Anhydrous Hydrofluoric Acid Market - Global Growth Opportunities 2021-2033

Global Anhydrous Hydrofluoric Acid Market is segmented by Application (Chemical Manufacturing, Semiconductor Processing, Metal Treatment, Glass Etching, Petrochemical Processing), Type (Industrial Grade, Electronic Grade, Reagent Grade, High Purity Grade, Technical Grade), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Industry Overview

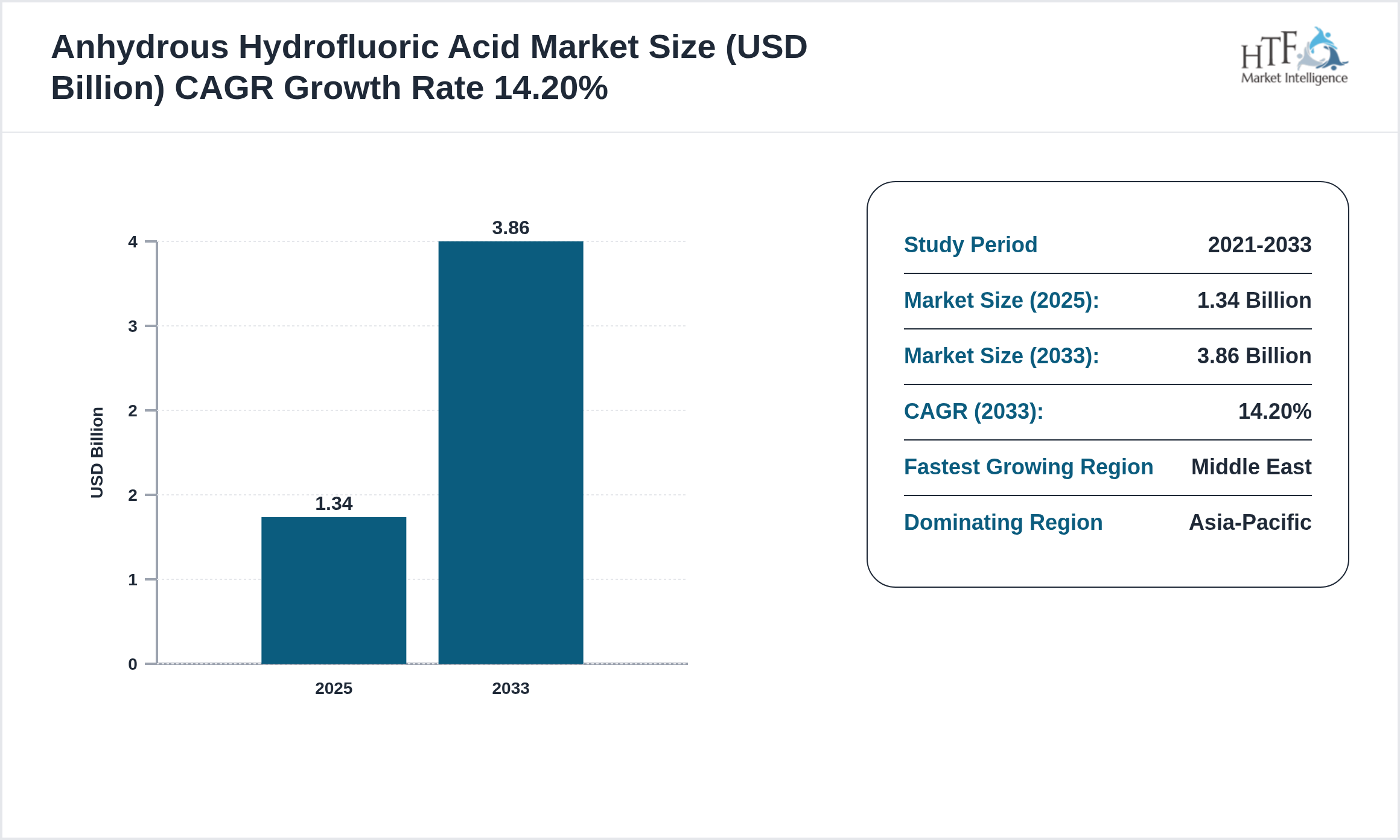

The Anhydrous Hydrofluoric Acid is at USD 1.34 billion in 2025 and is expected to reach 3.86 billion by 2033. The Anhydrous Hydrofluoric Acid is driven by increasing demand in end-use industries, technological advancements, research and development (R&D), economic growth, and global trade.

A highly reactive chemical used in various industrial applications, including etching and cleaning, valued for its properties. Anhydrous hydrofluoric acid enhances the performance of chemical processes. The demand for this compound is growing with the increasing focus on industrial chemistry. Innovations in chemical handling are driving advancements in this sector.

Source: HTF Market Intelligence (HTF MI)

Competitive landscape

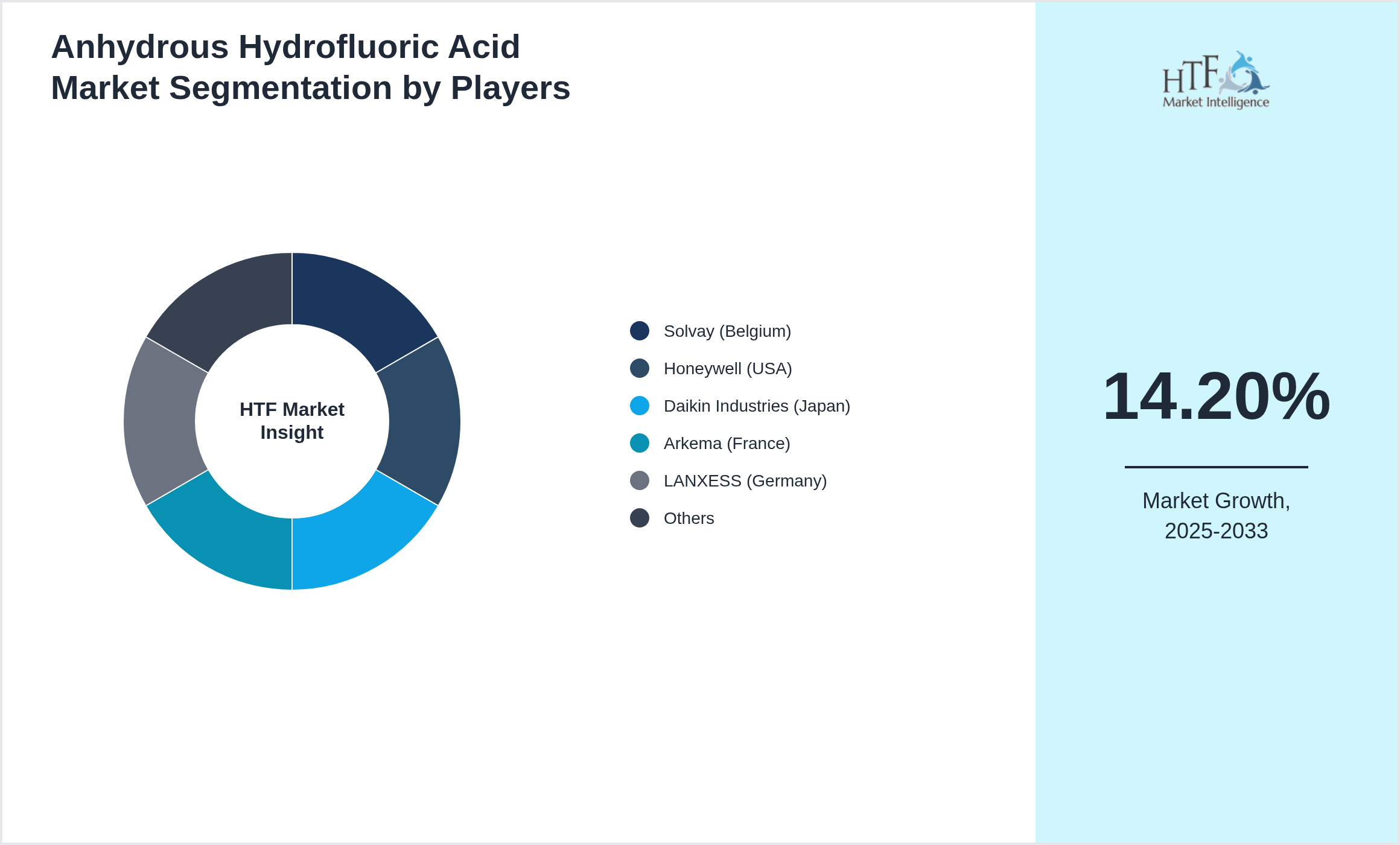

The companies highlighted in this profile were selected based on insights from primary experts and an evaluation of their market penetration, product offerings, and geographical reach:

- • Solvay (Belgium)

- • Honeywell (USA)

- • Daikin Industries (Japan)

- • Arkema (France)

- • LANXESS (Germany)

- • Fubao Group (China)

- • Dongyue Group (China)

- • Zhejiang Sanmei (China)

- • Gujarat Fluorochemicals (India)

- • Navin Fluorine (India)

- • Mexichem (Mexico)

- • Fluorchemie Group (Germany)

- • Sinochem Lantian (China)

- • Juhua Group (China)

- • Morita Chemical (Japan)

Market Drivers:

Challenge Factor:

Opportunities:

Important Trend:

Regulatory Framework

- • Strict chemical handling regulations govern production

- • storage

- • and transportation of hydrofluoric acid

- • ensuring worker safety

- • environmental protection

- • and compliance with hazardous material standards globally.

Regional Insight

The Asia-Pacific leads the market share, largely due to rising consumption, a growing population, and strong economic momentum that boosts demand. In contrast, the Middle East is emerging as the fastest-growing area, driven by rapid infrastructure development, the expansion of industrial sectors, and heightened consumer demand, making it a critical factor for future market growth. The regions covered in the report are

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

Regional Analysis

- • Asia-Pacific leads in chemical production. North America follows with industrial demand. Europe emphasizes safety compliance. Latin America is growing. Middle East supports petrochemical use.

Market Segmentation

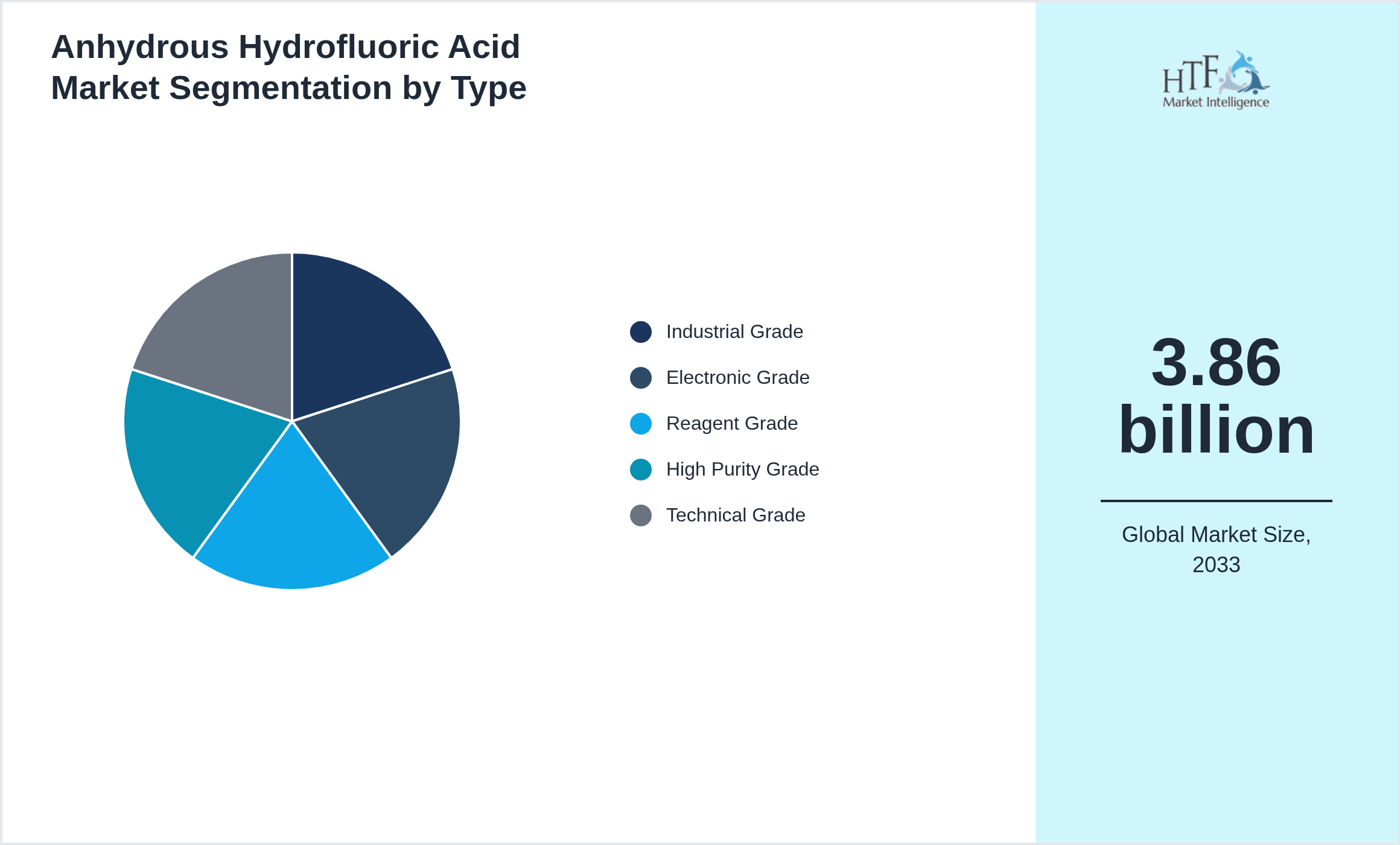

Segmentation by Type

- • Industrial Grade

- • Electronic Grade

- • Reagent Grade

- • High Purity Grade

- • Technical Grade

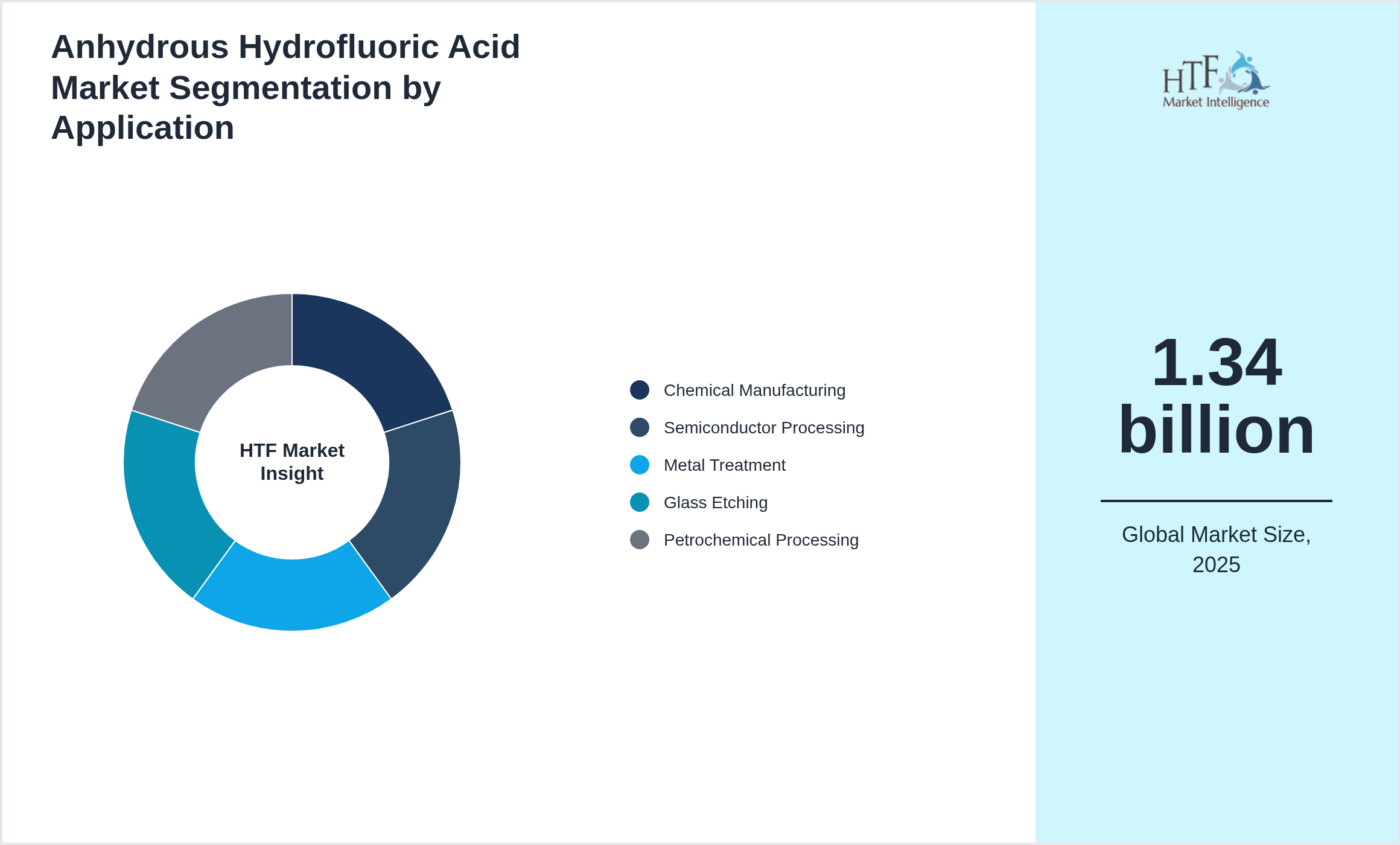

Segmentation by Application

- • Chemical Manufacturing

- • Semiconductor Processing

- • Metal Treatment

- • Glass Etching

- • Petrochemical Processing

Key Development Activities

Market Entropy

- • In 2024: Chemical manufacturing expansion strengthened demand for hydrofluoric acid applications.

- • Industrial processing requirements improved material utilization.

- • Semiconductor manufacturing strengthened specialized demand.

- • Safety regulations improved handling infrastructure.

- • In 2025: Advanced chemical purification technologies enhanced production efficiency.

- • Demand from electronics manufacturing strengthened supply chain stability.

- • In 2026: Sustainable chemical processing strengthened environmental compliance.

- • Smart monitoring systems improved industrial safety

Merger & Acquisition

- • In 2024: Chemical processing increased hydrofluoric acid demand.

- • Industrial applications diversified usage.

- • In 2025: Semiconductor manufacturing strengthened demand.

- • Safety regulations improved handling practices.

- • In 2026: Mature chemical markets stabilized acid demand cycles.

Regulatory Landscape

- • Strict chemical handling regulations govern production

- • storage

- • and transportation of hydrofluoric acid

- • ensuring worker safety

- • environmental protection

- • and compliance with hazardous material standards globally.

Patent Analysis

- • Patent activity focuses on safe handling and processing technologies. Chemical purity improvements are emerging. Storage innovations are patented. Industrial applications drive filings. Safety technologies dominate.

Investment and Funding Scenario

- • Investments are driven by chemical and petrochemical industries. Funding focuses on safety and efficiency. Asia-Pacific leads production investment. Industrial demand drives funding. Regulatory compliance impacts spending.

Report Details

| Report Features | Details |

| Base Year | 2025 |

| Based Year Market Size (2025) | 1.34 billion |

| Historical Period | 2021 to 2025 |

| CAGR (2025 to 2033) | 14.20% |

| Forecast Period | 2026 to 2033 |

| Forecasted Period Market Size (2033) | 3.86 billion |

| Scope of the Report | Industrial Grade, Electronic Grade, Reagent Grade, High Purity Grade, Technical Grade, Chemical Manufacturing, Semiconductor Processing, Metal Treatment, Glass Etching, Petrochemical Processing |

| Companies Covered | Solvay (Belgium), Honeywell (USA), Daikin Industries (Japan), Arkema (France), LANXESS (Germany), Fubao Group (China), Dongyue Group (China), Zhejiang Sanmei (China), Gujarat Fluorochemicals (India), Navin Fluorine (India), Mexichem (Mexico), Fluorchemie Group (Germany), Sinochem Lantian (China), Juhua Group (China), Morita Chemical (Japan) |

| Customization Scope | 15% Free Customization |

| Delivery Format | PDF and Excel through Email |

Research Methodology

The research methodology involves several key steps to ensure comprehensive and accurate insights. First, the objectives of the research are clearly defined, focusing on aspects such as market size, growth trends, and competitive dynamics. Data collection is conducted through both primary and secondary methods. Primary research includes interviews with industry experts, surveys, and focus groups to gather firsthand information, while secondary research involves analyzing existing reports, government publications, and company filings.

The collected data is then subjected to rigorous analysis, with quantitative methods used to evaluate market size and trends and qualitative methods applied to understand industry dynamics and consumer behavior. Findings are compiled into a detailed report featuring key insights, data visualizations, and strategic recommendations. Validation is achieved through data verification and peer reviews to ensure accuracy.

Finally, the research concludes with actionable insights and recommendations, along with suggestions for future studies to address emerging trends and gaps. This methodology provides a structured approach to understanding the {keywords} and guiding strategic decisions.