Graphite Electrode Rod Market - United States Industry Size & Growth Analysis 2020-2034

United States Graphite Electrode Rod Market is segmented by Type (Ultra High Power, High Power, Regular Power) by Application (Steel Manufacturing, Foundry, Automotive, Construction, Others) by Manufacturing Process (Breathing, Extrusion, Isostatic Pressing) Geography (Northeast, Southwest, The South, The Midwest)

Pricing

Report Overview

Graphite Electrode Rod Market Overview

The United States Graphite Electrode Rod market is a critical segment of the metallurgical industry, primarily serving the electric arc furnace (EAF) steel manufacturing sector. This market has experienced steady growth driven by increasing steel production capacity, technological advancements in electrode manufacturing, and heightened focus on energy efficiency. Graphite electrodes are essential for conducting electrical current in EAFs, enabling efficient melting of scrap steel. The market is characterized by a diverse product portfolio including Ultra High Power (UHP), High Power (HP), and Regular Power (RP) electrodes, each catering to different furnace specifications and operational requirements. The integration of automation and precision manufacturing has enhanced product quality and operational efficiency. Furthermore, supply chain optimization, including sourcing of raw materials such as needle coke and petroleum coke, is crucial to market dynamics. Regulatory frameworks emphasizing environmental sustainability and emission reduction also influence production methodologies, compelling manufacturers to innovate and improve process efficiencies. Overall, the market exhibits a strategic blend of operational sophistication, commercial realism, and technological transformation, positioning it for robust growth through 2034.

Key Market Takeaways

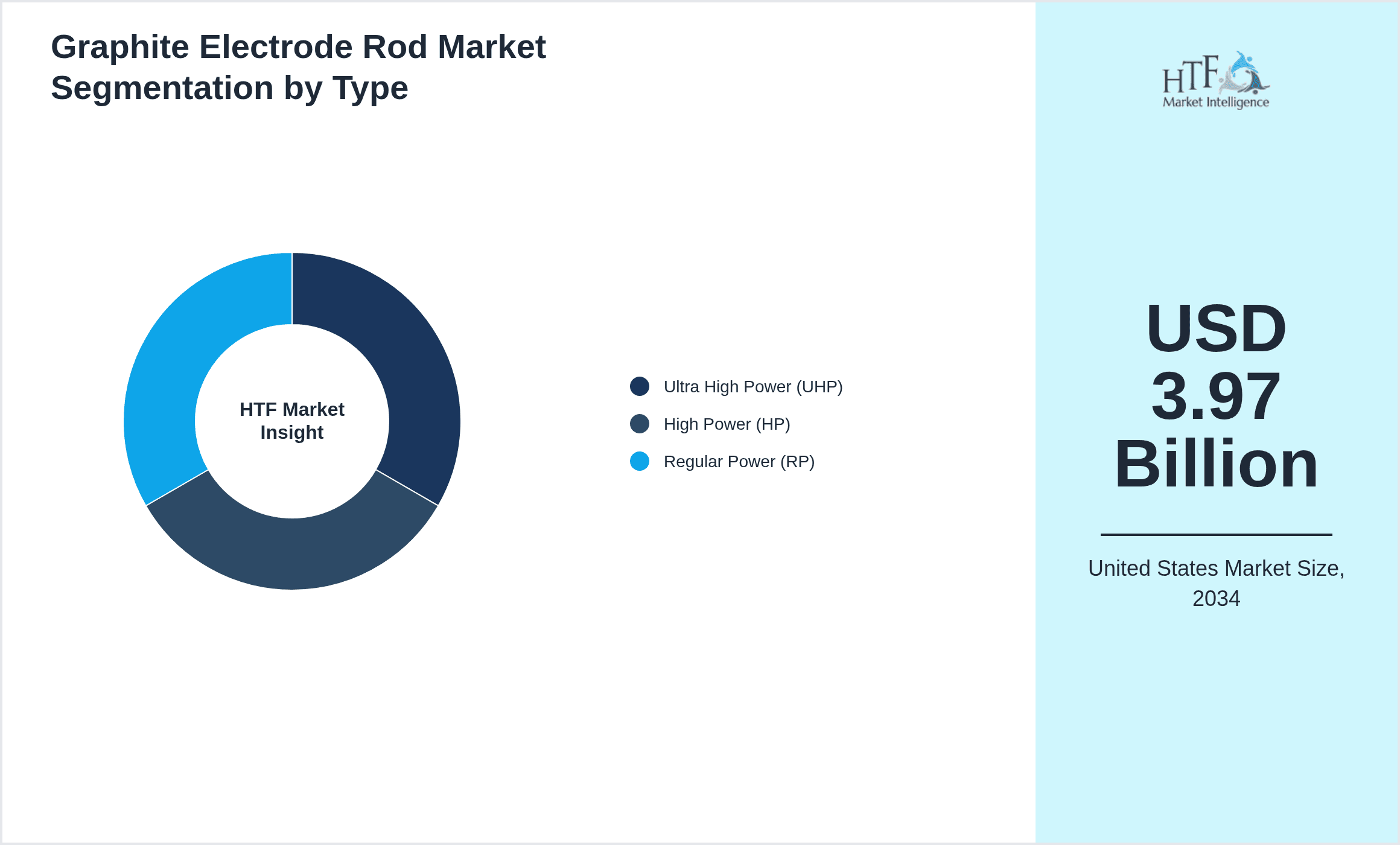

- •The Ultra High Power (UHP) graphite electrode segment dominates due to superior conductivity and longer lifespan, capturing significant market share.

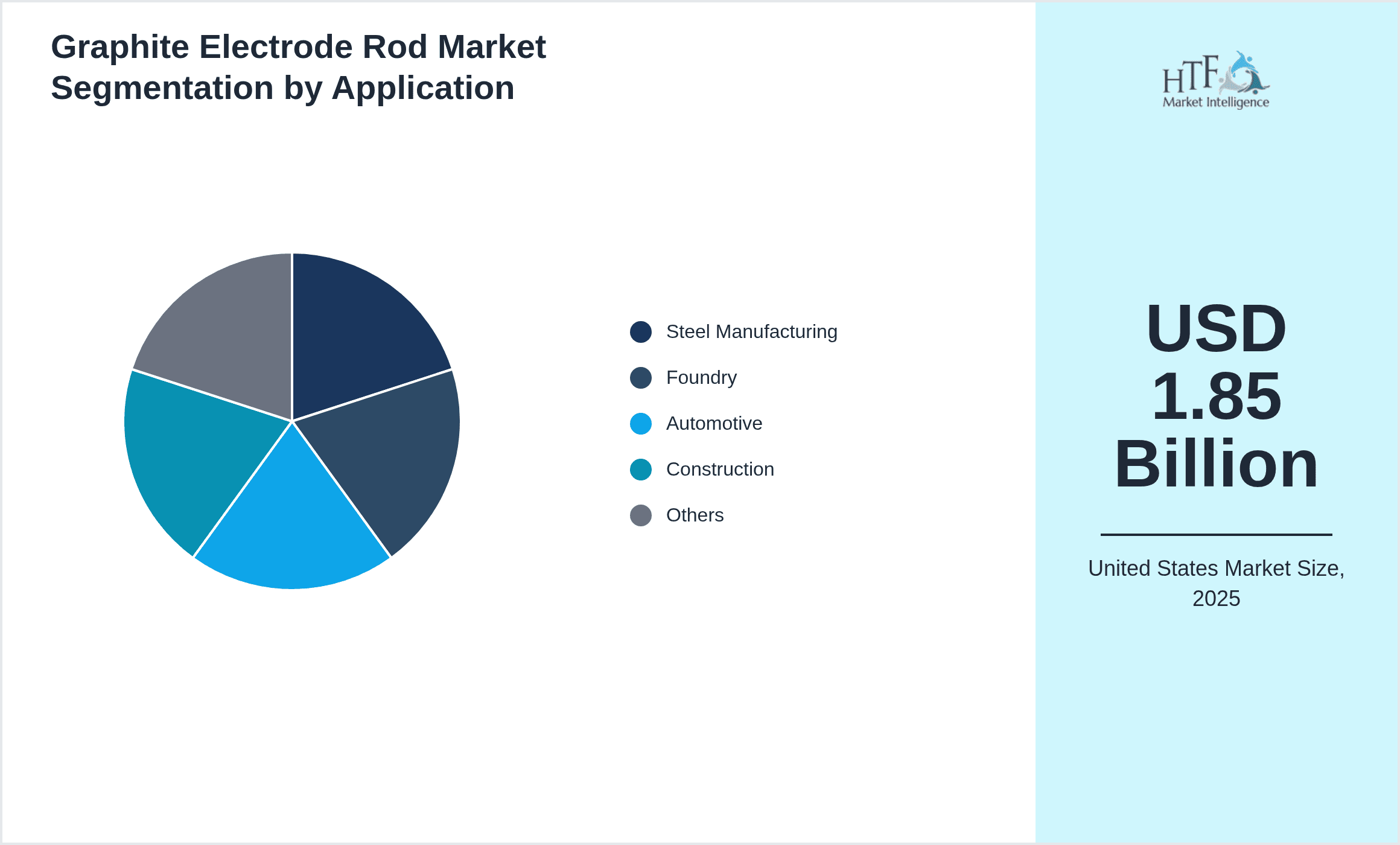

- •Steel manufacturing remains the largest application sector, driven by the growing adoption of electric arc furnace technology across the United States.

- •The Midwest region leads in market size, attributed to the concentration of steel production facilities and established supply chain infrastructure.

- •Technological advancements and sustainability initiatives are key growth drivers, enabling improved electrode performance and compliance with environmental regulations.

Graphite Electrode Rod Segment Analysis

By Type, the Ultra High Power (UHP) electrodes dominate the market due to their ability to handle higher current densities and longer operational cycles, which translates to improved energy efficiency and reduced downtime in EAF steelmaking. High Power (HP) electrodes are rapidly gaining adoption owing to their balanced performance and cost-effectiveness, serving mid-capacity furnaces and secondary steel production. Regular Power (RP) electrodes maintain demand in smaller-scale foundry applications where operational intensity is lower. Manufacturing processes such as Breathing, Extrusion, and Isostatic Pressing significantly influence electrode quality and pricing. Isostatic Pressing, although costlier, produces electrodes with superior density and uniformity, preferred by premium steel producers. Application-wise, Steel Manufacturing commands the largest share, followed by Foundry, Automotive, and Construction sectors. Each application segment demands specific electrode characteristics reflecting operational parameters and industry requirements. The evolving automotive sector’s shift towards electric vehicles is triggering incremental demand for high-performance electrodes, particularly in specialty steel grades. Construction industry demand follows infrastructure development, further stimulating market expansion. The segment analysis underscores a technologically nuanced market with product differentiation aligned to operational and commercial realities.

Graphite Electrode Rod Regional Analysis

The United States graphite electrode rod market is regionally segmented into the Midwest, Northeast, Southeast, Southwest, West Coast, and Pacific Northwest zones. The Midwest dominates the market, accounting for 36% share, driven by its dense steel manufacturing cluster, established supply chains, and proximity to raw material suppliers. The West Coast exhibits the fastest growth at a CAGR of 9.5%, propelled by expanding EAF capacities, investments in green steel initiatives, and robust downstream industrial demand. The Northeast and Southeast maintain steady growth fueled by automotive and construction sectors, while the Southwest and Pacific Northwest contribute niche demand supported by specialized foundry operations and emerging electric steel production hubs. Regional logistics advantage, energy costs, and regulatory frameworks significantly influence market dynamics within these zones. Transportation infrastructure efficiencies and port access in the West Coast facilitate import-export activities critical for raw material sourcing and finished product distribution, enhancing the region’s growth trajectory. The regional analysis reflects a market shaped by operational geography, industrial concentration, and evolving economic policies.

Competitive Landscape

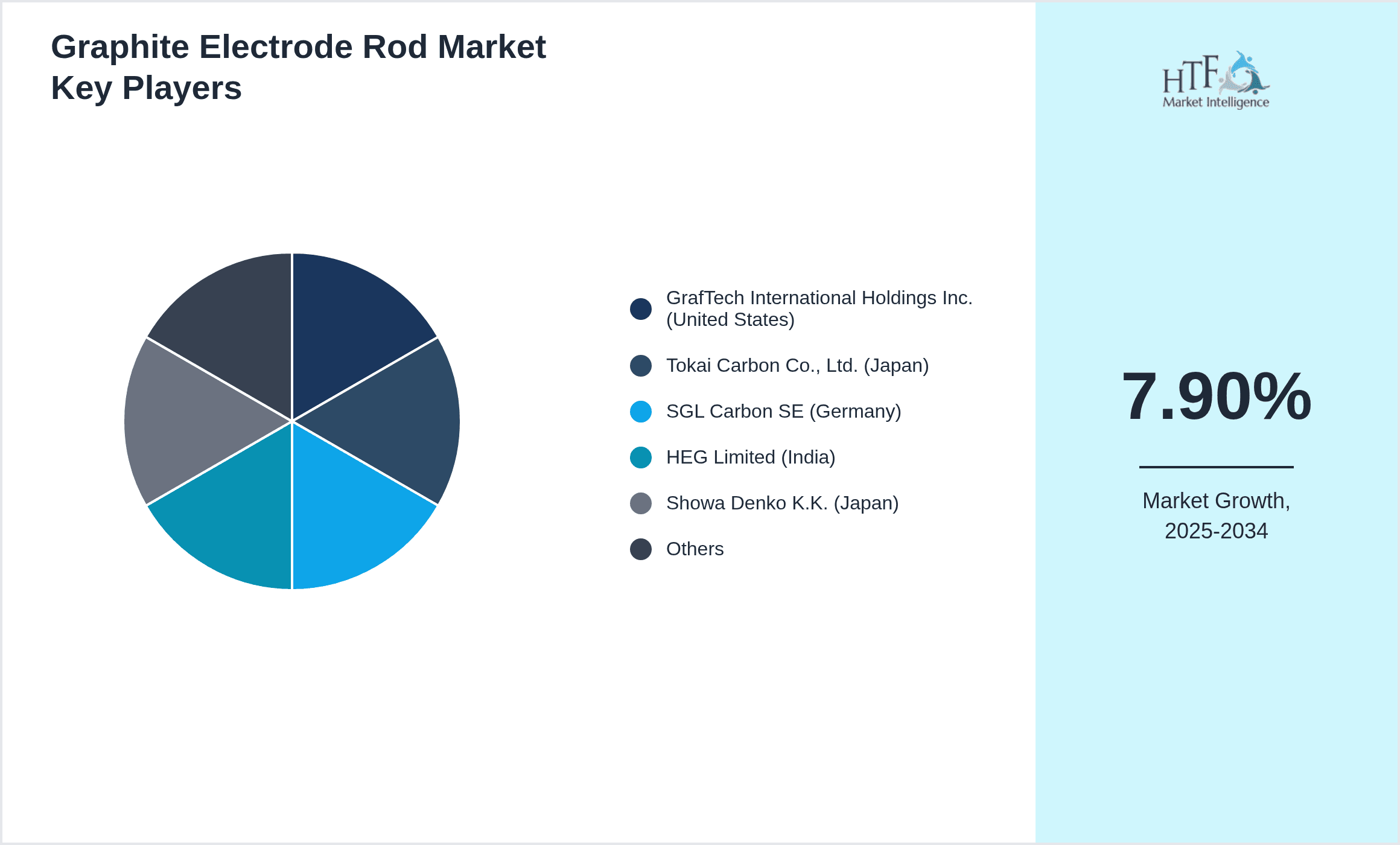

The United States graphite electrode rod market is characterized by a moderately concentrated competitive environment dominated by well-established multinational and domestic players. Market competition is intense with companies leveraging advanced manufacturing technologies, strategic vertical integration, and robust distribution networks to consolidate market share. Leading firms emphasize research and development to enhance electrode performance, focusing on improving electrical conductivity, mechanical strength, and oxidation resistance to meet stringent steel production requirements. Pricing strategies are closely aligned with raw material cost fluctuations and capacity utilization rates, with companies deploying flexible pricing models to maintain competitiveness. Strategic mergers and acquisitions have been pivotal for expanding production capabilities and geographic reach, particularly targeting enhanced presence in high-growth regional zones such as the West Coast. Partnerships with steel manufacturers and raw material suppliers ensure supply chain stability and cost optimization. Sustainability initiatives including energy-efficient production processes and utilization of recycled graphite materials are becoming differentiators. The market exhibits significant entry barriers due to high capital intensity, specialized technology requisites, and regulatory compliance, limiting new entrants. Future competition outlook indicates heightened focus on innovation, digitalization of manufacturing, and expansion into emerging applications to sustain growth and profitability.

Recent Industry Developments

- •Qtr 4 2025: GrafTech International announced a breakthrough in electrode manufacturing with a proprietary nano-coating technology that enhances oxidation resistance and extends electrode lifespan by 20%, promising significant cost savings for steel producers. This innovation incorporates advanced material science and automation, reinforcing GrafTech's market leadership and commitment to sustainability. The development is expected to accelerate adoption of Ultra High Power electrodes in the United States, supporting the transition to more energy-efficient electric arc furnace operations. Source: GrafTech International Press Release, December 2025.

- •Qtr 3 2025: The U.S. Environmental Protection Agency implemented updated emissions regulations specifically targeting graphite electrode manufacturing plants. These regulations mandate advanced air filtration and energy optimization systems, compelling manufacturers to invest in cleaner technologies. The move aims to reduce carbon footprint and particulate emissions, aligning the industry with national climate goals. Companies are strategically upgrading facilities to maintain compliance and capitalize on government incentives for green manufacturing, reinforcing technology transformation trends. Source: U.S. EPA Regulatory Update, September 2025.

- •Qtr 2 2025: A consortium of major U.S. graphite electrode producers and steel manufacturers launched a supply chain digitization initiative leveraging blockchain technology to enhance raw material traceability, inventory management, and logistics coordination. This transformative approach aims to reduce lead times, mitigate supply disruptions, and improve operational transparency. Early pilot projects demonstrated a 15% reduction in inventory holding costs and a 10% improvement in on-time delivery metrics, underscoring significant commercial benefits and operational realism in supply chain modernization. Source: Industry Consortium Press Release, June 2025.

Graphite Electrode Rod Market Statistics

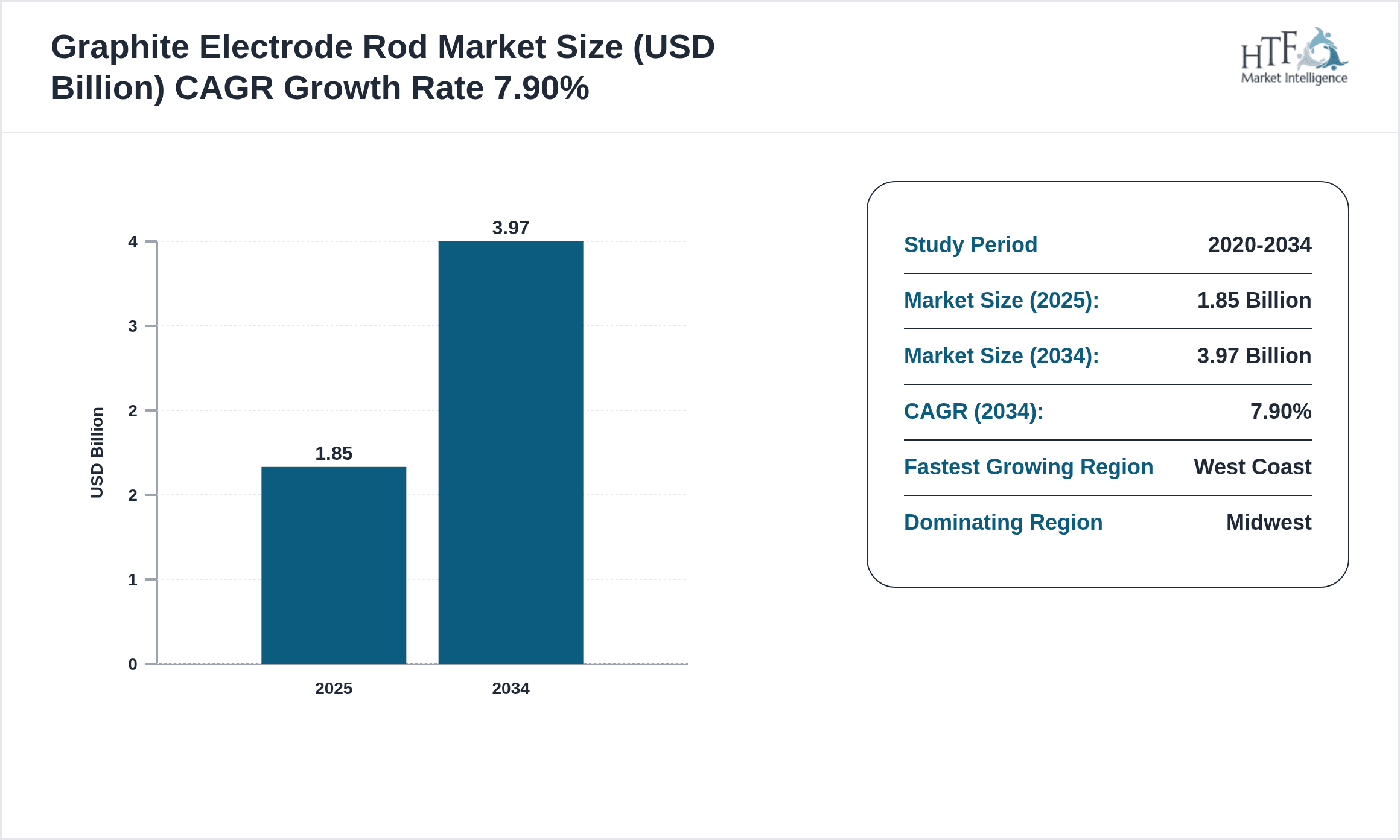

- •CAGR by 2034: 7.9%

- •Market Size by 2034: USD 3.97 Billion

- •Market Size in 2025: USD 1.85 Billion

- •Dominating Type: Ultra High Power; Next-following Type: High Power

- •Dominating Application: Steel Manufacturing; Next-following Application: Foundry

- •Dominating Region: Midwest; Second-leading Region with Highest Growth Rate: West Coast

- •Dominating Country: United States

Growth Drivers in Graphite Electrode Rod

- •Expansion of electric arc furnace steel production facilities increases demand for high-performance graphite electrodes due to their energy efficiency and operational advantages.

- •Technological advancements in electrode materials and manufacturing processes enhance product durability, conductivity, and lifespan, driving market growth.

- •Government incentives promoting energy-efficient and low-emission manufacturing support investment in advanced graphite electrode technologies.

- •Rising demand from automotive and construction sectors stimulates specialized electrode requirements, expanding application scope.

Market Restraints

- •Volatility in raw material prices, particularly needle coke and petroleum coke, impacts production costs and profit margins.

- •Stringent environmental regulations increase manufacturing complexity and capital expenditure, potentially limiting operational scalability.

- •Supply chain disruptions, including logistics constraints and geopolitical risks, affect raw material availability and timely product delivery.

Graphite Electrode Rod Market Segmentation

- •By Type

- ◦Ultra High Power (UHP)

- ◦High Power (HP)

- ◦Regular Power (RP)

- •By Application

- ◦Steel Manufacturing

- ◦Foundry

- ◦Automotive

- ◦Construction

- ◦Others

- •By Manufacturing Process

- ◦Breathing Process

- ◦Extrusion Process

- ◦Isostatic Pressing Process

The Road Ahead: Graphite Electrode Rod

- •The graphite electrode rod industry in the United States is poised for transformational growth driven by technological innovation, sustainability imperatives, and expanding electric arc furnace steel production. Strategic investments in automation, advanced materials, and digital supply chain integration will redefine operational efficiencies and competitive dynamics.

- •Long-term industry impact will be shaped by the convergence of environmental regulations, circular economy practices, and evolving market demands, positioning the market as a critical enabler of sustainable and efficient metallurgical manufacturing over the next decade.

Regional Outlook

The Midwest currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, West Coast is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Northeast

- Southwest

- The South

- The Midwest

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.85 Billion |

| Forecast Year Market Size | USD 3.97 Billion |

| CAGR | 7.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.9% |

| Regions Covered | Northeast, Southwest, The South, The Midwest |

| Key Companies | GrafTech International Holdings Inc. (United States), Tokai Carbon Co., Ltd. (Japan), SGL Carbon SE (Germany), HEG Limited (India), Showa Denko K.K. (Japan), National Carbon Company (United States), Mersen Group (France), SEC Carbon Limited (India), Sinosteel Corporation (China), SGL Carbon Fibers LLC (United States) |

Graphite Electrode Rod Market - United States Industry Size & Growth Analysis 2020-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.