Middle East Automotive Adaptive Lighting Systems Market Size, Growth & Revenue 2025-2034

Middle East Automotive Adaptive Lighting Systems Market is segmented by Type (LED Adaptive Lighting, HID Adaptive Lighting, Laser Adaptive Lighting, OLED Adaptive Lighting, Halogen Adaptive Lighting), Application (Passenger Vehicles, Commercial Vehicles, Electric Vehicles, Luxury Vehicles, SUVs), Vehicle Class (Light-Duty Vehicles, Heavy-Duty Vehicles, Two-Wheelers, Three-Wheelers), Distribution Channel (OEMs, Aftermarket, Tier 1 Suppliers), and Geography (Turkey, Egypt, United Arab Emirates, Saudi Arabia, Israel, Others)

Pricing

Report Overview

Executive Summary

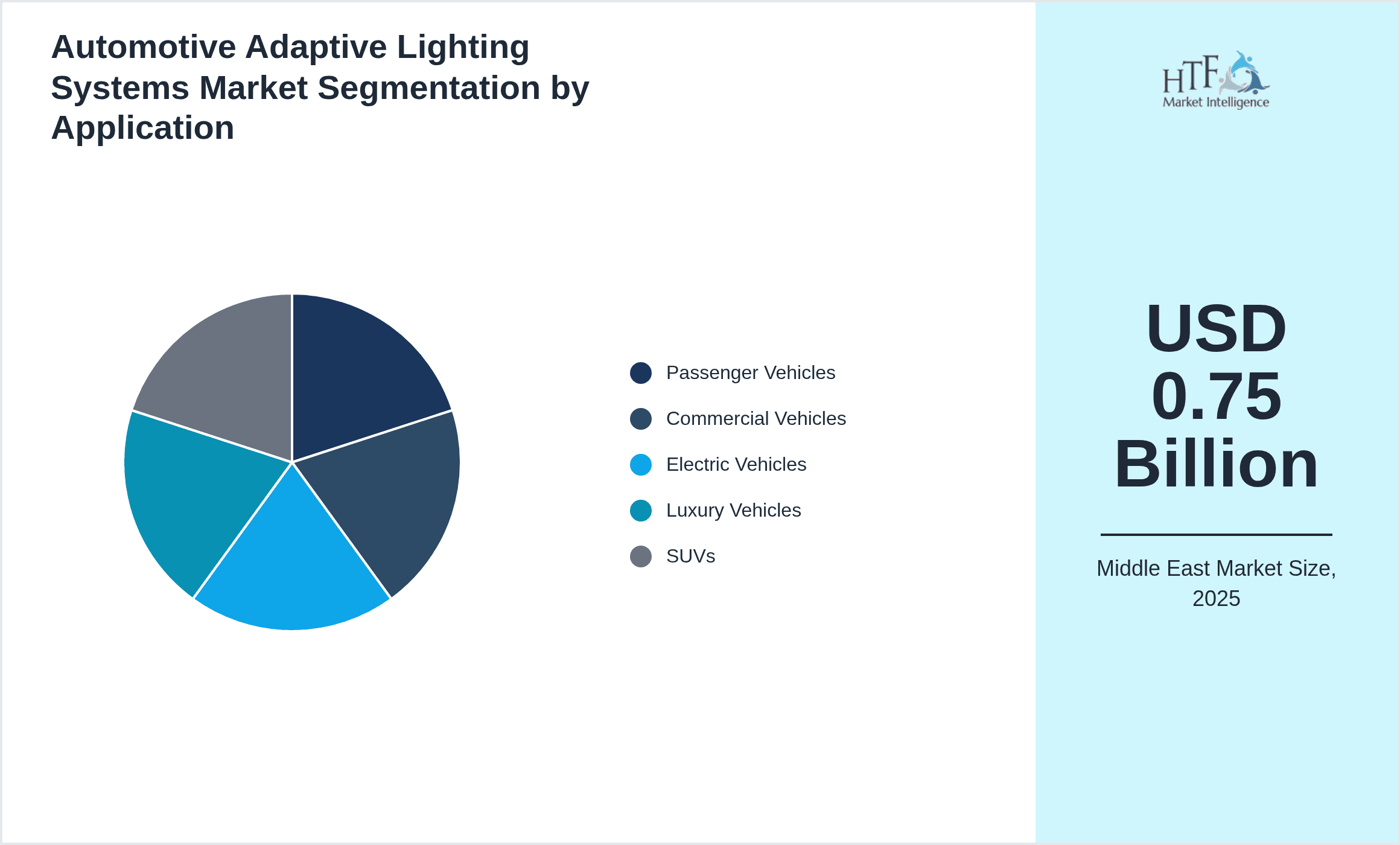

- •This market focuses on automotive adaptive lighting systems in the Middle East, covering product types like LED, HID, Laser, OLED, and Halogen adaptive lighting, primarily used in passenger and commercial vehicles, including electric and luxury segments. It excludes non-adaptive or conventional lighting systems.

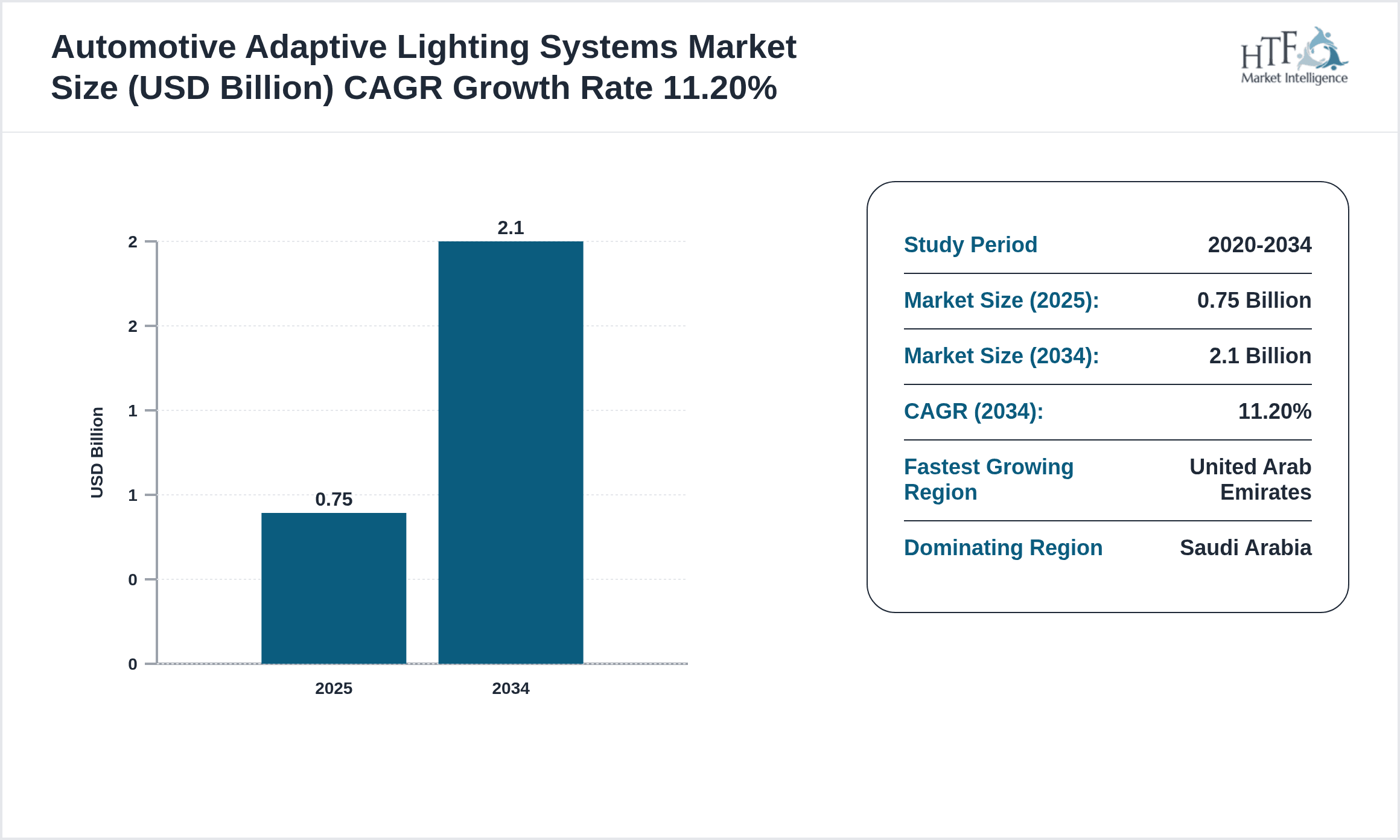

- •The market is expected to expand significantly from USD 0.75 billion in 2025 to USD 2.10 billion by 2034, driven by rising safety concerns, regulatory pushes, and growing vehicle production in the region, though adoption rates vary widely across countries and vehicle segments.

- •Adaptive lighting systems offer enhanced visibility and safety, addressing night driving challenges prevalent in different Middle Eastern terrains, while also aligning with increasing consumer demand for advanced vehicle technologies and energy-efficient lighting solutions.

Competitive Landscape

Competition in the Middle East automotive adaptive lighting systems market is fragmented with global manufacturers partnering with regional suppliers to tailor products for local conditions. Strategies revolve around technological innovation, cost optimization, and expanding aftermarket services. Pricing pressures are notable due to varying adoption rates and economic disparities across countries. Companies emphasize integration of smart sensors and AI-driven adaptive algorithms to differentiate. Distribution channels remain uneven, with luxury and electric vehicle segments showing faster uptake. Regulatory incentives and infrastructure development influence market entry and product acceptance. Regional competition is shaped by government fleet modernization programs and rising demand for premium vehicles. Future competitive trends suggest increased collaboration, focus on lightweight materials, and enhanced connectivity features in lighting systems.

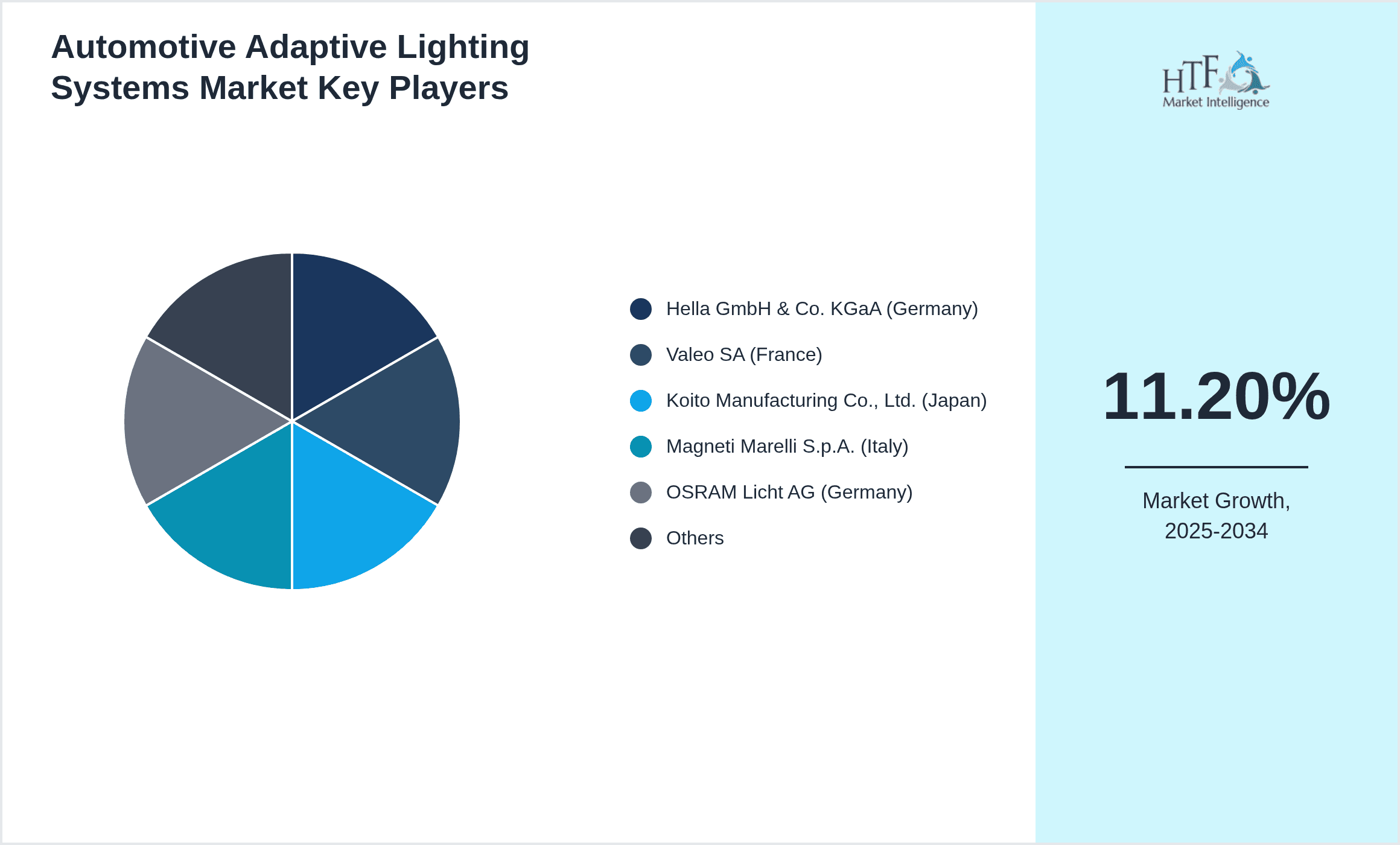

Leading Companies in Middle East Automotive Adaptive Lighting Systems Market

- •Hella GmbH & Co. KGaA (Germany)

- •Valeo SA (France)

- •Koito Manufacturing Co., Ltd. (Japan)

- •Magneti Marelli S.p.A. (Italy)

- •OSRAM Licht AG (Germany)

- •Stanley Electric Co., Ltd. (Japan)

- •Lumileds Holding B.V. (Netherlands)

- •Varroc Lighting Systems (India)

- •ZF Friedrichshafen AG (Germany)

- •Auto Lite Co. (Middle East)

- •Al Jomaih Automotive Company (Saudi Arabia)

- •Al Masaood Group (UAE)

- •Nasser Bin Khaled Automobiles (Qatar)

- •Kuwait Automotive Lighting Solutions (Kuwait)

- •Oman Auto Lighting Technologies (Oman)

Market Breakdown

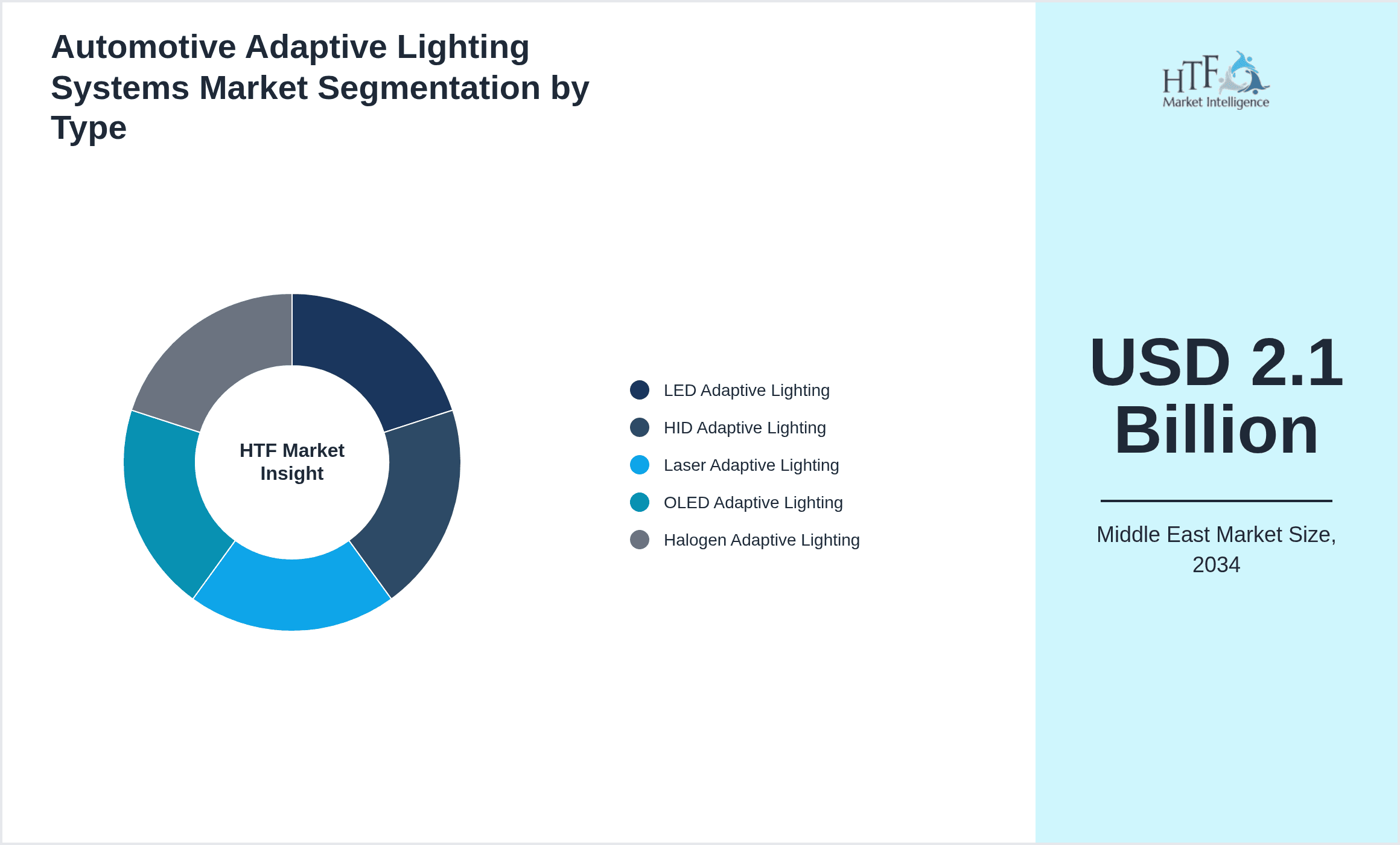

- •By Type

- ◦LED Adaptive Lighting

- ◦HID Adaptive Lighting

- ◦Laser Adaptive Lighting

- ◦OLED Adaptive Lighting

- ◦Halogen Adaptive Lighting

- •By Application

- ◦Passenger Vehicles

- ◦Commercial Vehicles

- ◦Electric Vehicles

- ◦Luxury Vehicles

- ◦SUVs

- •By Vehicle Class

- ◦Light-Duty Vehicles

- ◦Heavy-Duty Vehicles

- ◦Two-Wheelers

- ◦Three-Wheelers

- •By Distribution Channel

- ◦OEMs

- ◦Aftermarket

- ◦Tier 1 Suppliers

Growth Dynamics

The Middle East market growth is mainly driven by increasing safety awareness among consumers and governments focusing on road safety improvements. The rise in luxury and electric vehicle sales also fuels demand for advanced lighting. Despite this, adoption is uneven, with wealthier countries like UAE and Saudi Arabia leading, while others lag due to cost sensitivity and infrastructure gaps. The regulatory push for better lighting standards is accelerating uptake but not uniformly. Manufacturers are innovating with LED and laser technologies to reduce energy consumption, which is critical given regional climate challenges. However, economic fluctuations and geopolitical tensions sometimes slow investments, causing unpredictable growth spurts.

Market Trends

There is a steady shift towards LED adaptive lighting due to its energy efficiency and customizable beam patterns. Laser lighting, although promising, faces slower adoption owing to higher costs and limited regional awareness. Integration with driver assistance systems is emerging, though not widespread yet. Interestingly, some fleet operators delay upgrading lighting systems despite clear safety benefits, often due to upfront costs or unclear ROI. Electrification of vehicles prompts more advanced lighting systems to improve range efficiency. Some markets show preference for OEM solutions, while others rely heavily on aftermarket replacements, indicating fragmented consumer behavior.

Market Opportunities

Untapped potential exists in commercial vehicle lighting upgrades, especially in logistics-heavy countries. The rise of electric vehicles in affluent Middle Eastern markets offers a niche for ultra-efficient adaptive lighting. Governments’ increasing focus on smart city initiatives may create demand for connected lighting systems integrated with vehicle-to-infrastructure communication. Aftermarket growth is another opportunity, as many vehicles currently use outdated lighting. Partnerships between global tech companies and local players could accelerate adoption and customization for regional conditions. Moreover, environmental regulations pushing for energy-efficient solutions open avenues for innovation.

Market Challenges

Cost remains a significant barrier, especially in less affluent Middle Eastern countries, limiting widespread adoption of high-end adaptive lighting. The lack of standardization across countries creates hurdles for manufacturers and suppliers. Infrastructure to support smart adaptive systems is uneven, and consumer awareness is patchy, with some drivers indifferent to lighting upgrades. Technical complexity and integration with existing vehicle electronics pose challenges for aftermarket suppliers. Additionally, geopolitical instability in parts of the region occasionally disrupts supply chains and delays market growth. Regulatory enforcement varies, causing uncertainty in compliance and slowing uniform adoption.

Market Entropy

The Middle East automotive adaptive lighting market exhibits irregular patterns, with adoption rates fluctuating sharply between countries and even within vehicle segments. While premium segments show steady growth, mass-market vehicles adapt slowly. The interplay of economic volatility, inconsistent regulatory enforcement, and cultural differences leads to unpredictable demand. Some countries push rapidly for modernization while others show inertia. The aftermarket channel’s growth is patchy, with urban areas more receptive than rural ones. Supply chain disruptions due to regional tensions add to market instability. Innovation cycles are uneven; some players introduce cutting-edge tech that fails to gain traction widely. Overall, the market resembles a patchwork rather than a smooth growth trajectory.

Merger & Acquisition News

Regional Analysis

Saudi Arabia dominates the market due to its large automotive fleet, government initiatives promoting vehicle safety, and higher consumer purchasing power. The UAE is the fastest growing country, driven by rapid electric vehicle adoption and luxury car ownership increase. Qatar and Kuwait show moderate growth linked to infrastructure development and rising commercial vehicle fleets. Oman is slower but exhibits potential due to increasing road transport activities. Economic diversification efforts and infrastructure investments across the Gulf Cooperation Council countries influence the market unevenly, with adoption rates varying based on local policies and market maturity. Cultural factors and urbanization also shape demand patterns.

Regulatory Landscape

Between 2020 and 2025, several Middle Eastern countries introduced vehicle lighting standards aligning more closely with UNECE regulations, mandating adaptive lighting systems for new vehicles. Saudi Arabia implemented stricter road safety laws requiring improved visibility features, driving OEM compliance. The UAE enforced regulations incentivizing energy-efficient lighting to support sustainability goals. However, regulatory enforcement remains inconsistent across countries, causing patchy market influence. Some nations lack comprehensive automotive lighting policies, leading to fragmented adoption. Import policies and certification requirements impact the entry of advanced lighting systems. Government programs promoting vehicle modernization indirectly encourage adaptive lighting uptake but often lack specific mandates.

Investment and Funding Scenario

Recent years show limited dedicated public or private funding focused solely on automotive adaptive lighting in the Middle East. However, investments in broader automotive technology and smart mobility projects indirectly benefit the sector. Some leading companies have increased R&D spending targeting regional adaptation of lighting technologies. Venture capital interest in automotive tech startups is growing, though primarily centered around EVs and autonomous driving rather than lighting specifically. Government grants supporting energy-efficient vehicle components provide some financial incentives. The overall funding landscape is fragmented, with most investments funneled through multinational corporations rather than local startups or SMEs.

Competitive Innovation Radar

Innovation centers on integrating adaptive lighting with sensor-driven safety systems and connectivity features. Companies develop AI-enabled beam adjustment algorithms to improve night driving safety in diverse Middle Eastern environments. LED and laser technologies are evolving rapidly to meet energy efficiency and design flexibility demands. Local players focus on customizing solutions to address harsh climate conditions like high temperatures and dust. Partnerships between global lighting tech firms and regional automotive suppliers aim to accelerate technology transfer. Yet, market fragmentation and inconsistent regulations slow widespread innovation adoption. There is also a noticeable gap between OEM offerings and aftermarket solutions in terms of technological sophistication.

Market Size & Growth Table for Middle East Automotive Adaptive Lighting Systems

- •2020 Market Size: USD 0.45 Billion

- •2025 Market Size: USD 0.75 Billion

- •2034 Market Size: USD 2.10 Billion

- •Compound Annual Growth Rate (CAGR): 11.2%

- •Year-on-Year Growth: 11.0%

Regional Performance Analysis

- •Dominating Country: Saudi Arabia

- •Fastest Growing Country: United Arab Emirates

Players List of Middle East Automotive Adaptive Lighting Systems with Head Quarter Operating in Middle East Market

- •Auto Lite Co. (Middle East)

- •Al Jomaih Automotive Company (Saudi Arabia)

- •Al Masaood Group (UAE)

- •Nasser Bin Khaled Automobiles (Qatar)

- •Kuwait Automotive Lighting Solutions (Kuwait)

- •Oman Auto Lighting Technologies (Oman)

Competitive Analysis

The competitive environment in Middle East automotive adaptive lighting is marked by a mix of global giants and regional firms. Global players leverage advanced technologies and scale but sometimes struggle with local customization. Regional companies benefit from market knowledge and relationships but face challenges in R&D and capital. Pricing and product differentiation are key battlegrounds, with innovation around laser and AI-based adaptive systems gaining traction. The aftermarket segment remains underdeveloped, offering growth potential but also operational challenges. Collaboration between OEMs and suppliers is evolving, aiming to balance cost, quality, and technology. Market entry barriers include regulatory uncertainty and infrastructure gaps, impacting new entrants. Despite these challenges, competition is intensifying as demand for safer and more efficient lighting grows.

Regional Outlook

The Saudi Arabia currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Turkey

- Egypt

- United Arab Emirates

- Saudi Arabia

- Israel

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.75 Billion |

| Forecast Year Market Size | USD 2.1 Billion |

| CAGR | 11.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11% |

| Scope of Report | Market is segmented by Type (LED Adaptive Lighting, HID Adaptive Lighting, Laser Adaptive Lighting, OLED Adaptive Lighting, Halogen Adaptive Lighting), Application (Passenger Vehicles, Commercial Vehicles, Electric Vehicles, Luxury Vehicles, SUVs), Vehicle Class (Light-Duty Vehicles, Heavy-Duty Vehicles, Two-Wheelers, Three-Wheelers), Distribution Channel (OEMs, Aftermarket, Tier 1 Suppliers) |

| Regions Covered | Turkey, Egypt, United Arab Emirates, Saudi Arabia, Israel, Others |

| Key Companies | Hella GmbH & Co. KGaA (Germany), Valeo SA (France), Koito Manufacturing Co., Ltd. (Japan), Magneti Marelli S.p.A. (Italy), OSRAM Licht AG (Germany) |

Middle East Automotive Adaptive Lighting Systems Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.