EMEA Heavy Duty Trucks Forged Wheels Market Size, Growth & Revenue 2024-2034

EMEA Heavy Duty Trucks Forged Wheels Market is segmented by Type (Aluminum Forged Wheels, Steel Forged Wheels, Magnesium Forged Wheels, Composite Forged Wheels, Titanium Forged Wheels), Application (Long-Haul Trucks, Construction Vehicles, Mining Trucks, Agricultural Trucks, Distribution Trucks), End-User Segment (Original Equipment Manufacturers (OEMs), Aftermarket Suppliers, Fleet Operators, Independent Truck Owners), Distribution Channel (Direct Sales, Dealerships and Distributors, Online Retail Platforms), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

- •The EMEA Heavy Duty Trucks Forged Wheels market focuses on production and application of forged wheels tailored for heavy-duty trucks operating within Europe, the Middle East, and Africa. The market includes a variety of forged wheel materials such as aluminum, steel, magnesium, composite, and titanium, each designed to meet rigorous performance and durability standards for sectors including long-haul transport, construction, mining, and agriculture. Key industry drivers include technological advancements in forging processes, increased demand for lightweight and fuel-efficient components, and stringent regional safety and environmental regulations.

- •Market highlights include a 10.3% CAGR forecasted from 2024 to 2034, with the base market size estimated at USD 1.1 Billion in 2024 and expected to reach USD 2.8 Billion by 2034. Germany dominates the regional market with a 30% share, while Poland exhibits the fastest growth rate at 14.2% CAGR. Aluminum forged wheels lead the product segment, closely followed by steel forged wheels, driven by their balance of strength and weight savings.

- •The market offers strategic value to OEMs, aftermarket suppliers, and heavy vehicle operators by enhancing vehicle performance, safety, and sustainability. Continuous innovation, compliance with evolving regulatory frameworks, and expanding applications across various heavy-duty truck segments underscore the market’s importance in the EMEA heavy vehicle ecosystem.

Competitive Landscape

The EMEA Heavy Duty Trucks Forged Wheels market is highly competitive, characterized by a blend of established multinational manufacturers and specialized regional players. Competition revolves around innovation in forging technologies, material development, and customization capabilities. Companies focus on enhancing product durability, reducing weight for improved fuel efficiency, and meeting stringent safety and environmental regulations to differentiate themselves. Strategic partnerships, investments in R&D, and expansion into emerging markets within EMEA intensify rivalry. Pricing strategies, quality certifications, and robust distribution networks also play critical roles in market positioning. The competitive environment drives continuous improvements and adoption of advanced materials such as composites and titanium to capture new applications and customer segments.

Leading Companies in Heavy Duty Trucks Forged Wheels Market

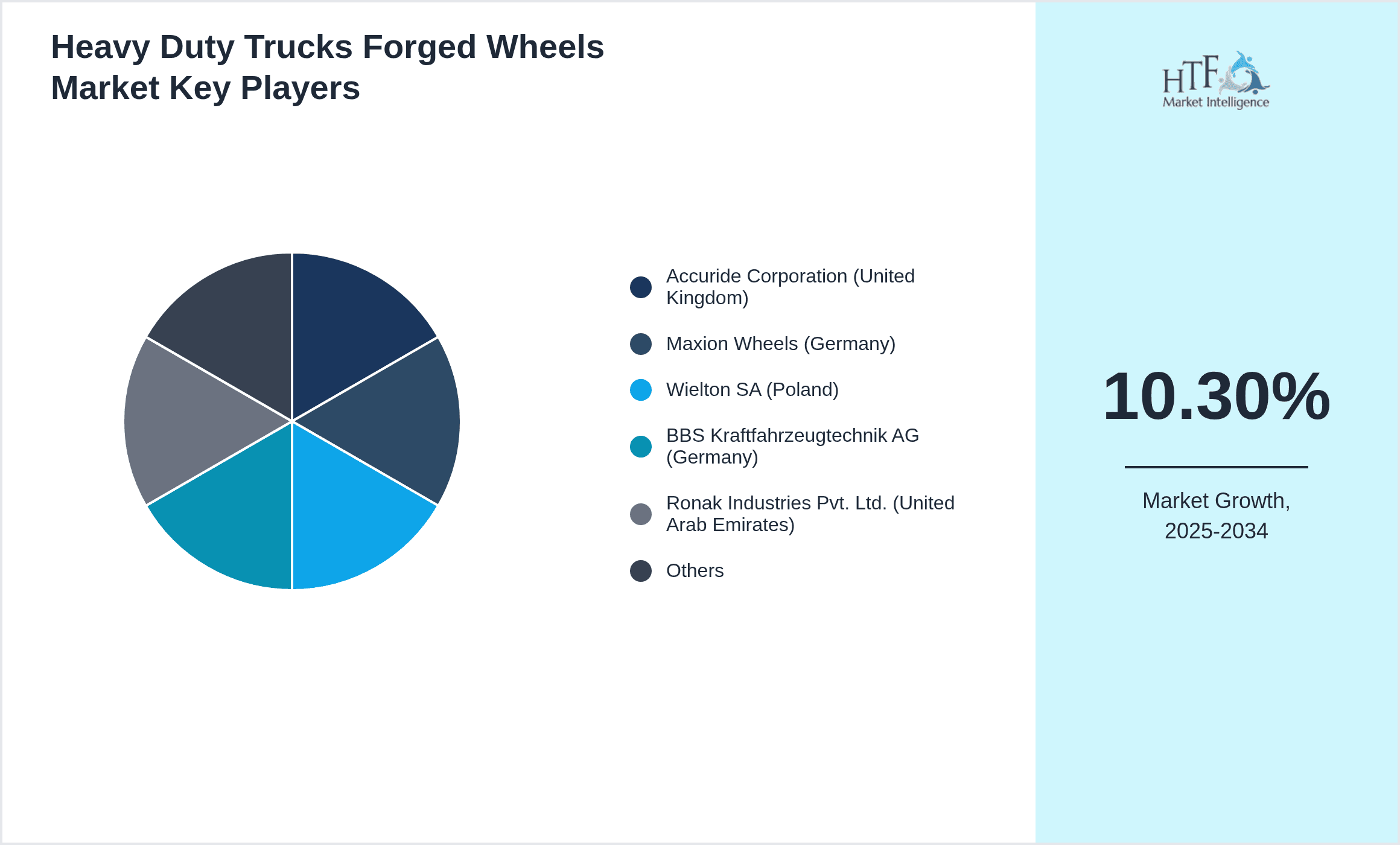

- •Accuride Corporation (United Kingdom)

- •Maxion Wheels (Germany)

- •Wielton SA (Poland)

- •BBS Kraftfahrzeugtechnik AG (Germany)

- •Ronak Industries Pvt. Ltd. (United Arab Emirates)

- •Alcoa Wheels (France)

- •ZF Friedrichshafen AG (Germany)

- •Steelwheels Europe GmbH (Germany)

- •Fast Wheels Ltd. (United Kingdom)

- •Magna Forged Wheels (Italy)

- •Titanium Wheels Solutions (South Africa)

- •Forged Excellence GmbH (Germany)

- •Euro Forged Wheels (France)

- •Kapsen Wheels (Poland)

- •Duraforge Technologies (United Kingdom)

- •Middle East Wheel Works (United Arab Emirates)

- •Vulcan Wheels (Germany)

- •HeavyDuty Forged Wheels Ltd. (Italy)

- •Nordic Forged Wheels (Sweden)

- •Atlas Forged Wheels (France)

Market Breakdown

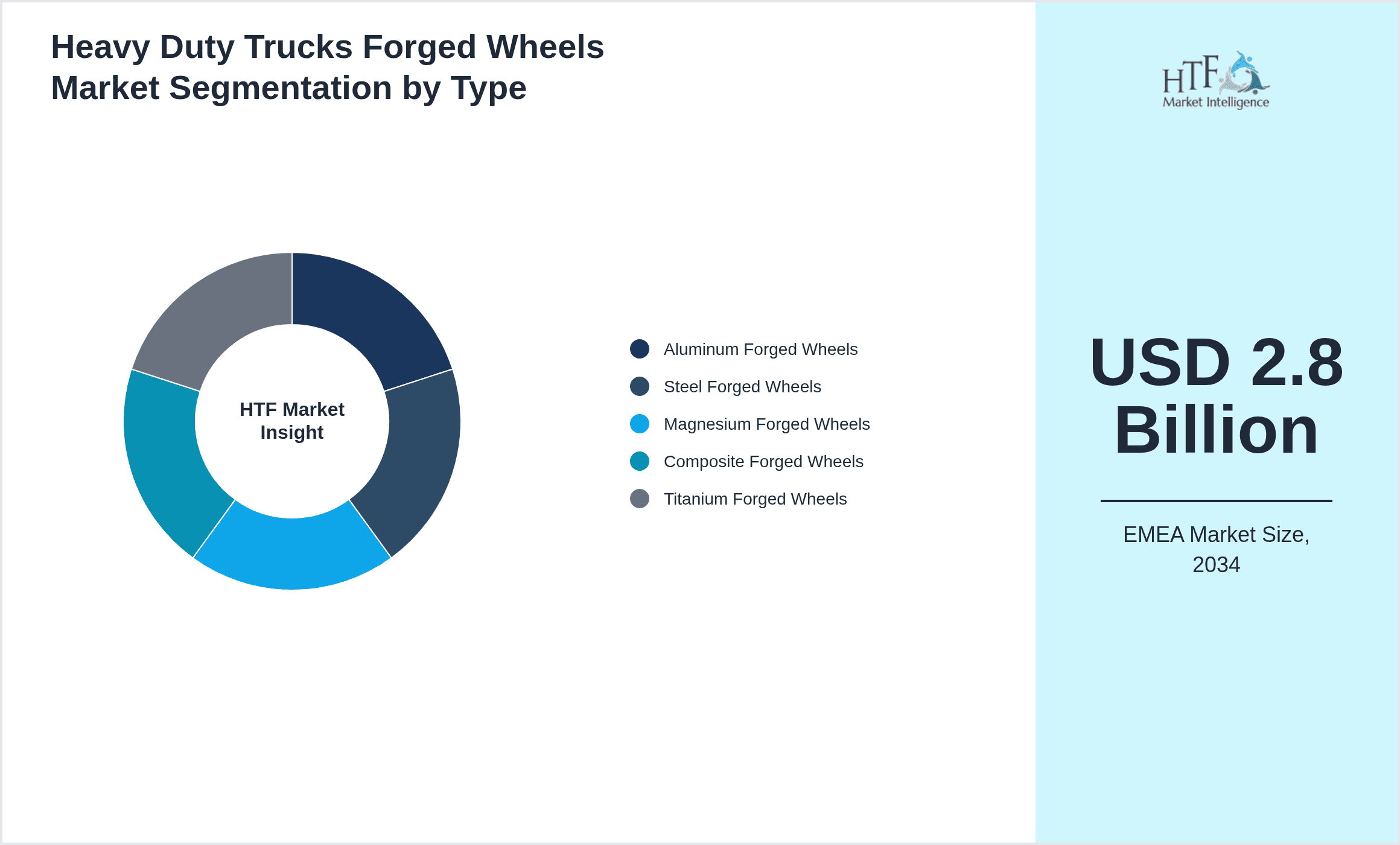

- •By Type

- ◦Aluminum Forged Wheels

- ◦Steel Forged Wheels

- ◦Magnesium Forged Wheels

- ◦Composite Forged Wheels

- ◦Titanium Forged Wheels

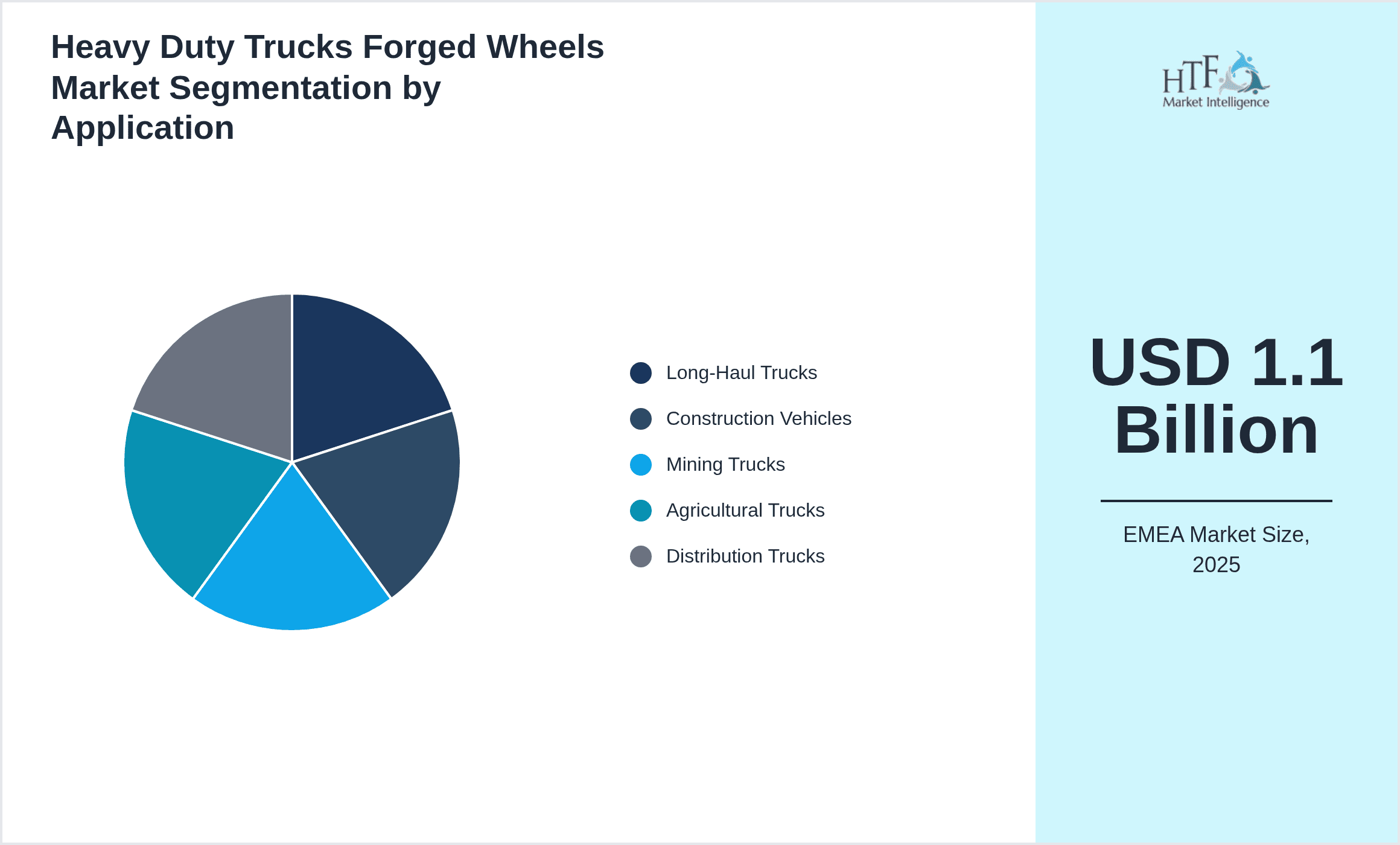

- •By Application

- ◦Long-Haul Trucks

- ◦Construction Vehicles

- ◦Mining Trucks

- ◦Agricultural Trucks

- ◦Distribution Trucks

- •By End-User Segment

- ◦Original Equipment Manufacturers (OEMs)

- ◦Aftermarket Suppliers

- ◦Fleet Operators

- ◦Independent Truck Owners

- •By Distribution Channel

- ◦Direct Sales

- ◦Dealerships and Distributors

- ◦Online Retail Platforms

Growth Drivers

- •Rising demand for fuel-efficient and lightweight heavy-duty trucks in the EMEA region drives adoption of forged wheels made from aluminum and composite materials. These wheels reduce overall vehicle weight, leading to lower fuel consumption and emissions, aligning with regional regulatory mandates targeting environmental sustainability.

- •Expansion of infrastructure and industrial sectors across Europe and emerging Middle Eastern markets boosts demand for durable forged wheels suited for construction, mining, and agricultural trucks, increasing market volume and encouraging technological innovation.

- •Stringent safety regulations across EMEA enforce high standards for wheel strength and reliability, pushing manufacturers to adopt advanced forging technologies and high-quality materials, thus elevating market growth through product upgrades.

- •Growing fleet modernization and replacement cycles among logistics and transportation companies in the region stimulate aftermarket demand, with a preference for forged wheels due to their superior performance and longevity compared to cast wheels.

- •Technological advancements in forging processes including precision forming and heat treatment enhance product quality and reduce production costs, enabling manufacturers to offer competitively priced forged wheels, further driving market expansion.

Market Trends

- •Increasing integration of composite materials in forged wheels is a notable trend, leveraging their lightweight and high-strength properties to improve fuel efficiency and payload capacity in heavy-duty trucks.

- •OEMs in EMEA are increasingly collaborating with wheel manufacturers to develop customized forged wheels tailored to specific vehicle models and applications, enhancing compatibility and performance.

- •Sustainability initiatives are driving the adoption of environmentally friendly manufacturing processes, including reduced waste forging techniques and recycling of raw materials within the forged wheels production cycle.

- •Digitalization and Industry 4.0 technologies such as IoT-enabled production lines and real-time quality monitoring are being implemented to optimize forging operations and ensure consistent product standards.

- •The aftermarket segment is witnessing growth with increased consumer awareness about the benefits of forged wheels, leading to higher replacement rates and demand for premium wheel options.

Market Restraints

- •High production costs associated with advanced forging technologies and premium raw materials limit price competitiveness, especially in price-sensitive emerging markets within the EMEA region.

- •Volatility in raw material prices, particularly aluminum and magnesium, poses challenges to maintaining stable pricing and profitability for forged wheel manufacturers.

- •Long lead times and complex manufacturing processes for forged wheels can delay delivery schedules, impacting supply chain efficiency and customer satisfaction.

- •Regulatory compliance costs related to environmental standards and safety certifications increase operational expenses and may slow down new product introductions.

- •Intense competition from alternative wheel manufacturing methods such as casting and machining restricts market penetration in certain segments focused on cost reduction.

Market Opportunities

- •The growing trend of electrification in heavy-duty trucks opens opportunities for lightweight forged wheels that can help offset increased battery weight and enhance vehicle range.

- •Emerging markets in Eastern Europe and Africa present untapped potential for forged wheel adoption driven by expanding transportation infrastructure and industrialization.

- •Development of smart forged wheels with embedded sensors for real-time monitoring of wheel health and performance offers a new value proposition to fleet operators focused on predictive maintenance.

- •Strategic partnerships between forged wheel manufacturers and truck OEMs for co-development projects can accelerate innovation and market penetration.

- •Increasing demand for aftermarket customization and premium wheels provides avenues for product differentiation and enhanced brand loyalty.

Market Challenges

- •The complexity of forging processes requires highly skilled labor and advanced machinery, creating barriers to entry for new manufacturers and limiting production scalability.

- •Fragmented market with diverse regulatory requirements across EMEA countries complicates standardization and increases compliance costs for manufacturers operating regionally.

- •Supply chain disruptions caused by geopolitical tensions and raw material shortages impact timely production and delivery of forged wheels.

- •Balancing cost, performance, and durability demands continuous R&D investment, which may be a challenge for mid-sized companies competing with large multinationals.

- •Consumer hesitation in switching from traditional cast wheels to forged alternatives due to higher upfront costs restricts market growth in some segments.

Regulatory Overview

Between 2020 and 2024, EMEA regulatory bodies have tightened safety and environmental standards for heavy vehicle components, including forged wheels. The European Union’s General Safety Regulation (effective 2022) mandates enhanced durability and performance testing protocols, compelling manufacturers to adopt rigorous quality assurance processes. Additionally, emissions reduction targets under the EU Green Deal indirectly influence wheel material choices by encouraging lightweight solutions to reduce vehicle fuel consumption. Compliance with REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) regulations governs the use of certain alloys and coatings in forged wheels, ensuring environmental and human health safety. These evolving regulations necessitate continuous innovation and investment from manufacturers to maintain market access and competitiveness across the EMEA region.

Industry Insights

- •Recent developments in the EMEA Heavy Duty Trucks Forged Wheels market highlight a strong focus on material innovation and strategic collaborations. In September 2023, Maxion Wheels Germany launched a new line of composite forged wheels designed for enhanced durability and significant weight reduction, targeting the long-haul trucking sector. This product integrates advanced fiber-reinforced polymers with traditional forging methods, resulting in up to 25% weight savings compared to conventional aluminum wheels, thereby improving fuel efficiency and reducing emissions. The launch underlines the growing demand for sustainable and high-performance components within the region.

- •In March 2024, Accuride Corporation UK announced a strategic partnership with a leading Middle Eastern logistics fleet operator to supply forged aluminum wheels optimized for harsh desert conditions. The collaboration involves co-development of wheels featuring enhanced corrosion resistance and thermal stability, addressing the unique challenges of the region’s operating environment. This initiative exemplifies the market’s approach towards tailored solutions and regional customization to meet diverse customer requirements across EMEA.

Mergers & Acquisitions

- •In October 2023, Wielton SA, a major Polish forged wheels manufacturer, acquired Forged Excellence GmbH in Germany to expand its footprint in Western Europe and enhance its R&D capabilities. This acquisition enables Wielton SA to integrate advanced forging technologies and accelerate product development aimed at premium heavy-duty truck applications. The strategic move strengthens Wielton’s position in the EMEA market by combining manufacturing expertise with innovative engineering solutions, facilitating access to new customer segments and distribution networks.

- •In July 2022, Alcoa Wheels France completed the acquisition of Nordic Forged Wheels, a Swedish company specializing in lightweight forged wheels for agricultural and mining vehicles. This deal expands Alcoa’s product portfolio and regional presence in Northern Europe, supporting its growth strategy focused on sustainable and high-performance wheel solutions. The acquisition also brings enhanced manufacturing efficiencies and innovation synergies, positioning Alcoa to better serve the evolving needs of the EMEA heavy vehicle market.

Recent Industry News

- •15th April 2024, Steelwheels Europe GmbH announced the launch of a new titanium forged wheel series designed for extreme durability and reduced weight, targeting the mining truck segment in EMEA. The wheels incorporate cutting-edge forging techniques and a proprietary alloy composition, enhancing load capacity by 20% while reducing overall wheel weight by 30%. This launch strengthens Steelwheels’ position in premium market segments. Source: Steelwheels Europe Official Press Release

- •10th November 2023, Ronak Industries Pvt. Ltd. (UAE) expanded its manufacturing facility to increase production capacity for magnesium forged wheels used in construction vehicles. The expansion includes investment in automated forging lines and quality control labs to meet growing demand across Middle Eastern markets. This move supports Ronak’s regional growth strategy and commitment to innovation. Source: Ronak Industries Corporate Announcement

- •8th August 2022, BBS Kraftfahrzeugtechnik AG (Germany) partnered with a leading European long-haul truck OEM to co-develop forged aluminum wheels featuring integrated smart sensors for real-time monitoring of wheel integrity and performance. The collaboration aims to enhance safety and predictive maintenance capabilities, marking a significant technological advancement in the market. Source: BBS AG Industry News

- •22nd May 2021, Maxion Wheels Germany inaugurated a state-of-the-art R&D center focused on lightweight forged wheels, incorporating simulation-driven design and advanced materials testing. The facility supports accelerated innovation cycles and product customization for diverse EMEA applications. Source: Maxion Wheels Press Release

Market Statistics

- •CAGR by 2034: 10.3%

- •Market Size by 2034: USD 2.8 Billion

- •Market Size in 2025: USD 1.2 Billion

- •Dominating Type: Aluminum Forged Wheels

- •Next-Following Type: Steel Forged Wheels

- •Dominating Application: Long-Haul Trucks

- •Next-Following Application: Construction Vehicles

- •Dominating Region: Germany

- •Second-Leading Region: France

- •Region with Highest Growth Rate: Poland

- •Dominating Country: Germany

Market Share Table

- •Market Share (%) of Dominating vs Followed Type

- ◦Aluminum Forged Wheels: 45%

- ◦Steel Forged Wheels: 30%

- •Market Share (%) of Dominating vs Followed Application

- ◦Long-Haul Trucks: 40%

- ◦Construction Vehicles: 25%

- •Growth Rate (%) of Dominating vs Followed Type

- ◦Aluminum Forged Wheels: 11.5%

- ◦Steel Forged Wheels: 8.7%

- •Growth Rate (%) of Dominating vs Followed Application

- ◦Long-Haul Trucks: 10.8%

- ◦Construction Vehicles: 9.2%

Top 5 Global Players

- •Accuride Corporation (United Kingdom)

- •Maxion Wheels (Germany)

- •Wielton SA (Poland)

- •BBS Kraftfahrzeugtechnik AG (Germany)

- •Ronak Industries Pvt. Ltd. (United Arab Emirates)

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Poland is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.1 Billion |

| Forecast Year Market Size | USD 2.8 Billion |

| CAGR | 10.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.8% |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | Accuride Corporation (United Kingdom), Maxion Wheels (Germany), Wielton SA (Poland), BBS Kraftfahrzeugtechnik AG (Germany), Ronak Industries Pvt. Ltd. (United Arab Emirates), Alcoa Wheels (France), ZF Friedrichshafen AG (Germany), Steelwheels Europe GmbH (Germany), Fast Wheels Ltd. (United Kingdom), Magna Forged Wheels (Italy), Titanium Wheels Solutions (South Africa), Forged Excellence GmbH (Germany), Euro Forged Wheels (France), Kapsen Wheels (Poland), Duraforge Technologies (United Kingdom), Middle East Wheel Works (United Arab Emirates), Vulcan Wheels (Germany), HeavyDuty Forged Wheels Ltd. (Italy), Nordic Forged Wheels (Sweden), Atlas Forged Wheels (France) |

EMEA Heavy Duty Trucks Forged Wheels Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.