Global Membrane Process Sodium Hydroxide Market - Outlook 2025-2034

Global Membrane Process Sodium Hydroxide Market is segmented by Type (Membrane Cell, Mercury Cell, Diaphragm Cell), Application (Chemical Manufacturing, Water Treatment, Pulp & Paper, Food Processing, Pharmaceuticals), End User (Industrial Manufacturing Plants, Municipal Water Facilities, Food & Beverage Companies, Pharmaceutical Manufacturers), Technology (Membrane Electrolysis, Mercury Electrolysis, Diaphragm Electrolysis), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Membrane Process Sodium Hydroxide Market centers on the production of sodium hydroxide via membrane cell technology, an electrolytic method prized for producing high purity caustic soda with lower environmental impact compared to older technologies. This market includes related products and services but excludes non-electrolytic or legacy manufacturing methods. Sodium hydroxide produced is critical across chemical manufacturing, water treatment, pulp & paper, food processing, and pharmaceutical sectors. The membrane process's increasing adoption, driven by regulatory pressures and process efficiency, defines the market scope.

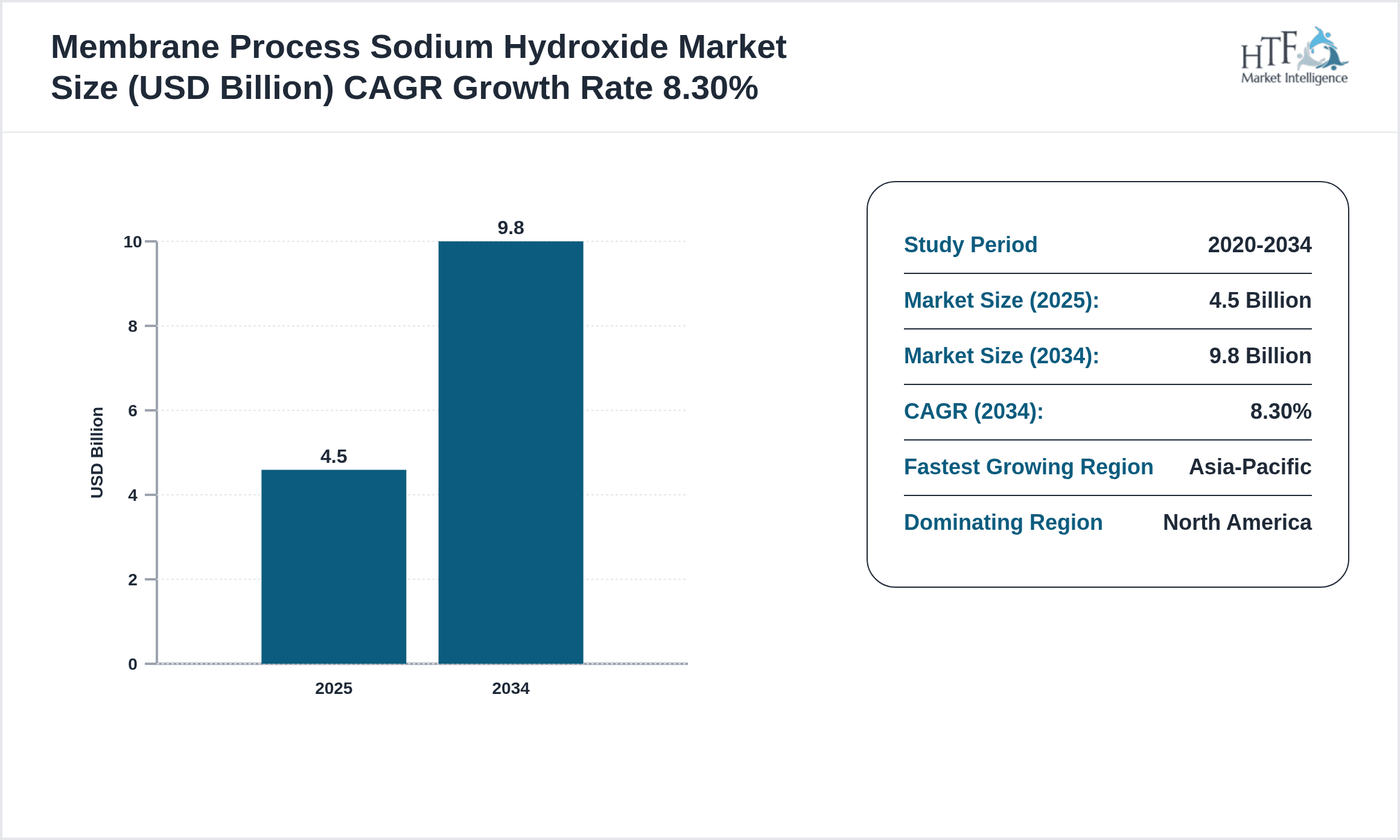

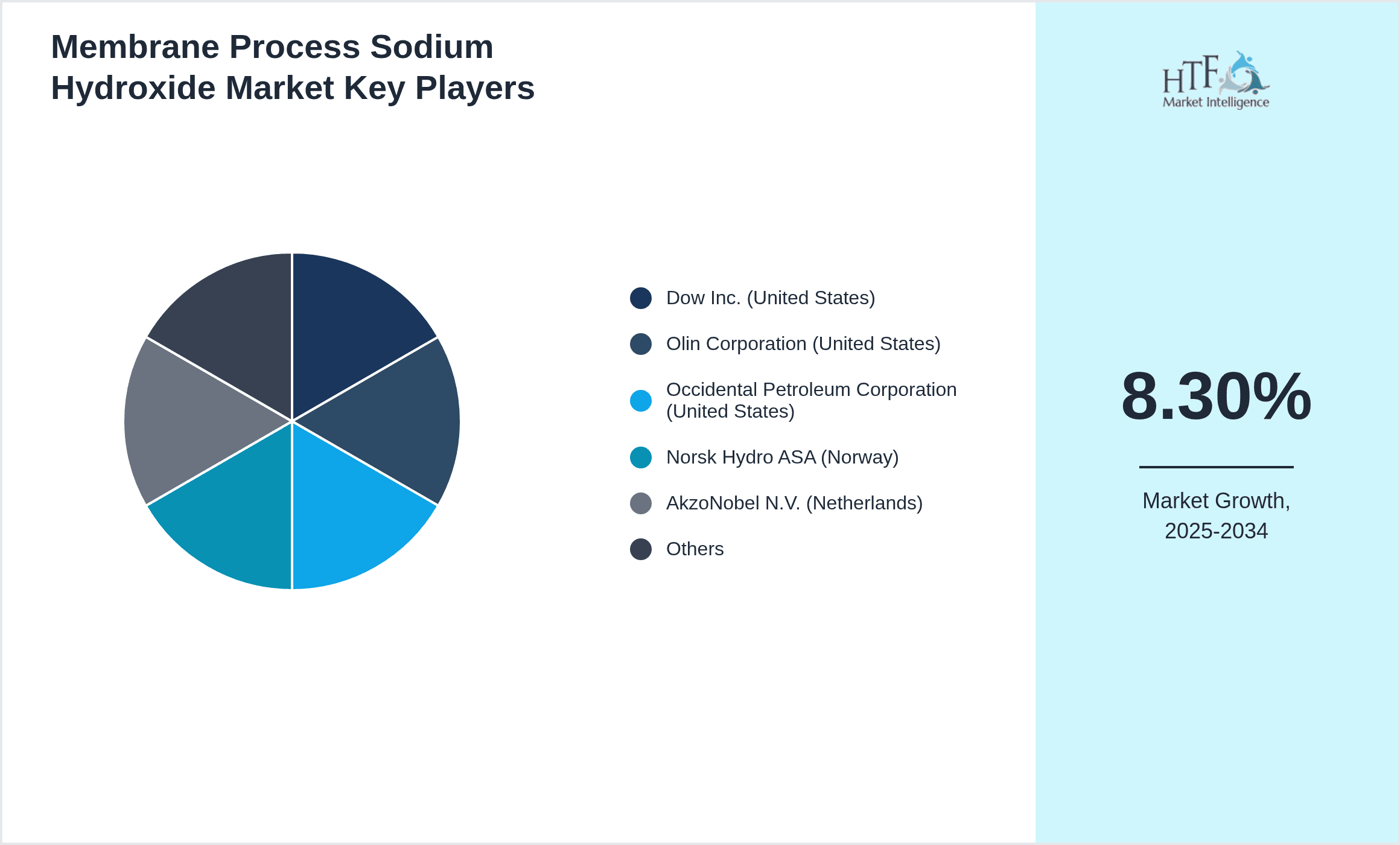

- •Key highlights show membrane cell technology as the dominant type with growing market share due to environmental and operational advantages. North America leads the market currently, but Asia-Pacific is rapidly gaining ground with a higher CAGR fueled by industrial expansion and infrastructure development. Overall market size is projected to more than double from USD 4.5 Billion in 2025 to USD 9.8 Billion by 2034 at a CAGR of 8.3%.

- •The market holds strategic importance for industries requiring high-purity sodium hydroxide and for stakeholders aiming to balance production efficiency with sustainability. Advances in membrane technology, coupled with regulatory trends pushing away from mercury cells, create a dynamic environment for investment and innovation. The membrane process sodium hydroxide market thus represents both an established and evolving industrial segment with broad application relevance.

Competitive Landscape

Competition in the membrane process sodium hydroxide market is intense, driven by innovation in membrane technology and the push for environmentally friendly production. Market leaders focus on developing energy-efficient membranes and scaling capacity while maintaining product purity. Rivalry revolves around technology licensing, process optimization, and strategic partnerships rather than price wars alone. Entry barriers are high due to capital intensity and regulatory compliance, but emerging players, especially in Asia-Pacific, are challenging established firms. Companies also differentiate via service support and integration capabilities, anticipating future environmental regulations. The market sees collaborative ventures and continuous R&D as key to securing and expanding market share.

Leading Companies in Membrane Process Sodium Hydroxide Market

- •Dow Inc. (United States)

- •Olin Corporation (United States)

- •Occidental Petroleum Corporation (United States)

- •Norsk Hydro ASA (Norway)

- •AkzoNobel N.V. (Netherlands)

- •Solvay S.A. (Belgium)

- •Tianjin Bohai Chemical Industry Group Co., Ltd. (China)

- •Formosa Plastics Corporation (Taiwan)

- •Mitsubishi Chemical Holdings Corporation (Japan)

- •Jiangsu Yangnong Chemical Group Co., Ltd. (China)

- •BASF SE (Germany)

- •Sinopec Corporation (China)

- •Linde plc (United Kingdom)

- •Ercros S.A. (Spain)

- •Tessenderlo Group (Belgium)

- •Westlake Chemical Corporation (United States)

- •Shandong Haihua Group Co., Ltd. (China)

- •Mosaic Company (United States)

- •Chemours Company (United States)

- •Covestro AG (Germany)

Market Breakdown

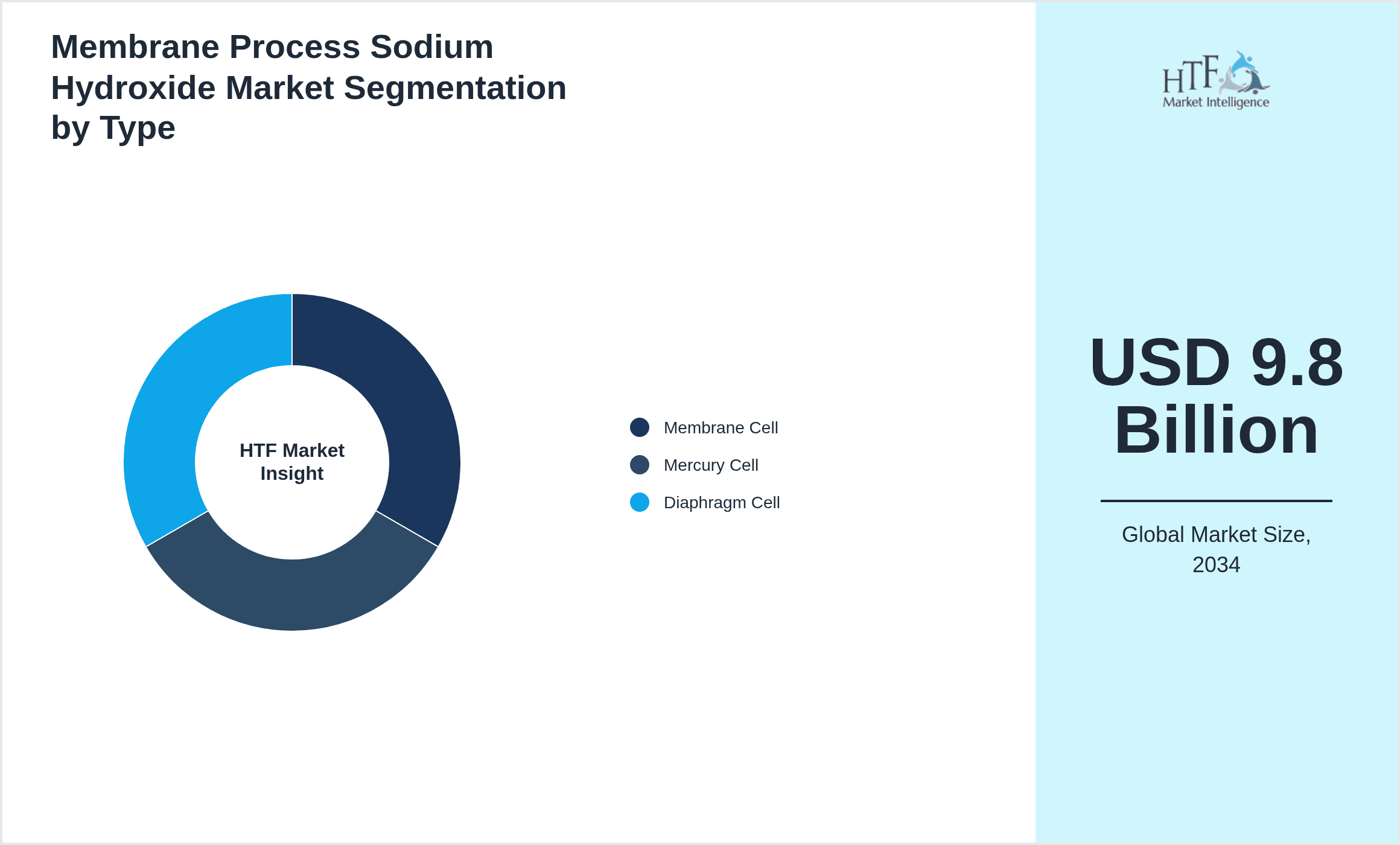

- •By Type

- ◦Membrane Cell

- ◦Mercury Cell

- ◦Diaphragm Cell

- •By Application

- ◦Chemical Manufacturing

- ◦Water Treatment

- ◦Pulp & Paper

- ◦Food Processing

- ◦Pharmaceuticals

- •By End User

- ◦Industrial Manufacturing Plants

- ◦Municipal Water Facilities

- ◦Food & Beverage Companies

- ◦Pharmaceutical Manufacturers

- •By Technology

- ◦Membrane Electrolysis

- ◦Mercury Electrolysis

- ◦Diaphragm Electrolysis

Growth Dynamics

- •Growth Drivers: Increasing demand for high-purity sodium hydroxide in chemical manufacturing and water treatment is a core driver. Membrane process offers environmental benefits over mercury cells, aligning with tightening regulations globally. Industrial expansion in Asia-Pacific, coupled with infrastructure development needing water treatment chemicals, propels market growth. The rising preference for sustainable processes and replacement of legacy technologies fuels investments in membrane cell plants. However, growth is sometimes inconsistent due to regional regulatory differences and capital intensity of membrane technology installations, which can delay adoption in less developed regions.

- •Trends: There's a notable shift towards membrane electrolysis driven by environmental concerns around mercury usage. Industry players are investing in energy-efficient membranes and automation to reduce operational costs. Growth in water treatment applications reflects increasing urbanization and stricter water quality standards globally. Also, integration with renewable energy for electrolysis processes is emerging, although adoption is uneven and sometimes limited by infrastructure constraints. Regional variations mean that while developed regions adopt newer technologies faster, emerging markets often rely longer on established methods.

- •Restraints: High initial capital expenditure for membrane cell setups restricts uptake, especially in price-sensitive markets. Additionally, membrane fouling and maintenance complexities can increase operating costs, which limits usage in industries with tight margins. Regulatory delays in some developing countries slow transitions from mercury-based processes. Supply chain interruptions for membrane components have also caused unexpected slowdowns. The technical expertise required for membrane technology operation is uneven globally, creating pockets where adoption lags even when economic incentives exist.

- •Opportunities: Expansion of water treatment infrastructure in developing regions offers significant growth prospects for membrane process sodium hydroxide. Innovations in membrane materials to enhance durability and performance can lower lifecycle costs and open new markets. Collaborations between membrane technology providers and chemical manufacturers can accelerate adoption. Furthermore, increasing demand in pharmaceutical and food processing industries for high-grade caustic soda presents niche opportunities. Emerging economies transitioning toward sustainable manufacturing present fertile ground, though real-world uptake is sometimes slower than projections suggest.

- •Challenges: Market players face challenges in balancing cost and performance, especially as membrane technology evolves rapidly. Regulatory uncertainties in certain jurisdictions create risk for long-term investments. Competition from alternative sodium hydroxide production methods, though less environmentally friendly, persists due to entrenched infrastructure. Technical challenges with membrane lifespan and fouling remain unresolved in some applications, leading to inconsistent operational efficiency. Additionally, uneven regional adoption rates create fragmented market dynamics, complicating global strategy planning for manufacturers and suppliers.

Market Trends

- •Increasing environmental regulations globally are accelerating the phase-out of mercury cell technology in favor of membrane processes, though the pace varies by region. This uneven regulatory landscape creates mixed adoption rates and investment patterns. Industry is also seeing a rise in digital monitoring and automation of membrane systems to improve reliability and reduce downtime. Some companies are experimenting with renewable energy-powered electrolysis, but infrastructure and costs limit scale. Water treatment demand is increasingly shaping product specifications, reflecting broader sustainability goals across industries.

- •Innovation in membrane materials is trending, aiming to enhance durability and reduce fouling, yet real-world performance gains are gradual and sometimes inconsistent. Strategic partnerships between chemical producers and membrane technology firms are becoming more common to accelerate technology adoption. However, in many emerging markets, legacy technologies persist due to cost and operational familiarity. This creates a patchwork market where cutting-edge and traditional processes coexist, complicating uniform growth forecasts.

- •Regional infrastructure development, especially in Asia-Pacific and Latin America, is a significant trend driving water treatment application growth. Meanwhile, mature markets in North America and Europe focus on process optimization and cost reduction. The pharmaceutical and food processing sectors are increasingly specifying membrane process sodium hydroxide for its purity and compliance benefits, reflecting a trend toward tighter quality controls. However, supply chain disruptions occasionally delay projects and affect market momentum.

Market Opportunities

- •Developing regions represent untapped potential for membrane process sodium hydroxide, especially where growing industries require high-purity chemicals but face environmental regulation pressures. Investment in membrane technology can enable compliance and operational efficiency, although financing and technical know-how remain barriers. New membrane materials that reduce fouling and maintenance costs could significantly enhance market penetration. Additionally, expanding applications in pharmaceuticals and specialty chemicals offer opportunities for premium product segments.

- •Collaborations between technology providers and end-users to co-develop tailored membrane solutions open avenues for competitive differentiation. Expansion into water treatment for municipal and industrial use in rapidly urbanizing areas could drive volume growth. There's also potential in integrating membrane electrolysis with renewable energy sources to reduce carbon footprints, aligning with global decarbonization trends. However, real adoption depends on infrastructure readiness and cost competitiveness.

Market Challenges

- •High capital requirements and complexity of membrane process installations limit uptake in cost-sensitive markets, especially where legacy technologies remain entrenched. Membrane fouling and related maintenance costs pose operational challenges, reducing attractiveness for some users. Regulatory uncertainty in emerging economies creates investment risk, slowing market expansion. Competition from conventional sodium hydroxide production methods, despite environmental drawbacks, persists due to established infrastructure and lower upfront costs. The uneven global distribution of technical expertise hampers consistent adoption, creating fragmented market growth.

- •Supply chain disruptions for specialized membrane components have caused unpredictable delays, affecting project timelines and operational continuity. Moreover, the rapid pace of membrane technology innovation requires continuous capital reinvestment, which can dissuade risk-averse players. The balance between maintaining membrane performance and controlling operational costs remains a persistent challenge. Regional differences in environmental policies further complicate market strategies for multinational players.

Regulatory Framework

- •Between 2020 and 2025, many regions, notably Europe and North America, implemented stricter regulations limiting or banning mercury cell technology due to environmental and health concerns. These regulations mandate gradual phase-outs and incentivize membrane process adoption through subsidies and tax benefits. Water quality standards have also tightened globally, pushing demand for purer sodium hydroxide products. Emerging markets have begun aligning with these trends but with slower enforcement, creating a staggered regulatory landscape. Compliance with environmental discharge norms and workplace safety standards continues to shape manufacturing practices and investment decisions in the membrane process sodium hydroxide market.

- •Additional guidelines focus on energy efficiency and emissions reduction in chemical manufacturing facilities, indirectly promoting membrane electrolysis due to its lower energy consumption relative to mercury cells. Some countries introduced mandatory reporting and certification for sodium hydroxide production technologies, enhancing transparency and driving market transformation. Overall, evolving regulatory frameworks are a key driver for technology shifts but also a source of complexity for global market players.

Market Intelligence

- •15th February 2024, Dow Inc. announced the launch of an advanced membrane electrolysis system with enhanced durability and energy efficiency targeting the chemical manufacturing sector. This new system aims to reduce operational costs by 15% while increasing sodium hydroxide purity levels, responding to growing environmental regulations and customer demand for sustainable solutions. Dow plans to roll out this technology globally over the next three years, focusing on emerging markets with increasing industrial demand.

- •23rd October 2024, Formosa Plastics Corporation introduced a next-generation membrane material designed to resist fouling and extend system operational life by up to 30%. This innovation could lower maintenance downtime and improve process reliability, particularly in water treatment applications where membrane degradation has been a limiting factor. Formosa’s strategic objective is to capture a larger share of the Asia-Pacific market by addressing these pain points with this new product line.

- •7th May 2025, Olin Corporation announced a strategic partnership with a leading membrane technology firm to co-develop customized electrolysis solutions geared towards pharmaceutical industry requirements. The collaboration aims to leverage Olin's chemical production expertise and its partner’s membrane advancements to create high-purity sodium hydroxide products meeting stringent pharmaceutical grade standards. This move reflects broader industry trends emphasizing product quality and regulatory compliance.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.5 Billion |

| Forecast Year Market Size | USD 9.8 Billion |

| CAGR | 8.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8% |

| Scope of Report | Market is segmented by Type (Membrane Cell, Mercury Cell, Diaphragm Cell), Application (Chemical Manufacturing, Water Treatment, Pulp & Paper, Food Processing, Pharmaceuticals), End User (Industrial Manufacturing Plants, Municipal Water Facilities, Food & Beverage Companies, Pharmaceutical Manufacturers), Technology (Membrane Electrolysis, Mercury Electrolysis, Diaphragm Electrolysis) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Dow Inc. (United States), Olin Corporation (United States), Occidental Petroleum Corporation (United States), Norsk Hydro ASA (Norway), AkzoNobel N.V. (Netherlands), Solvay S.A. (Belgium), Tianjin Bohai Chemical Industry Group Co., Ltd. (China), Formosa Plastics Corporation (Taiwan), Mitsubishi Chemical Holdings Corporation (Japan), Jiangsu Yangnong Chemical Group Co., Ltd. (China), BASF SE (Germany), Sinopec Corporation (China), Linde plc (United Kingdom), Ercros S.A. (Spain), Tessenderlo Group (Belgium), Westlake Chemical Corporation (United States), Shandong Haihua Group Co., Ltd. (China), Mosaic Company (United States), Chemours Company (United States), Covestro AG (Germany) |

Global Membrane Process Sodium Hydroxide Market - Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.