GCC Smectite Clays Market - Middle East Size & Outlook 2025-2034

GCC Smectite Clays Market is segmented by Type (Montmorillonite, Nontronite, Beidellite, Saponite, Hectorite), Application (Oil & Gas Drilling, Environmental Remediation, Cosmetics & Personal Care, Agriculture, Construction), End-User Industry (Petroleum Extraction Companies, Environmental Agencies, Cosmetic Manufacturers, Farming Operations, Building Contractors), Distribution Channel (Direct Sales, Distributors, Online Platforms), and Geography (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates)

Pricing

Report Overview

Executive Summary

- •The GCC Smectite Clays Market involves mining and supply of natural smectite clays with applications varying from drilling muds in oil extraction to cosmetics and agriculture. The market includes key clay types like montmorillonite and hectorite, but other non-smectite clays are excluded. The industry is somewhat fragmented with uneven demand across GCC countries, influenced significantly by fluctuating oil sector investments and environmental policies. Supply inconsistencies and regional variations in clay quality also shape market dynamics.

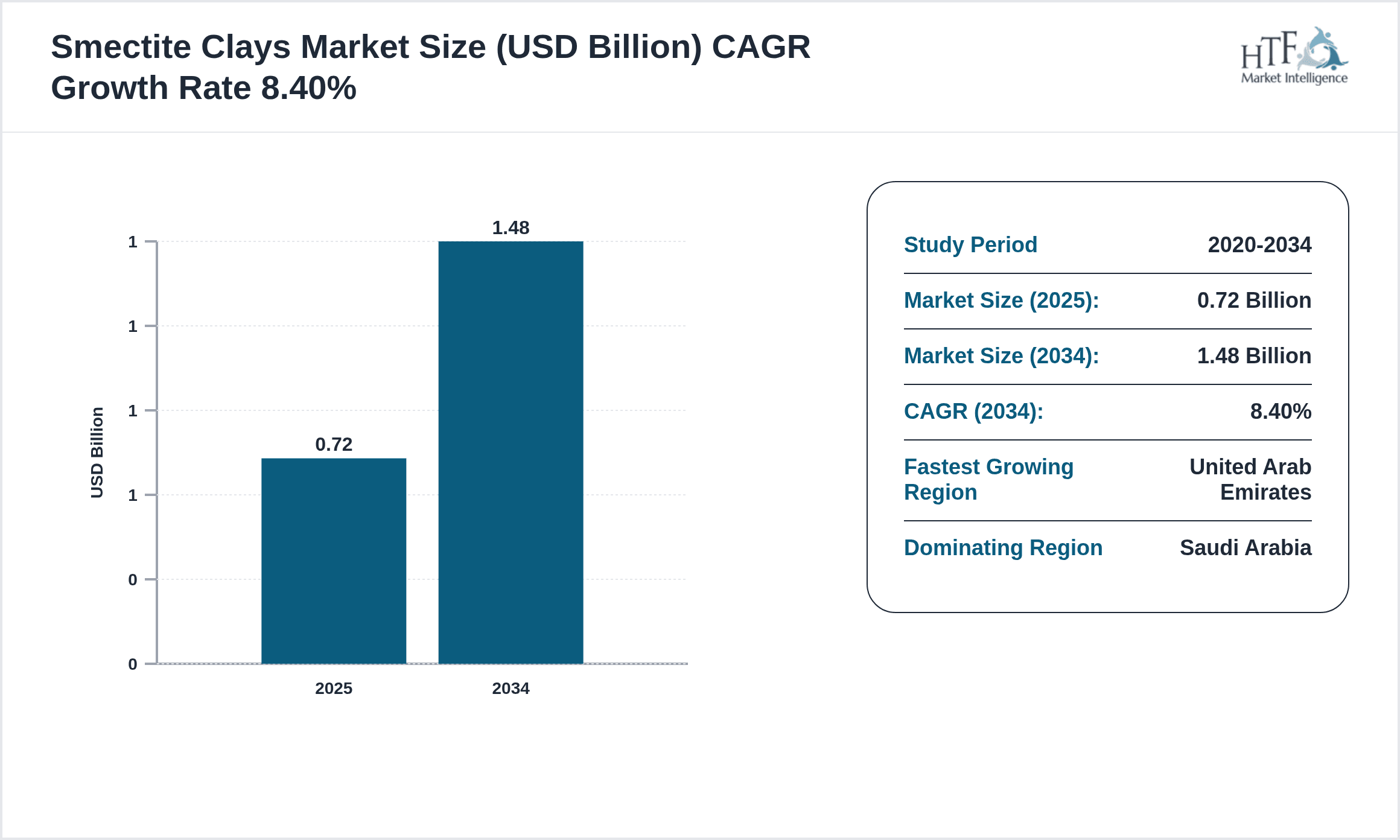

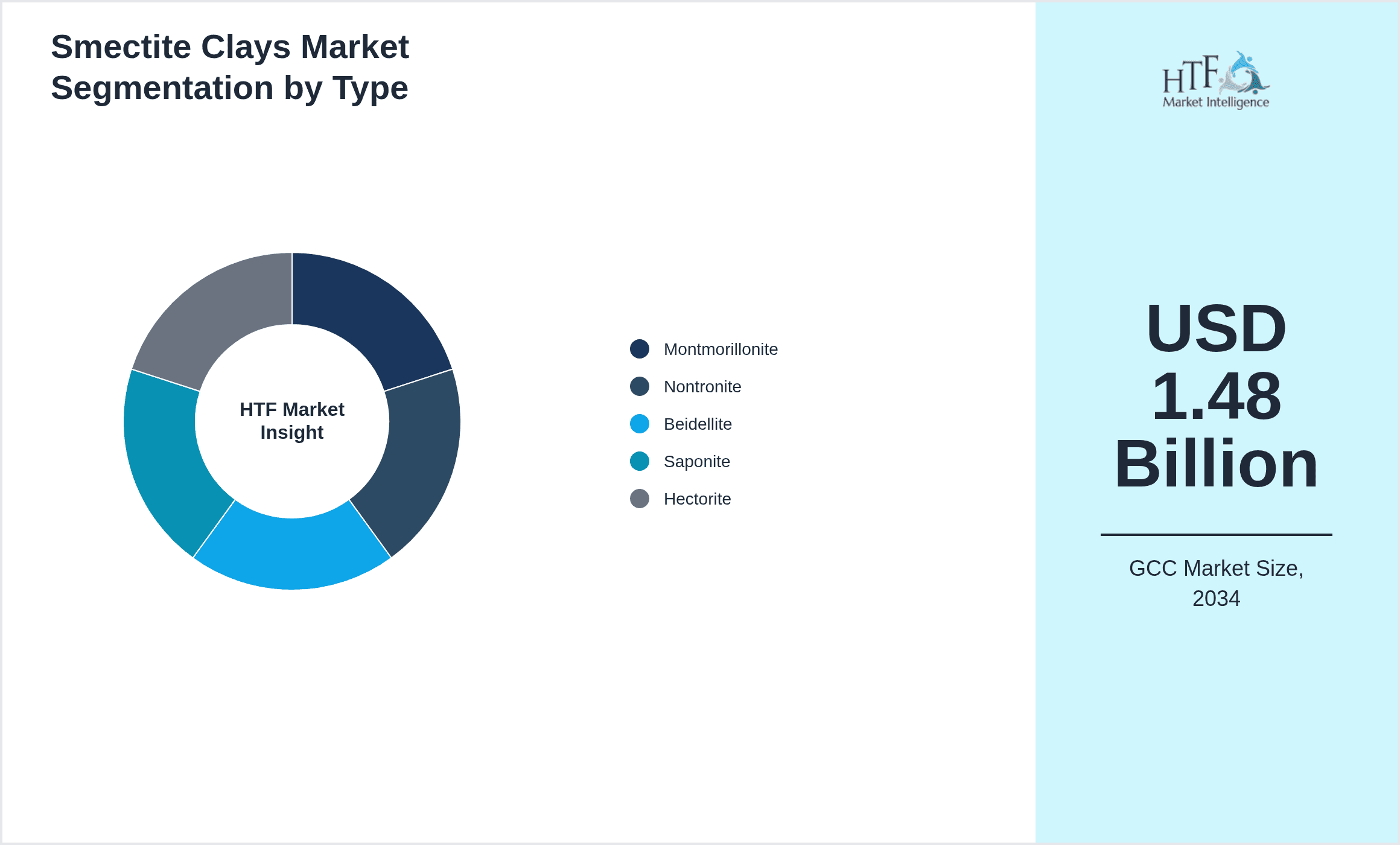

- •Key highlights include a base market size of USD 0.72 Billion in 2025 projected to almost double by 2034 at a CAGR of 8.4%. Saudi Arabia leads the market share due to its oil and construction sectors, while the UAE shows fastest growth driven by environmental remediation and cosmetic applications. Montmorillonite dominates product usage but hectorite gains faster adoption owing to its specialty applications.

- •The market's value proposition lies in the multifunctional nature of smectite clays, serving critical roles in high-value industries. This versatility creates strategic importance, but practical challenges like inconsistent raw material quality and regulatory complexities temper growth prospects. Stakeholders from mining companies to end-users in drilling and cosmetics must navigate these nuances in GCC’s unique economic and environmental landscape.

Competitive Landscape

Competition in the GCC Smectite Clays market is moderately concentrated among a handful of regional and international players. The market players often compete on supply reliability and customized product formulations rather than just price. Innovation is mostly incremental, focusing on enhancing clay purity and tailoring particle size distribution to end-use needs, especially in oil drilling and cosmetics. Rivalry intensifies around securing long-term contracts with oil companies and expanding downstream partnerships in construction and agriculture. While global suppliers occasionally enter the GCC market, local producers leverage proximity and regulatory familiarity to maintain advantage. Barriers include limited high-quality clay reserves and the complexity of logistics across GCC nations. Future competition may see increased collaboration between clay miners and technology providers for advanced clay processing solutions.

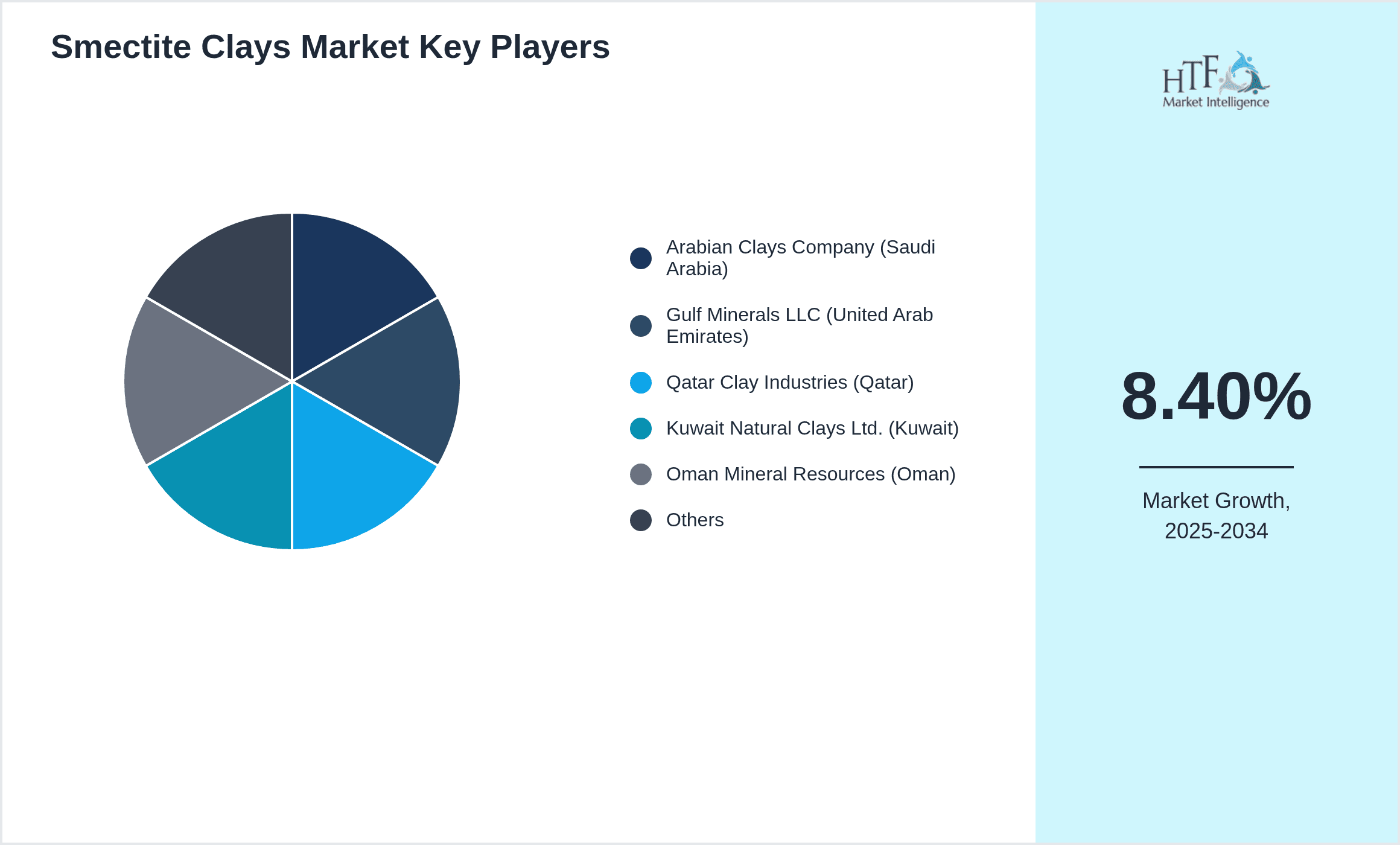

Leading Companies in GCC Smectite Clays Market

- •Arabian Clays Company (Saudi Arabia)

- •Gulf Minerals LLC (United Arab Emirates)

- •Qatar Clay Industries (Qatar)

- •Kuwait Natural Clays Ltd. (Kuwait)

- •Oman Mineral Resources (Oman)

- •Middle East Clay Group (UAE)

- •Desert Earth Mining (Saudi Arabia)

- •Al Jazeera Clays (Qatar)

- •Khor Minerals (Kuwait)

- •Sahara Clay Works (Oman)

- •Emirates Clay Corporation (UAE)

- •Riyadh Industrial Minerals (Saudi Arabia)

- •Dunes Clay Industries (UAE)

- •Fujairah Minerals (UAE)

- •Al Khobar Clay Enterprises (Saudi Arabia)

- •Zain Clay Solutions (Kuwait)

- •Oasis Clay Products (Oman)

- •Al Ain Clay Suppliers (UAE)

- •Bahrain Clay Co. (Bahrain)

- •Al Dhafra Clay Industries (UAE)

Market Breakdown

- •By Type

- ◦Montmorillonite

- ◦Nontronite

- ◦Beidellite

- ◦Saponite

- ◦Hectorite

- •By Application

- ◦Oil & Gas Drilling

- ◦Environmental Remediation

- ◦Cosmetics & Personal Care

- ◦Agriculture

- ◦Construction

- •By End-User Industry

- ◦Petroleum Extraction Companies

- ◦Environmental Agencies

- ◦Cosmetic Manufacturers

- ◦Farming Operations

- ◦Building Contractors

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

Growth Dynamics

- •Growth Drivers

- ◦The GCC market benefits heavily from ongoing oil & gas exploration activities, where smectite clays, especially montmorillonite, are crucial as drilling mud components. Despite fluctuations in oil prices, regional investments continue, sustaining demand. Additionally, increasing environmental regulations pushing for soil and water remediation boost clay usage. The cosmetics sector's growth in GCC, particularly in UAE and Saudi Arabia, also propels demand, as natural clays gain popularity for skin care. Infrastructure development catalyzes construction applications, adding to market momentum. However, demand can be inconsistent, sometimes tied oddly to shifts in geopolitical factors affecting regional projects.

- •Trends

- ◦A noticeable trend is rising interest in specialty smectite clays like hectorite for high-end cosmetics and pharmaceuticals, driven by consumer preferences for natural ingredients. Environmental remediation projects increasingly adopt smectite clays for pollutant adsorption but face challenges from variable clay quality across GCC sites. Digitization in supply chain management is emerging but unevenly implemented, causing logistical inefficiencies. Also, some smaller players experiment with blending smectite with synthetic alternatives, though adoption remains limited. Regional initiatives focusing on sustainability sometimes conflict with traditional mining practices, creating an inconsistent market rhythm.

- •Restraints

- ◦Key restraints include the uneven distribution of high-grade smectite clay deposits within GCC countries, which complicates consistent supply. Regulatory hurdles around mining permits and environmental impact assessments can delay projects, especially in Saudi Arabia and Kuwait. Price volatility linked to global commodity markets affects profitability. Moreover, adoption in newer applications like agriculture is slower than expected, partly due to lack of localized research proving efficacy. Infrastructure gaps and transport challenges across some GCC regions introduce logistical bottlenecks. These factors collectively restrain rapid market expansion despite underlying demand.

- •Opportunities

- ◦Opportunities arise from expanding environmental remediation projects, especially with GCC countries increasing focus on sustainable development goals. Developing tailored smectite clay products for cosmetics to meet rising GCC consumer demand for organic and natural products is promising. Technological advancements in clay processing can improve product quality and open new applications in pharmaceuticals. Growing construction activity, driven by urbanization and mega projects like NEOM in Saudi Arabia, creates demand for clay-based additives. Strategic partnerships between clay producers and end-users may unlock innovation and market penetration. However, some opportunities depend on overcoming supply chain inconsistencies.

- •Challenges

- ◦Challenges include managing environmental concerns linked to mining activities that face growing scrutiny in GCC countries. The market also grapples with inconsistent demand patterns across sectors; oil & gas demand swings impact overall stability. Quality variation in local clay deposits demands additional processing, increasing costs. Competition from imported clays and synthetic substitutes pressures pricing. Regulatory compliance complexities differ country-wise, adding operational burdens. Furthermore, limited R&D investment in understanding smectite clay potentials in agriculture and cosmetics slows innovation adoption. Addressing infrastructure gaps and improving supply chain efficiency remain ongoing hurdles.

Industry Insights

The GCC smectite clays market shows interesting shifts with increasing emphasis on sustainability. For instance, in March 2024, Gulf Minerals LLC launched a new high-purity montmorillonite product tailored for environmentally friendly drilling fluids, aiming to reduce ecological footprints in oil extraction. This move aligns with regional regulatory tightening around drilling waste management. Also, in November 2023, Arabian Clays Company introduced a cosmetic-grade hectorite clay blend designed for premium skincare brands targeting GCC consumers who favor natural ingredients. These launches reflect growing diversification beyond traditional oil sector uses and highlight innovation driven by local market preferences and regulations.

Regulatory Overview

From 2020 to 2025, GCC countries have progressively strengthened mining and environmental regulations impacting smectite clay extraction. Saudi Arabia implemented stricter permitting processes in 2023, requiring comprehensive environmental impact assessments before mining approvals. The UAE updated waste disposal standards in 2024, pushing for eco-friendly drilling mud components, indirectly boosting demand for high-quality smectite clays. Qatar introduced new soil remediation guidelines in 2022, mandating use of natural absorbents like smectite clays in certain industrial sites. These evolving regulations increase compliance costs but encourage adoption of purified and specialty clays, shaping market supply and product development strategies.

Mergers & Acquisitions

- •In July 2024, Gulf Minerals LLC completed acquisition of Desert Earth Mining, a Saudi Arabia-based smectite clay supplier specializing in montmorillonite. This deal expanded Gulf Minerals' footprint across Saudi regional zones and enhanced its product portfolio with advanced beneficiation capabilities. The acquisition aimed at consolidating supply chains and improving logistics, addressing inconsistencies previously challenging in the GCC market. Post-merger, Gulf Minerals is expected to leverage Desert Earth’s existing client relationships in oil & gas and construction sectors, streamlining product delivery and innovation efforts within the GCC.

- •In January 2025, Arabian Clays Company entered a strategic merger with Al Jazeera Clays of Qatar, consolidating their operations to strengthen market presence in environmental remediation and cosmetic applications. The merger allowed combined R&D resources to develop specialty smectite blends tailored for GCC consumer demands, particularly focusing on sustainability and quality improvements. This move also aimed to mitigate supply volatility through shared mining assets across Qatar and Saudi Arabia, improving resilience against regional regulatory challenges and market fluctuations.

Recent Industry News

- •15th February 2025, Gulf Minerals LLC announced a strategic partnership with NEOM Construction Authority to supply montmorillonite-based additives for upcoming mega infrastructure projects in Saudi Arabia. This collaboration includes joint research on improving clay properties for sustainable construction materials, aiming to align with NEOM’s green city objectives. The initiative reflects growing integration of smectite clays into advanced building solutions in the GCC. Source: Gulf Minerals Press Release

- •10th April 2025, Arabian Clays Company launched a new eco-certified hectorite clay product line targeting cosmetic manufacturers in the UAE. The launch emphasized natural ingredient sourcing and compliance with emerging GCC cosmetic regulations, meeting rising demand for organic skincare. Initial market response indicated strong interest from regional premium brands. Source: Arabian Clays Official Website

- •8th June 2025, Khor Minerals of Kuwait expanded its smectite clay mining operations with new extraction facilities to increase supply for environmental remediation projects across GCC industrial zones. The expansion aims to support stricter pollution control mandates enacted in recent years and addresses previous supply-demand mismatches. Source: Khor Minerals Industry Bulletin

- •22nd August 2025, Middle East Clay Group signed a distribution agreement with a leading European clay processor to introduce advanced smectite clay blends in GCC markets, focusing on high-performance drilling muds and agricultural soil conditioners. This marks a significant step in product diversification and technology transfer within the region. Source: Middle East Clay Group News Release

Market Statistics

- •CAGR by 2034: 8.4%

- •Market Size by 2034: USD 1.48 Billion

- •Market Size in 2025: USD 0.72 Billion

- •Dominating Type: Montmorillonite

- •Next-Following Type: Hectorite

- •Dominating Application: Oil & Gas Drilling

- •Next-Following Application: Environmental Remediation

- •Dominating Region: Saudi Arabia

- •Second-Leading Region with Highest Growth Rate: United Arab Emirates

- •Dominating Country: Saudi Arabia

Market Share Table

- •Market Share (%) of Dominating vs Followed Type

- ◦Montmorillonite: 52%

- ◦Hectorite: 21%

- •Market Share (%) of Dominating vs Followed Application

- ◦Oil & Gas Drilling: 44%

- ◦Environmental Remediation: 25%

- •Growth Rate (%) of Dominating vs Followed Type

- ◦Montmorillonite: 7.8%

- ◦Hectorite: 11.2%

- •Growth Rate (%) of Dominating vs Followed Application

- ◦Oil & Gas Drilling: 7.5%

- ◦Environmental Remediation: 9.0%

Top 5 Global Players

- •Gulf Minerals LLC (United Arab Emirates)

- •Arabian Clays Company (Saudi Arabia)

- •Qatar Clay Industries (Qatar)

- •Kuwait Natural Clays Ltd. (Kuwait)

- •Oman Mineral Resources (Oman)

Regional Outlook

The Saudi Arabia currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Bahrain

- Kuwait

- Oman

- Qatar

- Saudi Arabia

- United Arab Emirates

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.72 Billion |

| Forecast Year Market Size | USD 1.48 Billion |

| CAGR | 8.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.1% |

| Scope of Report | Market is segmented by Type (Montmorillonite, Nontronite, Beidellite, Saponite, Hectorite), Application (Oil & Gas Drilling, Environmental Remediation, Cosmetics & Personal Care, Agriculture, Construction), End-User Industry (Petroleum Extraction Companies, Environmental Agencies, Cosmetic Manufacturers, Farming Operations, Building Contractors), Distribution Channel (Direct Sales, Distributors, Online Platforms) |

| Regions Covered | Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates |

| Key Companies | Arabian Clays Company (Saudi Arabia), Gulf Minerals LLC (United Arab Emirates), Qatar Clay Industries (Qatar), Kuwait Natural Clays Ltd. (Kuwait), Oman Mineral Resources (Oman), Middle East Clay Group (UAE), Desert Earth Mining (Saudi Arabia), Al Jazeera Clays (Qatar), Khor Minerals (Kuwait), Sahara Clay Works (Oman), Emirates Clay Corporation (UAE), Riyadh Industrial Minerals (Saudi Arabia), Dunes Clay Industries (UAE), Fujairah Minerals (UAE), Al Khobar Clay Enterprises (Saudi Arabia), Zain Clay Solutions (Kuwait), Oasis Clay Products (Oman), Al Ain Clay Suppliers (UAE), Bahrain Clay Co. (Bahrain), Al Dhafra Clay Industries (UAE) |

GCC Smectite Clays Market - Middle East Size & Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.