Europe Auto Glass Market Size, Growth & Revenue 2024-2034

Europe Auto Glass Market is segmented by Type (Laminated Glass, Tempered Glass, Insulated Glass, Coated Glass, Others), Application (Passenger Vehicles, Commercial Vehicles, Specialty Vehicles, Aftermarket Services, OEM), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Market Definition & Scope

So, the Europe Auto Glass market, it's basically about all types of glass used in vehicles — that includes the usual laminated stuff, tempered panes, and also some insulated or coated types. It’s not just car windows, but also windshield glass, back windows, and sometimes even specialty applications in commercial vehicles. The market covers everything from original equipment manufacturing to aftermarket repairs, which is quite important because glass replacement happens a lot in Europe, but not evenly everywhere. Some countries lean more on OEM while others have a thriving aftermarket scene. Technologies like UV protection coatings or embedded sensors are gaining traction, but adoption varies with vehicle types and regions. And there’s a bit of a mess with regulations sometimes overlapping or differing across European countries, which impacts how products are developed and sold here. All in all, it’s a patchwork market with steady growth but many small quirks to watch.

Market Segmentation

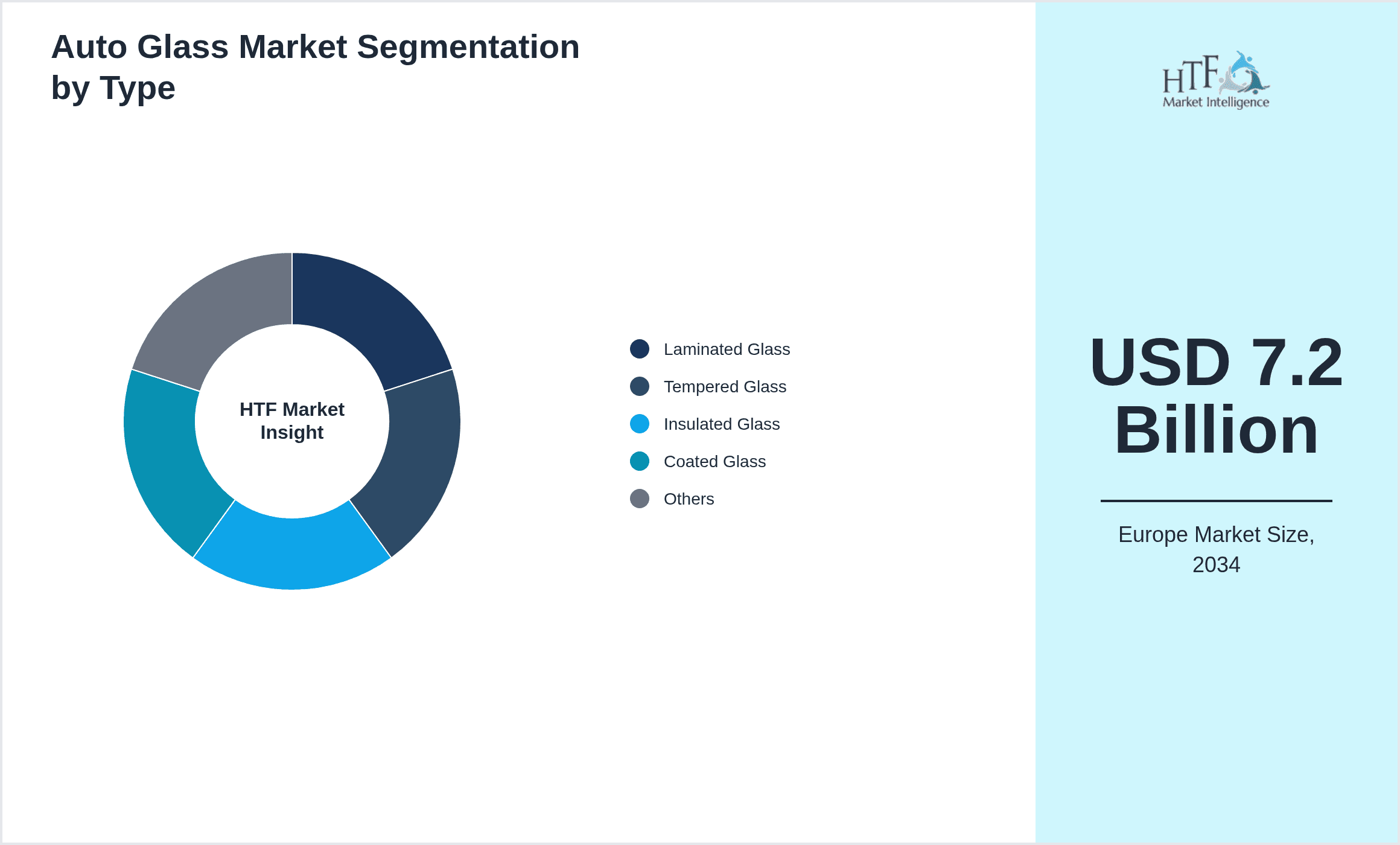

- •By Type

- ◦Laminated Glass

- ◦Tempered Glass

- ◦Insulated Glass

- ◦Coated Glass

- ◦Others

- •By Application

- ◦Passenger Vehicles

- ◦Commercial Vehicles

- ◦Specialty Vehicles

- ◦Aftermarket Services

- ◦OEM

- •By Distribution Channel

- ◦OEM Supply

- ◦Aftermarket Retail

- ◦Direct to Fleet Operators

- ◦Online Platforms

- •By Technology

- ◦UV Protection Coatings

- ◦Acoustic Glass

- ◦Smart Glass with Sensors

- ◦Heated Glass

Leading Companies in Europe Auto Glass Market

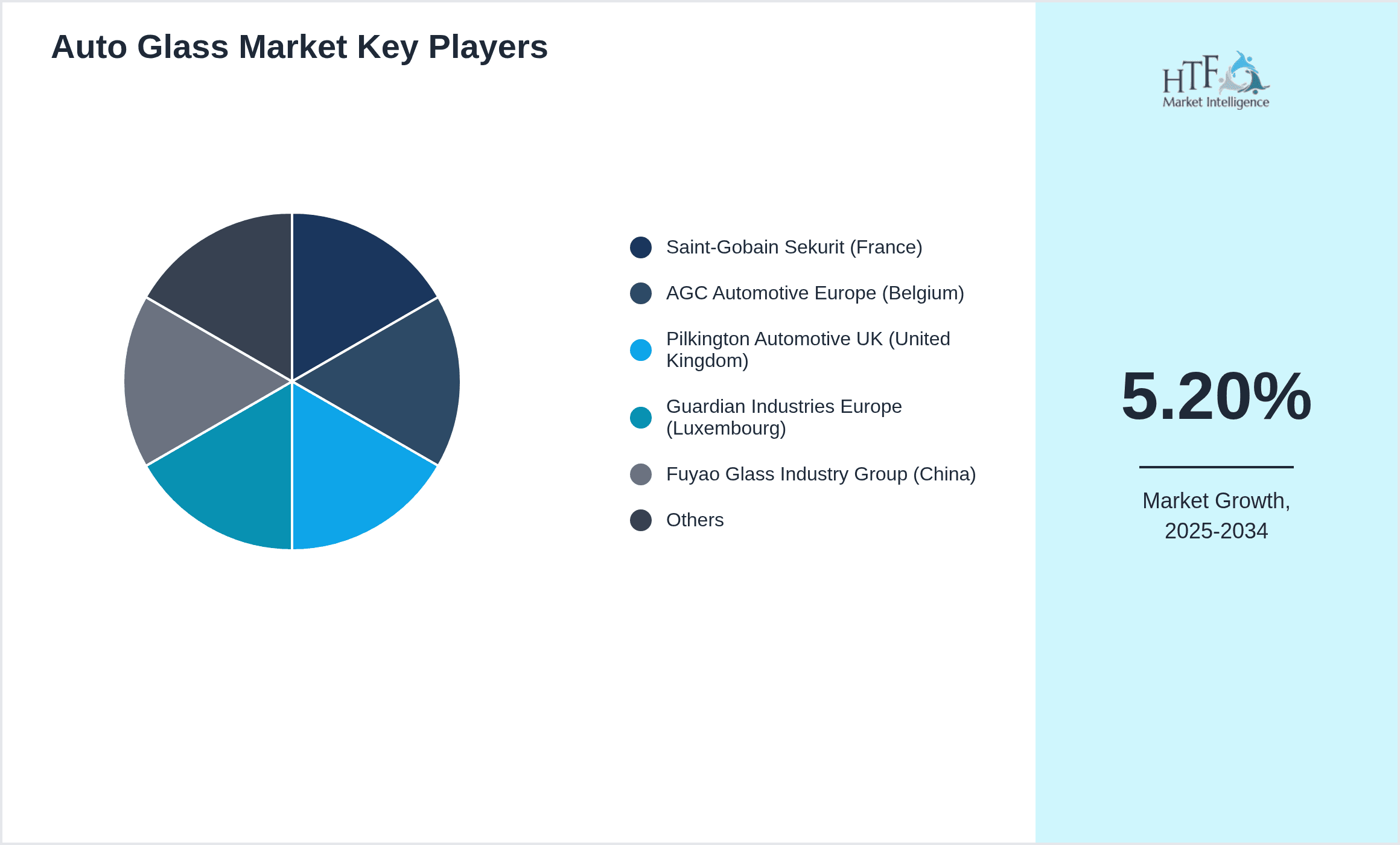

- •Saint-Gobain Sekurit (France)

- •AGC Automotive Europe (Belgium)

- •Pilkington Automotive UK (United Kingdom)

- •Guardian Industries Europe (Luxembourg)

- •Fuyao Glass Industry Group (China)

- •PGW Auto Glass Europe (France)

- •Interpane Glasindustrie GmbH (Germany)

- •Xinyi Automotive Glass Europe (Belgium)

- •Carlex Glass Europe (Poland)

- •AGP Group (Italy)

- •Securit Industries (France)

- •Pilkington Group Ltd (United Kingdom)

- •European Glass Group (Germany)

- •Saint-Gobain Glass Polska (Poland)

- •Guardian Glass Deutschland (Germany)

- •AGC Flat Glass Europe (Belgium)

- •Fuyao Europe GmbH (Germany)

- •Saint-Gobain Autover (France)

- •Pilkington Italia (Italy)

- •Interpane Austria GmbH (Austria)

- •Xinyi Solar Europe (Germany)

- •Carlex Europe S.A. (Poland)

- •AGP Automotive Italia (Italy)

- •Securit Automotive GmbH (Germany)

- •Guardian Automotive Poland (Poland)

Growth Drivers

- •Rising demand for passenger vehicles in emerging European markets is fueling the need for advanced auto glass solutions, especially laminated and coated variants that enhance safety and aesthetics.

- •Stricter safety regulations across Europe are pushing automakers and suppliers to adopt higher-quality, impact-resistant glass, which boosts market growth but creates uneven adoption in less regulated countries.

- •Growing preference for electric and autonomous vehicles leads to demand for smart glass technologies integrated with sensors and displays, though rollout is slower than expected due to cost concerns.

- •Expanding aftermarket repair and replacement services, particularly after the pandemic disruptions, have increased regional glass replacement frequency but vary significantly by country and vehicle segment.

- •Technological advances such as acoustic and heated glass are gradually gaining traction, enhancing passenger comfort and safety, although adoption remains patchy across different vehicle classes.

Market Trends

- •Integration of heads-up displays (HUD) in laminated windshields is becoming more common, with manufacturers experimenting, yet consumer uptake is inconsistent due to pricing and tech familiarity gaps.

- •Sustainability concerns are pushing suppliers to develop eco-friendly glass manufacturing with recycled materials, though the transition pace varies widely among European producers.

- •Aftermarket services are increasingly leveraging digital platforms for ordering and installation scheduling, but regional digital infrastructure disparities slow uniform adoption.

- •Increased cross-border collaborations among European auto glass suppliers aim to standardize quality and reduce costs, but regulatory fragmentation still complicates full harmonization.

- •Rising urbanization encourages use of acoustic glass to reduce noise pollution in vehicles, yet effectiveness varies with installation quality and local environmental factors.

Restraints

- •High cost of advanced glass technologies limits penetration in budget vehicle segments and some Eastern European markets where price sensitivity remains high.

- •Fragmented regulatory environment across Europe causes delays and increased compliance costs for manufacturers trying to standardize products region-wide.

- •Supply chain disruptions impacting raw materials like specialty glass components have led to intermittent production halts and increased lead times.

- •Reluctance among certain fleet operators to upgrade to newer glass technologies due to perceived return-on-investment uncertainties slows market expansion.

- •Lack of skilled labor in several regions causes inconsistent installation quality, impacting customer satisfaction and market reputation.

Opportunities

- •Rising adoption of electric vehicles in Western Europe opens opportunities for specialized auto glass with integrated battery management sensors and enhanced thermal insulation.

- •Growth in automotive aftermarket digital platforms can be leveraged to expand reach and improve customer engagement, especially in less penetrated Eastern European markets.

- •Increasing demand for customization in luxury and specialty vehicles creates space for premium coated and smart glass products tailored to niche segments.

- •Potential to expand into retrofit solutions for older vehicles with advanced glass technologies offers a new revenue stream, although consumer awareness is still limited.

- •Collaboration with automotive OEMs on next-gen autonomous vehicle glass integrating multiple sensors presents long-term growth prospects despite current adoption lags.

Challenges

- •Navigating the complex and sometimes conflicting regulatory landscapes across European countries poses significant challenges for product approvals and market entry.

- •Technological fragmentation where different manufacturers adopt varying standards for smart glass integration complicates interoperability and aftermarket services.

- •Volatile raw material prices and geopolitical tensions contribute to unpredictable supply costs, affecting pricing strategies and profitability.

- •Consumer hesitation toward advanced auto glass technologies due to lack of perceived immediate benefit limits demand growth in certain segments.

- •Intense competition from low-cost glass producers outside Europe pressures margins and forces continuous innovation to maintain market share.

Industry Insights

In March 2024, Saint-Gobain Sekurit unveiled a new laminated glass product featuring integrated solar control and acoustic dampening layers designed for electric vehicles, aiming to boost energy efficiency and passenger comfort. The move targets Western European EV markets where such innovations are increasingly sought. Meanwhile, in November 2023, AGC Automotive Europe launched a smart windshield equipped with built-in sensors for driver assistance systems, signaling a push toward connected car technologies despite uneven adoption among OEMs. These developments reflect a market gradually shifting toward smarter, multifunctional glass, although uptake remains uneven across countries and vehicle segments.

Regulatory Overview

Europe’s auto glass market is shaped by evolving safety standards like the UNECE Regulation 43 revisions, which tightened requirements for laminated and tempered glass in vehicles from 2020 to 2024. These standards mandate enhanced impact resistance and optical clarity, pushing manufacturers to innovate. Additionally, environmental directives encourage use of recyclable materials and limit hazardous substances in glass production, influencing manufacturing processes. Compliance across multiple European countries remains complex due to differing enforcement timelines, with some nations adopting stricter national rules alongside EU-wide regulations, impacting market entry strategies and product development.

Competitive Landscape

Competition in the Europe Auto Glass market is intense, with well-established players holding significant shares but constantly challenged by emerging suppliers and technological entrants. Market leaders often compete on innovation, especially in smart glass and coatings, but also on cost efficiency due to price sensitivity in various segments. Strategic partnerships between OEMs and glass manufacturers are common, securing supply chains and fostering collaborative R&D. However, regional fragmentation and regulatory hurdles create barriers for new entrants. Rivalry also centers on aftermarket services, with companies expanding digital platforms for customer reach. Overall, the market shows a mix of consolidation and niche specialization as firms jockey to balance innovation with affordability.

Mergers & Acquisitions

- •In July 2023, Fuyao Glass Industry Group expanded its European footprint by acquiring a majority stake in Carlex Glass Europe, a Polish-based specialist in automotive glass coatings and smart glass technologies. This strategic move enhances Fuyao’s product portfolio and strengthens its presence in Eastern Europe, targeting growing demand for advanced glass solutions. The acquisition also aims to integrate Carlex’s R&D capabilities with Fuyao’s manufacturing scale, positioning the combined entity to better serve both OEM and aftermarket segments across the region.

- •In January 2025, Saint-Gobain Sekurit completed its acquisition of Guardian Automotive Poland, consolidating its position in Central and Eastern Europe. This deal expands Saint-Gobain’s manufacturing capacity and distribution network, enabling quicker response times and broader product offerings. The integration is expected to streamline operations and enhance innovation pipelines, focusing on next-generation laminated and acoustic glass products tailored for European automotive trends, including electrification and autonomous driving support.

Recent Industry News

- •On 12th February 2025, AGC Automotive Europe announced a partnership with a leading European electric vehicle manufacturer to co-develop smart windshields featuring embedded augmented reality displays. This collaboration aims to enhance driver experience by integrating navigation and safety alerts directly into the windshield. The initiative marks a significant step toward connected vehicle ecosystems, with pilot vehicles expected on European roads by late 2026. Source: AGC Official Press Release.

- •On 5th March 2025, Pilkington Automotive UK launched a new line of heated laminated glass designed specifically for cold climate regions in Northern Europe. The product promises faster defrosting times and improved safety during winter months, addressing a common consumer pain point. Early adoption by fleet operators in Scandinavia has been encouraging, though wider market penetration is pending further validation. Source: Pilkington Corporate News.

- •On 20th April 2025, Saint-Gobain Sekurit opened a new state-of-the-art manufacturing facility in BeNeLux focused on producing coated and acoustic glass. The plant incorporates advanced automation and eco-friendly processes, aiming to reduce carbon footprint while increasing output. This expansion responds to growing demand in Western Europe for premium auto glass products and supports Saint-Gobain’s sustainability goals. Source: Saint-Gobain Press Release.

- •On 15th January 2025, Fuyao Glass Industry Group expanded its aftermarket glass distribution network in Germany through a strategic alliance with regional service providers. This move enhances availability and reduces delivery times for replacement glass, catering to rising repair volumes post-pandemic. The alliance also incorporates digital ordering systems to streamline customer experience, though integration challenges remain in some locales. Source: Fuyao Industry Report.

Market Statistics

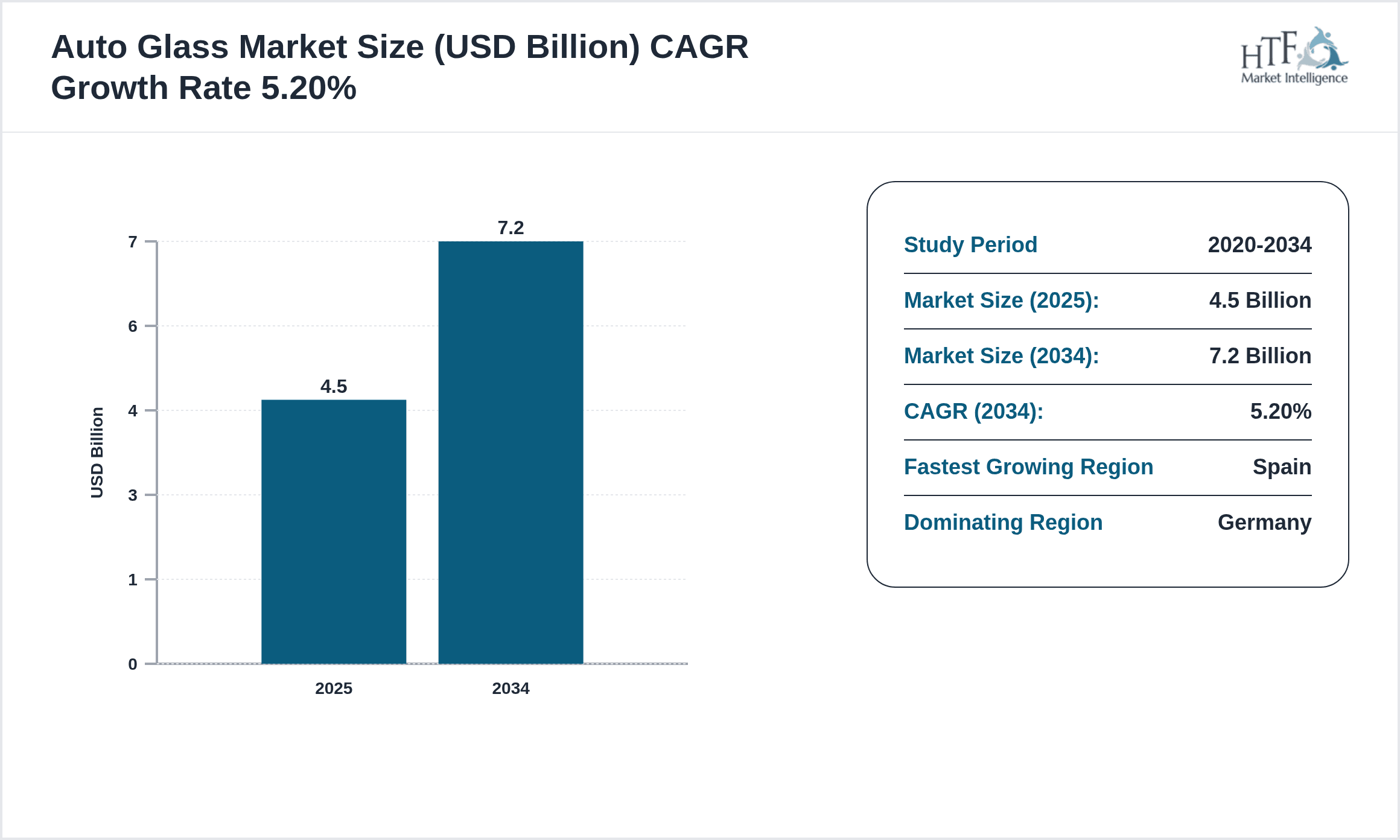

- •CAGR by 2034: 5.2%

- •Market Size by 2034: USD 7.2 Billion

- •Market Size in 2025: USD 4.7 Billion

- •Dominating Type: Laminated Glass

- •Next-Following Type: Tempered Glass

- •Dominating Application: Passenger Vehicles

- •Next-Following Application: Commercial Vehicles

- •Dominating Region: Germany

- •Second-Leading Region: France

- •Region with Highest Growth Rate: Spain

- •Dominating Country: Germany

Market Share Table

- •Market Share (%) of Dominating vs Followed Type

- ◦Laminated Glass: 45%

- ◦Tempered Glass: 30%

- •Market Share (%) of Dominating vs Followed Application

- ◦Passenger Vehicles: 55%

- ◦Commercial Vehicles: 25%

- •Growth Rate (%) of Dominating vs Followed Type

- ◦Laminated Glass: 5.0%

- ◦Tempered Glass: 4.1%

- •Growth Rate (%) of Dominating vs Followed Application

- ◦Passenger Vehicles: 5.5%

- ◦Commercial Vehicles: 4.2%

Top 5 Global Players

- •Saint-Gobain Sekurit (France)

- •AGC Automotive Europe (Belgium)

- •Pilkington Automotive UK (United Kingdom)

- •Guardian Industries Europe (Luxembourg)

- •Fuyao Glass Industry Group (China)

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Spain is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.5 Billion |

| Forecast Year Market Size | USD 7.2 Billion |

| CAGR | 5.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 5.1% |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Saint-Gobain Sekurit (France), AGC Automotive Europe (Belgium), Pilkington Automotive UK (United Kingdom), Guardian Industries Europe (Luxembourg), Fuyao Glass Industry Group (China), PGW Auto Glass Europe (France), Interpane Glasindustrie GmbH (Germany), Xinyi Automotive Glass Europe (Belgium), Carlex Glass Europe (Poland), AGP Group (Italy), Securit Industries (France), Pilkington Group Ltd (United Kingdom), European Glass Group (Germany), Saint-Gobain Glass Polska (Poland), Guardian Glass Deutschland (Germany), AGC Flat Glass Europe (Belgium), Fuyao Europe GmbH (Germany), Saint-Gobain Autover (France), Pilkington Italia (Italy), Interpane Austria GmbH (Austria), Xinyi Solar Europe (Germany), Carlex Europe S.A. (Poland), AGP Automotive Italia (Italy), Securit Automotive GmbH (Germany), Guardian Automotive Poland (Poland) |

Europe Auto Glass Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.