Spatial Computing Platforms Market - Japan Size & Outlook 2020-2034

Japan Spatial Computing Platforms Market Breakdown by Application (Enterprise, Healthcare, Retail, Manufacturing, Education) by Type (Hardware, Software, Services) by Technology (Augmented Reality, Virtual Reality, Mixed Reality, Location-based Services) by Deployment Model (Cloud-based, On-premise, Hybrid) Geography (Hokkaido, Tohoku, Kanto, Chubu, Kansai, Chugoku, Shikoku, Kyushu)

Pricing

Report Overview

Market Scope

The Spatial Computing Platforms market in Japan encompasses integrated hardware, software, and service solutions that enable immersive interaction between real and virtual environments through technologies such as augmented reality, virtual reality, mixed reality, and location-based services. Products within this scope include AR/VR headsets, sensors, spatial mapping software, analytics platforms, and deployment services tailored for enterprise, healthcare, retail, manufacturing, and educational sectors. Excluded from this scope are standalone conventional computing devices and general-purpose consumer electronics without spatial computing capabilities. The market also excludes peripheral accessories not directly involved in spatial computing processes. This comprehensive scope accounts for technological, operational, and commercial dimensions of spatial computing platforms, factoring in supply chain logistics, manufacturing economics, and regulatory compliance aspects critical to Japan’s technologically advanced market ecosystem.

Regional Performance Analysis

Japan's spatial computing platforms market shows pronounced regional differentiation driven by industrial concentration and infrastructure maturity. The Kanto region, home to Tokyo and Yokohama, dominates due to its dense concentration of technology companies, access to capital, and advanced ICT infrastructure facilitating production and consumption of spatial computing solutions. Kanto's robust supply-chain networks and skilled workforce underpin its commanding 32.7% market share and sustained CAGR of 14.1%. Kansai follows as a significant industrial hub with a strong manufacturing and technology cluster centered around Osaka and Kyoto, enabling substantial production capabilities and innovation. Meanwhile, Chubu, including Nagoya, is the fastest-growing region, driven by automotive and manufacturing industries adopting spatial computing for process optimization, reflecting an 18.2% CAGR and 21.5% market share growth. Tohoku and Kyushu regions contribute modestly but are witnessing increasing investment and consumer adoption. Regional competitive advantages arise from Japan’s integrated logistics infrastructure and government-backed digital transformation initiatives, fostering commercial opportunities and market maturity progression across these zones.

Players Coverage

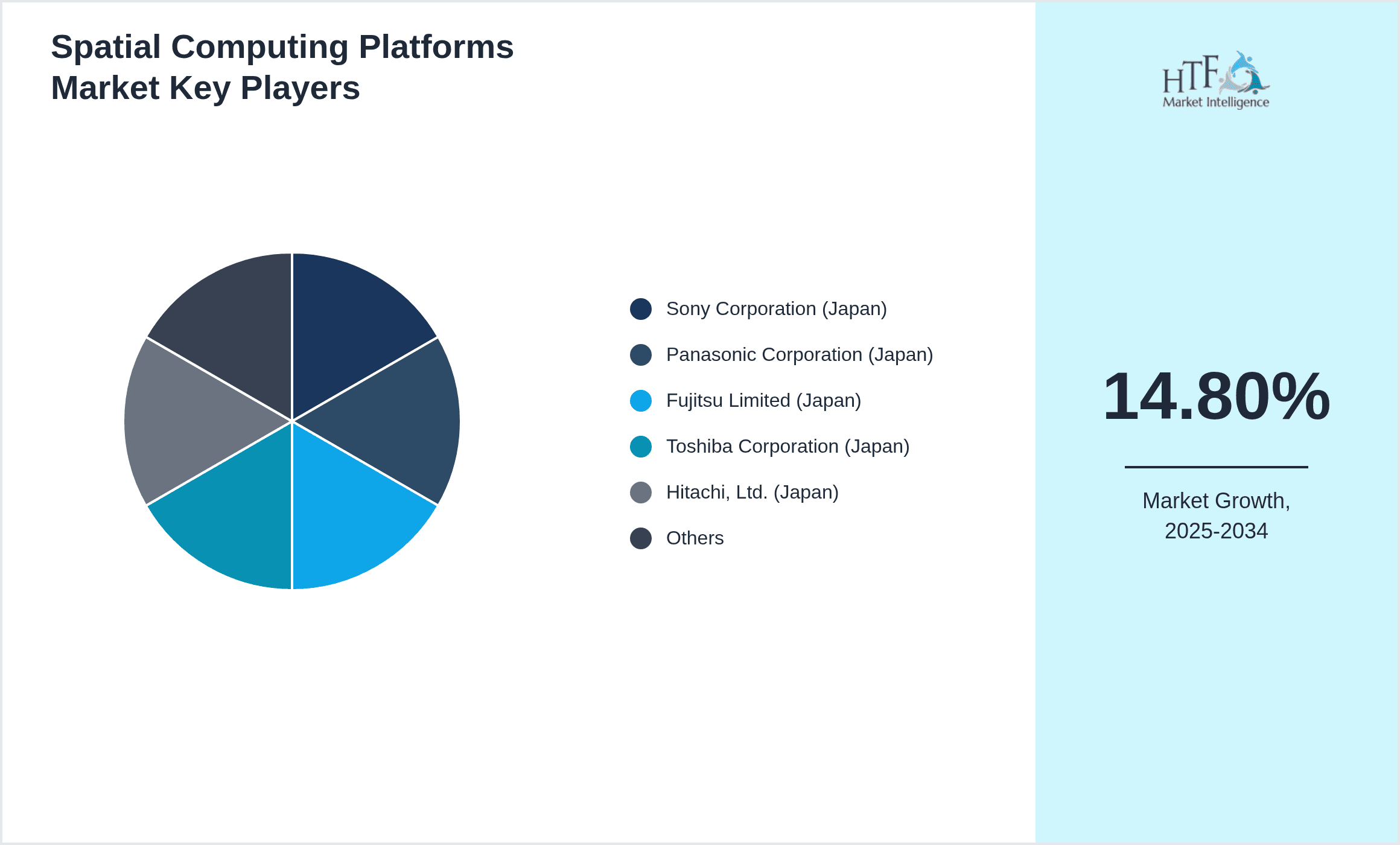

- •Sony Corporation (Japan)

- •Panasonic Corporation (Japan)

- •Fujitsu Limited (Japan)

- •Toshiba Corporation (Japan)

- •Hitachi, Ltd. (Japan)

- •NEC Corporation (Japan)

- •SoftBank Group Corp. (Japan)

- •Nikon Corporation (Japan)

- •Kudan Inc. (Japan)

- •CyberAgent, Inc. (Japan)

Competition Analysis

The competitive landscape of Japan’s spatial computing platforms market is intensely dynamic, characterized by rapid technological innovation and strategic positioning among incumbent technology giants and emerging startups. Industry leaders are leveraging AI integration, edge computing, and 5G connectivity to differentiate their offerings and enhance user experience. Strategic partnerships and mergers are prevalent, facilitating ecosystem expansion and cross-sector collaboration, particularly between hardware manufacturers and software developers. Pricing strategies are carefully calibrated to balance adoption acceleration with sustainable margins amidst high R&D expenditures. Distribution channels are evolving, emphasizing cloud-based delivery models and enterprise service contracts over traditional hardware sales. Entry barriers remain high due to the complexity of spatial computing technologies and the necessity for deep integration with existing enterprise systems. Future competition will increasingly hinge on the ability to deliver scalable, interoperable, and AI-enhanced solutions that align with Japan’s stringent regulatory standards and evolving market demands, positioning technology differentiation and customer-centric innovation as pivotal success factors.

Growth Drivers & Demand Determinants

- •The Japanese government’s robust support for digital transformation and Industry 4.0 initiatives accelerates spatial computing adoption across manufacturing and healthcare sectors.

- •Strategic partnerships between domestic technology firms and global software providers enhance innovation capacity and market penetration.

- •Technological advancements in sensor miniaturization and AI-powered spatial analytics drive demand for sophisticated hardware and software platforms.

Dominant Segments

- •Software solutions represent the leading product segment within Japan’s spatial computing platforms market, driven by demand for sophisticated spatial mapping, analytics, and content creation tools that enable enterprise-scale deployments and customized applications across healthcare, manufacturing, and education sectors.

- •Enterprise application is the dominant service model owing to increasing requirements for remote collaboration, virtual training, and real-time operational insights, which spatial computing uniquely addresses in Japan’s technologically advanced and innovation-driven industries.

- •The cloud-based deployment model is gaining prominence as it delivers scalability, reduces capital expenditure, and supports integration with Japan’s expanding 5G infrastructure, facilitating broader adoption across SMEs and large corporations alike.

Market Segments & Classification

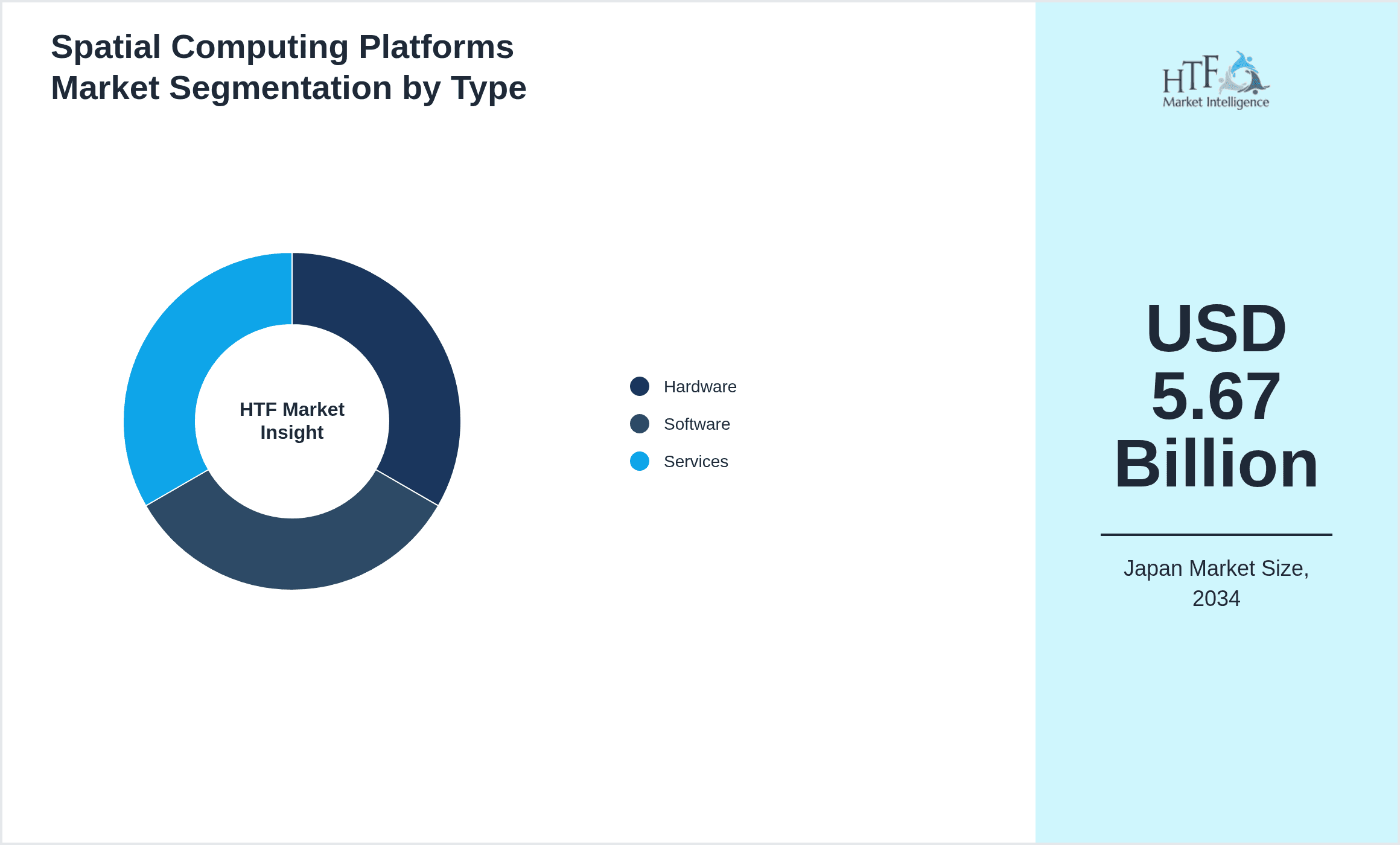

- •By Type

- ◦Hardware

- ◦Software

- ◦Services

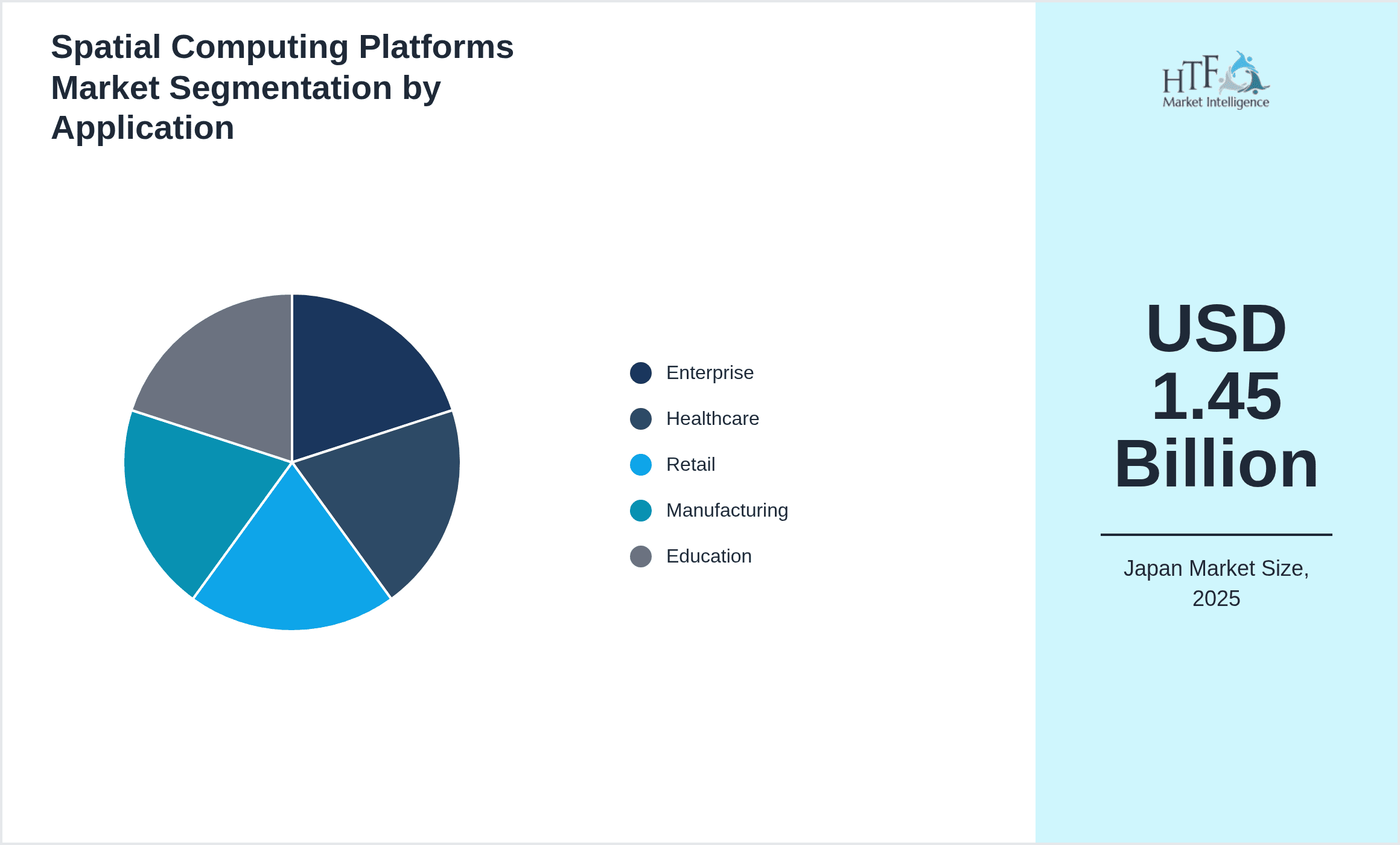

- •By Application

- ◦Enterprise

- ◦Healthcare

- ◦Retail

- ◦Manufacturing

- ◦Education

- •By Technology

- ◦Augmented Reality

- ◦Virtual Reality

- ◦Mixed Reality

- ◦Location-based Services

- •By Deployment Model

- ◦Cloud-based

- ◦On-premise

- ◦Hybrid

Regulatory Constraints

- •Japan’s stringent environmental regulations and sustainability mandates impose rigorous standards on the manufacturing processes of hardware components, necessitating investment in green technologies and energy-efficient operations.

- •Trade restrictions and certification standards, including data privacy laws and cybersecurity requirements, create operational complexities that spatial computing platform providers must navigate to ensure compliance and market access.

- •Inflationary pressures on raw material costs and semiconductor supply-chain disruptions amplify production expenses, impacting pricing strategies and profit margins across the value chain.

Future Outlook of Spatial Computing Platforms Market

- •Future expansion will be driven by increased adoption in healthcare for telemedicine and surgical assistance, as well as in manufacturing for smart factory implementations.

- •Kanto is projected to maintain dominance due to continued investment in technology infrastructure and concentration of corporate headquarters.

- •The industry will undergo significant transformation with the integration of AI and edge computing, improving platform intelligence and responsiveness over the long term.

The Road Ahead: Technology Revolution

- •Spatial computing platforms will catalyze a paradigm shift in digital interaction, embedding immersive technologies deeply into enterprise workflows and consumer experiences, fundamentally transforming operational models across sectors.

- •Long-term impacts include the convergence of spatial computing with AI, IoT, and 5G networks, enabling unprecedented levels of automation, personalization, and data-driven decision-making that will redefine competitive dynamics and value creation in Japan’s technology landscape.

Regional Outlook

The Kanto currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Chubu is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Hokkaido

- Tohoku

- Kanto

- Chubu

- Kansai

- Chugoku

- Shikoku

- Kyushu

| Feature | Details |

|---|---|

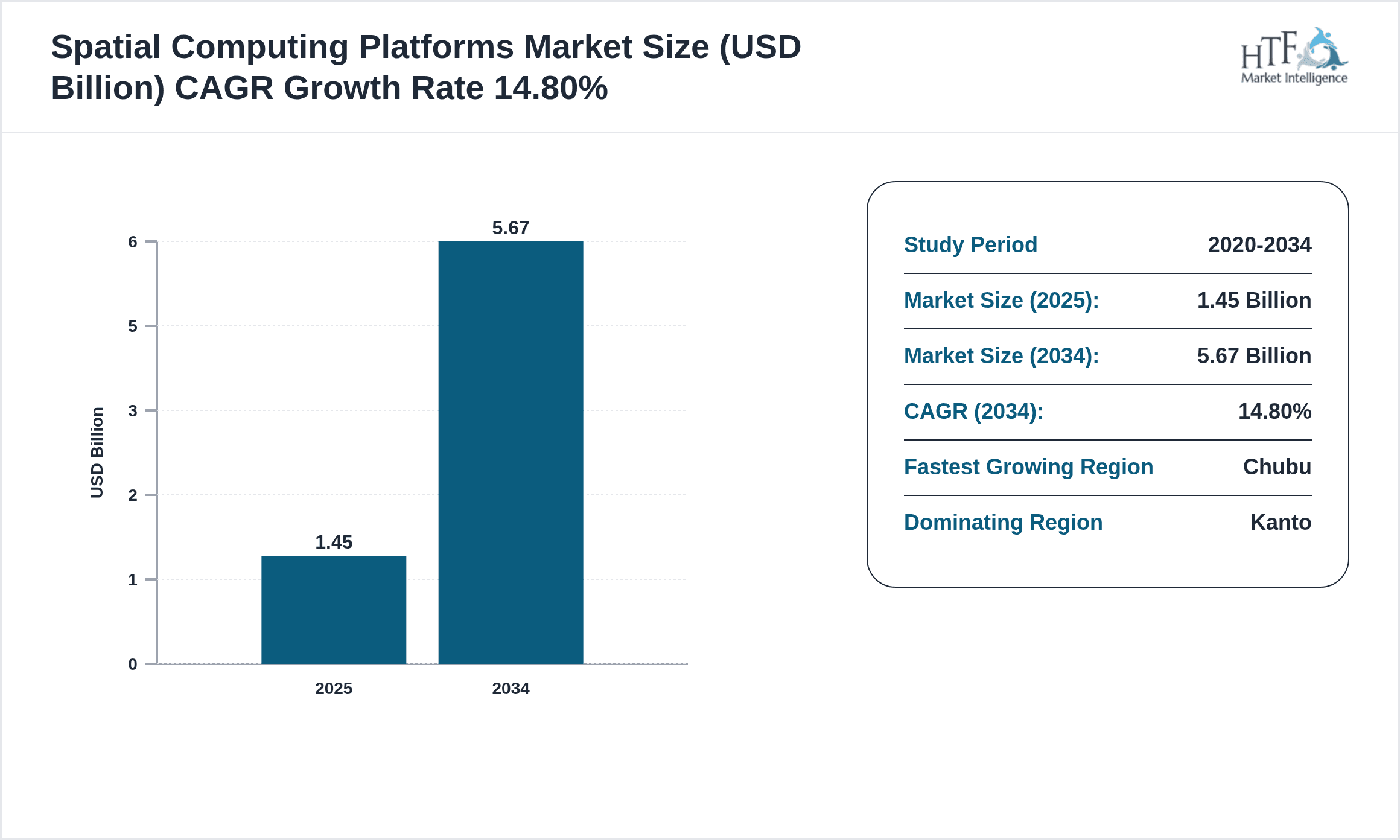

| Base Year Market Size | USD 1.45 Billion |

| Forecast Year Market Size | USD 5.67 Billion |

| CAGR | 14.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 13.0% |

| Regions Covered | Hokkaido, Tohoku, Kanto, Chubu, Kansai, Chugoku, Shikoku, Kyushu |

| Key Companies | Sony Corporation (Japan), Panasonic Corporation (Japan), Fujitsu Limited (Japan), Toshiba Corporation (Japan), Hitachi, Ltd. (Japan), NEC Corporation (Japan), SoftBank Group Corp. (Japan), Nikon Corporation (Japan), Kudan Inc. (Japan), CyberAgent, Inc. (Japan) |

Spatial Computing Platforms Market - Japan Size & Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.