North America Cloud Infrastructure In Chemical Market Size, Growth & Revenue 2024-2034

North America Cloud Infrastructure In Chemical Market is segmented by Application (Process Optimization, Supply Chain Management, Quality Control, Research & Development, Regulatory Compliance), Type (Public Cloud, Private Cloud, Hybrid Cloud, Community Cloud, Multi-Cloud), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

- •The North America Cloud Infrastructure in Chemical market focuses on cloud solutions designed to meet the specific needs of the chemical industry, including data management, process optimization, and regulatory compliance across the United States, Canada, and Mexico.

- •Key market highlights include a robust CAGR of 13.4% forecasted from 2024 to 2034, driven by increasing digital transformation initiatives and demand for scalable cloud platforms to accelerate innovation and operational efficiency.

- •The market's value proposition lies in enabling chemical companies to leverage cloud infrastructure for cost-effective, secure, and flexible operations, facilitating enhanced collaboration, faster R&D cycles, and improved supply chain transparency.

Competitive Landscape

The North America Cloud Infrastructure in Chemical market is characterized by intense competition among global cloud service providers and specialized technology firms. Market players focus heavily on innovation, strategic partnerships, and customized solutions for chemical industry applications. Competitive strategies include technological advancements in hybrid and multi-cloud environments, aggressive pricing models, and expansion of data center capabilities to meet stringent security and compliance requirements. The rivalry fosters continuous product differentiation, with companies investing in AI-driven analytics and IoT integration to enhance cloud offerings. Market positioning hinges on the ability to offer scalable, reliable, and secure cloud platforms tailored to chemical industry needs, alongside extensive customer support and regional presence. As the market evolves, emerging players leverage niche expertise, while incumbents consolidate through mergers and acquisitions to strengthen market share and broaden service portfolios. Regional competition is also influenced by regulatory compliance and local data sovereignty demands, which shape the competitive dynamics and client preferences.

Leading Companies in North America Cloud Infrastructure In Chemical Market

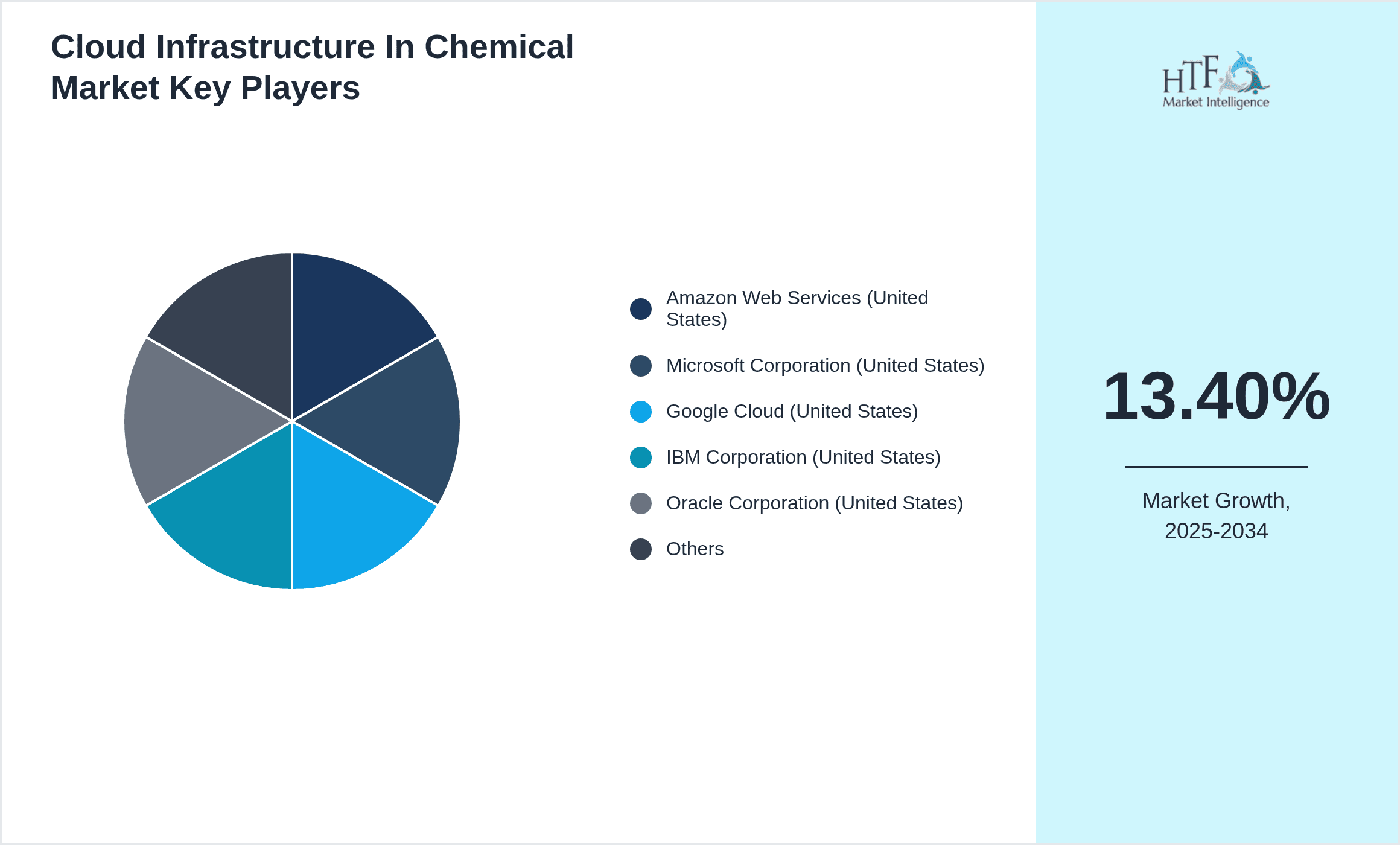

- •Amazon Web Services (United States)

- •Microsoft Corporation (United States)

- •Google Cloud (United States)

- •IBM Corporation (United States)

- •Oracle Corporation (United States)

- •Salesforce Inc. (United States)

- •Dell Technologies (United States)

- •Cisco Systems, Inc. (United States)

- •VMware, Inc. (United States)

- •Hewlett Packard Enterprise (United States)

- •Rackspace Technology (United States)

- •ServiceNow, Inc. (United States)

- •Snowflake Inc. (United States)

- •Citrix Systems, Inc. (United States)

- •C3.ai, Inc. (United States)

- •Red Hat, Inc. (United States)

- •SAS Institute Inc. (United States)

- •OpenText Corporation (Canada)

- •Mitel Networks Corporation (Canada)

- •Teradata Corporation (United States)

Market Breakdown

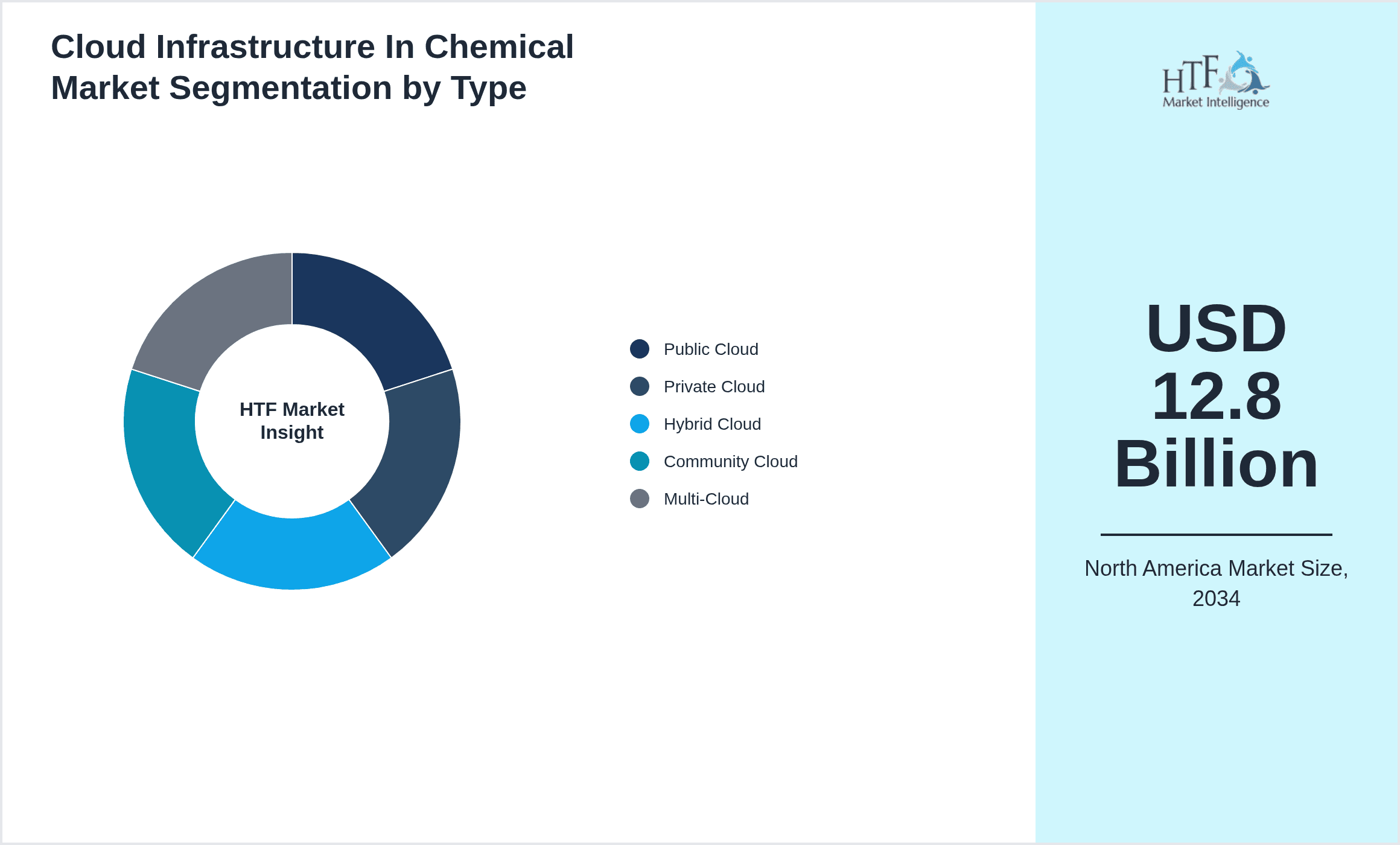

- •By Type

- ◦Public Cloud

- ◦Private Cloud

- ◦Hybrid Cloud

- ◦Community Cloud

- ◦Multi-Cloud

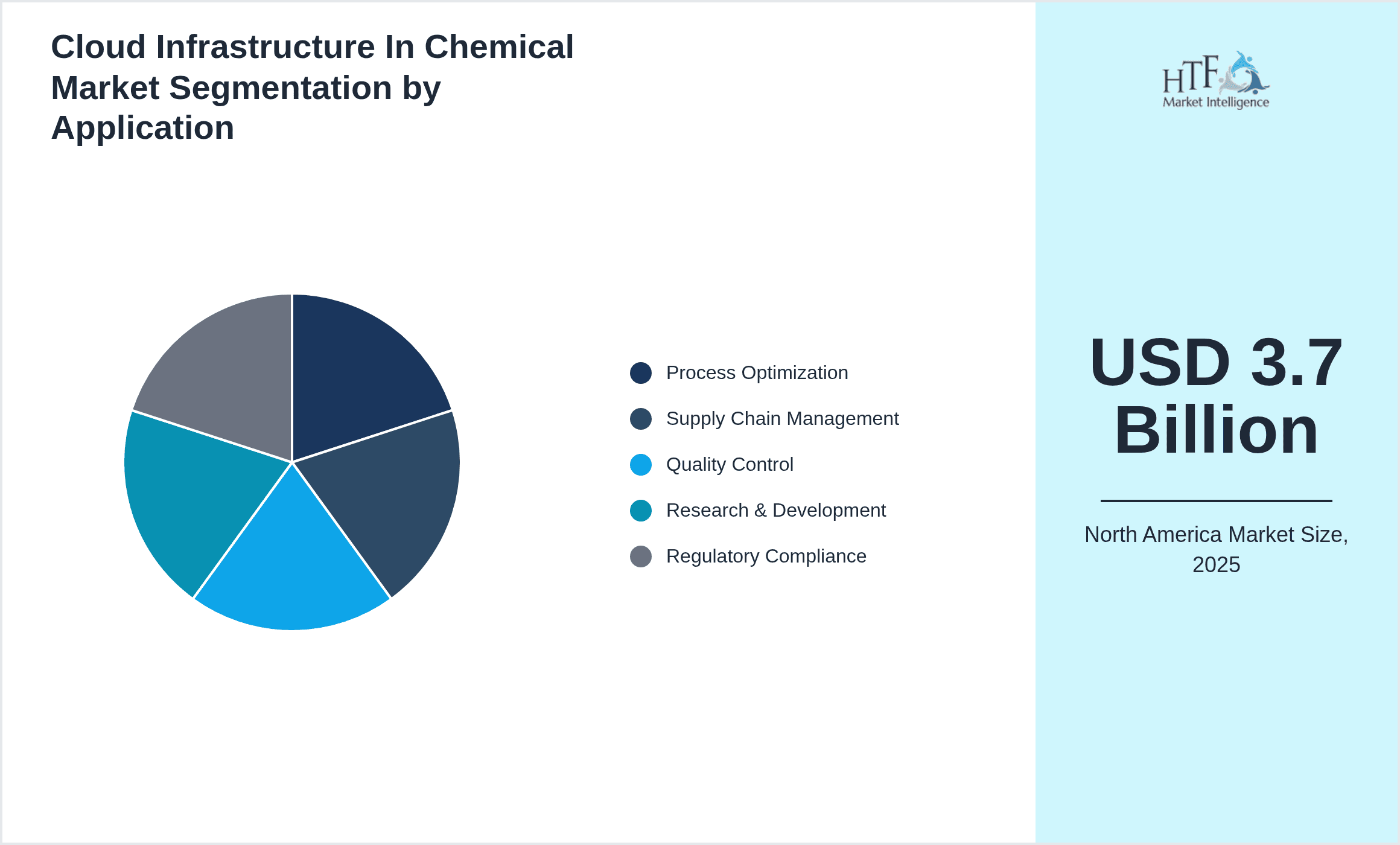

- •By Application

- ◦Process Optimization

- ◦Supply Chain Management

- ◦Quality Control

- ◦Research & Development

- ◦Regulatory Compliance

- •By Deployment Model

- ◦On-Premise Integration

- ◦Cloud-Native Solutions

- ◦Edge Computing

- •By End User

- ◦Chemical Manufacturing

- ◦Pharmaceuticals

- ◦Petrochemicals

- ◦Agrochemicals

- ◦Specialty Chemicals

Growth Drivers

- •The North America Cloud Infrastructure in Chemical market growth is propelled by the increasing adoption of digital transformation strategies among chemical companies seeking enhanced operational efficiency and agility. Cloud platforms enable real-time data analytics, facilitating smarter decision-making and process optimization that reduce downtime and improve yield.

- •Rising regulatory compliance demands in the chemical sector require robust data management and reporting capabilities, driving demand for secure and scalable cloud infrastructure to maintain audit trails and ensure transparency across operations.

- •The growing need for collaboration across geographically dispersed teams and supply chains encourages cloud adoption, as it provides seamless connectivity and data sharing capabilities critical to innovation and rapid product development cycles.

- •Advancements in hybrid cloud technologies allow chemical firms to balance security and flexibility, integrating on-premise systems with cloud services to meet complex IT requirements and safeguard sensitive intellectual property.

- •Increasing investments by cloud providers in data center infrastructure across North America enhance service reliability and reduce latency, further accelerating market adoption among chemical industry stakeholders.

Market Trends

- •A significant trend in the market is the integration of artificial intelligence and machine learning within cloud infrastructure, enabling predictive analytics and automation that improve chemical process efficiencies and product quality.

- •There is a marked shift toward multi-cloud and hybrid cloud deployments, as chemical companies seek to avoid vendor lock-in and optimize workloads between public and private environments for cost and performance benefits.

- •Sustainability initiatives are driving cloud adoption as organizations leverage cloud platforms to monitor environmental impact, manage energy consumption, and comply with evolving green regulations in the chemical industry.

- •Increased focus on cybersecurity within cloud environments is shaping market offerings, with providers enhancing encryption, identity management, and threat detection tailored to chemical sector vulnerabilities.

- •The emergence of edge computing integrated with cloud infrastructure is gaining traction, allowing real-time data processing closer to chemical manufacturing sites, minimizing latency, and supporting critical operational decisions.

Market Opportunities

- •Expanding cloud adoption in mid-sized and small chemical enterprises represents a significant growth opportunity, as these organizations seek cost-effective, scalable infrastructure solutions to enhance competitiveness and innovate.

- •The convergence of IoT with cloud infrastructure opens avenues for real-time monitoring and automation in chemical manufacturing, improving safety, process control, and predictive maintenance capabilities.

- •Emerging regulatory frameworks emphasizing data transparency and traceability create demand for advanced cloud-based compliance and reporting solutions tailored to the chemical industry’s unique challenges.

- •Strategic partnerships between cloud providers and chemical technology firms offer opportunities to co-develop specialized applications, driving deeper market penetration and customer loyalty.

- •Geographic expansion into underserved markets within North America, such as Mexico, provides growth potential by offering localized cloud infrastructure services adapted to regional industry needs.

Market Challenges

- •Data security and privacy concerns remain significant barriers, as chemical companies handle sensitive proprietary information requiring stringent protection against cyber threats within cloud environments.

- •High initial integration costs and complexity of migrating legacy chemical manufacturing systems to cloud platforms deter some firms, especially those with limited IT resources or expertise.

- •Regulatory and compliance variability across North America creates challenges for cloud providers to offer uniformly compliant solutions, complicating deployment and governance for multinational chemical companies.

- •Resistance to change within traditional chemical industry segments slows cloud adoption, as stakeholders weigh operational risks and cultural shifts associated with digital transformation.

- •Dependence on reliable high-speed internet infrastructure is critical; regions with limited connectivity face delays in cloud implementation, affecting scalability and performance of chemical operations.

Regulatory Framework

- •Between 2020 and 2024, data privacy regulations such as the California Consumer Privacy Act (CCPA) have mandated stricter controls on cloud data management, impacting chemical companies’ cloud infrastructure strategies in the U.S.

- •The Chemical Facility Anti-Terrorism Standards (CFATS) require enhanced cybersecurity measures for chemical manufacturing facilities, prompting cloud providers to develop compliant security frameworks.

- •Environmental regulations like the U.S. EPA’s Toxic Substances Control Act (TSCA) necessitate accurate data reporting and monitoring, increasing reliance on cloud platforms for compliance and audit readiness.

- •Canada’s Personal Information Protection and Electronic Documents Act (PIPEDA) enforces data handling and storage standards that cloud infrastructure services must comply with when servicing Canadian chemical companies.

- •Industry-specific standards such as ISO 27001 adoption have become critical for cloud providers serving the chemical sector to ensure information security management and build customer trust.

Industry Insights

- •In March 2023, Amazon Web Services launched a specialized cloud solution tailored for chemical manufacturers, integrating AI-powered analytics and compliance management tools designed to accelerate digital transformation and operational efficiency in the sector. This launch underscores growing emphasis on industry-specific cloud capabilities to meet complex regulatory and process requirements in North America.

- •In November 2022, Microsoft Corporation expanded its Azure cloud platform with enhanced hybrid cloud features targeting chemical companies, enabling seamless integration of on-premise infrastructure with cloud environments. This strategic move enables chemical firms to balance data security concerns with the benefits of scalable computing, driving market growth and innovation.

Mergers & Acquisitions

- •In August 2023, IBM Corporation completed the acquisition of a cloud-based chemical data analytics startup, enhancing its portfolio with advanced AI-driven solutions tailored for chemical process optimization. This strategic acquisition strengthens IBM’s position in the North America chemical cloud infrastructure market by accelerating innovation and expanding specialized service offerings.

- •In January 2024, Oracle Corporation acquired a leading hybrid cloud services provider focused on the chemical industry, expanding its capabilities in secure, scalable cloud deployment models. This move enables Oracle to cater more effectively to chemical companies requiring flexible infrastructure solutions that comply with stringent regulatory requirements.

Recent Industry News

- •15th February 2024, Salesforce Inc. announced a partnership with a major chemical manufacturer to deploy cloud-based customer relationship management and supply chain solutions, enhancing operational transparency and customer engagement through integrated cloud infrastructure. Source: Salesforce Official Press Release

- •10th October 2023, Google Cloud unveiled its new AI-powered quality control platform for chemical companies, enabling real-time defect detection and process optimization via cloud analytics, marking a significant technological advancement in the market. Source: Google Cloud Newsroom

- •5th July 2022, Dell Technologies expanded its cloud data center footprint in North America with new facilities designed to support chemical industry clients requiring high availability and compliance-focused infrastructure. Source: Dell Technologies Press Release

- •20th May 2021, Cisco Systems, Inc. launched enhanced cybersecurity solutions for cloud infrastructure tailored to chemical manufacturers, addressing increasing cyber threats and regulatory compliance challenges in the sector. Source: Cisco Official Blog

Market Statistics

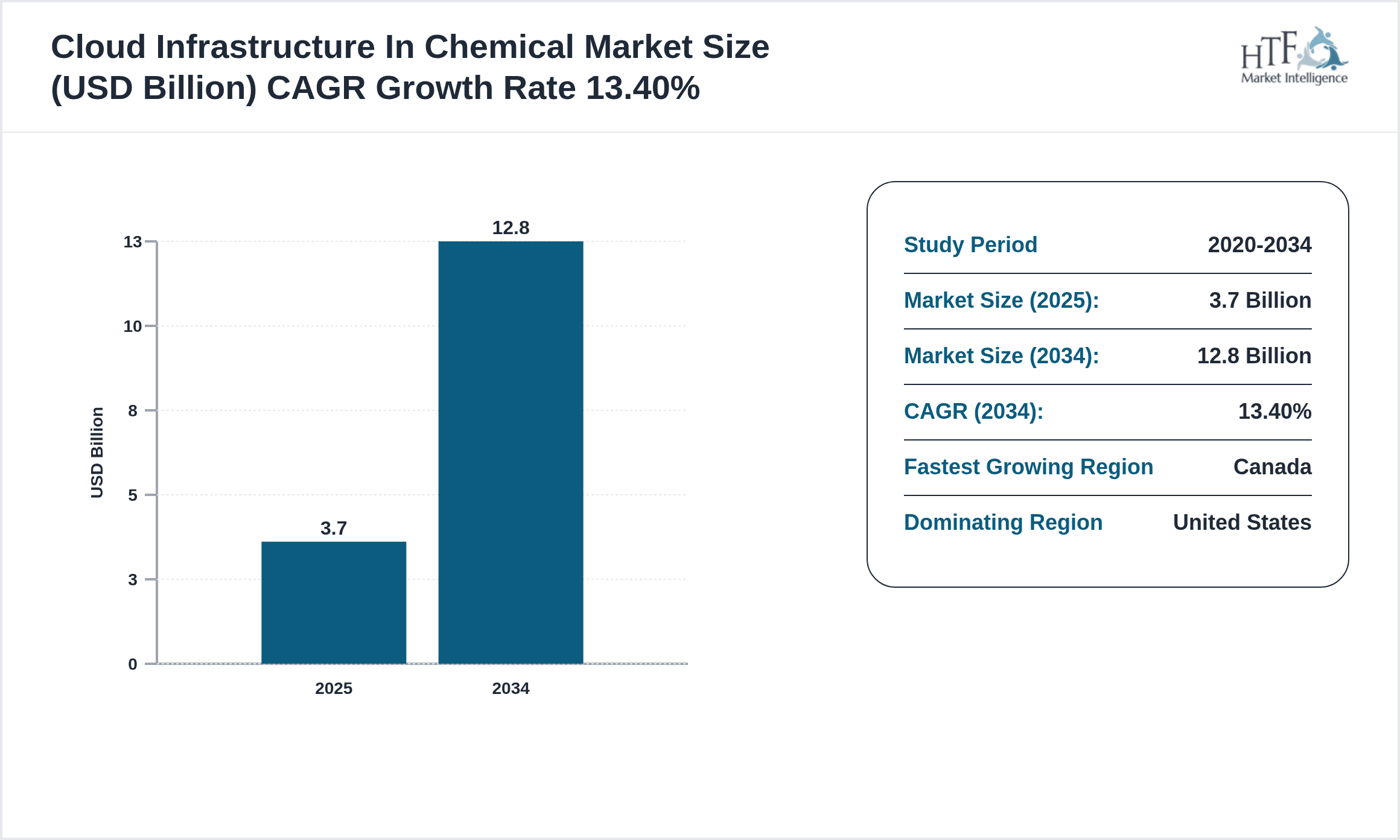

- •CAGR by 2034: 13.4%

- •Market Size by 2034: USD 12.8 Billion

- •Market Size in 2025: USD 4.2 Billion

- •Dominating Type: Public Cloud

- •Next-Following Type: Hybrid Cloud

- •Dominating Application: Process Optimization

- •Next-Following Application: Supply Chain Management

- •Dominating Region: United States

- •Second-Leading Region: Canada

- •Region with Highest Growth Rate: Canada

- •Dominating Country: United States

Market Share Table

- •Market Share of Dominating vs Followed Type (%)

- ◦Public Cloud: 54%

- ◦Hybrid Cloud: 28%

- •Market Share of Dominating vs Followed Application (%)

- ◦Process Optimization: 42%

- ◦Supply Chain Management: 35%

- •Growth Rate (%) of Dominating vs Followed Type

- ◦Public Cloud: 12.5%

- ◦Hybrid Cloud: 15.8%

- •Growth Rate (%) of Dominating vs Followed Application

- ◦Process Optimization: 13.0%

- ◦Supply Chain Management: 14.2%

Top 5 Global Players

- •Amazon Web Services (United States)

- •Microsoft Corporation (United States)

- •Google Cloud (United States)

- •IBM Corporation (United States)

- •Oracle Corporation (United States)

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.7 Billion |

| Forecast Year Market Size | USD 12.8 Billion |

| CAGR | 13.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 13.4% |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Amazon Web Services (United States), Microsoft Corporation (United States), Google Cloud (United States), IBM Corporation (United States), Oracle Corporation (United States), Salesforce Inc. (United States), Dell Technologies (United States), Cisco Systems, Inc. (United States), VMware, Inc. (United States), Hewlett Packard Enterprise (United States), Rackspace Technology (United States), ServiceNow, Inc. (United States), Snowflake Inc. (United States), Citrix Systems, Inc. (United States), C3.ai, Inc. (United States), Red Hat, Inc. (United States), SAS Institute Inc. (United States), OpenText Corporation (Canada), Mitel Networks Corporation (Canada), Teradata Corporation (United States) |

North America Cloud Infrastructure In Chemical Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.