Global Hybrid Cloud Management Software Market Size, Growth & Revenue 2025-2034

Global Hybrid Cloud Management Software Market is segmented by Type (Cloud Orchestration Software, Workload Automation Software, Security Management Software, Cost Management Software, Compliance Management Software), Application (Enterprise IT, Cloud Service Providers, Government, Healthcare, Banking, Financial Services, and Insurance (BFSI)), Deployment Model (On-Premises, Cloud-Based, Hybrid), Organization Size (Small and Medium Enterprises (SMEs), Large Enterprises), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •Global Hybrid Cloud Management Software market includes software solutions that manage and orchestrate workloads across private, public, and on-premises clouds to optimize hybrid cloud environments for enterprises worldwide.

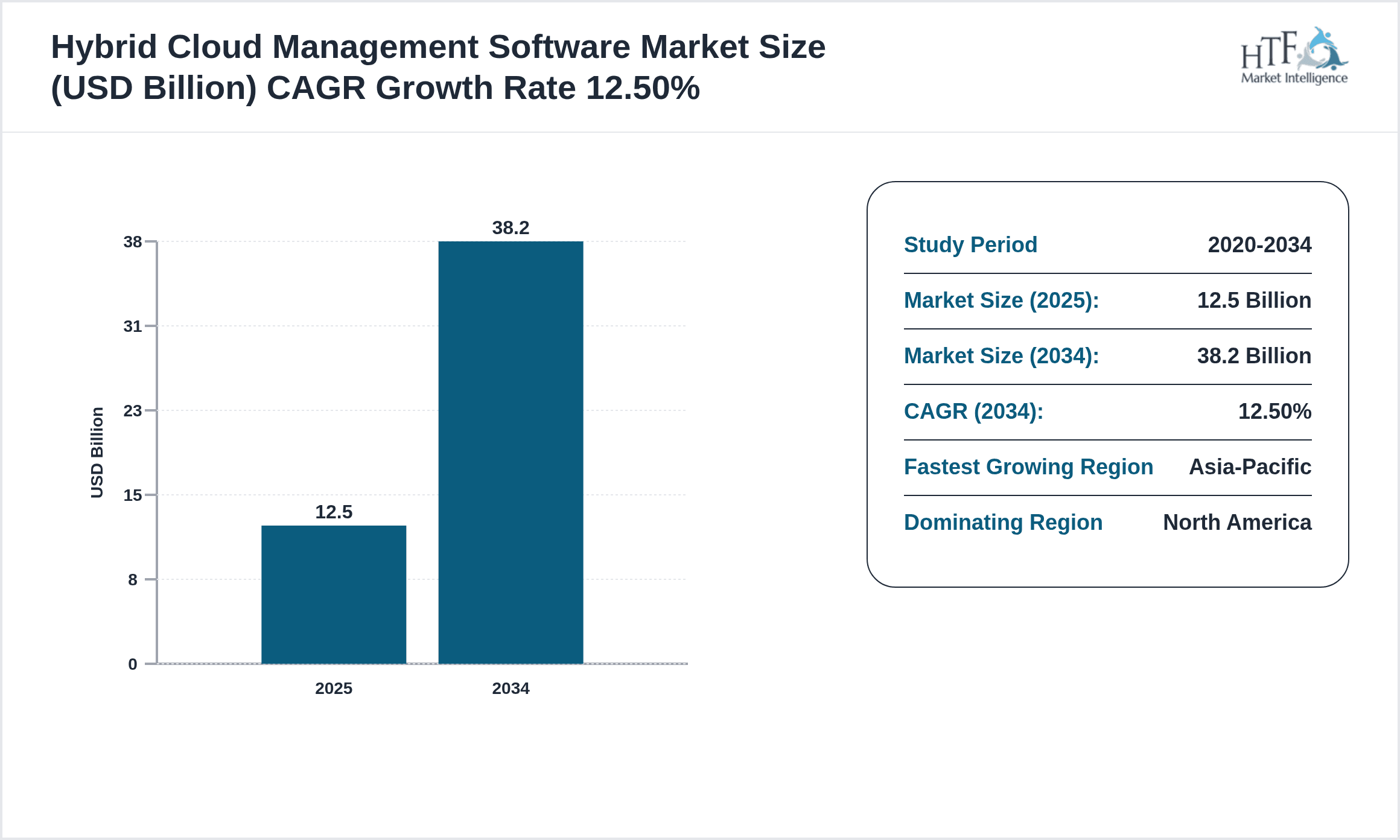

- •Key highlights include a base market size of USD 12.5 Billion in 2025, projected to reach USD 38.2 Billion by 2034, driven by rapid cloud adoption and multi-cloud strategies across industries.

- •The market offers strategic value by enabling operational efficiency, security, and cost control, thereby supporting digital transformation initiatives across sectors like enterprise IT, healthcare, BFSI, and government.

Competitive Landscape

Companies in the Global Hybrid Cloud Management Software market sustain and enhance their presence through strategic partnerships with cloud providers, continuous product innovation, and adoption of AI and automation technologies. Expansion into emerging markets and increased focus on cybersecurity integration remain key to competitive advantage. Firms leverage multi-cloud compatibility and flexible deployment models to address diverse customer needs. Innovation in cost management and compliance monitoring software differentiates offerings. Collaborations with major cloud platforms and acquisitions strengthen portfolios, while investments in R&D drive next-generation hybrid cloud solutions. Pricing strategies and scalable subscription models enable penetration across enterprise sizes. Regional market adaptations and ecosystem collaborations create resilient competitive positioning. Future trends emphasize AI-driven workload automation and enhanced security frameworks to meet evolving enterprise demands.

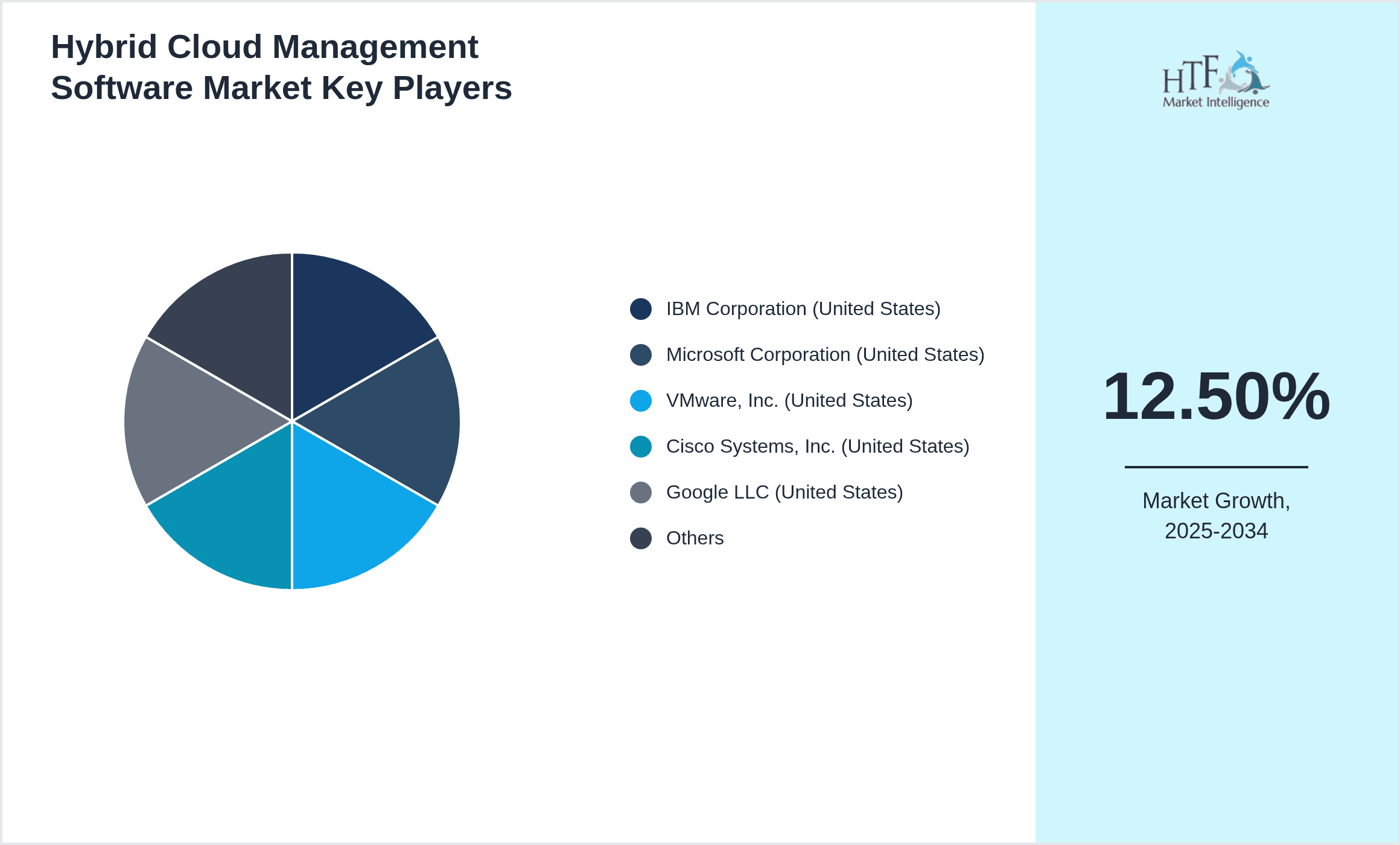

Leading Companies in Hybrid Cloud Management Software Market

- •IBM Corporation (United States)

- •Microsoft Corporation (United States)

- •VMware, Inc. (United States)

- •Cisco Systems, Inc. (United States)

- •Google LLC (United States)

- •Red Hat, Inc. (United States)

- •Oracle Corporation (United States)

- •BMC Software, Inc. (United States)

- •ServiceNow, Inc. (United States)

- •Hewlett Packard Enterprise (United States)

- •Dell Technologies Inc. (United States)

- •Citrix Systems, Inc. (United States)

- •Broadcom Inc. (United States)

- •Cisco Systems, Inc. (United States)

- •Snow Software AB (Sweden)

- •Micro Focus International plc (United Kingdom)

- •Morpheus Data, Inc. (United States)

- •CloudHealth Technologies, Inc. (United States)

- •Flexera Software LLC (United States)

- •Turbonomic, Inc. (United States)

Market Breakdown

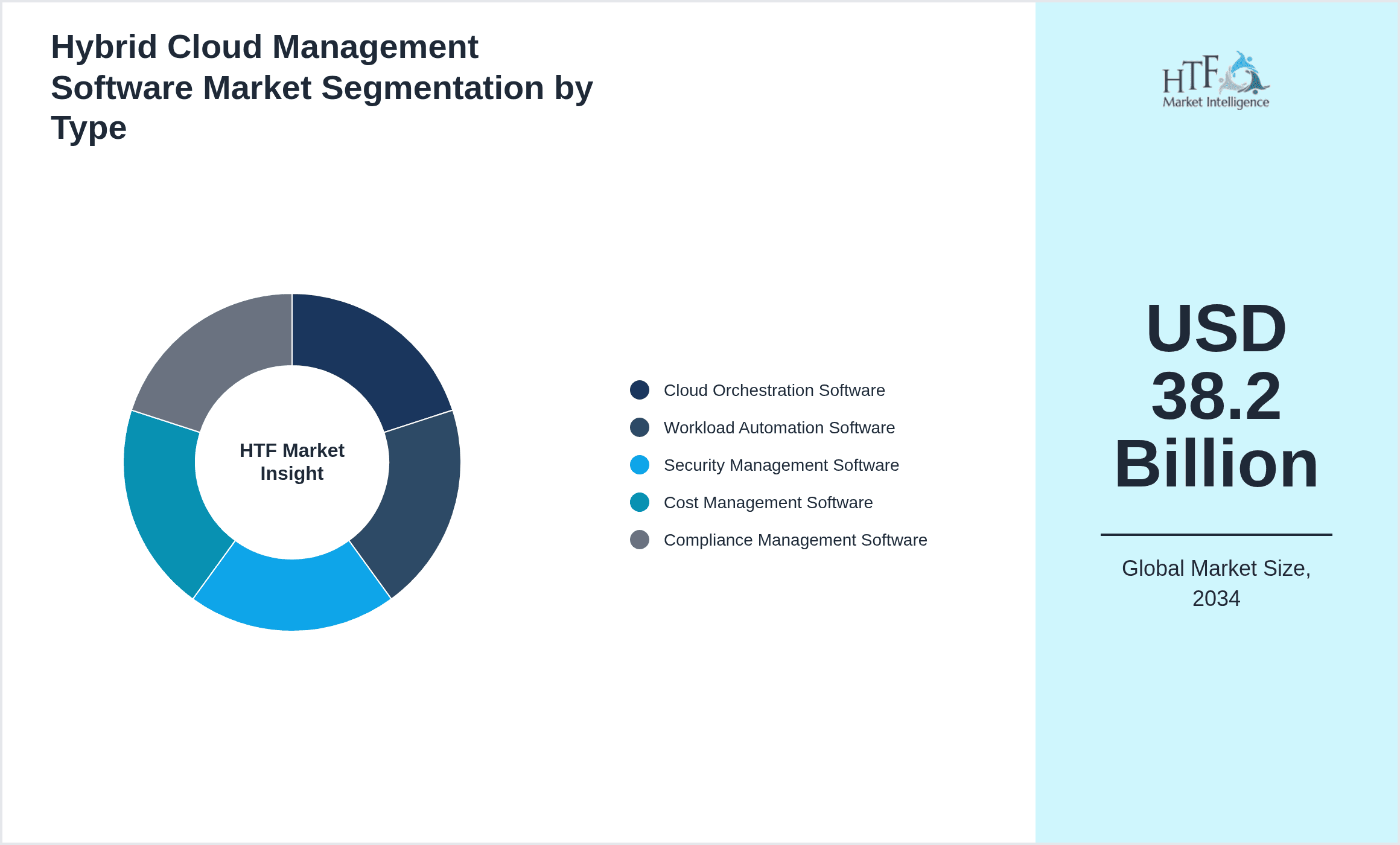

- •By Type

- ◦Cloud Orchestration Software

- ◦Workload Automation Software

- ◦Security Management Software

- ◦Cost Management Software

- ◦Compliance Management Software

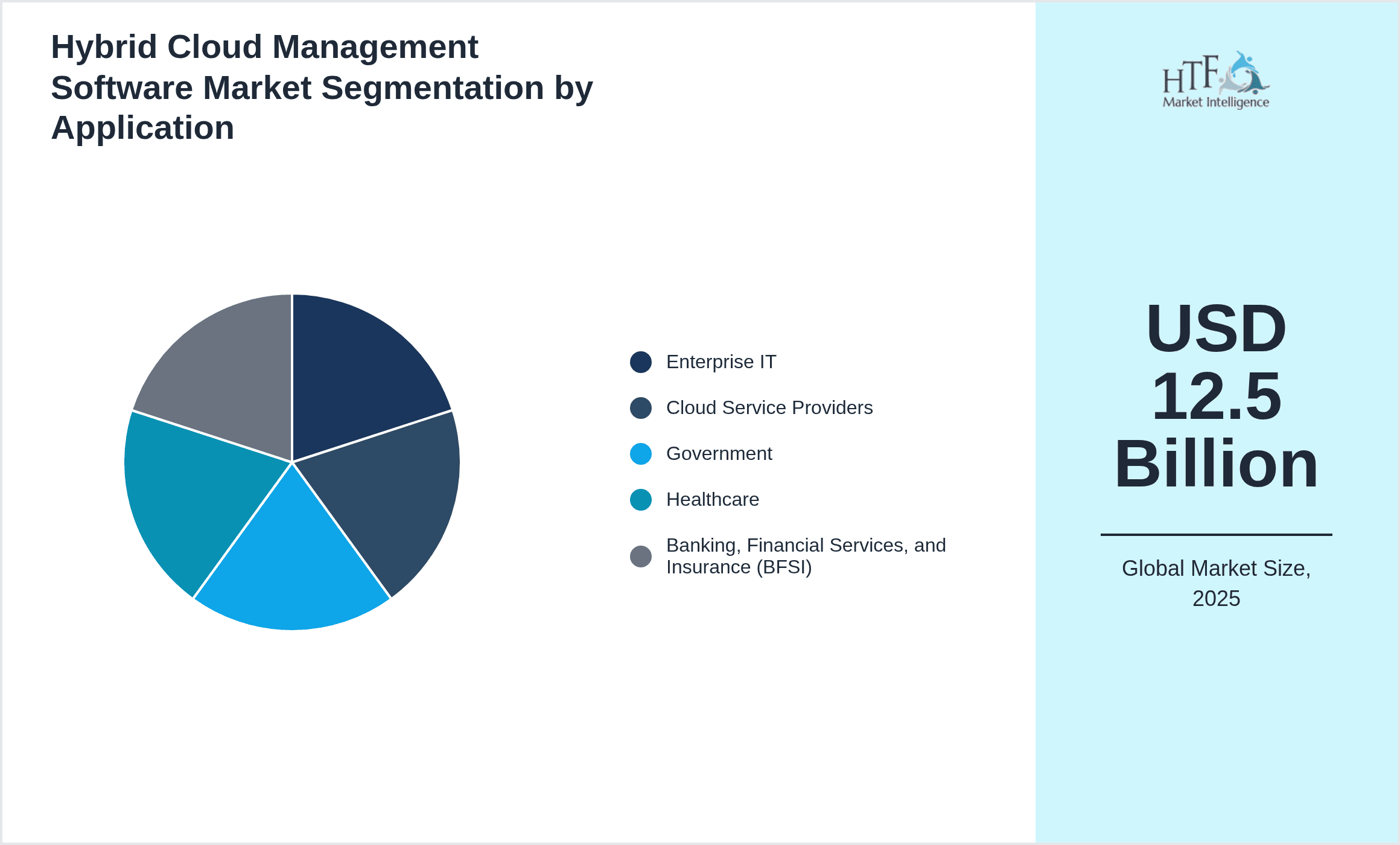

- •By Application

- ◦Enterprise IT

- ◦Cloud Service Providers

- ◦Government

- ◦Healthcare

- ◦Banking, Financial Services, and Insurance (BFSI)

- •By Deployment Model

- ◦On-Premises

- ◦Cloud-Based

- ◦Hybrid

- •By Organization Size

- ◦Small and Medium Enterprises (SMEs)

- ◦Large Enterprises

Market Drivers

Rapid global adoption of multi-cloud strategies across enterprises fuels demand for hybrid cloud management software solutions. Organizations increasingly seek integrated platforms that enable seamless workload orchestration between private and public clouds to optimize resource utilization and reduce operational complexity. Increasing cybersecurity threats necessitate advanced security management features, driving investment in software that provides centralized governance and compliance. For instance, IBM’s recent launch of hybrid cloud security integrations in 2024 highlights the trend toward securing multi-cloud environments comprehensively. Additionally, cost optimization pressures encourage adoption of cost management modules that deliver real-time cloud expenditure visibility and forecasting. The surge in remote work and digital transformation initiatives accelerated by pandemic recovery further underline the need for scalable, flexible hybrid cloud management tools. Market players continuously enhance AI-driven automation capabilities to improve workload management efficiency, exemplified by VMware’s AI-enhanced orchestration platform introduced in early 2025. These factors collectively accelerate market expansion, driven by enterprises’ pursuit of agility, security, and cost-effectiveness in their hybrid cloud deployments.

Market Trends

The Global Hybrid Cloud Management Software market exhibits trends toward greater integration of artificial intelligence and machine learning to automate workload distribution and anomaly detection. Companies emphasize developing unified dashboards that provide visibility across multi-cloud environments to simplify management and enhance decision-making. The rise of edge computing demands hybrid cloud solutions capable of orchestrating workloads closer to data sources, as demonstrated by Cisco’s edge cloud management initiatives launched in 2025. Sustainability considerations prompt software providers to integrate energy-efficient resource allocation features. Increasing partnerships between software vendors and hyperscale cloud providers strengthen ecosystem interoperability and accelerate hybrid cloud adoption. The trend of containerization and microservices architecture drives demand for hybrid cloud management solutions supporting Kubernetes and similar orchestration frameworks. Furthermore, subscription-based pricing models gain traction, improving affordability and scalability for diverse enterprise sizes. These developments position the market for sustained growth, driven by innovation aligned with evolving cloud infrastructure paradigms and enterprise IT modernization efforts worldwide.

Market Opportunities

Expanding adoption of hybrid cloud strategies in emerging regions such as Asia-Pacific presents significant growth opportunities for hybrid cloud management software vendors. Enterprises in these regions increasingly prioritize digital transformation, creating demand for scalable, secure cloud orchestration and cost control solutions. Integration of AI-driven analytics and automation capabilities enables differentiation and enhanced value propositions, encouraging investment in research and development. Cloud service providers expanding their offerings through partnerships with software vendors open avenues for co-marketing and bundled solutions. Increasing regulatory requirements for data sovereignty and privacy create opportunities for compliance management software tailored to regional mandates. The rise of Internet of Things and edge computing applications necessitates hybrid cloud solutions capable of distributed workload orchestration, representing an untapped market segment. Vendors focusing on SMEs benefit from growing cloud adoption among smaller enterprises seeking flexible, cost-effective hybrid cloud management tools. These opportunities, combined with advancements in security management and cost optimization, position the market for robust expansion and innovation over the forecast period.

Market Challenges

Complexity in integrating disparate cloud environments remains a significant challenge for hybrid cloud management software providers. Diverse architectures, varying APIs, and inconsistent security protocols across public and private clouds complicate unified management efforts. Enterprises face difficulties in achieving seamless interoperability, leading to increased deployment times and higher costs. Data privacy and compliance requirements vary globally, creating regulatory hurdles and necessitating adaptable software solutions, which increases development complexity. High initial implementation costs and skill shortages in hybrid cloud technologies hinder adoption, particularly among SMEs. Recent cybersecurity incidents targeting cloud infrastructures underscore the challenge of maintaining robust security across hybrid environments, requiring continuous software updates and monitoring. For example, some companies experienced delays integrating hybrid management platforms due to compatibility issues reported in 2024. Market players must address these technical and operational barriers through standardized frameworks and enhanced support services to ensure broader market penetration and customer satisfaction.

Regulatory Framework

In the last five years, global regulatory environments have increasingly emphasized data protection and cloud security compliance impacting hybrid cloud management software providers. Regulations such as the European Union's GDPR updates and the US Cybersecurity Maturity Model Certification (CMMC) mandate stringent controls on data handling and cloud infrastructure security. These regulations require software solutions to incorporate advanced encryption, audit trails, and compliance reporting features. Additionally, countries have introduced data localization laws compelling hybrid cloud platforms to support region-specific data residency requirements. Compliance frameworks also address cloud service provider certifications and operational transparency. These evolving regulations necessitate continuous adaptation of hybrid cloud management software to meet legal standards, increasing demand for integrated compliance management modules. Providers that proactively align their products with regulatory mandates gain competitive advantages by reducing clients’ compliance risks and facilitating secure hybrid cloud adoption globally.

Market Intelligence

Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.5 Billion |

| Forecast Year Market Size | USD 38.2 Billion |

| CAGR | 12.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.3% |

| Scope of Report | Market is segmented by Type (Cloud Orchestration Software, Workload Automation Software, Security Management Software, Cost Management Software, Compliance Management Software), Application (Enterprise IT, Cloud Service Providers, Government, Healthcare, Banking, Financial Services, and Insurance (BFSI)), Deployment Model (On-Premises, Cloud-Based, Hybrid), Organization Size (Small and Medium Enterprises (SMEs), Large Enterprises) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | IBM Corporation (United States), Microsoft Corporation (United States), VMware, Inc. (United States), Cisco Systems, Inc. (United States), Google LLC (United States), Red Hat, Inc. (United States), Oracle Corporation (United States), BMC Software, Inc. (United States), ServiceNow, Inc. (United States), Hewlett Packard Enterprise (United States), Dell Technologies Inc. (United States), Citrix Systems, Inc. (United States), Broadcom Inc. (United States), Cisco Systems, Inc. (United States), Snow Software AB (Sweden), Micro Focus International plc (United Kingdom), Morpheus Data, Inc. (United States), CloudHealth Technologies, Inc. (United States), Flexera Software LLC (United States), Turbonomic, Inc. (United States) |

Global Hybrid Cloud Management Software Market Size, Growth & Revenue 2025-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.