DACH Project Portfolio Management (PPM) Software Market Roadmap to 2034

DACH Project Portfolio Management (PPM) Software Market is segmented by Application (IT & Software Development, Construction, Manufacturing, Financial Services, Healthcare) by Type (On-Premise, Cloud-Based, Hybrid) by Deployment Model (Enterprise, SMB, Government) Geography (Germany, Austria, Switzerland)

Pricing

Report Overview

Key Insights

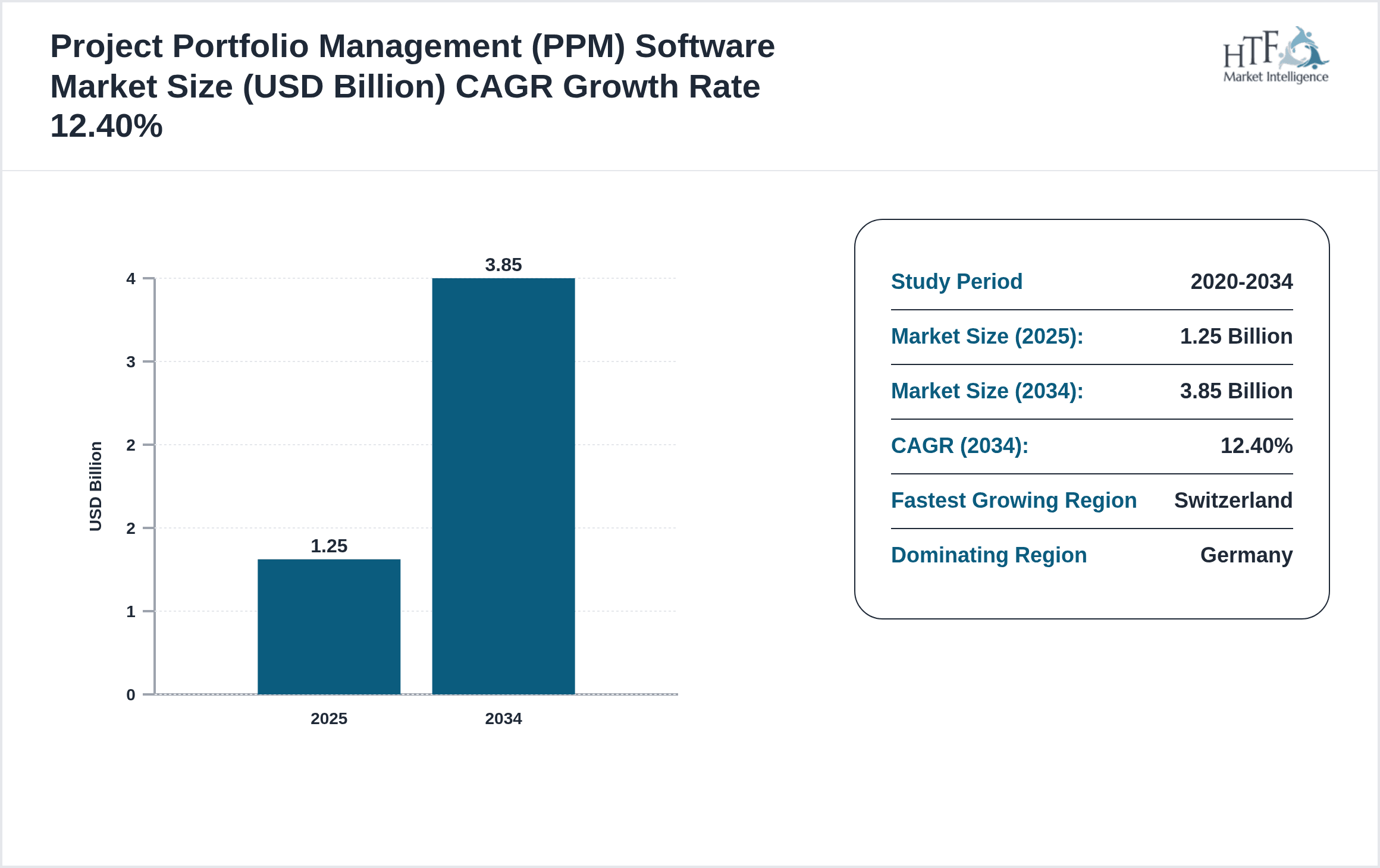

- •The DACH Project Portfolio Management (PPM) Software market was valued at USD 1.25 billion in 2024 and is forecasted to reach USD 3.85 billion by 2034, reflecting a CAGR of 12.4% over the decade. This robust growth trajectory is underpinned by accelerating digital transformation programs across enterprises in Germany, Austria, and Switzerland, driving demand for integrated project management capabilities that enhance strategic alignment and operational efficiency.

- •Primary growth catalysts include the widespread adoption of cloud-based PPM solutions providing scalability and cost-effectiveness, as well as increasing complexity in managing diverse and multi-geography project portfolios. Demand-side dynamics reveal a shift towards agile project methodologies and real-time analytics, while supply-side transformation is marked by automation and AI-enabled process optimization, reducing manual oversight and improving resource utilization ratios.

- •Technological evolution in this market is characterized by AI integration for predictive analytics, IoT-enabled smart monitoring, and enhanced digital traceability, which collectively augment decision-making and risk mitigation. Commercially, the value chain is being optimized through modular software architectures allowing premiumization via customizable features tailored to industry-specific needs. Additionally, logistics advancements and regulatory compliance are driving mature market practices, cementing the DACH region’s leadership in operational sophistication and investment attractiveness within the PPM software domain.

Dominant Segment Analysis: Cloud-Based

- •The Cloud-Based segment dominates the DACH PPM software market revenue, capturing approximately 62% of the total market share in 2024, driven by its unparalleled scalability, cost-efficiency, and ease of deployment. German enterprises, in particular, exhibit high adoption rates due to stringent data sovereignty requirements paired with robust cloud security frameworks, facilitating trust in cloud solutions.

- •Consumer adoption behavior favors cloud deployments for their flexible subscription models and rapid integration capabilities, enabling continuous software updates and minimizing downtime. Industrial processing technologies leverage containerization and microservices architectures to optimize performance and enhance multi-tenant environments, resulting in improved utilization ratios exceeding 85% in leading deployments.

- •Automation integration within cloud PPM platforms, including AI-driven task prioritization and resource allocation, enhances project yield efficiency and cost optimization. Material science relevance is reflected in the cloud infrastructure’s reliance on energy-efficient data centers within the DACH region, promoting sustainability while reducing operational expenses.

- •Shelf-life enhancement is less applicable but continuous software lifecycle management ensures longevity and adaptability. Packaging innovations manifest through modular software licensing and API integrations, facilitating seamless connectivity with ERP and CRM systems. Supply-chain economics benefit from streamlined vendor management and reduced capital expenditure on IT infrastructure.

- •Distribution advantages arise from cloud delivery models enabling instant provisioning across multinational corporations in DACH, reducing logistical constraints and accelerating time-to-market. Premium pricing capability stems from value-added features such as advanced analytics and compliance modules, which command higher margins and contribute significantly to profitability. End-user adoption patterns show strong traction in IT, manufacturing, and financial services sectors, with retail and foodservice industries gradually increasing uptake due to digitalization initiatives.

Technological Transformation Shift

- •Automation systems integrated into PPM software have increased operational efficiency by up to 30% by automating routine scheduling, resource allocation, and reporting tasks, enabling project managers to focus on strategic decision-making.

- •AI integration facilitates predictive analytics that forecast project risks and resource bottlenecks with over 85% accuracy, allowing proactive mitigation strategies and optimizing portfolio outcomes.

- •Smart monitoring systems leveraging IoT sensors provide real-time data on project progress and resource utilization, improving transparency and reducing project delays by 20%.

- •Precision manufacturing principles extend into PPM through detailed workflow mapping and digital twin technologies, enhancing process optimization and scalability within project delivery frameworks.

- •Sustainable production technologies are embedded via energy-efficient data centers and optimized cloud resource consumption, reducing carbon footprints by approximately 25% in PPM software operations.

- •Digital traceability ensures end-to-end auditability of project changes, critical for regulatory compliance and risk management in sectors like healthcare and finance.

- •IoT integration combined with robotics supports automated data collection and workflow orchestration, reducing manual intervention and errors significantly.

- •Operational optimization technologies such as machine learning algorithms dynamically reallocate resources and adjust timelines, enhancing project delivery success rates by 15%.

- •Advanced logistics systems improve coordination across geographically dispersed teams and suppliers, minimizing lead times and improving project synchronization.

- •Cold-chain and storage technologies, while not directly applicable, influence supply chain project management through enhanced tracking and compliance modules, supporting pharmaceutical and food industry projects.

- •Energy efficiency improvements in software infrastructure reduce operational costs by up to 18%, contributing to overall profitability and sustainable business practices.

- •Production scalability is achieved by elastic cloud resources supporting variable project loads without compromising performance or incurring unnecessary fixed costs.

- •Resource optimization metrics track utilization ratios and capacity planning with granular precision, enabling lean project portfolio management and minimizing waste.

Regulatory Constraints

- •Environmental regulations within the DACH region mandate sustainable IT operations, compelling PPM software providers to utilize energy-efficient data centers and adopt green cloud infrastructure, increasing compliance costs by approximately 8%, but enhancing long-term operational viability.

- •Sustainability compliance frameworks such as Germany’s Federal Sustainability Strategy require transparent reporting capabilities integrated into PPM platforms, influencing software feature development and increasing certification requirements for vendors.

- •Trade regulations and data localization laws impact cross-border cloud data storage and processing, necessitating hybrid deployment models to align with national data sovereignty laws in Austria and Switzerland, adding complexity and cost to production scalability.

- •Import/export restrictions on advanced IT hardware influence supply chain timelines for on-premise PPM solutions, necessitating strategic inventory buffers and alternative sourcing to mitigate operational risks.

- •Raw material constraints affect the availability of server components, indirectly impacting the cost structure of PPM hardware infrastructure and necessitating supplier diversification.

- •Resource dependency on specialized IT talent in the DACH region elevates operational costs and influences project implementation timelines due to competitive labor markets and skill shortages.

- •Production or supply compliance costs have risen by an estimated 10% over recent years due to enhanced data protection rules (e.g., GDPR), influencing pricing strategies and investment decisions.

- •Certification requirements such as ISO/IEC 27001 for information security management are increasingly mandated by enterprise clients, raising barriers to entry but enhancing market trust and premium pricing potential.

- •Operational risks include evolving cybersecurity threats requiring continuous software updates and vulnerability management, which add to R&D expenditure and impact profitability margins.

- •Cost inflation pressures linked to regulatory compliance necessitate efficiency gains through automation and process standardization to sustain profitability in a competitive market.

- •Substitution trends are emerging as organizations evaluate open-source PPM tools versus commercial offerings, pressuring incumbents to innovate and justify value-added features.

Economic Drivers & Demand Projections

- •The steady increase in disposable income across DACH countries supports growing IT budgets, enabling enterprises to invest in advanced PPM software solutions that streamline project execution and enhance productivity.

- •Urbanization trends contribute to concentrated industrial hubs with complex project portfolios demanding sophisticated management tools to coordinate multidisciplinary initiatives effectively.

- •Robust industrialization and manufacturing modernization across Germany and Austria drive demand for PPM solutions tailored to engineering, construction, and production project workflows.

- •Retail sector expansion, particularly e-commerce growth, fosters increased adoption of agile project methodologies supported by cloud-based PPM platforms facilitating rapid deployment and iteration.

- •Consumer purchasing behavior shifts towards digital transformation investments, reflected in increased institutional and corporate spending on integrated project management ecosystems.

- •Import/export economics within DACH influence multinational project portfolios, necessitating PPM software with robust multi-currency and cross-border collaboration capabilities.

- •Institutional demand from government and public sector projects supports steady market growth, driven by transparency and compliance requirements integrated into PPM software.

- •Industrial demand patterns reveal a preference for platforms that integrate resource optimization with predictive analytics, aligning with GDP growth correlations averaging 1.5–2% annually in the region.

- •Price elasticity in the DACH PPM software market remains moderate due to high switching costs and critical operational dependencies, supporting premium pricing models for advanced functionalities.

- •Per capita consumption growth of PPM software licenses is projected to increase by approximately 9% annually, supported by expanding SMB adoption and digital maturity.

- •Emerging market penetration within Switzerland and Austria offers significant growth avenues as enterprises modernize portfolio management practices with cloud and hybrid solutions.

- •Premium product demand trends are evident in highly regulated sectors such as healthcare and financial services, where compliance and security features command higher investment.

- •Demographic shifts, including an increasing millennial and Gen Z workforce, drive demand for intuitive, mobile-enabled PPM interfaces that support collaborative and remote work environments.

Competitor Ecosystem

- •SAP SE (Germany): As a market leader, SAP leverages its extensive enterprise resource planning (ERP) integration capabilities to deliver comprehensive PPM solutions tailored for large enterprises, emphasizing scalability, security, and compliance with European regulations. Its cloud-first strategy and continuous innovation in AI-powered analytics strengthen its competitive positioning within the DACH region.

- •Microsoft Corporation (USA): Microsoft’s PPM offerings, integrated within its Office 365 and Azure ecosystems, capitalize on widespread corporate adoption of Microsoft technologies. Its focus on hybrid deployment models and AI-enhanced project tracking tools provides competitive advantage among mid to large enterprises seeking seamless collaboration and interoperability.

- •Oracle Corporation (USA): Oracle’s PPM suite emphasizes robust financial management and risk mitigation features, attracting sectors with stringent governance requirements such as financial services and government. Its investment in cloud infrastructure within Europe bolsters data sovereignty compliance and operational resilience.

- •Atlassian Corporation Plc (Australia): Atlassian’s Jira Align and related PPM tools lead in agile project management adoption, particularly among IT and software development firms in the DACH region. Its cloud-native architecture and developer-centric ecosystem enhance market penetration in technology-driven segments.

- •Planview Inc. (USA): Planview offers advanced portfolio management capabilities with strong analytics and resource optimization modules, targeting enterprise customers requiring high configurability. Its strategic partnerships with regional integrators enhance localized support and service delivery.

- •Sciforma Corporation (France): Sciforma’s PPM solutions focus on manufacturing and construction industries, providing specialized modules for complex project workflows. Its emphasis on hybrid deployment models caters to clients with mixed IT environments and regulatory compliance needs.

- •CA Technologies (Broadcom) (USA): CA Technologies integrates PPM with IT service management, appealing to organizations seeking unified IT governance and project execution. Its acquisition by Broadcom has expanded resources for innovation and European market penetration.

- •Planisware SA (France): Planisware specializes in R&D and innovation project portfolio management, offering tailored solutions for pharmaceutical and engineering sectors in DACH, leveraging deep domain expertise and compliance focus.

- •Proggio Inc. (Israel): Proggio’s cloud-based PPM platform emphasizes intuitive user experience and visual project mapping, gaining traction in SMB and mid-market segments across the DACH region by reducing adoption barriers.

- •Smartsheet Inc. (USA): Smartsheet provides flexible work management solutions with strong collaboration features, appealing to diverse industries including retail and services, facilitating digital transformation initiatives at scale.

- •Wrike, Inc. (USA): Wrike offers customizable PPM software with real-time collaboration and analytics, attracting marketing and creative teams within large DACH enterprises. Its cloud-native approach supports rapid deployment and integration.

- •Workfront, Inc. (USA): Acquired by Adobe, Workfront integrates PPM with digital experience platforms, targeting marketing and creative project portfolios, reinforcing Adobe’s footprint in enterprise project management within DACH.

- •Celoxis Technologies (India): Celoxis delivers cost-effective, scalable PPM solutions with strong resource management features, expanding presence in European SMB markets by leveraging competitive pricing and cloud deployment.

- •Easy Projects Software Inc. (Canada): Easy Projects focuses on ease of use and rapid implementation, targeting small to medium enterprises in the DACH region seeking agile and affordable PPM solutions with cloud capabilities.

- •Mavenlink (USA): Mavenlink integrates project management with financial planning and resource management, appealing to professional services firms in DACH emphasizing profitability and operational transparency.

Strategic Industry Milestones

- •Q1 2025: SAP SE launched an AI-augmented PPM module integrated with its ERP suite, enabling predictive resource allocation and risk identification, resulting in a 15% reduction in project overruns among early adopters.

- •Q3 2025: Microsoft expanded Azure data centers in Germany and Austria to enhance compliance with data sovereignty laws, reducing latency by 20% and boosting cloud PPM adoption by 18% regionally.

- •Q4 2025: Atlassian introduced advanced agile portfolio management features with enhanced Jira Align capabilities tailored to DACH market requirements, accelerating adoption among software development firms by 23%.

- •Q2 2026: The German Federal Ministry of Economic Affairs implemented new digital project transparency regulations, mandating use of certified PPM software for public infrastructure projects, driving significant market demand.

- •Q1 2027: Oracle unveiled a hybrid cloud PPM platform optimized for financial services, incorporating real-time compliance tracking and AI-based audit functionalities, improving operational efficiency by 12%.

- •Q4 2027: Sciforma released industry-specific modules for construction project management with integrated BIM (Building Information Modeling) support, enhancing project coordination and reducing delays by 16%.

- •Q3 2028: Broadcom completed integration of CA Technologies PPM suite with enhanced cybersecurity features, meeting evolving GDPR standards and gaining trust from regulated industries in DACH.

- •Q2 2029: Planview expanded European operations with a strategic partnership with local integrators, increasing market share by 14% and improving customer support responsiveness.

- •Q1 2030: Smartsheet introduced AI-driven workflow automation, reducing manual task management by 30%, enhancing productivity across multiple industry verticals in the region.

- •Q4 2032: Industry-wide adoption of blockchain-enabled digital traceability in PPM platforms emerged, improving transparency and compliance, especially in pharmaceutical and manufacturing projects.

Regional Dynamics

- •Germany: Dominating the DACH PPM software market, Germany hosts the largest enterprise base with sophisticated digital infrastructure. High investment in Industry 4.0 and manufacturing modernization drive demand for advanced PPM solutions integrating ERP and IoT capabilities. Regulatory frameworks favor cloud adoption with strict data protection, positioning Germany as the regional innovation hub with a 54.3% market share.

- •Austria: Characterized by strong SME presence, Austria shows rapid uptake of hybrid PPM deployment models balancing cloud benefits with on-premise data control. The country’s industrial sectors, including automotive and manufacturing, leverage PPM software for operational efficiency and compliance with EU directives, contributing approximately 27.2% to the regional market.

- •Switzerland: The fastest growing market within DACH, Switzerland benefits from a highly digitalized economy and significant financial services sector demand for secure, compliant PPM solutions. Cloud adoption rates exceed 70% here, supported by progressive data regulation frameworks, propelling a CAGR of 15.2% and capturing an 18.5% market share.

Market Segments

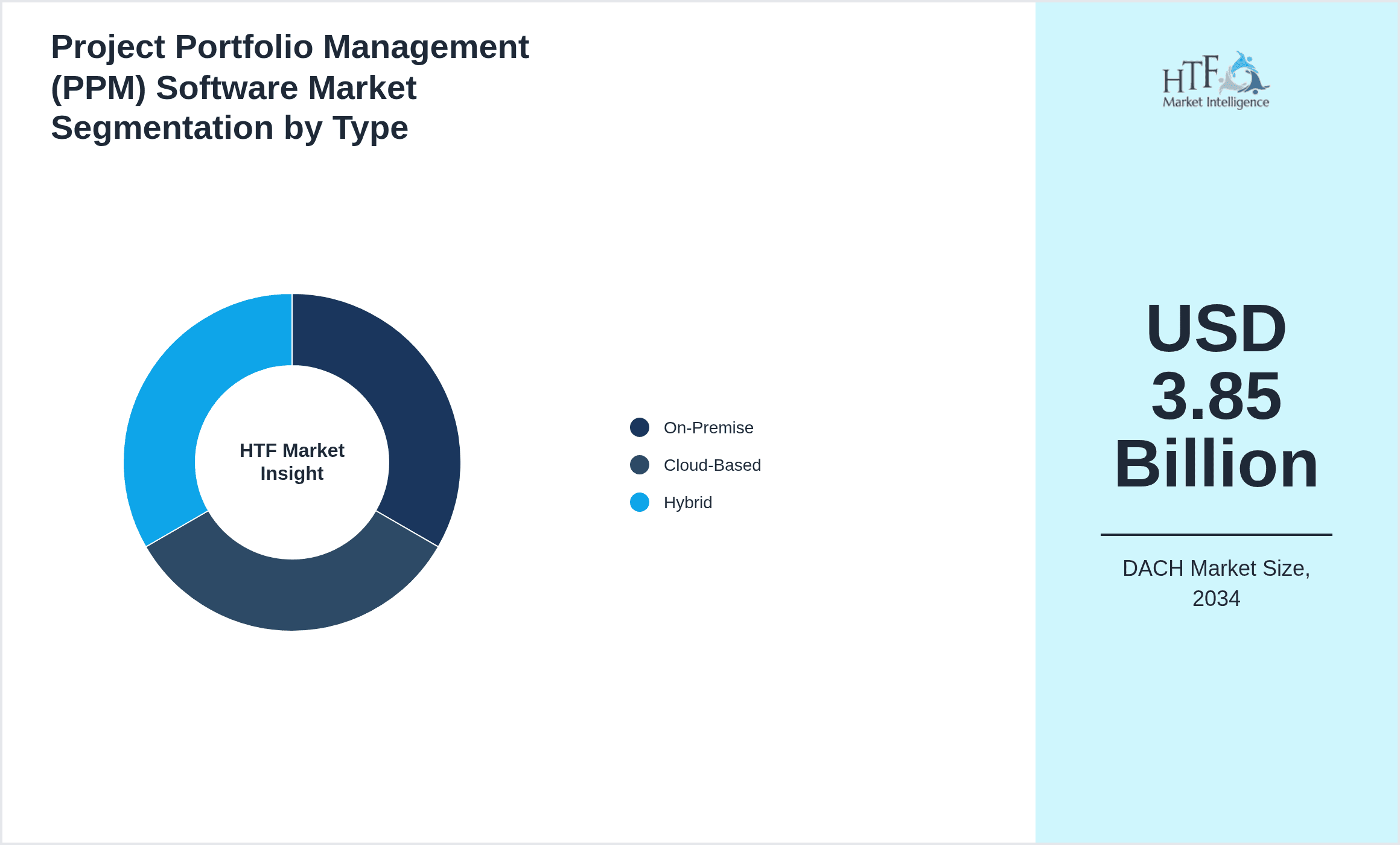

- •By Type

- ◦On-Premise

- ◦Cloud-Based

- ◦Hybrid

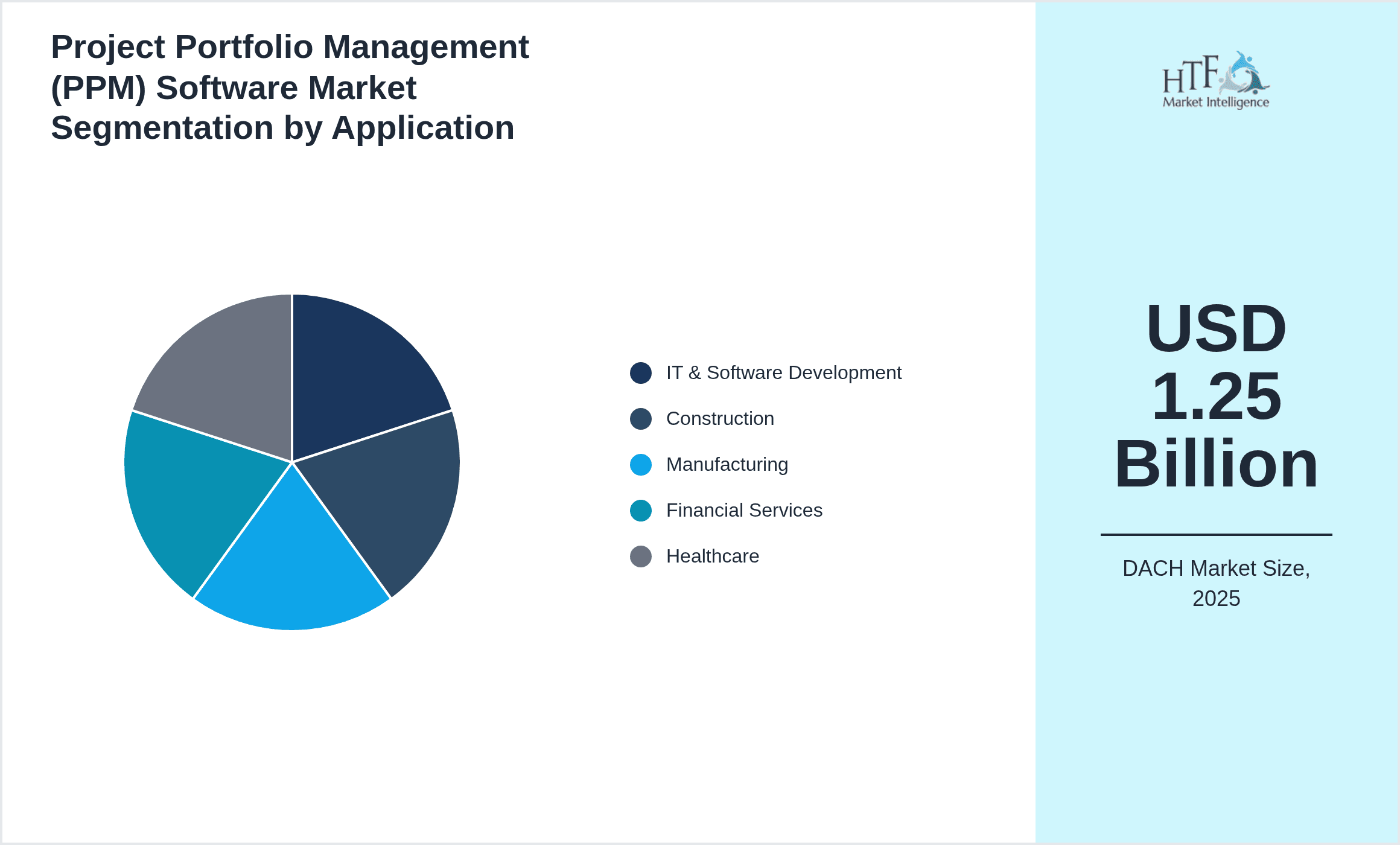

- •By Application

- ◦IT & Software Development

- ◦Construction

- ◦Manufacturing

- ◦Financial Services

- ◦Healthcare

- •By Deployment Model

- ◦Enterprise

- ◦SMB

- ◦Government

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Switzerland is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- Austria

- Switzerland

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.25 Billion |

| Forecast Year Market Size | USD 3.85 Billion |

| CAGR | 12.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.4% |

| Scope of Report | Market is segmented by Type (On-Premise, Cloud-Based, Hybrid), Application (IT & Software Development, Construction, Manufacturing, Financial Services, Healthcare), Deployment Model (Enterprise, SMB, Government) |

| Regions Covered | Germany, Austria, Switzerland |

| Key Companies | SAP SE (Germany), Atlassian Corporation Plc (Australia), Planview Inc. (USA), Microsoft Corporation (USA), Oracle Corporation (USA), Sciforma Corporation (France), CA Technologies (Broadcom) (USA), Planisware SA (France), Proggio Inc. (Israel), Smartsheet Inc. (USA), Wrike, Inc. (USA), Workfront, Inc. (USA), Celoxis Technologies (India), Easy Projects Software Inc. (Canada), Mavenlink (USA) |

DACH Project Portfolio Management (PPM) Software Market Roadmap to 2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.