Saint-Gobain (France), Armstrong World Industries (United Kingdom), Knauf Insulation (Germany), Rockwool International (Denmark), Ecophon (Sweden), Acoustical Surfaces Europe (United Kingdom), Fakro Group (Poland), Decoustics (France), Basotect GmbH (Germany), Unilin Insulation (Belgium), Armacell (Germany), Mitsubishi Polyester Film GmbH (Germany), Interface Inc. (Netherlands), JSP Group (United Kingdom), Knauf AMF (Germany), Ecowave (Italy), Sonae Indústria (Portugal), Finsa (Spain), Isover Saint-Gobain (France), BASF SE (Germany) |

EMEA Acoustical PET Panel Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.