North America Vehicle Entrance Control Systems Market Size, Growth & Revenue 2024-2034

North America Vehicle Entrance Control Systems Market is segmented by Type (Barrier Gates, Bollards, Turnstiles, Automatic Doors, Access Control Systems), Application (Commercial Facilities, Residential Complexes, Industrial Sites, Parking Lots, Government Buildings), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

- •The North America Vehicle Entrance Control Systems market covers a range of products and technologies aimed at controlling vehicle access to properties. This includes physical barriers like gates and bollards, as well as electronic access control systems integrating modern tech like RFID and biometrics. The market's boundaries stretch across commercial, residential, industrial, and governmental applications, each with distinct needs and adoption challenges. While security enhancement is a core purpose, traffic management and authorized access enforcement are equally vital. The industry scope encompasses product manufacturing, system integration, installation, and maintenance services, reflecting a multifaceted ecosystem.

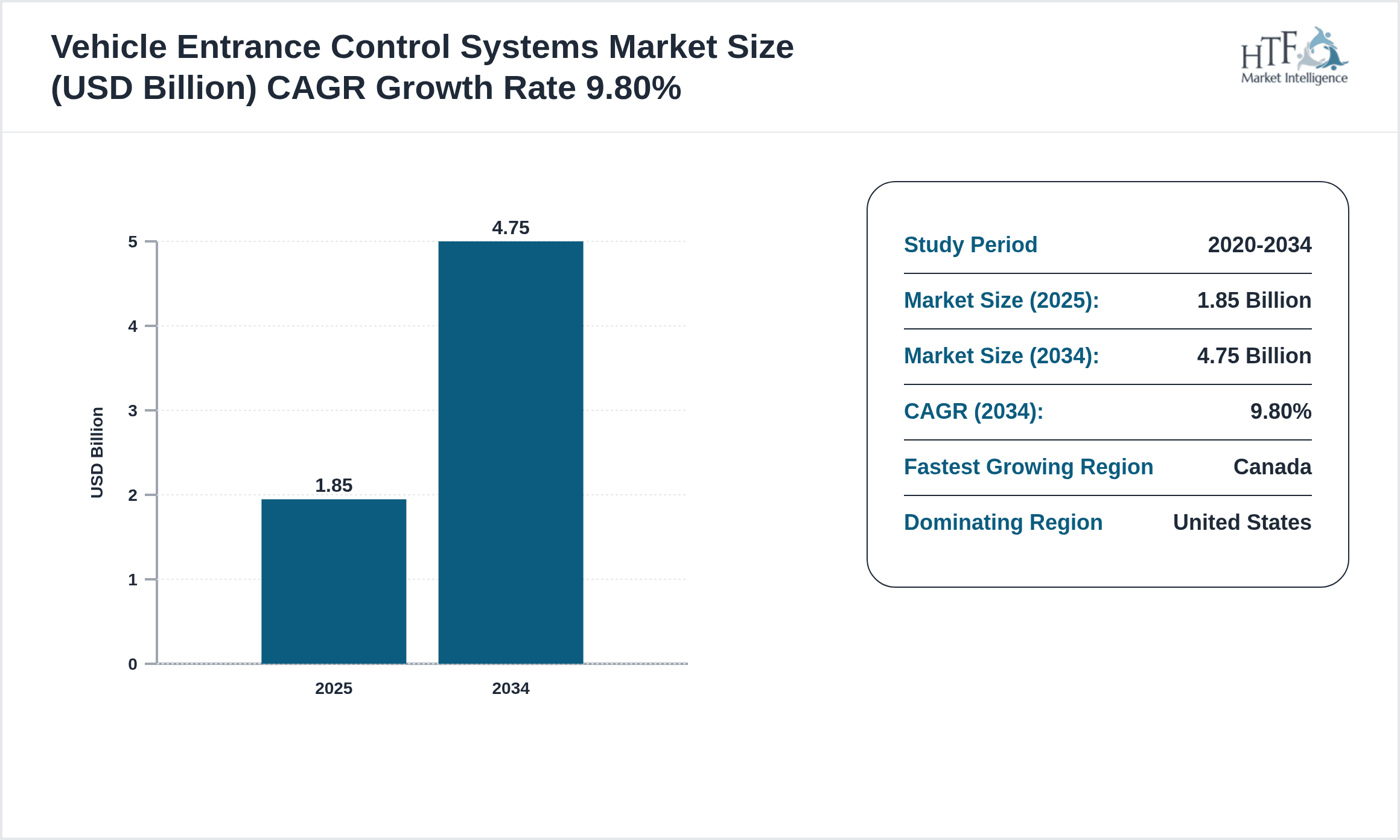

- •Market growth is influenced by increasing security concerns, urbanization, and smart infrastructure development, though adoption rates differ notably across sectors. Commercial and government sites tend to lead, while residential uptake can be inconsistent depending on local regulations and economic factors. The market size in 2024 stands at USD 1.85 Billion, expected to grow to USD 4.75 Billion by 2034, reflecting a compound annual growth rate (CAGR) of approximately 9.8%. This growth is propelled by technological advancements and increasing demand for integrated security solutions.

- •The strategic importance of vehicle entrance control systems lies in their role within broader security and access management frameworks. They enable facilities to mitigate risks, streamline vehicle flow, and support compliance with safety regulations. Despite some uneven adoption patterns, these systems are critical for modern infrastructure, and ongoing innovation is expected to drive further integration and market expansion.

Competitive Landscape

Competition in the North America Vehicle Entrance Control Systems market is dynamic, with a mix of established multinational corporations and regional specialists. Players often differentiate through technology innovation, such as integrating IoT capabilities or biometric authentication. Market positioning varies; some companies focus on large-scale commercial and government contracts, while others target residential or small business segments. Rivalry is intense, with a push towards offering comprehensive solutions combining hardware, software, and services. Strategic partnerships and product customization are common approaches to gain competitive advantage. Pricing pressures exist but innovation and service quality often offset pure cost competition. The fragmented nature of the market also leads to varied regional competition levels, influenced by local regulations and infrastructure maturity.

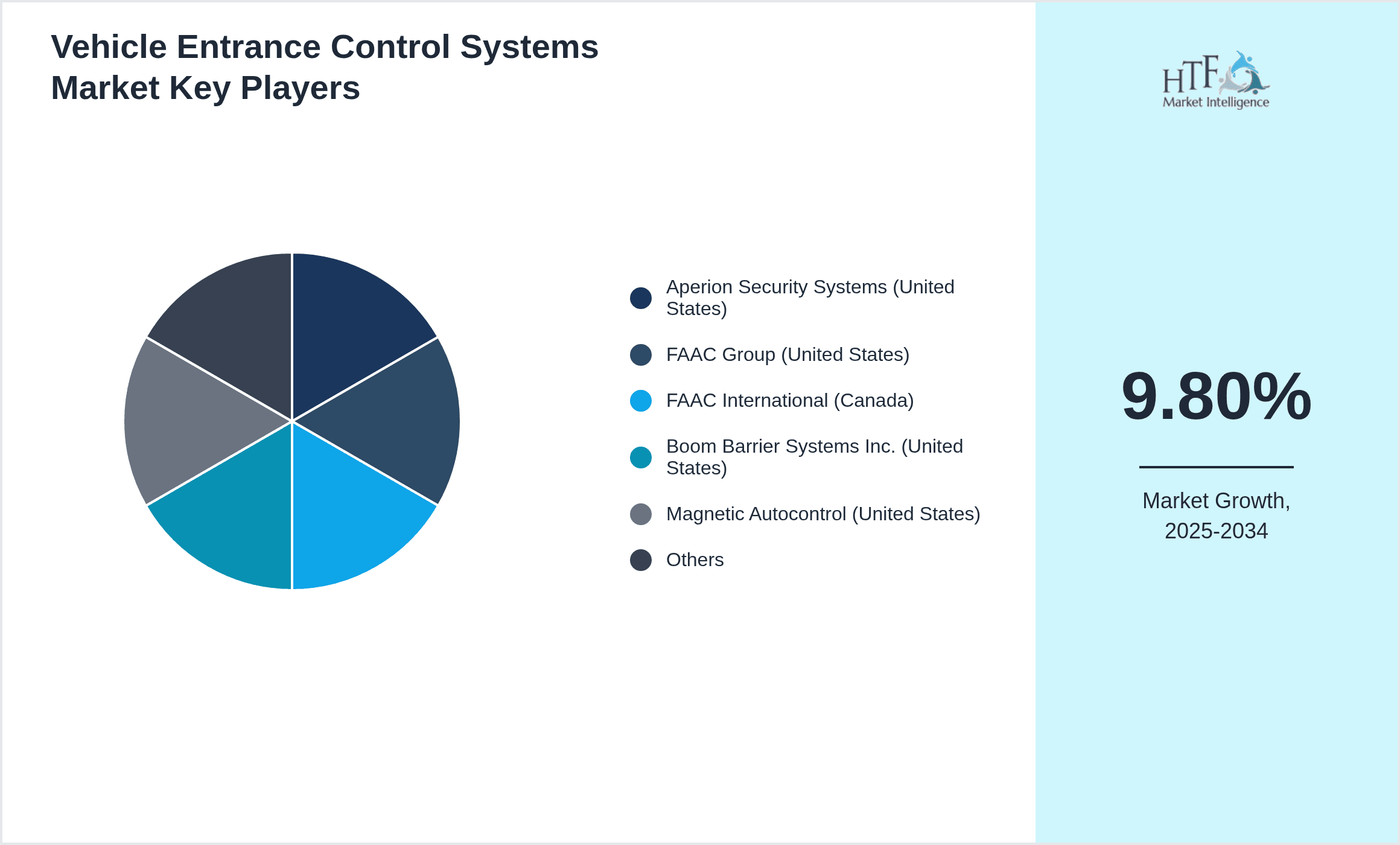

Leading Companies in Vehicle Entrance Control Systems Market

- •Aperion Security Systems (United States)

- •FAAC Group (United States)

- •FAAC International (Canada)

- •Boom Barrier Systems Inc. (United States)

- •Magnetic Autocontrol (United States)

- •Delta Scientific Corporation (United States)

- •Alvarado Manufacturing Co. (United States)

- •Gates & Barriers Inc. (Canada)

- •Hysecurity (United States)

- •DoorKing Inc. (United States)

- •FAAC USA (United States)

- •Stanley Security Solutions (United States)

- •Schneider Electric (United States)

- •Honeywell International Inc. (United States)

- •ASSA ABLOY Entrance Systems (United States)

- •Cardinal Gates Inc. (United States)

- •DormaKaba Group (Canada)

- •FAAC Group Canada (Canada)

- •Maglocks Inc. (United States)

- •Raymond Security Devices (United States)

- •LiftMaster (United States)

- •Nedap Identification Systems (United States)

- •FAAC North America (United States)

- •Gatekeeper Systems Inc. (United States)

- •TIBA Parking Systems (United States)

Market Breakdown

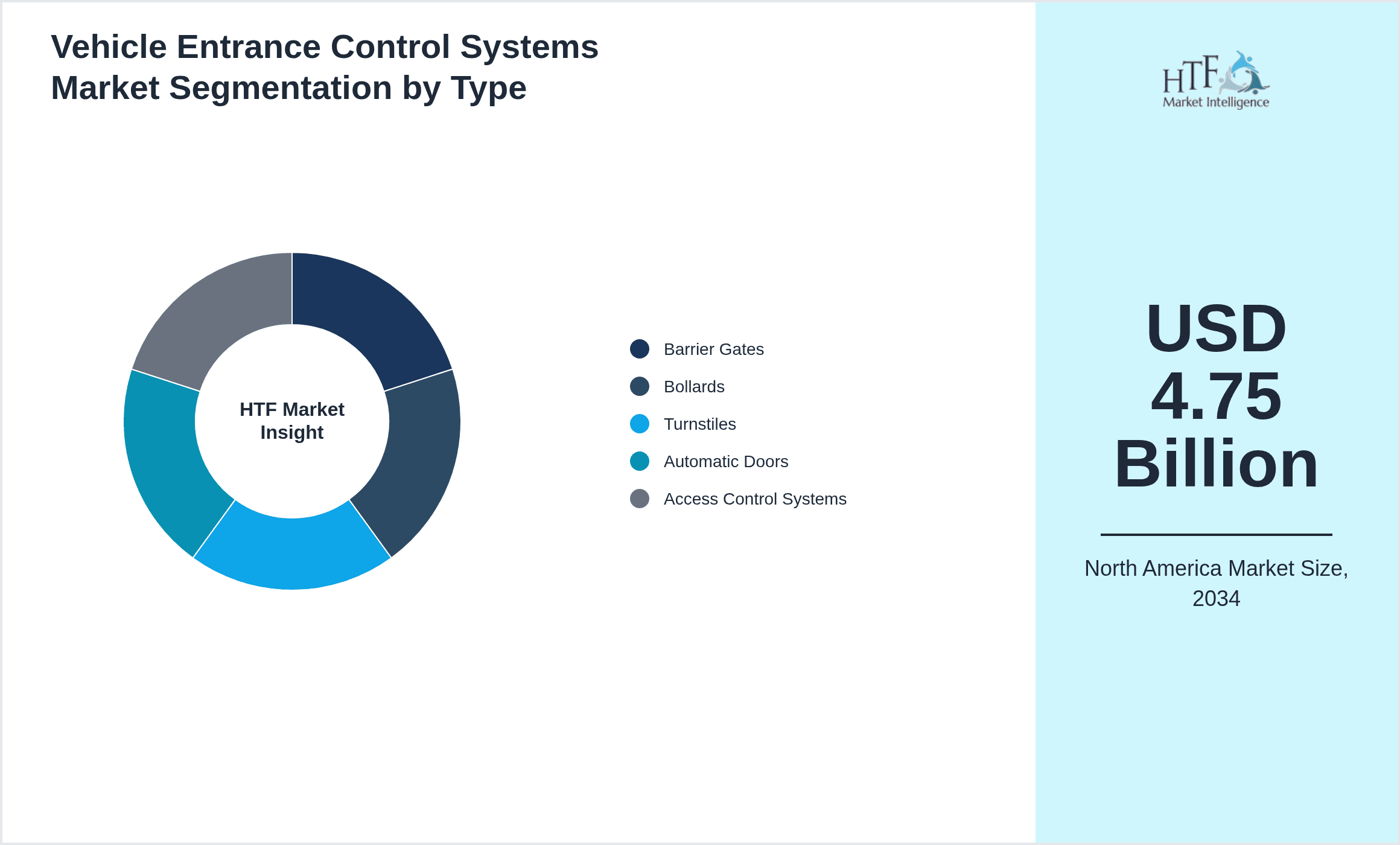

- •By Type

- ◦Barrier Gates

- ◦Bollards

- ◦Turnstiles

- ◦Automatic Doors

- ◦Access Control Systems

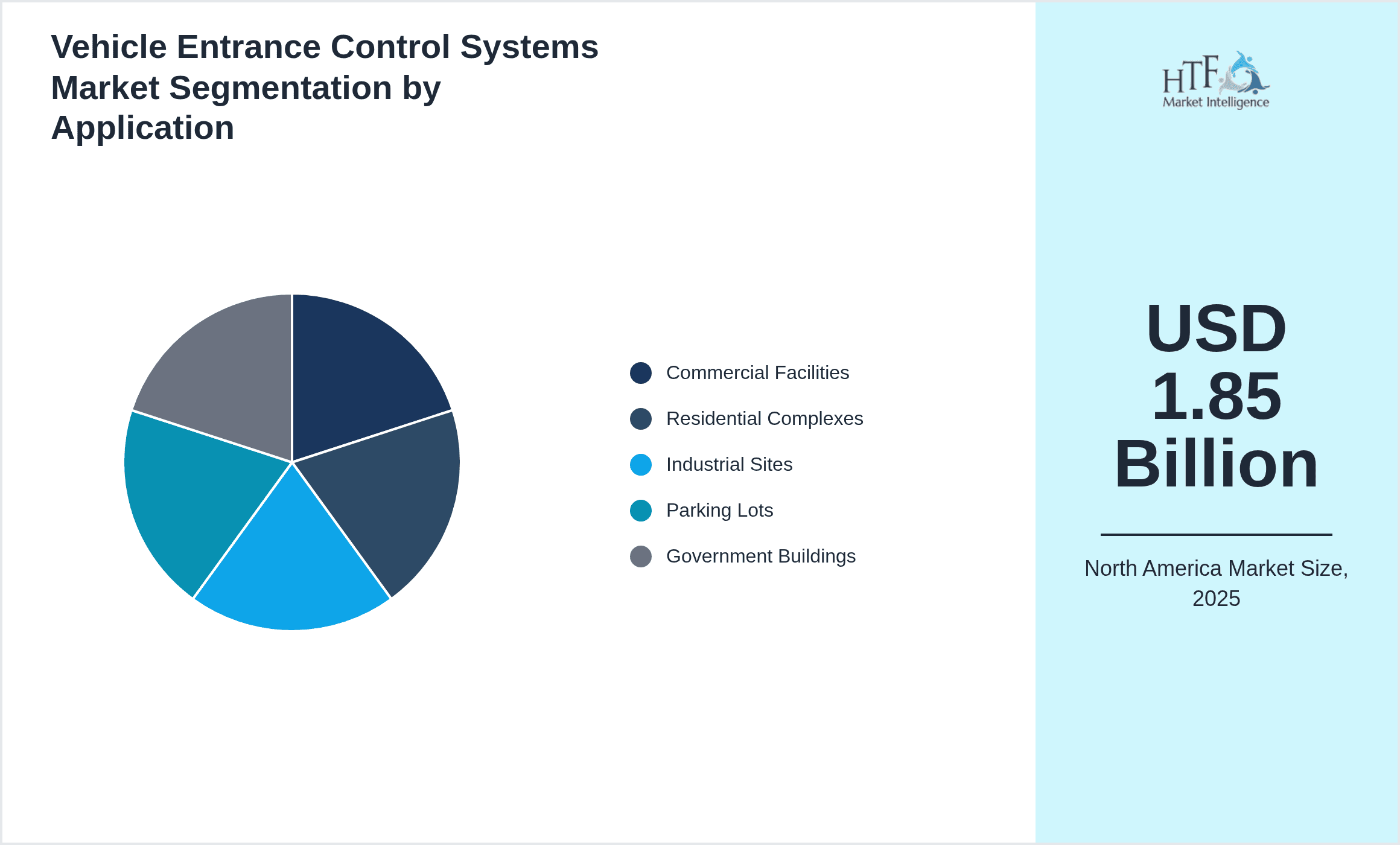

- •By Application

- ◦Commercial Facilities

- ◦Residential Complexes

- ◦Industrial Sites

- ◦Parking Lots

- ◦Government Buildings

- •By End User

- ◦Private Sector

- ◦Public Sector

- ◦Infrastructure

- ◦Transportation

- •By Technology

- ◦RFID-based Systems

- ◦Biometric Authentication

- ◦IoT-enabled Controls

- ◦Manual Controls

Growth Drivers

- •Rising security concerns across commercial and government premises are pushing the demand for advanced vehicle entrance control systems, especially in urban areas with increasing vehicular traffic and security threats.

- •Smart city initiatives and infrastructure modernization projects in North America are encouraging adoption of integrated, IoT-enabled systems that provide real-time monitoring and remote control capabilities.

- •Increasing regulatory mandates for safety and access control in residential and commercial buildings are incentivizing investments in automated entrance control solutions to comply with evolving standards.

- •Technological advancements such as biometric authentication and RFID applications are making vehicle entrance control systems more reliable and user-friendly, thus expanding their market appeal.

- •Growing emphasis on traffic management and vehicle flow optimization in parking and industrial sites is driving demand for sophisticated entrance control systems that can balance security with convenience.

Market Trends

- •There is a noticeable trend towards integration of vehicle entrance control systems with broader building management and security platforms, creating unified control environments but also introducing complexity in system compatibility.

- •Adoption of cloud-based management and analytics for entrance control is growing, allowing for better data-driven decisions though concerns over cybersecurity remain a stumbling block for some users.

- •Sustainability is influencing product design with more energy-efficient and durable materials being preferred, though cost considerations sometimes limit widespread uptake of greener options.

- •COVID-19 accelerated interest in contactless and automated vehicle entrance solutions, but the initial momentum has somewhat plateaued as budgets tighten and priorities shift.

- •Regional differences in adoption remain pronounced, with the United States leading in innovation uptake, while Canada and Mexico show more cautious investment patterns reflecting local economic conditions.

Market Restraints

- •High upfront costs for installation and integration of advanced vehicle entrance control systems can deter smaller businesses and residential complexes from adopting state-of-the-art solutions.

- •Complexity in integrating new systems with existing infrastructure often leads to delays and increased expenses, impacting the pace of market growth.

- •Concerns about privacy and data security related to biometric and IoT-enabled access systems raise regulatory and consumer hurdles that slow adoption.

- •Fragmented market demand across diverse applications creates challenges for manufacturers in standardizing products, limiting scalability and cost-efficiency.

- •Supply chain disruptions and component shortages, especially in semiconductor parts, have occasionally slowed down production and delivery timelines.

Market Opportunities

- •Expanding smart city programs offer significant opportunities to deploy advanced vehicle entrance control systems integrated with urban mobility and security networks.

- •Emerging technologies like AI-based vehicle recognition and predictive analytics can create new product categories and enhance system capabilities, attracting innovative adopters.

- •Growing demand for retrofit solutions in aging infrastructure provides a niche for companies specializing in cost-effective upgrades and modular system components.

- •Cross-industry partnerships, for example with IoT providers and cybersecurity firms, can open avenues for comprehensive security offerings and broaden market reach.

- •Increasing awareness and regulatory pressure for environmental compliance can stimulate demand for energy-efficient and sustainable entrance control products.

Market Challenges

- •Varying regional regulations and standards across North America complicate product design and certification processes, leading to longer time-to-market for new solutions.

- •Resistance to change among end-users, especially in traditional industries or smaller businesses, limits adoption of newer, more automated vehicle entrance control systems.

- •Competition from low-cost imports and non-specialized providers pressures pricing and erodes margins for established players focusing on quality and innovation.

- •Cybersecurity risks associated with networked access control systems require continuous investment in updates and monitoring, adding to operational costs.

- •Lack of skilled personnel for installation and maintenance in some regions hampers effective deployment and customer satisfaction.

Regulatory Overview

- •Recent regulatory updates in North America emphasize stricter safety standards for vehicle entrance control systems, particularly regarding emergency egress and fail-safe operations, enacted between 2019 and 2024.

- •Data privacy laws, including state-level regulations in the United States, now require enhanced protections for biometric data collected by access control systems, impacting system design and compliance.

- •Energy efficiency mandates under regional environmental programs push manufacturers to develop low-power and sustainable vehicle entrance control products.

- •Building codes increasingly integrate requirements for automated vehicle control systems in commercial and residential developments, influencing market demand and installation practices.

- •Government incentives for smart infrastructure projects provide financial support for deploying advanced vehicle entrance control technologies in public sector applications.

Industry Insights

- •In March 2024, Aperion Security Systems launched a new AI-enabled access control platform tailored for commercial parking facilities, featuring enhanced vehicle recognition and real-time analytics to improve security and traffic management. This product aims to address growing urban congestion issues while providing robust security features. The launch marks a significant step toward integrating AI into vehicle entrance systems in North America, highlighting shifting market demands towards smarter, data-driven solutions.

- •In October 2023, FAAC Group introduced a modular bollard system with IoT connectivity designed for industrial and government sites. The system allows remote monitoring and automated response capabilities, aiming to reduce manual interventions and enhance perimeter security. This innovation reflects increasing interest in scalable and remotely manageable vehicle control infrastructure, catering to sectors with complex security requirements.

Mergers & Acquisitions

- •In July 2024, Delta Scientific Corporation acquired Maglocks Inc., a move aimed at expanding its product portfolio into advanced electronic locking mechanisms and access control hardware. The acquisition is expected to strengthen Delta Scientific’s foothold in the high-security vehicle entrance segment, enabling integration of electronic and physical barriers under a unified brand. This strategic consolidation reflects the market trend toward offering comprehensive security solutions.

- •In December 2023, Stanley Security Solutions completed the acquisition of Gatekeeper Systems Inc., enhancing its presence in the North American vehicle entrance control market. This acquisition provides Stanley with advanced automated gate technology and access management software, facilitating cross-selling opportunities and improved service offerings. The deal underscores the importance of software integration in modern vehicle entrance control systems.

Recent Industry News

- •On 15th January 2025, DoorKing Inc. announced a partnership with a leading IoT platform provider to develop cloud-based vehicle entrance control solutions for smart cities. This collaboration aims to deliver scalable, remotely managed access systems that integrate with urban infrastructure, addressing the increasing demand for connected security solutions in metropolitan areas. The initiative positions DoorKing to capitalize on smart city investments across North America. Source: Company Press Release

- •On 28th February 2025, Hysecurity launched its latest automatic barrier gate with AI-powered vehicle identification capabilities, designed for commercial and government facilities. The new product enables faster processing of authorized vehicles and enhanced security through machine learning algorithms, facilitating improved traffic flow and threat detection. This launch highlights the growing role of AI in vehicle entrance management. Source: Industry Publication

- •On 10th March 2025, FAAC Group expanded its manufacturing facility in Canada to increase production capacity for smart bollards and access control systems. This expansion responds to rising demand in industrial and municipal sectors, reflecting optimism in market growth despite recent supply chain challenges. The move supports FAAC's strategy to localize production and reduce lead times. Source: Company Website

- •On 22nd April 2025, Aperion Security Systems entered into a strategic alliance with a cybersecurity firm to enhance the data protection features of its vehicle entrance control platforms. The partnership focuses on integrating advanced encryption and threat detection to address increasing cybersecurity concerns in IoT-enabled security devices. This collaboration reflects the market’s prioritization of secure, reliable access control solutions. Source: Official Press Release

Market Statistics

- •CAGR by 2034: 9.8%

- •Market Size by 2034: USD 4.75 Billion

- •Market Size in 2025: USD 2.03 Billion

- •Dominating Type: Barrier Gates; Next-Following Type: Access Control Systems

- •Dominating Application: Commercial Facilities; Next-Following Application: Residential Complexes

- •Dominating Region: United States; Second-Leading Region: Canada

- •Region with Highest Growth Rate: Canada

- •Dominating Country: United States

Market Share Table

- •Market Share (%) by Type: Barrier Gates 45%, Access Control Systems 30%

- •Market Share (%) by Application: Commercial Facilities 50%, Residential Complexes 25%

- •Growth Rate (%) by Type: Barrier Gates 8.5%, Access Control Systems 12.3%

- •Growth Rate (%) by Application: Commercial Facilities 9.0%, Residential Complexes 10.5%

Top 5 Global Players

- •FAAC Group (United States)

- •Delta Scientific Corporation (United States)

- •Stanley Security Solutions (United States)

- •Aperion Security Systems (United States)

- •DoorKing Inc. (United States)

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.85 Billion |

| Forecast Year Market Size | USD 4.75 Billion |

| CAGR | 9.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.4% |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Aperion Security Systems (United States), FAAC Group (United States), FAAC International (Canada), Boom Barrier Systems Inc. (United States), Magnetic Autocontrol (United States), Delta Scientific Corporation (United States), Alvarado Manufacturing Co. (United States), Gates & Barriers Inc. (Canada), Hysecurity (United States), DoorKing Inc. (United States), FAAC USA (United States), Stanley Security Solutions (United States), Schneider Electric (United States), Honeywell International Inc. (United States), ASSA ABLOY Entrance Systems (United States), Cardinal Gates Inc. (United States), DormaKaba Group (Canada), FAAC Group Canada (Canada), Maglocks Inc. (United States), Raymond Security Devices (United States), LiftMaster (United States), Nedap Identification Systems (United States), FAAC North America (United States), Gatekeeper Systems Inc. (United States), TIBA Parking Systems (United States) |

North America Vehicle Entrance Control Systems Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.