Fly Ash Cement Market - Middle East Size & Outlook 2025-2034

Middle East Fly Ash Cement Market is segmented by Type (Class F Fly Ash Cement, Class C Fly Ash Cement, Blended Cement, Portland Pozzolana Cement), Application (Infrastructure, Residential Construction, Commercial Construction, Industrial Facilities, Roadways), End User (Government Projects, Private Developers, Industrial Sector, Real Estate Companies), Distribution Channel (Direct Sales, Distributors, Retail Outlets, Online Platforms), and Geography (Turkey, Egypt, United Arab Emirates, Saudi Arabia, Israel, Others)

Pricing

Report Overview

Executive Summary

- •So, the Middle East Fly Ash Cement market is basically about cement that uses fly ash—a byproduct from coal plants—as a key ingredient. It’s not just one type of cement, but several like Class F, Class C, and blends that mix fly ash with other materials. The idea is to reduce reliance on traditional cement, which is heavy on carbon emissions, and instead use waste material that can improve strength and durability. This market covers countries like Saudi Arabia, UAE, and others where construction is booming but adoption rates vary quite a bit. Some places are quick to use fly ash cement for infrastructure, while others lag due to supply inconsistencies or lack of standards. So, it's a mixed bag with interesting push and pull factors, shaped by environmental concerns and practical construction needs.

- •The market has been growing steadily but not always in a straight line. Growth is driven by urbanization, government green initiatives, and rising infrastructure projects. Yet, the uptake is uneven—some regions see faster adoption because of better regulations or incentives. The use of blended cement is picking up pace especially where quality fly ash supply is stable. But challenges like fluctuating raw material availability and lack of uniform standards sometimes slow things down. Overall, the market is expected to nearly double in size by 2034, with a CAGR around 7.8%.

- •From a value perspective, fly ash cement offers cost advantages and sustainability benefits, making it attractive to contractors and developers trying to meet green building codes. It's a niche but growing segment of the overall cement market. Strategic importance stems from the global push for lower carbon footprints and efficient resource use. Still, practical realities like logistics, variable fly ash quality, and market education create a patchy adoption landscape. This complexity makes the Middle East market particularly interesting to watch.

Competitive Landscape

Competition in the Middle East Fly Ash Cement market is somewhat fragmented but dominated by a handful of big players with strong regional presence. Companies often compete on blending technology quality, supply chain reliability, and meeting local environmental standards. Innovation is mostly incremental, focusing on enhancing fly ash cement performance and optimizing mix proportions rather than radical new tech. Rivalry is also influenced by partnerships with local suppliers and construction firms, which can lock in demand. Pricing pressure is moderate, balanced by growing demand for eco-friendly materials. New entrants face barriers like raw material sourcing and certification challenges, but the market remains attractive due to increasing green mandates and infrastructure projects.

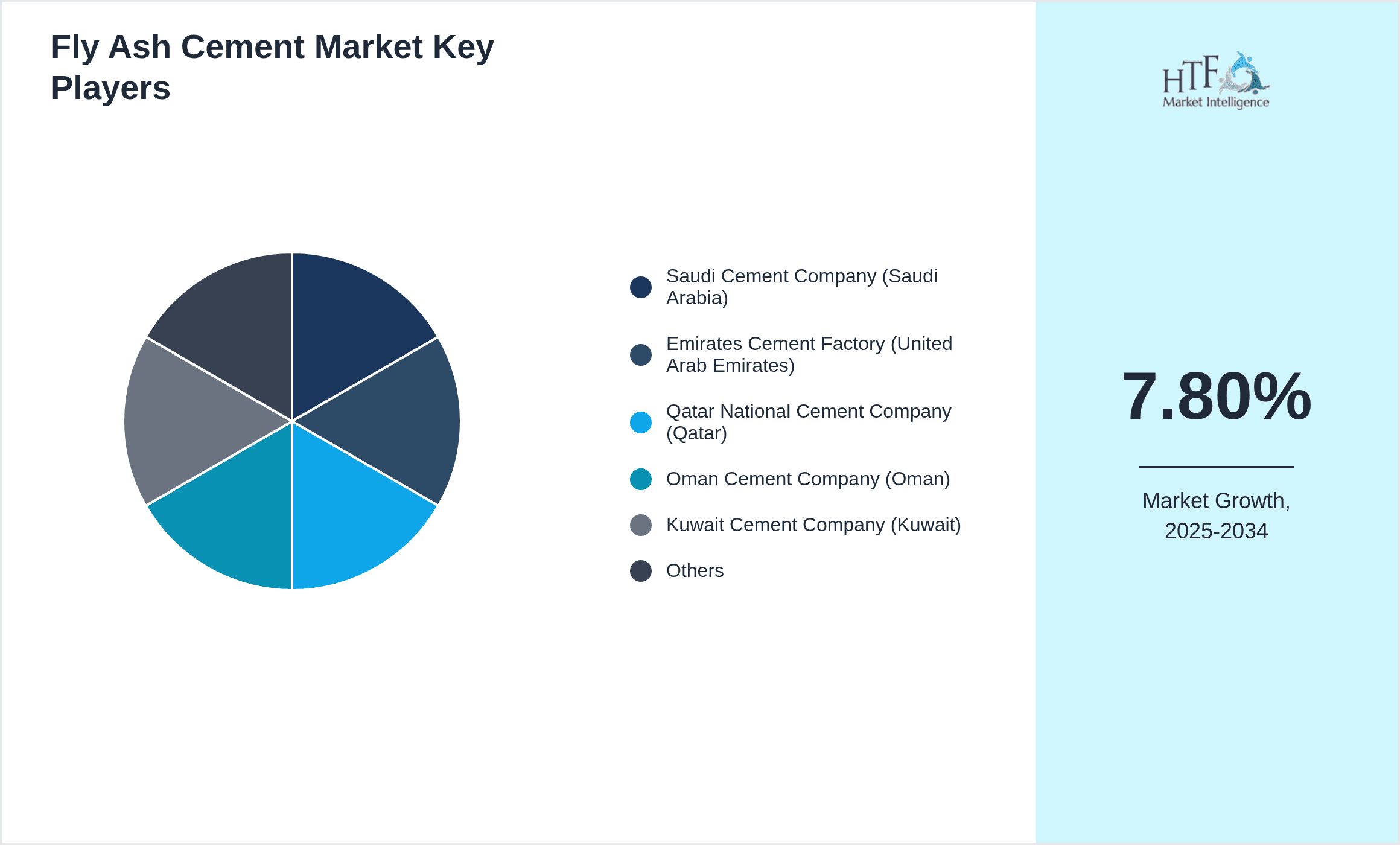

Leading Companies in Middle East Fly Ash Cement Market

- •Saudi Cement Company (Saudi Arabia)

- •Emirates Cement Factory (United Arab Emirates)

- •Qatar National Cement Company (Qatar)

- •Oman Cement Company (Oman)

- •Kuwait Cement Company (Kuwait)

- •Cemex Middle East (United Arab Emirates)

- •LafargeHolcim Middle East (United Arab Emirates)

- •Dubai Cement Factory (United Arab Emirates)

- •Yamama Cement (Saudi Arabia)

- •National Cement Company (Oman)

- •Union Cement Company (Jordan)

- •Abu Dhabi National Cement Company (UAE)

- •Riyadh Cement Company (Saudi Arabia)

- •Qassim Cement Company (Saudi Arabia)

- •Al Gharbia Cement (United Arab Emirates)

Market Breakdown

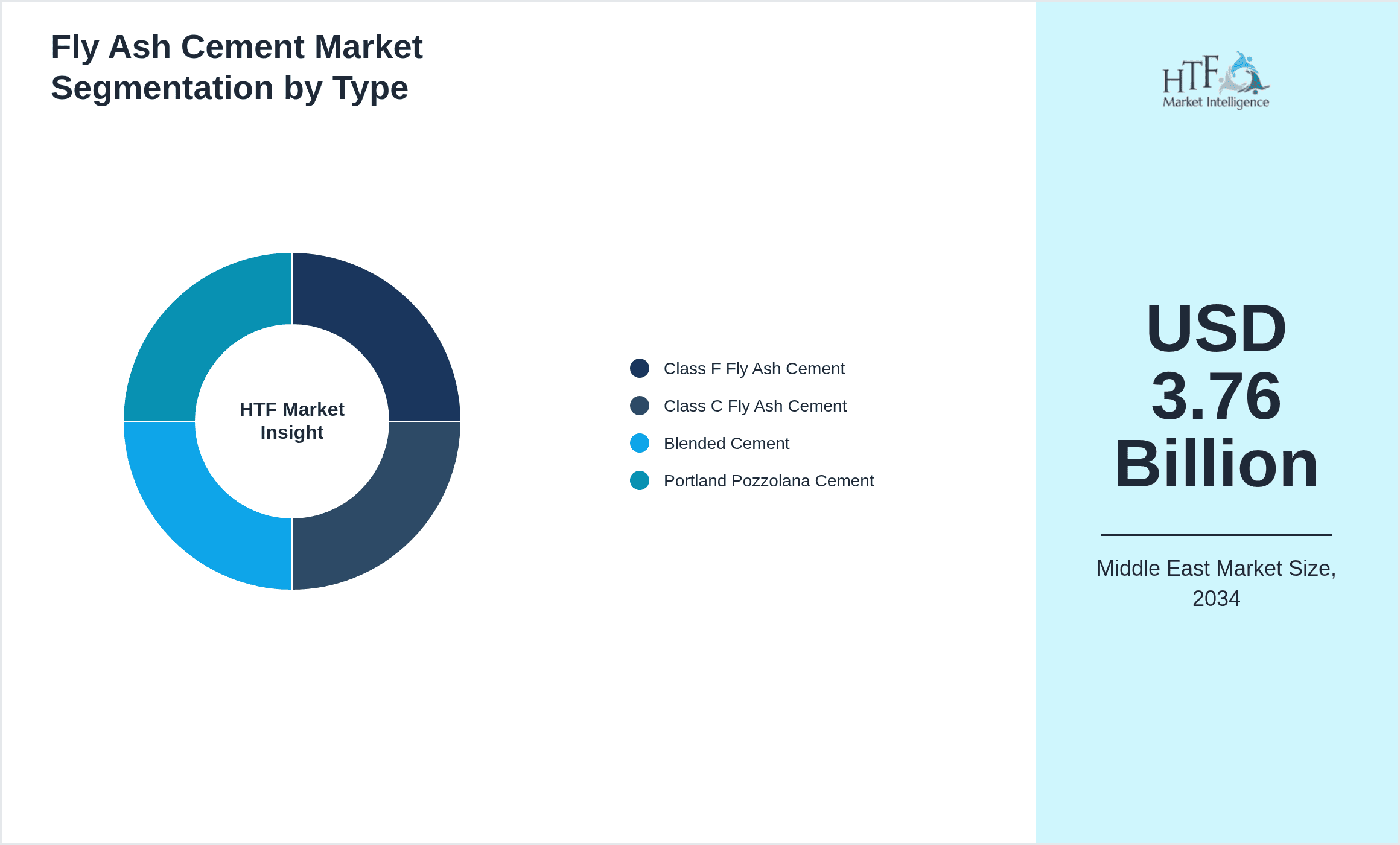

- •By Type

- ◦Class F Fly Ash Cement

- ◦Class C Fly Ash Cement

- ◦Blended Cement

- ◦Portland Pozzolana Cement

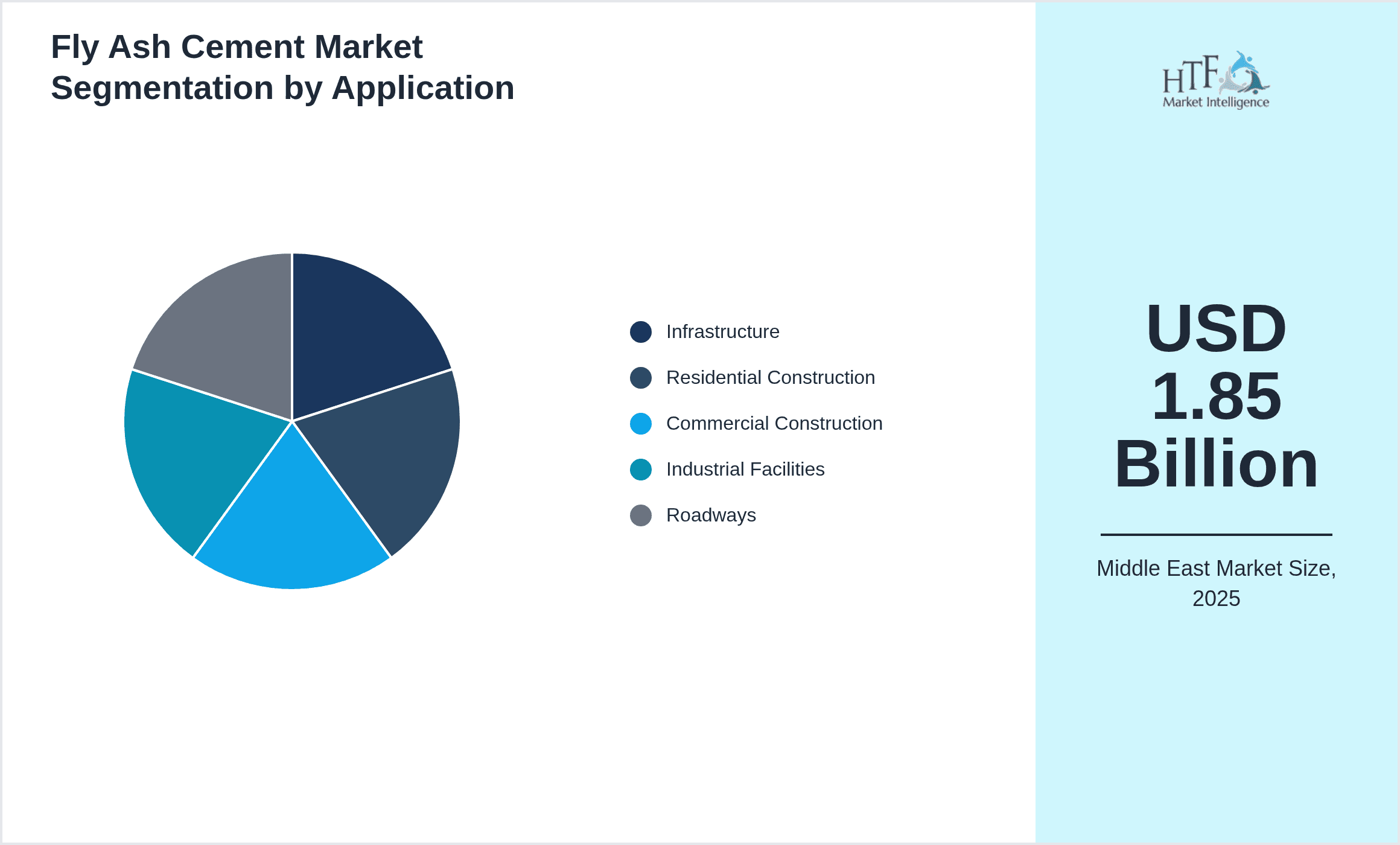

- •By Application

- ◦Infrastructure

- ◦Residential Construction

- ◦Commercial Construction

- ◦Industrial Facilities

- ◦Roadways

- •By End User

- ◦Government Projects

- ◦Private Developers

- ◦Industrial Sector

- ◦Real Estate Companies

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Retail Outlets

- ◦Online Platforms

Growth Dynamics

- •Rapid urbanization across Gulf countries fuels infrastructure and real estate demand, pushing fly ash cement adoption as a cost-effective and eco-friendly alternative, especially in large-scale projects where sustainability is a priority.

- •Government regulations promoting green building materials and emission reductions have incentivized manufacturers to incorporate higher fly ash content, stimulating the market despite some resistance in traditional construction sectors.

- •Increasing awareness among contractors about the long-term durability benefits of fly ash cement, especially for roadways and industrial facilities, is leading to gradual but steady market growth.

- •Rising costs and environmental impact concerns around conventional cement production push stakeholders towards blended cement options that reduce carbon footprint, making fly ash cement a preferred choice in the region.

- •Investment in new production technologies and enhanced fly ash processing facilities in the Middle East is improving product quality and availability, overcoming previous supply inconsistencies that limited market expansion.

Market Trends

- •Blended cement formulations are increasingly favored over pure fly ash types due to better performance in high-temperature and saline Middle Eastern environments, reflecting a shift in industry preference.

- •Digital platforms and supply chain digitization improve distribution efficiency, although some regions still face logistics bottlenecks affecting timely delivery of fly ash cement products.

- •Collaborations between cement manufacturers and government agencies on sustainable construction projects are gaining traction, promoting the use of fly ash cement in public infrastructure.

- •Despite push for sustainability, traditional Portland cement remains dominant in certain conservative markets due to familiarity and price sensitivity, slowing fly ash cement penetration.

- •Innovation focuses on improving fly ash cement curing times and strength gain to match or exceed Portland cement, aiming to reduce construction delays and increase adoption.

Market Opportunities

- •Expanding renewable energy projects in the Middle East generate fly ash as a byproduct, presenting opportunities for local sourcing and sustainable cement production integration.

- •Untapped markets in smaller Gulf Cooperation Council countries show potential for fly ash cement growth as infrastructure and housing projects increase.

- •Technological advancements in fly ash beneficiation and blending open avenues for higher-quality products that can compete with traditional cement on performance and cost.

- •Growing green building certifications and sustainability mandates across the region drive demand for eco-friendly construction materials, including fly ash cement.

- •Strategic partnerships between cement producers and construction firms could streamline supply chains and improve market penetration for fly ash cement products.

Market Challenges

- •Inconsistent quality and availability of fly ash, often dependent on coal-fired power plant operations that are limited in the Middle East, constrain consistent cement production.

- •Lack of unified regional standards for fly ash cement creates barriers for manufacturers and confuses end users, slowing adoption rates.

- •Price sensitivity among private developers limits willingness to switch from cheaper traditional cement, especially where regulatory incentives are weak or absent.

- •Technical challenges such as longer curing times and variable strength development compared to Portland cement affect contractor confidence.

- •Supply chain complexities, including transportation and storage of fly ash cement, pose logistical hurdles in certain Middle Eastern countries with less developed infrastructure.

Regulatory Framework

- •Between 2020 and 2025, several Middle Eastern governments introduced green building codes mandating minimum fly ash content in cement for public infrastructure projects, aiming to reduce carbon emissions and promote sustainability.

- •Environmental regulations now require cement manufacturers to report carbon footprints and incentivize use of supplementary cementitious materials like fly ash, increasing compliance costs but driving market adoption.

- •Standardization efforts in 2023 led to the adoption of regional quality benchmarks for fly ash cement, aligning with international norms to facilitate trade and acceptance.

- •Import tariffs on clinker and Portland cement in some Gulf countries have indirectly made fly ash cement more competitive price-wise, impacting market dynamics since 2022.

- •Government subsidies and grants for research on sustainable construction materials have supported fly ash cement innovation and pilot projects in key Middle Eastern countries.

Industry Insights

In May 2024, Saudi Cement Company unveiled a new blended cement product incorporating higher fly ash percentages aimed at infrastructure projects, emphasizing improved durability and reduced carbon footprint. This launch reflects growing environmental awareness among regional contractors and government bodies. Meanwhile, in November 2023, Emirates Cement Factory expanded its production capacity with upgraded fly ash processing technology to meet rising demand in the UAE and neighboring countries. These developments signal a strategic focus on sustainability and market responsiveness, although supply chain challenges remain a concern.

Mergers & Acquisitions

- •In August 2023, LafargeHolcim Middle East completed the acquisition of a 40% stake in Dubai Cement Factory to strengthen its foothold in the fly ash cement segment. This move aimed to leverage Dubai Cement's existing supply chains and expand sustainable product offerings across the UAE and surrounding markets. By integrating operations, LafargeHolcim sought to optimize production efficiency and accelerate innovation in eco-friendly cement solutions, addressing increasing regional demand for greener construction materials.

- •March 2024 saw Saudi Cement Company acquire a local fly ash beneficiation plant in Riyadh, enhancing its raw material sourcing capabilities. This acquisition supports the company’s strategy to secure consistent fly ash supply amid fluctuating availability in the Middle East. The move also enables greater control over product quality and cost structures, positioning Saudi Cement to capitalize on the growing demand for fly ash cement in government and private sector projects.

Recent Industry News

- •15th January 2025, Qatar National Cement Company announced a strategic partnership with a leading UAE-based construction firm to supply fly ash cement for a major infrastructure development in Doha. The collaboration aims to promote sustainable building practices and increase the use of eco-friendly cement blends in the region. This partnership is expected to boost fly ash cement demand significantly over the next five years. Source: Qatar National Cement Official Release

- •22nd March 2025, Emirates Cement Factory launched an innovative fly ash cement product designed for enhanced resistance to corrosion and high temperatures, targeting industrial facilities across the Gulf. The product utilizes advanced blending techniques to improve performance in harsh environments. Early adoption feedback from clients in Dubai and Abu Dhabi has been positive, highlighting durability gains. Source: Emirates Cement Press

- •10th May 2025, Oman Cement Company expanded its production plant capacity by 30%, incorporating new fly ash processing units to meet rising domestic and export demand. This expansion aligns with Oman’s national sustainability goals and infrastructure expansion plans. The company also plans to roll out training programs to educate contractors on fly ash cement benefits and usage. Source: Oman Cement Corporate News

- •5th July 2025, Kuwait Cement Company signed a memorandum of understanding with a European cement technology provider to implement state-of-the-art fly ash beneficiation technology. The initiative aims to improve product consistency and reduce environmental footprint, supporting Kuwait’s green construction agenda. This collaboration marks a significant step towards modernizing the region’s cement industry. Source: Kuwait Cement Official Statement

Market Statistics

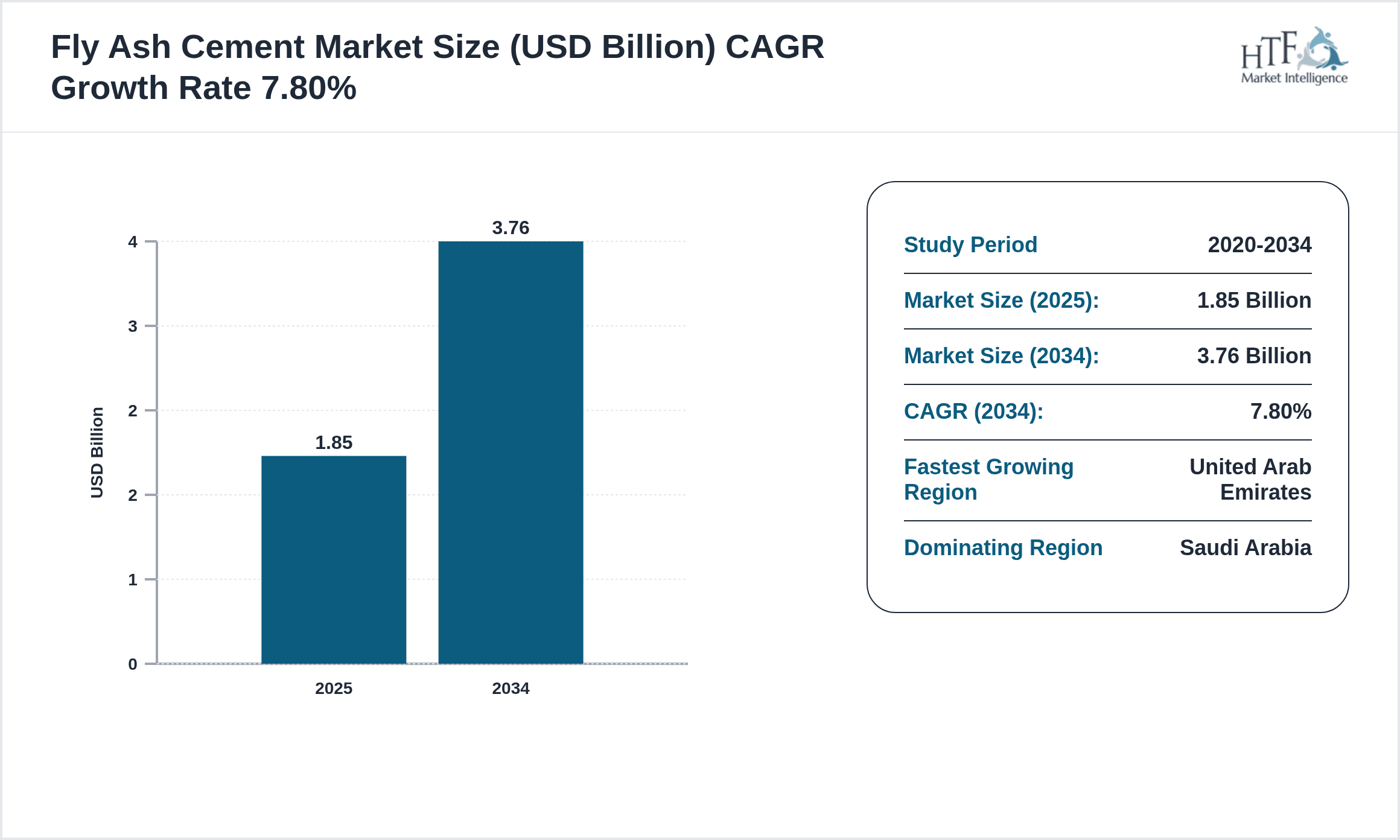

- •CAGR by 2034: 7.8%

- •Market Size by 2034: USD 3.76 Billion

- •Market Size in 2025: USD 1.85 Billion

- •Dominating Type: Class F Fly Ash Cement

- •Next-Following Type: Blended Cement

- •Dominating Application: Infrastructure

- •Next-Following Application: Residential Construction

- •Dominating Region: Saudi Arabia

- •Second-Leading Region: United Arab Emirates

- •Region with Highest Growth Rate: United Arab Emirates

- •Dominating Country: Saudi Arabia

Market Share Table

- •Market Share (%)

- ◦Class F Fly Ash Cement: 45%

- ◦Blended Cement: 32%

- •Market Share (%)

- ◦Infrastructure Application: 50%

- ◦Residential Construction: 28%

- •Growth Rate (%)

- ◦Class F Fly Ash Cement: 7.3%

- ◦Blended Cement: 9.1%

- •Growth Rate (%)

- ◦Infrastructure Application: 7.5%

- ◦Residential Construction: 8.2%

Top 5 Global Players

- •LafargeHolcim Middle East (United Arab Emirates)

- •Cemex Middle East (United Arab Emirates)

- •Saudi Cement Company (Saudi Arabia)

- •Emirates Cement Factory (United Arab Emirates)

- •Qatar National Cement Company (Qatar)

Regional Outlook

The Saudi Arabia currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Turkey

- Egypt

- United Arab Emirates

- Saudi Arabia

- Israel

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.85 Billion |

| Forecast Year Market Size | USD 3.76 Billion |

| CAGR | 7.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.5% |

| Scope of Report | Market is segmented by Type (Class F Fly Ash Cement, Class C Fly Ash Cement, Blended Cement, Portland Pozzolana Cement), Application (Infrastructure, Residential Construction, Commercial Construction, Industrial Facilities, Roadways), End User (Government Projects, Private Developers, Industrial Sector, Real Estate Companies), Distribution Channel (Direct Sales, Distributors, Retail Outlets, Online Platforms) |

| Regions Covered | Turkey, Egypt, United Arab Emirates, Saudi Arabia, Israel, Others |

| Key Companies | Saudi Cement Company (Saudi Arabia), Emirates Cement Factory (United Arab Emirates), Qatar National Cement Company (Qatar), Oman Cement Company (Oman), Kuwait Cement Company (Kuwait), Cemex Middle East (United Arab Emirates), LafargeHolcim Middle East (United Arab Emirates), Dubai Cement Factory (United Arab Emirates), Yamama Cement (Saudi Arabia), National Cement Company (Oman), Union Cement Company (Jordan), Abu Dhabi National Cement Company (UAE), Riyadh Cement Company (Saudi Arabia), Qassim Cement Company (Saudi Arabia), Al Gharbia Cement (United Arab Emirates) |

Fly Ash Cement Market - Middle East Size & Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.