United States Microtomes Market Size, Growth & Revenue 2025-2034

United States Microtomes Market is segmented by Application (Histopathology, Research Laboratories, Clinical Diagnostics, Forensic Labs, Educational Institutions), Type (Rotary Microtomes, Cryostats, Ultramicrotomes, Vibrating Microtomes, Disposable Microtomes), and Geography (Northeast, Southwest, The South, The Midwest)

Pricing

Report Overview

Market Definition

Microtomes are instruments used to slice tissues into thin sections for microscopic examination. In the US, this market covers rotary microtomes, cryostats for frozen samples, ultramicrotomes for electron microscopy, vibrating microtomes, and disposable blade microtomes. They find applications in histopathology labs, clinical diagnostics, research centers, forensic investigations, and educational institutions. This equipment is critical in preparing samples for disease diagnosis, drug research, and forensic analysis, but adoption varies widely depending on lab size and budget constraints. Some smaller clinics still rely on manual or older versions, affecting uniform growth. The value chain includes manufacturers, distributors, consumable suppliers, and service providers who maintain equipment. While advanced technologies like automation and digital integration are emerging, many users still prefer traditional methods citing cost and training challenges. Market scope is narrow but essential for medical research and diagnostics in the US healthcare ecosystem.

Drivers

- •Increasing demand for accurate disease diagnosis in hospitals and research labs is pushing microtome sales, especially in histopathology applications.

- •Technological advancements like automated slicing and disposable blades improve efficiency and safety, encouraging replacement of older models.

- •Growing research activities in pharmaceutical and biotech sectors fuel demand for high-precision microtomes in sample preparation.

- •Rising prevalence of chronic diseases necessitates advanced diagnostic tools, indirectly boosting microtome usage.

Trends

- •Shift towards disposable blade microtomes for better hygiene and reduced cross-contamination, although some labs hesitate due to cost implications.

- •Integration of digital controls and automation in microtome design is gaining traction, but adoption is uneven across smaller clinics.

- •Cryostats remain preferred for rapid frozen section diagnosis, with steady demand in surgical pathology settings.

- •Increased focus on user safety features like blade guards and ergonomic designs is influencing purchasing decisions.

Opportunities

- •Expanding use of microtomes in forensic labs presents untapped potential due to rising demand for detailed tissue analysis in legal investigations.

- •Development of cost-effective disposable blade microtomes could open markets in smaller clinics and educational institutions.

- •Collaborations between microtome manufacturers and digital pathology companies offer scope for integrated diagnostic solutions.

- •Increasing government funding for biomedical research boosts procurement of advanced microtomes in academic and research labs.

Challenges

- •High cost of advanced microtomes limits adoption in smaller healthcare facilities and regional labs, leading to market fragmentation.

- •Lack of standardized training for operating sophisticated microtomes results in underutilization and operational errors in some labs.

- •Competition from alternative sample preparation technologies sometimes reduces microtome demand in niche applications.

- •Maintenance and servicing challenges, especially in remote or less developed regions, affect equipment uptime and customer satisfaction.

Market Entropy

The US microtomes market is somewhat disjointed, with clear pockets of advanced adoption mostly in major urban and research centers, while smaller or rural labs lag behind. Cost constraints, varying training levels, and inconsistent procurement patterns contribute to this uneven landscape. Some labs cycle through equipment upgrades quickly, others maintain older models due to budget or familiarity. This inconsistency creates a patchwork demand profile that defies smooth growth trajectories. Additionally, competing diagnostic technologies sometimes pull focus away from traditional microtomes, causing fluctuations in purchase cycles. Regional disparities add complexity; for example, the West Coast and Pacific Northwest show faster modernization compared to Midwest and Southeast, where legacy equipment still dominates. The market is dynamic but lacks uniformity in user experience and technology penetration, making forecasting a bit tricky.

Merger & Acquisition News

Regional Analysis

In the United States, the West Coast dominates microtome consumption, driven by the concentration of advanced research institutions and biotech companies in California and neighboring states. The Pacific Northwest is the fastest growing sub-region, benefiting from emerging biotech hubs and increasing healthcare infrastructure investments. The Northeast and Midwest maintain stable demand, with established medical centers and universities contributing steady procurement. The Southeast and Southwest show moderate growth, although adoption rates vary widely due to economic disparities and healthcare accessibility. Regional variation is influenced by funding availability, presence of specialized labs, and local regulatory environments. Overall, growth is uneven but weighted by strong pockets of innovation and research activity, especially on the coasts.

Regulatory Landscape

- •The US Food and Drug Administration (FDA) regulates microtomes as medical devices, requiring manufacturers to comply with quality and safety standards under the Medical Device Regulation framework. Pre-market notification (510(k)) is mandatory for new products, ensuring safety and effectiveness. Compliance with Good Manufacturing Practices (GMP) is critical and regularly audited.

- •Occupational safety regulations, including those from OSHA, influence microtome design, particularly regarding blade guards and ergonomic features to reduce operator injury risk.

- •Environmental regulations impact disposal practices for used blades and consumables, prompting manufacturers to develop safer, eco-friendly disposable microtomes.

- •Regulatory updates between 2020 and 2025 have tightened documentation and reporting requirements, increasing compliance costs but improving traceability and market trust.

Investment and Funding Scenario

- •Since 2025, there has been moderate but steady investment flowing into microtome manufacturing startups focusing on automation and disposable blade technology, supported by venture capital and government grants aimed at medical device innovation.

- •Large established players continue to allocate R&D budgets toward enhancing precision and safety features, reflecting steady internal funding rather than external investment influx.

Competitive Innovation Radar

- •Innovation in the US microtomes market centers around automation and user safety enhancements. Some companies have introduced digital control systems that allow for programmable slicing thickness and automated blade advancement, reducing user error. Disposable microtomes with integrated blade disposal mechanisms are gaining traction, especially in clinical environments focused on infection control.

- •Despite these advances, many labs still use traditional manual microtomes due to cost sensitivity and resistance to change. This creates a split market where high-end and basic products coexist. Manufacturers face the challenge of balancing innovation with affordability. Additionally, partnerships between microtome makers and digital pathology firms are emerging, aiming to streamline sample prep and analysis workflows, but these remain in early stages.

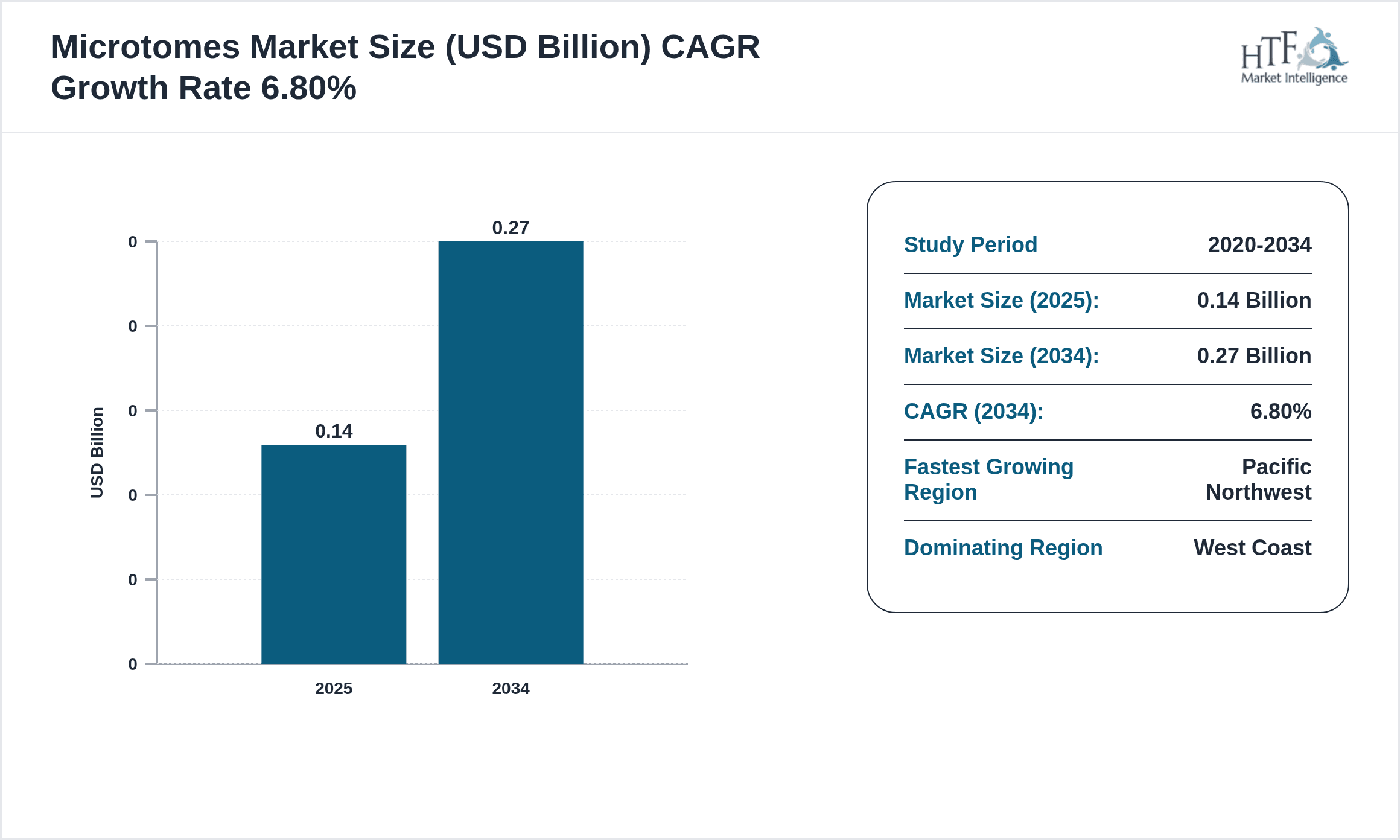

Market Size & Growth Table of United States Microtomes

- •Base Year Market Size: USD 145 Million

- •Historical Year Market Size (2020): USD 102 Million

- •Forecast Year Market Size (2034): USD 265 Million

- •Compound Annual Growth Rate (CAGR): 6.8%

- •Year-on-Year Growth: 6.6%

Regional Performance Analysis

- •Dominating Region: West Coast

- •Fastest Growing Region: Pacific Northwest

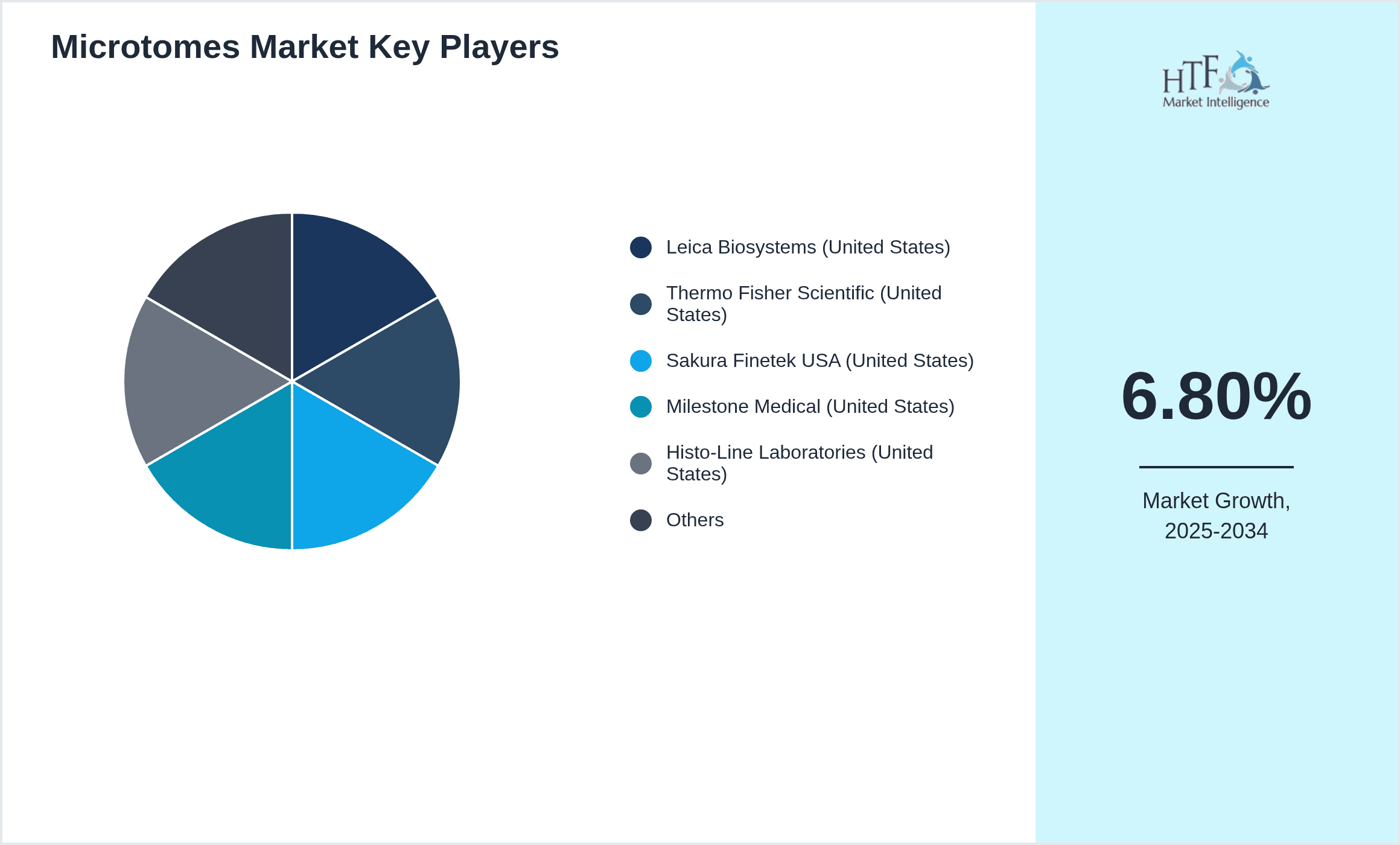

Players List

- •Leica Biosystems (United States)

- •Thermo Fisher Scientific (United States)

- •Sakura Finetek USA (United States)

- •Milestone Medical (United States)

- •Histo-Line Laboratories (United States)

- •FEI Company (United States)

- •Electron Microscopy Sciences (United States)

- •DiagnoPath (United States)

- •Richard-Allan Scientific (United States)

- •Ted Pella (United States)

Competitive Analysis

The US microtomes market is characterized by a blend of established multinational companies and specialized domestic manufacturers. Competitive dynamics revolve around technological innovation, product reliability, and after-sales service quality. Market leaders invest heavily in R&D to introduce automation, safety features, and disposable blade technologies, while smaller players focus on niche segments or cost-effective solutions. Pricing strategies vary, with premium brands commanding higher prices justified by advanced features. Distribution channels include direct sales to hospitals and labs, partnerships with medical equipment distributors, and online platforms. Strategic collaborations with digital pathology firms are nascent but gaining importance. Market entry barriers include stringent FDA regulations and the need for technical expertise. Regional preferences and budget constraints fragment the market, fostering competition across multiple levels. Future competition will likely intensify around integration with digital diagnostics and expanding into underpenetrated regional sub-markets.

Regional Outlook

The West Coast currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Pacific Northwest is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Northeast

- Southwest

- The South

- The Midwest

| Feature | Details |

|---|---|

| Base Year Market Size | USD 145 Million |

| Forecast Year Market Size | USD 265 Million |

| CAGR | 6.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6.6% |

| Regions Covered | Northeast, Southwest, The South, The Midwest |

| Key Companies | Leica Biosystems (United States), Thermo Fisher Scientific (United States), Sakura Finetek USA (United States), Milestone Medical (United States), Histo-Line Laboratories (United States), FEI Company (United States), Electron Microscopy Sciences (United States), DiagnoPath (United States), Richard-Allan Scientific (United States), Ted Pella (United States) |

United States Microtomes Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.